GOVERNMENT OF INDIA

MINISTRY OF FINANCE

(DEPARTMENT OF REVENUE)

Notification No. 68/2017-Customs (N. T.)

New Delhi, the 30th June, 2017

G.S.R.803(E). -In exercise of the powers conferred by section 156 of the Customs Act, 1962 (52 of 1962),and in supersession of the Customs(Import of Goods at Concessional Rate of Duty for Manufacture of Excisable Goods) Rules,2016 except as things done or omitted to be done before such supersession, the Central Government hereby makes the following, namely: –

1. Short title and commencement. –

(1) These rules may be called the Customs (Import of Goods at Concessional Rate of Duty) Rules, 2017.

(2) They shall come into force on the 1st day of July, 2017.

2. Application. –

(1) These rules shall apply to an importer, who intends to avail the benefit of an exemption notification issued under sub-section (1) of section 25 of the Customs Act, 1962 (52 of 1962) and where the benefit of such exemption is dependent upon the use of imported goods covered by that notification for the manufacture of any commodity or provision of output service.

(2) These rules shall apply only in respect of such exemption notifications which provide for the observance of these rules.

3. Definition. –

In these rules, unless the context otherwise requires, –

(a) “Act” means the Customs Act, 1962 (52 of 1962);

(b) “exemption notification” means a notification issued under sub-section (1) of section 25 of the Act;

(c) “information” means the information provided by the manufacturer who intends to avail the benefit of an exemption notification;

(d) “Jurisdictional Custom Officer” means an officer of Customs of a rank equivalent to the rank of Superintendent or an Appraiser exercising jurisdiction over the premises where either the imported goods shall be put to use for manufacture or for rendering output services;

(e) “manufacture” means the processing of raw material or inputs in any manner that results in emergence of a new product having a distinct name, character and use and the term “manufacturer” shall be construed accordingly;

(f) “output service” means supply of service with the use of the imported goods.

4. Information about intent to avail benefit of exemption notification.–

An importer who intends to avail the benefit of an exemption notification shall provide the information to the Deputy Commissioner of Customs or, as the case may be, Assistant Commissioner of Customs having jurisdiction over the premises where the imported goods shall be put to use for manufacture of goods or for rendering output service, the particulars, namely:-

(i) the name and address of the manufacturer;

(ii) the goods produced at his manufacturing facility;

(iii)the nature and description of imported goods used in the manufacture of goods or providing an output service.

5. Procedure to be followed. –

(1) The importer who intends to avail the benefit of an exemption notification shall provide information –

(a) in duplicate, to the Deputy Commissioner of Customs or, as the case may be, Assistant Commissioner of Customs having jurisdiction over the premises where the imported goods shall be put to use for manufacture of goods or for rendering output service, the estimated quantity and value of the goods to be imported, particulars of the exemption notification applicable on such import and the port of import in respect of a particular consignment for a period not exceeding one year; and

(b) in one set, to the Deputy Commissioner of Customs or, as the case may be, Assistant Commissioner of Customs at the Custom Station of importation.

(2) The importer who intends to avail the benefit of an exemption notification shall submit a continuity bond with such surety or security as deemed appropriate by the Deputy Commissioner of Customs or Assistant Commissioner of Customs having jurisdiction over the premises where the imported goods shall be put to use for manufacture of goods or for rendering output service, with an undertaking to pay the amount equal to the difference between the duty leviable on inputs but for the exemption and that already paid, if any, at the time of importation, along with interest, at the rate fixed by notification issued under section 28AA of the Act, for the period starting from the date of importation of the goods on which the exemption was availed and ending with the date of actual payment of the entire amount of the difference of duty that he is liable to pay.

(3) The Deputy Commissioner of Customs or, as the case may be, Assistant Commissioner of Customs having jurisdiction over the premises where the imported goods shall be put to use for manufacture of goods or for rendering output service, shall forward one copy of information received from the importer to the Deputy Commissioner of Customs, or as the case may be, Assistant Commissioner of Customs at the Custom Station of importation.

(4) On receipt of the copy of the information under clause (b) of sub-rule (1), the Deputy Commissioner of Customs or, as the case may be, Assistant Commissioner of Customs at the Custom Station of importation shall allow the benefit of the exemption notification to the importer who intends to avail the benefit of exemption notification.

(6) Importer who intends to avail the benefit of an exemption notification to give information regarding receipt of imported goods and maintain records. –

(1) The importer who intends to avail the benefit of an exemption notification shall provide the information of the receipt of the imported goods in his premises where goods shall be put to use for manufacture, within two days (excluding holidays, if any) of such receipt to the jurisdictional Customs Officer.

