Aditya Singhania

This edition brings to apprise with the decisions taken in the 43rd GST Council Meeting held via video conferencing on 28th May, 2021 after a gap of 7 months. The meeting is attended by the 5 new debut entries of 4 new Finance Ministers of Assam, Bihar (Shri Tarkishor Prasad succeeding Shri Sushil Modi), Kerala (Shri KN Balagopal replacing Shri TM Thomas Issac) and Tamil Nadu while 1 as Chief Minister of Puducherry.

EXTENSION REGARDING EXEMPTION FROM GST ON COVID RELIEF MATERIALS

With the second wave of the ongoing pandemic, Government of India has taken remarkable steps on the war footing basis to make the life-saving materials available in the country from across the globe with the continuous support of all the Ministries and their respective departments and the Corporate houses, Charitable Organisation, NGOs, etc.

Unlike the first wave where even the basic materials were not available like masks, sanitizers, PPE kits, etc., in the current second wave India is equipped with all these, however, with the requirement of life saving materials, adequate and timely steps have been taken to import these materials like oxygen cylinders, oxygen concentrators, vaccines, etc.

From the perspective of taxation, exemptions from taxation have been given by the CBIC from Customs duty, Health Cess and IGST on many such items. Few notifications have been regarding the exemption which has been dealt below along-with the procedural requirement. It is important to note that exemptions have been given on import of only those items whose availability are not in adequate quantity in India, therefore, one may find masks, sanitizers, PPE kits, oximeter, thermometer, Test kit, etc. not been exempted from these taxes.

Customs duty and health cess exemption

Notification No. 27/2021–Customs New Delhi, the 20th April, 2021: The notification exempts Customs duty &/or Health Cess and is applicable till 31st October, 2021. The same is applicable on following goods:

- Remdesivir Active Pharmaceutical Ingredients;

- Beta Cyclodextrin (SBEBCD) used in manufacture of Remdesivir, subject to the condition that the importer follows the procedure set out in the Customs (Import of Goods at Concessional Rate of Duty) Rules, 2017;

- Injection Remdesivir.

Notification No. 28/2021–Customs New Delhi, the 24th April, 2021: The notification exempts Customs duty &/or Health Cess and is applicable till 31st July, 2021. The same is applicable on following goods:

| S.No. | Chapter, heading, sub-heading or tariff item | Description |

| (1) | (2) | (3) |

| 1. | 9019 20, 9804 | Oxygen concentrator including flow meter, regulator, connectors and tubings.

[Important Note: For commercial use 9804, For personal use (Courier/FPO) 9804] |

| 2. | 2804 40 | Medical Oxygen |

| 3. | 8421 39 | Vacuum Pressure Swing Absorption (VPSA) and Pressure Swing Absorption (PSA) oxygen plants, Cryogenic oxygen Air Separation Units (ASUs) producing liquid/gaseous oxygen. |

| 4. | 7311 | Oxygen canister. |

| 5. | 9018 | Oxygen filling systems. |

| 6. | 7311 | Oxygen storage tanks |

| 7. | 9018 | Oxygen generator |

| 8. | 7311 | ISO containers for Shipping Oxygen |

| 9. | 7311, 8418 or 8419 | Cryogenic road transport tanks for Oxygen |

| 10. | 7311, 8418 or 8419 | Oxygen cylinders including cryogenic cylinders and tanks |

|

11. |

Any Chapter |

Parts of goods at S.No.1 and 3 to 10 above, used in the manufacture of equipment related to the production, transportation, distribution or storage of Oxygen, subject to the condition that the importer follows the procedure set out in the Customs (Import of Goods at Concessional Rate of Duty) Rules, 2017. |

| 12. | 9019 | Any other device from which oxygen can be generated |

| 13. | 9018 or 9019 | Ventilators, including ventilator with compressors; all accessories and tubings; humidifiers; viral filters (should be able to function as high flow device and come with nasal canula). |

| 14. | 9018 | High flow nasal canula device with all attachments; nasal canula for use with the device. |

| 15. | 6506 99 00 | Helmets for use with non-invasive ventilation. |

| 16. | 9019 | Non-invasive ventilation oronasal masks for ICU ventilators. |

| 17. | 9019 | Non-invasive ventilation nasal masks for ICU ventilators. |

| 18. | 3002 | COVID-19 vaccine. |

IGST Exemption

Notification No. 30/2021-Customs New Delhi, the 1st May, 2021: The notification reduced the rate of tax of IGST to 12% on Oxygen concentrator, imported for personal use and is applicable till 30th June, 2021. It is worthwhile to note that the levy of GST on import for personal use when received as gift is challenged before the Hon’ble High Courts of Delhi as well as Bombay wherein the former has held that the imposition of IGST on the import of oxygen concentrators as gift for personal use is unconstitutional in the case of Gurcharan Singh vs UOI which was challenged primarily on the grounds of Article 14 and 21 of the Constitution of India and in order to bring a parity with the commercial purpose where the Government has already given adhoc exemption.

Ad hoc Exemption Order No. 4/2021-Customs dated 3rd May, 2021 read with Instruction No. 09/2021-Customs dated 3rd May, 2021: The notification exempts IGST and is applicable till 30th June, 2021. It is pertinent to note that the exemption order shall apply to all the such consignments pending clearance from Customs as on date of issue of order, i.e., the 3rd May, 2021.

The same is applicable on goods covered under the said mentioned below subject to the conditions of approval from Nodal Authority appointed in States and its usage:

- Notification No. 27/2021-Customs, dated the 20th April, 2021

- Notification No. 28/2021-Customs, dated the 24th April, 2021

Conditions:

- The said goods are imported free of cost for the purpose of Covid relief by a State Government or, any entity, relief agency or statutory body, authorised in this regard by any State Government.

- The said goods are received from abroad for free distribution in India for the purpose of Covid relief.

- Before clearance of the goods, the importer produces to the Deputy or Assistant Commissioner of Customs, as the case may be, a certificate from a nodal authority, appointed by a State Government, that the imported goods are meant for free distribution for Covid relief, by the State Government, or the entity, relief agency or statutory body, as specified in such certificate.

