Advisory No. 02/2021 dated 03/03/2021 by DGS Bangalore for tracking of Legacy Arrears using DRC 07A and DRC 08A is released.

File No.DGSYS/APP/BZU/DSRR/2/2020-DSR-Recovery-1/o ADG-DGS-ZU-BENGALURU

Government Of India | Ministry Of Finance | Department Of Revenue

Central Board Of Indirect Taxes And Customs

Office Of The Additional Director General Of

Systems And Data Management, Bengaluru

3rd Floor, Visveswaraya Kendriya Bhawan, No.806,

Old Airport Road, Domlur, Benglauru-560071

Email: dgsystems-bengaluru@gov.in

Date: 03.03.2021

ADVISORY No. 02/2021

Sub: Release functionalities for tracking Legacy Arrears using DRC 07A/08A in Recovery Module— Reg.

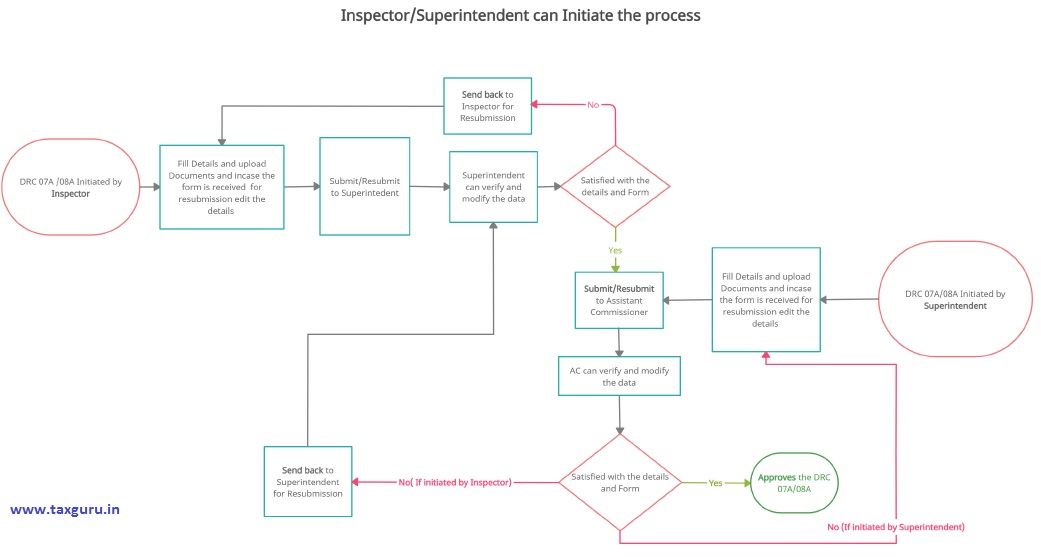

The Bangalore Zonal unit of Directorate of Systems and Data management is entrusted with the task relating to the development of modules of Dispute settlement and resolution (DSR), Investigation, Audit, Mobility and E-way Bill related modules. Recovery (including of Legacy Arrears) is one of the modules encompassed in the comprehensive Dispute Settlement and Resolution (DSR) module is now available for use by the officers of executive Commissionerates and is mainly built for Recovery Section. As you are all aware, Section 142(8) of the CGST Act, 2017 provides for recovery of confirmed dues under the existing Acts, unless recovered earlier, to be recovered as arrears under CGST Act, 2017. This module is intended for recovery of legacy arrears by uploading summary of demand order in FORM GST DRC-7A electronically on the common portal and creating demand in the Electronic Liability LedgerPart.II. Subsequently, when the demand is rectified or modified or quashed in any proceedings, including in appeal, review or revision, or the recovery is made under the existing laws, a summary thereof shall be uploaded in FORM GST DRC-08A and at the same time, the demand amount in Electronic Liability Ledger-Part.II shall be updated. As the dues are already confirmed and this is mostly a data entry specific functionality, there are only three roles involved in the present module. They are Inspector, Superintendent and Assistant/Deputy Commissioner. Further, irrespective of the fact as to whether the assessee is currently under state jurisdiction or central jurisdiction, the CGST officers can create the liability for the legacy arrears of all the assesses who were earlier registered in their jurisdiction as Central Excise/ Service Tax assessees. The salient features of the functionalities are discussed as under:

(I) Issuance of FORM GST DRC-7A:

Legal Provisions: Section 142(8) & (9) of the CGST Act, 2017 and Rule 142A of the CGST Rules, 2017.