(2) The importer who has availed the benefit of an exemption notification shall maintain an account in such manner so as to clearly indicate the quantity and value of goods imported, the quantity of imported goods consumed in accordance with provisions of the exemption notification, the quantity of goods re-exported, if any, under rule 7 and the quantity remaining in stock, bill of entry wise and shall produce the said account as and when required by the Deputy Commissioner of Customs or, as the case may be, Assistant Commissioner of Customs having jurisdiction over the premises where the imported goods shall be put to use for manufacture of goods or for rendering output service.

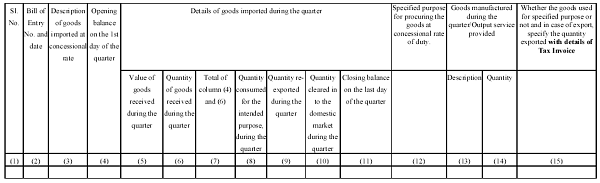

(3) The importer who has availed the benefit of an exemption notification shall submit a quarterly return, in the Form appended to these rules, to the Deputy Commissioner of Customs or, as the case may be, Assistant Commissioner of Customs having jurisdiction over the premises where the imported goods shall be put to use for manufacture of goods or for rendering output service, by the tenth day of the following quarter.

7. Re-export or clearance of unutilised or defective goods. –

(1) The importer who has availed benefit of an exemption notification, prescribing observance of these rules may reexport the unutilised or defective imported goods, within six months from the date of import, with the permission of the jurisdictional Deputy Commissioner of Customs or, as the case may be, Assistant Commissioner of Customs having jurisdiction over the premises where the imported goods shall be put to use for manufacture of goods or for rendering output service:

Provided that the value of such goods for re-export shall not be less than the value of the said goods at the time of import.

(2) The importer who has availed benefit of an exemption notification, prescribing observance of these rules may also clear the unutilised or defective imported goods, with the permission of the jurisdictional Deputy Commissioner of Customs or, as the case may be, Assistant Commissioner of Customs having jurisdiction over the premises where the imported goods shall be put to use for manufacture of goods or for rendering output service, within a period of six months from the date of import on payment of import duty equal to the difference between the duty leviable on such goods but for the exemption availed and that already paid, if any, at the time of importation, along with interest, at the rate fixed by notification issued under section 28AA of the Act, for the period starting from the date of importation of the goods on which the exemption was availed and ending with the date of actual payment of the entire amount of the difference of duty that he is liable to pay.

8. Recovery of duty in certain case. –

The importer who has availed the benefit of an exemption notification shall use the goods imported in accordance with the conditions mentioned in the concerned exemption notification or take action by re-export or clearance of unutilised or defective goods under rule 7 and in the event of any failure, the Deputy Commissioner of Customs or, as the case may be, Assistant Commissioner of Customs having jurisdiction over the premises where the imported goods shall be put to use for manufacture of goods or for rendering output service shall take action by invoking the Bond to initiate the recovery proceedings of the amount equal to the difference between the duty leviable on such goods but for the exemption and that already paid, if any, at the time of importation, along with interest, at the rate fixed by notification issued under section 28AA of the Act, for the period starting from the date of importation of the goods on which the exemption was availed and ending with the date of actual payment of the entire amount of the difference of duty that he is liable to pay.

8. References in any rule, notification, circular, instruction, standing order, trade notice or other order pursuance to the Customs (Import of Goods at Concessional Rate of Duty for Manufacture of Excisable Goods) Rules,1996 and any provision thereof or to the Customs (Import of Goods at Concessional Rate of Duty for Manufacture of Excisable Goods) Rules, 2016 and any corresponding provisions thereof shall, be construed as reference to the Customs(Import of Goods at Concessional Rate of Duty) Rules, 2017.

[F. No.450/28/2016-Cus IV]

(Zubair Riaz)

Director (Customs)

Form

[See rule 6(3)]

QUARTERLY RETURN

Return for the quarter ending_____

capital goods purchase against bond capiltal goods life

Would like to know whether IGCR rules applicable for STPI units also

need annexure format for taking benifit on custom duty for import ion battery eg 5%

hi i am shriniwas from RANJANS LI-ON ENERGY PVT LTD PUNE OUR COMPANY IS EV BATTERY AND LITHIUM BATTERY MANUFACTURING UNIT IS WADKI, our raw material is lithium cell and bms this material is available for only china , so i am import the material in china so i am requesting you to please tell me the procedure for conventional rate of duty certificate.

Do i need to submit bank guarantee if we are registered with AEO

Dear Sir,

Can we take re credit on capital goods also under this notification 68/2107. If so what is the procedure.

Dear Sir what is what is amount of security to be issued to Assistant commissioner of Custom ?