- The importer produces before the Deputy or Assistant Commissioner of Customs, as the case may be, at the port of import within a period of six months from the date of importation, or within such extended period not exceeding nine months from the said date as that Deputy or Assistant Commissioner of Customs may allow, a statement containing details of goods distributed free of cost duly certified by the said nodal authority of the State Government.

Exemption from IGST is not available if the Covid relief materials are not imported free of cost

In this regard, it is significant to note that Shri Tarun Bajaj, Secretary, Ministry of Finance vide F No. CBIC – 190354/2/2021-TO(TRU-I)-CBEC(Part-I) dated 3rd May, 2021 has communicated to Chief Secretary stating that exemption from IGST has been given to any entity or charitable organization for free distribution anywhere in India which has been donated/received free of cost from outside India. Further, the same thing has been reiterated by the CBIC vide FAQ last updated on 7th May, 2021 that Condition No. 1 of Annexure to the said Order states that, the said goods are imported free of cost for the purpose of Covid relief by a State Government or, any entity, relief agency or statutory body, authorised in this regard by any State Government. Thus, it is clear that the adhoc exemption order applies only where the importer gets goods free of cost for free distribution. Other instances are not covered by the exemption order. It may be mentioned that in case any corporate buys it and even gives it for free, such exemption will not be available. Hence, the intent of the Government appears not to grant exemption from IGST where the Covid relief materials are bought and then given for free.

In this regard, it is worthwhile to note that the same has been challenged before Hon’ble Rajasthan High Court on the grounds that the end-use in both the cases remains the same i.e. used for free distribution.

Any ‘relief agency’ authorised by a State can make free distribution of goods so imported anywhere in India.

Exemption order only envisages that relief agency should have been authorised by a State and should have obtained a certificate to this effect. Therefore, even if one State Nodal Agency authorize the relief agency and issue the certificate for compliance of Condition No. 3 of the Annexure to the said Order, the same can be distributed across India.

Specified format for issuing certificate recommending exemption to a relief agency

A format for the said authorization for import is placed on CBIC’s website, under Customs Instruction 9/2021-Customs dated 3rd May, 2021. This format is for facilitation purpose. Certificate in any format containing information as mentioned in format at the above link shall be accepted by Customs. In this regard, few states have reiterated the same format and displayed at their respective State Commercial Tax website like Gujarat. Besides few states have also come up with the online feature filing in the same format like Haryana.

Procedure for certification of the statement containing details of such imported goods distributed free of cost, both if distributed within the state whose nodal authority authorising the importing entity/ relief agency, and if distributed in other states

Condition No. 4 of the Annexure to the said Order requires that a statement containing details of goods distributed free of cost, duly certified by the said nodal authority of the State Government, is to be produced by the importer before the specified Customs officer at the port of importation. The certification of statement shall be done by the nodal authority that authorises the relief agency

and issues certificate to relief agency recommending exemption under the adhoc order. There is no prescribed procedure for certification of statement and the States/ State nodal authorities are at liberty to devise their own suitable mechanism as deemed fit, for certification of statement.

Nodal authority will issue the certificate to the entity who will submit the same before the concerned customs authority at the time of clearance of goods.

Condition No. 3 of Annexure to said Order may be referred to and as mentioned therein, the State nodal authority will authorize the importing entity, and the importer will produce the said authorization before Customs at time of clearance for availing the exemption.

Certificate could be issued covering multiple imports by a relief agency

Although a certificate is required to be produced by an importer to Customs at the time of clearance of each consignment, a separate, consignment-wise certificate is not necessary. A certificate issued to a relief agency may cover goods imported under multiple consignments. The certificate should specify port-wise anticipated import by relief agency, in the format as mentioned at S. No. 3 above.

Saving grace announced by few states by reimbursing the GST

It may be mentioned that in case any corporate buys the Covid relief materials and distributes it for free, such exemption will not be available. Hence, the intent of the Government appears not to grant exemption from IGST where the Covid relief materials are bought and then given for free.

However, as most of the corporate houses are importing such materials on procurement, hence, it takes a shape of cost to the organization since the input tax credit of IGST paid on import (CGST, SGST or IGST paid on domestic purchase) is not available on account of the blocked credits envisaged under section 17(5). Further, if such materials are bought from domestic market, there is still neither any exemption nor availability of input tax credit is admissible.

Certainly, as the input tax credit is not allowed on free supplies, however, there is an incentive scheme rolled out by States of Gujarat & Haryana wherein the Department of Health & Family Affairs proposed to reimburse the GST component subject to the condition that the donation of Covid relief materials is given to the States, which may become as an add on at the top of CSR compliance. The place where Haryana gives an add on benefit is that it envisages to reimburse both CGST & SGST as well as IGST component while the Gujarat has proposed to reimburse only IGST on import of such materials.

Government of Gujarat, vide Resolution released by Ministry of Finance, Gujarat vide No. GST-102021-Tax-1-GST Cell dated 1st May, 2021 valid till 31st July, 2021 has announced the incentive scheme as mentioned below:

(i) By way of reimbursing / giving grant in aid the IGST leviable under the Customs Tariff Act, 1975 already paid by the recipient on such imported material; or

(ii) By way of upfront payment of applicable IGST leviable under the Customs Tariff Act, 1975 on such imported material.

With the following conditions which aims to strengthen the Covid relief infrastructure of the State of Gujarat:

1) Such imported material shall be donated free of cost to the Government of Gujarat, hospitals run by state government, hospitals run by local authority or any Hospital/Institution permitted by state government to receive such material through Commissioner of Health, Government of Gujarat.

2) ln case where permission is granted to hospital/institution not owned by state government or local authority, such imported material cannot be sold or transferred by them without prior permission of the state government.

Besides, Government of Haryana vide Notification No. 28/19/2021-5B&C dated 17th May, 2021 has also announced similar scheme having validity till 30th June, 2021.