Pre-requisite: The tax payer who has unpaid confirmed tax arrears, including interest/ penalty or fine, pending against him as per the existing Acts of Central Excise Act 1944 or Finance Act 1994 should have migrated as a Tax payer under the GST Act and should be operating within the particular State.

(a) Either Inspector or Superintendent has the credentials to create FORM DRC-07A ((Menu>DISPUTE SETTLEMENT AND RESOLUTION>ARREARS>Issue DRC07A>Create New DRC-07A). After creating the form, the officer selects the GSTIN and enters the details of demand order: uploads the copy of demand order & other relevant documents and submits to the next higher level officer. In case the form (task) is created by the Superintendent, task moves to the Assistant /Deputy Commissioner.

(b) The Assistant/Deputy Commissioner or the Superintendent can access the task (Menu>Task Lists>DSR>DRC-07A) and peruse/modify the contents of the form. If the task is received by the Superintendent, he can verify the form and submits to the Assistant/Deputy Commissioner.

(c) The Assistant/Deputy Commissioner has the credentials to approve the form. If satisfied, he can approve the form. After approval, the FORM GST DRC-07A gets generated and issued to the tax payer through GSTN portal and demand ID gets created in the Electronic Liability Ledger-Part-II of the tax payer.

(II) Issuance of FORM GST DRC-8A:

Legal Provisions: Section 161 of the CGST Act,2017 and Rule 142A of the CGST Rules,2017.

Pre-requisite: FORM DRC-07A has already been issued and demand exists in Electronic Liability Ledger-Part.II.

(a) Either Inspector or Superintendent can initiate the task (Menu>DISPUTE SETTLEMENT AND RESOLUTION>ARREARS>DRC-08A List View). From the list, the officer can select DRC-07A reference number to get FORM DRC-07A. After accessing the form, the officer can create FORM GST DRC-08A. All the data of DRC-07A are auto pulled and editable. The necessary entries can be modified and rectified order or relevant documents can be uploaded. When it is submitted, task moves to next higher level officer. In case, the form (task) is created by the Superintendent, task moves to the Assistant /Deputy Commissioner.

(b) The Assistant/Deputy Commissioner or the Superintendent can access the task (Menu>Task Lists>DSR>DRC-08A) and peruse/modify the contents of the form. If the task is received by the Superintendent, he can verify the form and submits to the Assistant/Deputy Commissioner.

(c) The Assistant/Deputy Commissioner has the credentials to approve the form. If satisfied, he can approve the form. After approval, the FORM GST DRC-08A gets generated and issued to the tax payer through GSTN portal and demand gets updated in the Electronic Liability Ledger-Part-II of the tax payer.

(d) In case of rework, the higher level officer can send back the task to lower level officer.

2. It is to be noted that the facility for digital signature is not available for the time being, it is advisable to ensure that notices or orders or any documents, which are legal in nature are signed by the respective authorities and issued, in addition to the online issuance of the same.

3. For clear understanding of the process, user manuals for both FORM DRC-07A and FORM GST DRC-08A are available on CBIC-GST portal and Antarang portal. A flow chart indicating the basic flow for creation of DRC7A/8A is attached herewith.

4. All the officers are advised to carefully study this advisory along with the User Manual attached and update the Liability Ledger of the tax payers against whom arrears are pending recovery under the pre-GST Acts.

5. The CGST Act and Rules made there under on the captioned subject will have precedence over the workflow built in the system. All Officers are advised to read the documents and the relevant legal provisions applicable to this functionality carefully. Wherever a deviation from the extant law, rules and procedures is observed in the system design, the jurisdictional officers are requested to raise a ticket on CBIC-Mitra. Any problems not resolved through CBICMitra may be brought to the notice of the Directorate of Systems and Data Management, Sir, M Visveswaraya Kendriya Bhavan, No 806, 3rd floor, Old Airport Road Domlur, Bangalore 560071. (email: adgblr.admin@gov. in).

( R. SRIRAM)

ADDITIONAL DIRECTOR GENERAL ( SYSTEMS)

Copy to :

(1) The Principal Director General of Systems & Data Management, New Delhi for information.

(2) All the Principal Chief Commissioners/Chief Commissioners of Central Tax. (3) All the Principal Commissioners/Commissioners of Central Tax

DRC 07A and DRC 08A Basic Flow

GST DRC THANKS FOR LATEST UPDATE INFORMATION

I SOLELY BELIEVE , BUT WHO WILL STOP THIS ACT, IS GOVT CAN TAKE ACTIONS AGAINST THESE OFFICERS. THE ANSWER IS BIG “NO”.