Goods and Services Tax (GST) introduced to the Indian economy to bring a new regime of business compliance by subsuming most of the indirect taxes such as excise, VAT, service tax etc. Though, the concept of Goods and Service Tax (GST) taxation regime is basically based on trust, wherein the registered taxable person is required to determine his tax liability and self- assess his returns. In order to ensure compliance under GST law various measure has been taken by the government and GST audit is one of them.

Audit under GST law signifies examination of books and accounts of the registered taxable person to vouch for the correctness of information furnished, input tax credit availed, refund claimed and tax liability discharged. GST Audit is an analysis of the compliance of a registered person with the provisions contained in the GST Act. The word ‘audit’ is defined under section 2(13) CGST Act, 2017.

GST Audit Applicability and threshold limit therein

Every taxable person registered under GST with a *turnover exceeding the prescribed limit [the turnover limit is above Rs 2 crore as per the latest GST Rules] during a financial year is required to get his accounts audited by a CA (Chartered Accountant) or a CMA (Cost & Management Accountant). The GST Audit limit 2 crore has been set by the government, it means if a taxpayer having a turnover exceeding Rs. 2 crore in a financial, it will create an obligation for compulsory audit under GST . The registered person shall electronically file:

- An annual return (by using GSTR 9B Form) together with the reconciliation statement. Both of them is required to be filed by 31st December of the next Financial Year.

- The audited account statement and the reconciliation statement, reconciling the value of supplies stated in the return furnished for the financial year with the audited annual financial statement,

- A copy of audited annual accounts duly certified

- Any other particulars as may be prescribed.

* turnover includes exports and value of all exempt supplies of the business registered under the same PAN, on all India basis.

Every taxable person registered under GST shall maintain his accounts to show the correct value in regards to:

- Manufacture or production of goods

- Outward supply of goods/services or both

- Inward supply of goods/services or both

- Input tax credit (ITC) availed

- Stock of goods

- Output tax payable and paid

There are three different types of audit under GST:

An audit by Registered Dealer

Every taxable person registered under GST with a turnover exceeding Rs 2 crore during a financial year is required to get his accounts audited by a CA (Chartered Accountant) or a CMA (Cost & Management Accountant).

An audit by Tax Authorities

General Audit:

The Commissioner or any officer authorized by him may conduct an audit of a registered person under the GST law. However, the manner and the of the audit will be prescribed later.

- A 15 days notice is required to conduct an audit

- The completion of the audit shall be within 3 months from the date of commencement of the audit.

- The Commissioner of CGST/SGST can extend the above time limit by a further six months.

Special Audit:

The assistant commissioner of CGST/SGST may conduct a special audit under GST, considering the nature and complexity involved and interest of the revenue. A Special audit can be initiated during any stage of inquiry/ scrutiny/ investigation, if the assistant commissioner is of the opinion that the value of the supplies has been incorrectly declared or wrongly/excess input tax credit has been availed.

Obligations of the Auditee

The registered taxable person will be required:

- To provide information and proper assistance for timely completion of the audit.

- To provide all the requisite documents (books of accounts) and provide a necessary facility required.

Findings of Audit

One the audit is concluded, the officer is required to inform the auditee within 30 days of:

- the findings of the audit,

- their reasons, and

- the rights and obligations of the auditee

If the audit detects any sum unpaid/short paid or wrongly refunded or wrongly an ailment of input tax credit, then demand and recovery actions will be initiated.

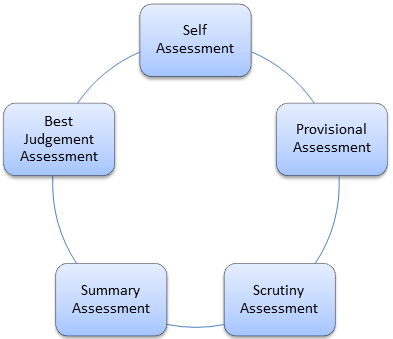

Assessments under GST

In GST law, Assessment implies determination of tax liability. Assessment under GST law has been divided into 5 categories

Self Assessment

Every taxable person registered under GST shall assess his own the taxes liability and file a GST return for each tax period accordingly. This process is termed as self-assessment.

Provisional Assessment

Where a registered person is unable to determine the value of supplies made by him or rate of tax, such registered taxpayer can request the proper officer to pass an order for provisional assessment. The proper officer after considering the fact produced by the registered person can allow him to pay tax on a provisional basis on the value or rate specified.

Scrutiny Assessment

An assessing officer under the CGST/SGST can scrutinize the return filed by the registered taxable person in order to verify its correctness. The assessing officer may enquire explanations from the assessee on any discrepancies noticed in the returns.

Summary Assessment

A summary Assessment is done when the assessing officer has some reasonable grounds to believe that any delay in showing a tax liability can be prejudicial to the interest of the revenue. In order to safeguard the interest of the revenue, the assessing officer can pass the summary assessment with the prior approval of the additional commissioner/joint commissioner.

Best Judgement Assessment

- Assessment of non-filers of returns

Where a taxable person registered under GST fails to file his GST return even after getting a notice from the department, then the proper officer will assess the tax liability of the assessee (defaulter) to the best of his judgment using the relevant available material.

- Assessment of unregistered persons

Where a taxable person who is liable to be registered under the GST law but fails to obtain registration, can result in Best Judgement Assessment. The assessing officer will assess the tax liability of such unregistered persons to the best of his judgement. Such taxable person will receive an SCN notice (show cause notice) and an opportunity of being heard will be given as well.

Demand and Recovery

The demand and recovery provisions become enable when a registered taxable person fails to pay the tax correctly or has not paid tax at all or availed incorrect refund or excess/wrongly Input Tax Credit has been claimed.

The proper officer under the CGST/SGST shall issue a show cause notice along with a demand order for payment of tax, interest and penalty in case of any fraud.

- Demands can arise in the following cases:

- Short Paid, Not paid or wrongly refunded

- Tax collected but not paid to the Central or a State Government

- CGST/SGST paid when IGST was payable or vice versa.

If demand is not paid by the person with the default, the GST department starts recovery proceedings.

Author Bio

For GST audit turnover limit is Rs.2 crores for the financial year. Since GST was implemented from 1st July 2017, whether turnover should considered from April 2017 or July 2017.

Pl explain that which Authority, Central or state dept will conduct audit