However, the department does need to ensure that the taxpayer does not avail the input tax credit of the same in the books as well as claims reimbursement from the State.

The tenders by the States for procuring the Covid relief materials from the vendors certainly is the procedure to arrange for the necessary infrastructure. However, with such an incentive scheme, the State is in a position to strengthen the Covid relief infrastructure of the State of Gujarat & Haryana by way of getting these materials as donations from the Corporates, NGOs, etc. merely at the cost of ‘amount of tax to be reimbursed’ to the donors. In similar lines, representation should also be made to other State Governments to come up with identical incentive scheme. The proposal to reimburse the GST component is by the Department of Health & Family Affairs of the Gujarat Government, however, in case of Haryana, the same shall be reimbursed by the Excise and Taxation Department. It’s a high time, corporates, Charitable Organizations, NGOs, etc. should come forward to take an extra leap to serve the society in larger interest of the humanity.

Outcome of 43rd GST Council Meeting:

- As per the reports of PTI, Rajasthan, Punjab, Chhattisgarh, Tamil Nadu, Maharashtra, Jharkhand, Kerala and West Bengal devised a joint strategy to press for a zero-tax rate on COVID essentials. However, basis the recommendation of the Law Committee and Fitment Committee, the proposal for exemption has not been accepted as it would create a far-reaching impact on consumers since majority of the vaccines are procured by the Centre & States and given free of cost and the other materials are procured by the Government or Private Hospitals. As regards individual items, it was decided to constitute a Group of Ministers (GoM) to go into the need for further relief to COVID-19 related individual items immediately. The GOM shall give its report by 08.06.2021.

- Further, regarding the issue of exemption from IGST, it has been decided to give the exemption even in cases where the Covid relief materials (such as medical oxygen, oxygen concentrators and other oxygen storage and transportation equipment, certain diagnostic markers test kits and COVID-19 vaccines, etc.) are imported on payment basis, for donating to the government or on recommendation of state authority to any relief agency. However, apart from exemption which would be applicable prospectively, the decision to reimburse the GST already paid on Covid relief materials used for free distribution for the period before the said exemption is applicable would have brough the parity as the objective remains the same. With this decision of outright exemption, the only difference which appears is that the Reimbursement Schemes announced by the Haryana & Gujarat requires payment of tax first and then claiming of reimbursement subject to the condition that the same is donated to the State Government. It must be noted that exemption is given only in case of import while the Haryana Reimbursement Scheme also provides reimbursement of GST paid on local procurement.

- Further, the medicine Amphotericin B required for treatment of Black Fungus has now been included in the exemption list.

- Besides, all the aforesaid exemptions have been extended till 31st August, 2021.

- To support the Lympahtic Filarisis (an endemic) elimination programme being conducted in collaboration with WHO, the GST rate on Diethylcarbamazine (DEC) tablets has been recommended for reduction to 5% (from 12%).

CLARIFICATION ON CERTAIN OTHER GOODS

Certain clarifications/clarificatory amendments have been recommended in relation to GST rates. Major ones are, –

a. Leviability of IGST on repair value of goods re-imported after repairs

b. GST rate of 12% to apply on parts of sprinklers/ drip irrigation systems falling under tariff heading 8424 (nozzle/laterals) to apply even if these goods are sold separately.

CLARIFICATION ON EXEMPTIONS RELATING TO EDUCATION SECTOR

- Services supplied to an educational institution including anganwadi (which provide pre-school education also), by way of serving of food including mid- day meals under any midday meals scheme, sponsored by Government is exempt from levy of GST irrespective of funding of such supplies from government grants or corporate donations.

- Services provided by way of examination including entrance examination, where fee is charged for such examinations, by National Board of Examination (NBE), or similar Central or State Educational Boards, and input services relating thereto are exempt from GST.

CLARIFICATION ON AVAILABILITY OF ITC TO THE LAND OWNER DEVELOPERS

- As developer promoter is required to pay GST on flats provided to land owners w.e.f. 1st April, 2019 at the time of providing Completion Certificate, due to which landowner was unable to avail and utilize the input tax credit as consideration from supply of flats were received before issuance of Completion Certificate. Hence, it has been recommended to make appropriate changes in the relevant notification for an explicit provision to make it clear that land owner promoters could utilize credit of GST charged to them by developer promoters in respect of such apartments that are subsequently sold by the land promotor and on which GST is paid. The developer promotor shall be allowed to pay GST relating to such apartments any time before or at the time of issuance of completion certificate.

RATIONALIZATION IN GST IN RESPECT OF MRO UNITS OF SHIPS/VESSELS

Dispensation as provided to MRO units of aviation sector to MRO units of ships/vessels so as to provide level playing field to domestic shipping MROs vis a vis foreign MROs and accordingly,

(a) GST on MRO services in respect of ships/vessels shall be reduced to 5% (from 18%).

(b) PoS of B2B supply of MRO Services in respect of ships/ vessels would be location of recipient of service.

The approach will align in order to align the tax rates with the competing nations like Singapore, United Arab Emirates (UAE) and Sri Lanka in the sector. The change in Place of Supply rules will incentivise foreign vessels to opt for tax free MRO services in the country as it often happens that the ships generally go in for MRO service during the intervening time between arrival and departure with cargo. The approach to reduce tax rate will also be a saving for companies engaged in other shipping related services like transportation, etc. which avails MRO services and where there is a huge accumulation of input tax credit. Further, it is important to note that the reduction from 18% t0 5% is without any restriction on input tax credit. It is also worthwhile to note that a similar tax reduction was done by the GST Council for the MRO in aviation sector last year.

CLARIFICATION REGARDING EXEMPTION FROM GST ON SERVICES OF MILLING BY THE FLOUR MILLS UNDER PBLIC DISTRIBUTION SYSTEM

A lot has been debated on this when the DGGI took up the issue of leviability of GST on the flour mill for crushing of wheat into fortified atta for public distribution system. The question was on availability of exemption under Sl. No. 3A of the exemption notification. Besides, as an alternative at best GST could be charged @5% treating the same as job work to the registered person against demand for 18% GST. The question does arose if the person having TDS registration can be considered as registered person for this purpose. All these issues have been clarified by stating that the supply of service by way of milling of wheat/paddy into flour (fortified with minerals etc. by millers or otherwise)/rice to Government/ local authority etc. for distribution of such flour or rice under PDS is exempt from GST if the value of goods in such composite supply does not exceed 25%. Otherwise, such services would attract GST at the rate of 5% if supplied to any person registered in GST, including a person registered for payment of TDS.

CLARIICATION ON EXEMPTIONS FROM GST ON CONSTRUCTION SECTOR

- GST is payable on annuity payments received as deferred payment for construction of road. Benefit of the exemption is for such annuities which are paid for the service by way of access to a road or a bridge.

- Services supplied to a Government Entity by way of construction of a rope-way attract GST at the rate of 18%.

EXEMPTION FROM GST ON GUARANTEE OF LOANS BY GOVERNMENT

Services supplied by Government to its undertaking/PSU by way of guaranteeing loans taken by such entity from banks and financial institutions is exempt from GST. In other words, it can be stated that Corporate Guarantee is taxable under GST.

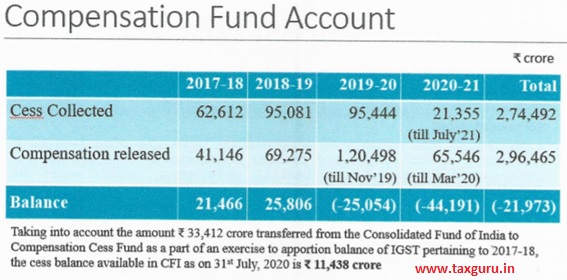

COMPENSATION CESS IN THE MIDST OF PANDEMIC

Compensation Cess is compensation to the States for the loss of revenue arising on account of implementation of the goods and services tax in pursuance of the provisions of the Constitution (One Hundred and First Amendment) Act, 2016. In order to compensate any loss arising due to transition has been kept at 14% per annum as nominal growth rate of revenue subsumed for a State, for which FY ending March 31, 2016 has been kept as the base year. The base year revenue for a State shall be net of refunds, with respect to the specified taxes which are subsumed into GST. It was envisaged to pay on provisional basis to the States at the end of every 2 months period, and shall be finally calculated for every FY after the receipt of final revenue figures, as audited by the Comptroller and Auditor-General of India. However, it has been observed that the estimated compensation to be given to the States/UTs was surpassing the collection amount due to which there were friction in making payment. During the initial couple of years of GST implementation, collections were sufficient to release payments to States/UTs, however, in FY 2019-20, though the collection were stable as compared to earlier years but the loss from the transition by taking growth rate of 14% from the base year FY 2015-16 was comparatively high. But due to the major hit of pandemic, there was a significant cut in collection of such cess while the compensation promised @14% remained constant, due to which GST Council recommended Centre to borrow funds on behalf of the States and UTs under the special window in October, 2020 to meet the shortfall of INR 1,10,208 Crore starting from October 23, 2020. Such an arrangement to borrow has been made as there was no express provision in the said Act for the Centre to bear the liability of making good the shortfall and at the top of it the fact that borrowing by the Centre would have escalate the borrowing cost for the entire economy. It is worthwhile to note that any payment shall be released from the Compensation Fund collected by levy of such cess or such other amount as may be recommended by the GST Council.

Source: 41st GST Council Meeting Minutes

Press Release dated March 15, 2021 by Ministry of Finance confirms that 100% of the total estimated GST Compensation shortfall of INR 1.10 lakh crore for year 2020-21 has been released by its last 20th weekly installment to all the 23 States and 3 UTs with Legislative Assembly barring the States of Arunachal Pradesh, Manipur, Mizoram, Nagaland and Sikkim where there is no such compensation gap. The total amount has been borrowed at the weighted average rate interest rate of 4.8473%. In addition to the borrowing under special window, Government of India has also granted additional borrowing permission of INR 1,06,830 to 28 States i.e. equivalent to 0.50% of Gross States Domestic Product (GSDP) to the states choosing Option-I to meet GST Compensation shortfall to help them in mobilizing additional financial resources. One of the probable reasons of no such compensation gaps in said 5 States could be that these are majorly consuming States and the application of 14% of growth rate for compensating was merely to maintain uniformity across all the States/UTs.

In order to meet the revenue gap, as against the levy of Compensation Cess for the initial 5 years is now recommended by the 42nd GST Council Meeting to be extended beyond the transition period of five years i.e. beyond June, 2022, for such period as may be required. Certainly, an option is always available to tweak in existing rate of cess on pan masala, aerated waters including caffeinated beverages, tobacco, cigarettes, coal, lignite, peat, motor vehicles excluding old/used once including services given in like goods or leasing of motor vehicles, though subject to maximum rate annexed in the law, which were based on the lines of the tariff that exist under the erstwhile regime. The levy of cess on motor vehicles may not scoop expected cess due to the speedy transition of the consumers into the electric vehicle segment which has been kept free from such cess.

Outcome of 43rd GST Council Meeting:

The Centre has estimated the GST shortfall to states at Rs 2.69 lakh crore. Finance Ministry expects to collect over Rs 1.11 lakh crore through cess on luxury, demerit and sin goods. The remaining Rs 1.58 lakh crore would have to be borrowed to meet the promised compensation. Based on this assumption, it has been estimated that for the period February 2021 to January 2022, the gap between projected revenue and the actual revenue after the release of the compensation would be around Rs 1.6 lakh crore.

APPROVAL OF DECISIONS TAKEN BY GST IMPLEMENTATION COMMITTEE (GIC)

GST Implementation Committee was formed vide F. No. 25/Committees-1/GST Council as per the decision taken in the 14th GST Council meeting held on 18-19th May, 2017 in Srinagar, Jammu & Kashmir. The Committee was formed to ensure smooth roll out of GST as well as facilitate quick administrative decisions required before and after roll out of GST, effective coordination between the Centre and States and amongst states and flagging important issues to the Revenue Secretary and the GST Council. As a part of a 3-tier structure, GIC shall be the Decision-making body at the top tier. It shall take decisions to the extent possible and wherever necessary, place the important issues before the Revenue Secretary/Union Finance Minister/ GST Council for decision. To facilitate this the GST Council Secretariat shall provide support in terms of coordination, documentation and technical input on various issues after collecting the same from the Standing Committee/ Sectoral Group.

Outcome of 43rd GST Council Meeting:

According to one of the Finance Minister of States, GST Council’s federal structure needs to be strengthened and the decision taken by the GIC should not merely inform GST Council and desired for formal approval from the States and in fact some of the decisions already been taken should be approved by the States. In this connection, nothing has been stated in Press Conference & in Press Release.

AMENSTY SCHEME FOR WAIVER OF LATE FEE& CAPPING OF LATE FOR DELAY IN FILING OF GSTR 3B

Section 47 states that any registered person who fails to furnish the returns by due date shall pay a late fee of INR 100 for every day during which the such failures continue subject to a maximum amount of INR 5,000 under each CGST Act and SGST/UTGST Act. From October, 2017 onwards, late fee in excess of INR 25 (in case of NIL return in excess of INR 10) has been waived vide Notification No. 76/2018-Central Tax dated 31st December, 2018 by superseding the erstwhile notifications (NN: 28/2017-CT dated 1-9-2017; NN: 50/2017-CT dated 24-10-2017; NN: 50/2017-CT dated 24-10-2017; NN: 64/2017-CT dated 15-11-2017; NN: 28/2017-CT dated 1-9-2017; NN: 41/2018-CT dated 4-9-2018.

The amnesty scheme of waiver from late fee has been given from time-to-time by Government as listed below:

- Full waiver: Period July, 2017 to September, 2018 if filed between the period from 22nd December, 2018 to 31st March, 2019 – Notification No. 76/2018-Central Tax dated 31st December, 2018

- Partial waiver in excess of INR 500 [250 +250]: Period July, 2017 to January, 2020 if filed between the period from 1st July, 2020 to 30th September, 2020 – Notification No. 53/2020-Central Tax dated 24th June, 2020

- Partial waiver in excess of INR 500 [250 +250]: Period February, 2020 to July, 2020 if filed within the specified dates – Notification No. 57/2020-Central Tax dated 30th June, 2020; Notification No. 52/2020-Central Tax dated 24th June, 2020; Notification No. 32/2020-Central Tax dated 3rd April, 2020

Outcome of 43rd GST Council Meeting:

Capping of Late Fee: The capping of late fee from INR 5,000 under each Acts is now recommended to cap late fee up to:

- INR 500 (250 + 250) – For Nil returns

- INR 2,000 (1000 + 1000) – For taxpayers having aggregate turnover in preceding FY upto INR 1.5 crores

- INR 5,000 (2500 + 2500) – For taxpayers having aggregate turnover in preceding FY between INR 1.5 crores to INR 5 crores

- INR 10,000 (5000 + 5000) – For taxpayers having aggregate turnover in preceding FY more than INR 5 crores

Waiver of late fee Amnesty Scheme: Relief has been provided to the taxpayers, from late fee for non-furnishing FORM GSTR-3B for the tax periods from July, 2017 to April, 2021 has been reduced / waived as under, if GSTR-3B returns for these tax periods are furnished between 01.06.2021 to 31.08.2021.: –

- late fee capped to a maximum of Rs 500/- (Rs. 250/- each for CGST & SGST) per return for taxpayers, who did not have any tax liability for the said tax periods;

- late fee capped to a maximum of Rs 1000/- (Rs. 500/- each for CGST & SGST) per return for other taxpayers;

The issue of refund regarding taxpayers who have already paid late fees for filing late fee continues to exist.

AMENSTY SCHEME FOR WAIVER OF LATE FEE & CAPPING OF LATE FEE FOR DELAY IN FILING OF GSTR 1

Section 47 states that any registered person who fails to furnish the returns by due date shall pay a late fee of INR 100 for every day during which the such failures continue subject to a maximum amount of INR 5,000 under each CGST Act and SGST/UTGST Act. Late fee in excess of INR 25 (in case of NIL return in excess of INR 10) has been waived vide Notification No. 4/2018-Central Tax dated 23rd January, 2018.

The amnesty scheme of waiver from late fee has been given from time-to-time by Government as listed below:

- Full waiver: Period July, 2017 to September, 2018 if filed between the period from 22nd December, 2018 to 31st March, 2019 – Notification No. 75/2018-Central Tax dated 31st December, 2018

- Full waiver: Period July, 2017 to November, 2019 if filed between the period from 19th December, 2019 to 10th January, 2020 extended till 17th January, 2020. – Notification No. 74/2019-Central Tax dated 26thDecember, 2019.

- Full waiver: Period March, 2020 to June, 2020 if filed within the specified dates – Notification No. 53/2020-Central Tax dated 24th June, 2020; Notification No. 33/2020-Central Tax dated 3rd April, 2020.

Outcome of 43rd GST Council Meeting:

Capping of Late Fee: The capping of late fee from INR 5,000 under each Acts is now recommended to cap late fee up to:

- INR 500 (250 + 250) – For Nil returns

- INR 2,000 (1000 + 1000) – For taxpayers having aggregate turnover in preceding FY upto INR 1.5 crores

- INR 5,000 (2500 + 2500) – For taxpayers having aggregate turnover in preceding FY between INR 1.5 crores to INR 5 crores

- INR 10,000 (5000 + 5000) – For taxpayers having aggregate turnover in preceding FY more than INR 5 crores

CAPPING OF LATE FOR DELAY IN FILING OF GSTR 4

The late fee for delay in furnishing of FORM GSTR-4 by composition taxpayers to be capped to:

- Rs 500 (Rs 250 CGST + Rs 250 SGST) per return, if tax liability is nil in the return

- Rs 2000 (Rs 1000 CGST + Rs 1000 SGST) per return for others.

REDUCTION & CAPPING OF LATE FOR DELAY IN FILING OF GSTR 7

Late fee payable for delayed furnishing of FORM GSTR-7 to be reduced to Rs.50/- per day (Rs. 25 CGST + Rs 25 SGST) and to be capped to a maximum of Rs 2000/- (Rs. 1,000 CGST + Rs 1,000 SGST) per return.

ANNUAL RETURN GSTR 9 OPTIONAL FOR TAXPAYERS UPTO INR 2 CRORES FOR FY 2020-21& SIMPLIFICATION OF ANNUAL RETURN

As per section 44(1), every registered person, other than an Input Service Distributor, a person paying tax under section 51 or section 52, a casual taxable person and a non-resident taxable person, shall furnish an annual return for every financial year electronically in GSTR 9 on or before the 31st December following the end of such financial year.

GST Annual Return for preceding FY 2019-20

Turnover upto INR 2 crore: GSTR 9 is Optional vide Notification No. 77/2020-Central Tax dated 15.10.2020

Turnover above INR 2 crore: Mandatory

Outcome of 43rd GST Council Meeting:

GST Annual Return for preceding FY 2020-21

Turnover upto INR 2 crore: GSTR 9 is Optional

Turnover above INR 2 crore: Mandatory

Amendments in section 35 and 44 of CGST Act made through Finance Act, 2021 to be notified. This would ease the compliance requirement in furnishing reconciliation statement in FORM GSTR-9C, as taxpayers would be able to self-certify the reconciliation statement, instead of getting it certified by chartered accountants. This change will apply for Annual Return for FY 2020-21.

RECONCILIATION STATEMENT IN GSTR 9C OPTIONAL FOR TAXPAYERS UPTO INR 5 CRORES FOR FY 2020-21

It is important to note that recently section 35(5) has been omitted vide Finance Act, 2021 along-with the amendment in section 44 (though the same has not yet been enforced and notified) which is reproduced here-in-below for ease-of-reference:

“44. Every registered person, other than an Input Service Distributor, a person paying tax under section 51 or section 52, a casual taxable person and a non-resident taxable person shall furnish an annual return which may include a self-certified reconciliation statement, reconciling the value of supplies declared in the return furnished for the financial year, with the audited annual financial statement for every financial year electronically, within such time and in such form and in such manner as may be prescribed:

Provided that the Commissioner may, on the recommendations of the Council, by notification, exempt any class of registered persons from filing annual return under this section:

Provided further that nothing contained in this section shall apply to any department of the Central Government or a State Government or a local authority, whose books of account are subject to audit by the Comptroller and Auditor General of India or an auditor appointed for auditing the accounts of local authorities under any law for the time being in force.”.

Section 35(5) of CGST Act, 2017 stipulates that every registered person whose turnover during a FY exceeds the prescribed limit shall get his accounts audited by a CA or a CWA and shall submit a copy of the audited annual accounts, the reconciliation statement under section 44(2) and such other documents in such form and manner as may be prescribed. However, it shall not apply to any department of the Central Government or a State Government or a local authority, whose books of account are subject to audit by the CAG or an auditor appointed for auditing the accounts of local authorities under any law for the time being in force. The aforesaid section 35(5) is being proposed to be omitted so as to remove the mandatory requirement of getting annual accounts audited and reconciliation statement submitted by specified professional.

GST Audit for preceding FY 2019-20

Turnover ranging between INR 2 -5 crore: GSTR 9C is Optional vide Notification No. 79/2020-Central Tax dated 15.10.2020 by amending Notification No. 16/2020-Central Tax dated 23.03.2020

Turnover above INR 5 crore: Mandatory vide Notification No. 79/2020-Central Tax dated 15.10.2020 by amending Notification No. 16/2020-Central Tax dated 23.03.2020

Outcome of 43rd GST Council Meeting:

GST Audit for preceding FY 2020-21

Turnover ranging between INR 2 -5 crore: GSTR 9C has been made optional

Turnover above INR 5 crore: Mandatory

Amendments in section 35 and 44 of CGST Act made through Finance Act, 2021 to be notified. This would ease the compliance requirement in furnishing reconciliation statement in FORM GSTR-9C, as taxpayers would be able to self-certify the reconciliation statement, instead of getting it certified by chartered accountants. This change will apply for Annual Return for FY 2020-21.The reconciliation statement in FORM GSTR-9C for the FY 2020-21 will be required to be filed by taxpayers with annual aggregate turnover above Rs 5 Crore.

RELAXATIONS IN TIME LIMITS FOR COMPLETION OR COMPLIANCE UNDER THE GST LAW – Notification No. 14/2021-Central Tax dated 1ST MAY, 2021

- Where, any time limit for completion or compliance of any action,

- by any authority or by any person,

- has been specified in, or prescribed or notified under the GST Act,

- which falls during the period from the 15th April, 2021 to 30th May, 2021, and

- where completion or compliance of such action has not been made within such time, then,

- the time limit for completion or compliance of such action, shall be extended upto the 31st May, 2021,

- INCLUDING for the purposes of –

(a)

- completion of any proceeding or

- passing of any order or

- issuance of any notice, intimation, notification, sanction or approval or

- such other action, by whatever name called,

by any authority, commission or tribunal, by whatever name called, under the provisions of the Acts stated above; or

(b)

- filing of any appeal, reply or application or

- furnishing of any report, document, return, statement or

- such other record, by whatever name called,

- under the provisions of the Acts stated above;

Non-applicability of aforesaid notification in certain cases

Such extension of time shall not be applicable for the compliances of the provisions of the said Act and Corresponding Rules, as mentioned below –

| Section No. | Corresponding rules | Provisions related to |

| Chapter IV | Chapter IV of CGST Rules, 2017, rules ranging from 27 to 35. | Time and Value of Supply |

| Section 10(3) | – | Lapse of Composition scheme

due to crossing of Limits |

| Section 25 | Rule No. 8, 14, 9, 10, 10A, 11, 12, 16, 17, 18, 24, 25, 26 | Procedure for Registration |

| Section 27 | Rule No. 13 & 15 | Provisions relating to Registration for Casual taxable person & Non-resident Taxable person. |

| Section 31 | Rule No. 46, 46A, 47, 49, 50, 51, 52, 53 | Tax Invoice |

| Section 37 | Rule No. 59, 78, 79 | Furnishing Details of Outward supplies |

| Section 39, except those covered u/s 39(3), (4) & (5). | Rule 61, 62 | Furnishing of returns. |

| Section 47 | – | Levy of Late fee on Failure to

Furnish return u/s 37, 38, 39 & 45. |

| Section 50 | – | Interest on delayed payment of Tax |

| Section 68, to the extent E-way Bill is considered. | – | Inspection of Goods in movement. |

| Section 69 | – | Power to Arrest |

| Section 90 | – | Liability of partners of firm to pay tax. |

| Section 122 | – | Penalty for certain offences |

| Section 129 | – | Detention, seizure and release of Goods and Conveyances in transit. |

- Notification comes from retrospective effect i.e. 15-4-2021

Outcome of 43rd GST Council Meeting:

Time limit for completion of various actions, by any authority or by any person, under the GST Act, which falls during the period from 15th April, 2021 to 29th June, 2021, to be extended upto 30th June, 2021, subject to some exceptions.

Further, it has been clarified that wherever the timelines for actions have been extended by the Hon’ble Supreme Court in its Suo Moto Order, the same would apply.

RELAXATION IN THE INTEREST RATE AND LATE FEES – NOTIFICATION NO. 8/2021-CENTRAL TAX & NOTIFICATION NO. 9/2021-CENTRAL TAX DATED 1ST MAY, 2021 RESPECTIVELY

| Aggregate Turnover | Tax Period | Interest Rate Relaxation from due date | Late Fee waiver from due date | ||

| For 1st 15 days | For next 15 days | Thereafter | |||

| More than INR 5 crores | March & April, 2021 | 9% | 18% | 18% | 15 days |

| Upto INR 5 Crores | March & April, 2021 | Nil | 9% | 18% | 30 days |

| Upto INR 5 Crores – Quarterly filers | March & April, 2021 | Nil | 9% | 18% | 30 days

[For the period January-March, 2021] |

| Return under Composition Scheme | Quarter ending March, 2021 | Nil | 9% | 18% | – |

- The NN 8/2021-CT comes from retrospective effect i.e. 18-4-2021

- The NN 9/2021-CT comes from retrospective effect i.e. 20-4-2021

Chances of refund arise where the taxpayers have already filed return for the month of March, 2021 till 30th April, 2021 along-with payment of interest and late fee.

Outcome of 43rd GST Council Meeting:

For the month of March, April& May, 2021

| Aggregate Turnover | Tax Period | Interest Rate Relaxation from due date | Late Fee waiver from due date | ||

| For 1st 15 days | For next fewdays | Thereafter | |||

| More than INR 5 crores | March, April& May, 2021 | 9% | 18% | 18% | 15 days |

| Upto INR 5 Crores | March, 2021 | Nil | 9% [For 45 days] | 18% | 60 days |

| April, 2021 | Nil | 9% [For 30 days] | 18% | 45 days | |

| May, 2021 | Nil | 9% [For 15 days] | 18% | 30 days | |

| Upto INR 5 Crores – Quarterly filers | March, 2021 | Nil | 9% [For 45 days] | 18% | 60 days

[For the period January-March, 2021] |

| April, 2021 | Nil | 9% [For 30 days] | 18% | 45 days | |

| May, 2021 | Nil | 9% [For 15 days] | 18% | 30 days | |

| Return under Composition Scheme | Quarter ending March, 2021 | Nil | 9% [For 45 days] | 18% | – |

EXTENSION IN THE DUE DATE FOR FILING GSTR 4 (ANNUAL RETURN FOR PERSON OPTED FOR COMPOSITION SCHEME)– NN 10/2021-CT DATED 1ST MAY, 2021

- From 31st March, 2021 till 31st May, 2021

- Notification comes from retrospective effect i.e. 30-4-2021

Outcome of 43rd GST Council Meeting:

Extension of due date of filing GSTR-4 for FY 2020-21 to 31.07.2021.

EXTENSION IN THE DUE DATE FOR FILING GST ITC-04 – NN 11/2021-CT DATED 1ST MAY, 2021

- In respect of goods dispatched to a job worker or received from a job worker, during the period from 1st January, 2021 to 31st March, 2021.

- Extended till 31st May, 2021

- Notification comes from retrospective effect i.e. 25-4-2021

Outcome of 43rd GST Council Meeting:

Extension of due date of filing ITC-04 for QE March 2021 to 30.06.2021.

EXTENSION IN THE DUE DATE FOR FILING GSTR 1 – NN 12/2021-CT DATED 1ST MAY, 2021

- In respect of April, 2021

- Till 26th May, 2021

Outcome of 43rd GST Council Meeting:

Extension of due date of filing GSTR-1/ IFF for the month of May 2021 by 15 days.

EXTENSION IN COMPLIANCE OF RULE 36(4) – NN 13/2021-CT DATED 1ST MAY, 2021

- Such condition shall apply cumulatively for the period April and May, 2021 and

- The return in FORM GSTR-3B for the tax period May, 2021 shall be furnished with the cumulative adjustment of input tax credit for the said months in accordance with the condition above.

Outcome of 43rd GST Council Meeting:

Cumulative application of rule 36(4) for availing ITC for tax periods April, May and June, 2021 in the return for the period June, 2021.

FACILITY TO FILE RETURNS THROUGH EVC

The facility to file the details of outward supplies under section 37 in FORM GSTR-1 or using invoice furnishing facility (IFF) or GSTR 3B is allowed to be verified through electronic verification code (EVC) vide Notification No. 7/2021-CT dated 27-4-2021 during the period from the 27th April, 2021 to 31st May, 2021 for a registered person registered under the provisions of the Companies Act, 2013.

Outcome of 43rd GST Council Meeting:

It has been decided to allowing filing of returns by companies using Electronic Verification Code (EVC), instead of Digital Signature Certificate (DSC) till 31.08.2021.

SCHEME FROM “QRMP” TO “QRQP” TO ACHIEVE THE OBJECTIVE OF REDUCING COMPLIANCE BURDEN FOR SMES

QRMP Scheme popularly termed as ‘Quarterly Return Filing and Monthly Payment of Taxes’ was introduced to help the taxpayers having aggregate turnover of less than INR 5 crores by doing away with the monthly compliance burden. However, factually, it posed an additional burden of monthly compliance in Invoice Furnishing Facility (IFF) and monthly payment of tax in Challan GST PMT-06 along-with quarterly filing in GSTR 1. With the facility of filing GSTR 1 on quarterly basis, the facility to upload B2B invoices has been provided for those quarterly taxpayers who want to pass on input tax credit (ITC) to their recipients (buyers/customers) in first two months of a quarter. Effectively, IFF is nothing but a minimized form of GSTR 1 with the functionality to upload B2B invoices, Credit & Debit notes. Apart from cut-off date of 13th of next month where invoice uploaded till 13th can only be availed as ITC by the recipient, limitation of INR 50 lakhs value of invoices per month is also posing the problem in availment of credit by the recipient due to which many suppliers does holds the payment of tax to the suppliers under QRMP Scheme. Besides option to pay liability through either Fixed Sum Method or Self-assessment method bring in more confusion in calculating taxes every month and in case the same falls short in case of Fixed Sum Method, levy of interest is the cost to the business of SMEs along-with compliance of GSTR 2A, 2B, rule 36(4), etc.

Outcome of 43rd GST Council Meeting:

It has been stated that the Law Committee will look into the issues and the modalities for the same needs to be worked out.

INVERTED DUTY STRUCTURE CORRECTION IN TEXTILE AND FOOTWEAR SECTOR

The GST rate of inputs in the textile sector is like 5% on cotton yarn, 12% on manmade yarn, 18% of certain chemicals, however, there is a lower rate of GST of 5% on garments and made-up articles of value upto INR 1,000 per piece and 12% on value exceeding 12% on value exceeding INR 1,000. Due to such rate structure, refund on account of inverted tax structure exceeds INR 4,000 crores annually and is expected to grow.

Likewise, in the footwear sector, inputs attract GST rate of 5% to 18% while 12% to 5% for products of value up to INR 1,000 per piece and 18% on value exceeding INR 1,000 per piece leading to annual refund of almost INR 2,000 crores as 2/3rd of the footwear in terms of value of footwear is sold at a retail price upto INR 1,000.

Outcome of 43rd GST Council Meeting:

The same has been deliberation but with no outcome in terms of rationalization.

RETROSPECTIVE EFFECT TO PROVISO TO SECTION 50 OF CGST ACT, 2017 ABOUT INTEREST ON LATE PAYMENT W.R.E.F. 1ST JULY, 2017

It has been decided that the retrospective amendment in section 50 of the CGST Act with effect from 01.07.2017, providing for payment of interest on net cash basis, to be notified at the earliest.

ALIGNMENT OF PROVISION OF GST LAW WITH GSTR 1 & 3B INSTEAD OF GSTR 1, 2 & 3

GST Council recommended amendments in certain provisions of the Act so as to make the present system of GSTR-1/3B return filing as the default return filing system in GST. The step to bring the said alignment, if done on retrospective basis, may dilute many grounds usually taken to defend the stand in disputes arising on denial of ITC under section 16(2), 16(4), etc.

*****

Disclaimer: The views expressed in this article for the for the purpose of awareness and readers must refer the relevant Press Release, Notification, Resolutions, Orders, etc. of the Government before taking any action. The author is not responsible or liable for any loss or damage caused to anyone due to any interpretation, error, omission in this article.

Auahtor Details : Aditya Singhania | Partner, Singhania’s GST Consultancy & Co. | info@singhaniasgstconsultancy.com

Dear Sir,

What about cancelled the registration who are unable to file the returns ? Is there any way to revoke ?

Thanks for the detailed explanations . Can yo explain in the Land owner – developer transaction ? The land owner is getting the flats as against the FSI he transferred to the developer . How does the ITC issue come to the Landowner ?

It is very sorry to note that on going to your site, which is sent by you to my mail ID, some verification is seen introduced. It is clear that we are downloading it from the mail which you sent. Then why a verification. This is making waste of time. Please avoid.

If guarantees issued by govt for PSU are exempted, it means corporate guarantees are taxable. If So how valuation of corporate guarantee will be worked out when no consideration or fee is charged. ?

Sir,

How can we get refund of late fee already paid for 3B returns during July-17 till April 2021.

Is there any waiver of late fee for Annual return filed for FY 19-20 in the 43rd Counsil meeting if so, kindly let us know sir,

Abdul Malik

Abdul, both concerns raised by you is valid.

1. Certainly, amensty scheme by Government for waiver of late fee to non-filers is discriminatory with the taxpayers who filed returns belatedly with late fee. However, let us not discount the fact that there is no waiver from interest, hence, if you have filed with late fee, you are at better advantage compared to taxpayers availing amensty scheme. Further, many taxpayers wouldn’t be in a position to avail ITC of past periods as per section 16(4) timelines to set off against the liabilities (though litigative). Nevertheless, the dispute remains alive and can be brought before the relevant authorities/ forum.

2. Regarding, amnesty scheme for annual return, it should have been ideally given considering the fact that annual returns cannot be filed unless returns of the tax periods of relevant FY is filed. Therefore, amnesty for Annual Return should have been considered where the amensty is considered for GSTR 3B. It appears that the issue would have been just an oversight and may be considered if brought before the authorities.

Regards

THENK YOU SIR

THIS INFORMATION WILL HELP TO ALL

T.A.MURUGESAN