Merger of large companies in same industry is Anti-Competitive but merger of Vodafone & Idea is not (though merged entity will have highest market share in Wireless Telecom Market). Here’s why?

Introduction:

Reliance Jio, A company which brought digital revolution in India and has changed the composition of telecom industry which was originally having 11 competitors (before inception of Jio) to now being only 5 competitors (Of which, R Com is set to be bankrupt due to huge debt)

It has also led to merger of two large companies namely Vodafone & Idea into a single entity namely Vodafone Idea Limited for facing stiff competition and to remain operating in prevailing price war despite having huge debt and running in heavy losses. Merger of Vodafone & Idea has led to better service provision in below manner:

– Broadband network covering 840 Million Indians

– Voice network covering 1.2 Billion Indians (Around 92% of Population)

– 1.7 Million Retailers & 15 Thousand Service Stores

– Subscriber base of over 408 million in Jun-18

– Enhanced coverage across 500,000 towns & villages

Issue Involved:

Competition Commission of India (CCI) set up under Competition Act, 2002 for regulating combinations of entities on certain criteria so as to check if such combination will have appreciable adverse effect on competition (i.e., such merged entity may exercise its power in merged entity for excluding competition / competitors from the market)

CCI Has noted that both Vodafone & Idea were operating in below businesses:

1. Wireless Telecommunication Services

2. Wireline Telecommunication Services

3. Broadband Services

4. Mobile Wallet Services

5. Passive infrastructure services through telecom towers

Analysis of facts and Representations made before CCI– CCI has carefully examined and concluded the following w.r.t. each of above businesses:

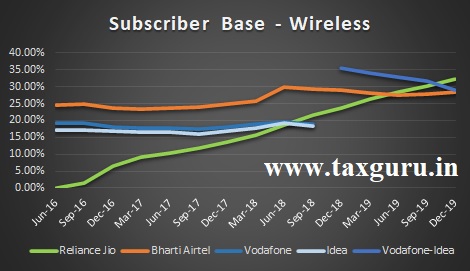

1. Wireless Telecommunication Services

Till the inception of Reliance Jio, both Vodafone (19%) & Idea (17%) were in second & third position respectively in industry after Bharti Airtel (25%). Inception of Reliance Jio with predatory pricing strategy has led to gaining of 9.29% share with more than 10.86 Crores users in less than 12 months and decline in Market Share of Vodafone & Idea as evidenced below

– Market Share in Various Circles

Out of 22 Telecom Circles in India, merged entity will have highest market share in 9 Circles and will have more than 30% stake in 14 circles. This may be termed as Anti-Competitive but CCI has turned down the same since in 10 out of 14 Circles as stated above, entity’s share appears to be close to that of competitors

– Net Subscriber Addition in FY 2016-17

Net Subscriber Addition in immediately preceding Financial Year evidences high growth among competitors as tabulated below. Reliance Jio’s predatory pricing has led to such a huge increase in subscriber base:

| Month | Reliance Jio | Bharti Airtel | Vodafone | Idea |

| Mar-16 (a) | – | 25,12,37,263 | 19,79,46,755 | 17,50,74,042 |

| Jun-16 | – | 25,57,34,650 | 19,93,83,512 | 17,62,34,152 |

| Sep-16 | 1,59,79,745 | 25,99,40,666 | 20,07,21,247 | 17,88,16,338 |

| Dec-16 | 7,21,57,644 | 26,58,52,605 | 20,46,86,930 | 19,05,17,876 |

| Mar-17 (b) | 10,86,80,772 | 27,36,48,383 | 20,90,62,866 | 19,53,68,847 |

| Net Addition (b-a) | 10,86,80,772 | 2,24,11,120 | 1,11,16,111 | 2,02,94,805 |

– Fair Distribution of Spectrum & Size of Competitors

On examination of spectrum holding of different companies in all telecom circles, CCI noted that the spectrum seems to be fairly distributed between them. Further, it also noted that there is a significant quantity of unsold spectrum in each telecom circle which may also obviate any access issues.

It further examined the size and resources of these competitors and is of the opinion they are in a position to exercise adequate competitive constraints on the Merged Entity and to eliminate any likelihood of appreciable adverse effect on competition resulting from the Proposed Combination

– Multi-SIMming

As on Jun-16, Out of 103.5 Crore subscribers, approximately two-third subscribers tend to have multiple SIMs which evidences that customers can easily and quickly switch from a primary to a secondary SIM and vice versa, considering relative price of one of their SIM providers (or any of the services offered by them) increases or decreases, by changing the selection of the SIM in their handset

– Easy Portability

As a result of the Mobile Number Portability Regulations, 2009, customers are able to switch their primary SIM / service provider seamlessly (with minimal or no charge and without any significant time taken or effort for switching). Till 31st December 2016, more than 25.4 Crore Subscribers (22.53% of total subscribers) has availed MNP facility which evidences above fact.

The near zero switching cost ensures that there is price competition amongst the TSPs to retain customers

– High Churn Rate

Churn Rate refers to annual percentage of customers stopping subscription to a service. As per CCI Order dated 03rd October 2017, churn rate of the Parties at pan India level is more than 60 percent and exceeds 50 percent for most of the telecom circles. The Commission observed that high churn rates imply rapid turnover of the customer base which indicates shifting consumer preferences and ease of switching

– Increase in HH Index

HH Index is used to measure competition in market. Lower the index is, better the competition. Pre-Combination HH Index is exceeding 2000 in all circles (except in 3 circles where it is exceeding 1800). Market in which HHI is in 1500-2500 range is assumed as moderately concentrated market.

A merger which will increase HHI by 200 is an indication of Anti-Competitive. Though this merger will result in increase of HHI by 400 – 1500 in various circles, CCI has considered it as Anti-Competitive considering competitor’s stake in such circles and factors as stated above

– Reduction in Number of Competitors

With increased HH Index, it becomes important to also assess the impact of reduction in number of competitors on the competition. Parties have submitted details regarding number of competitors in 220 countries among globe stating that 213 countries are having four or less operators and 6 countries having five operators & India is the only country having more than 5 operators and reduction on number of competitors at this stage is not likely to have any adverse effect on competition

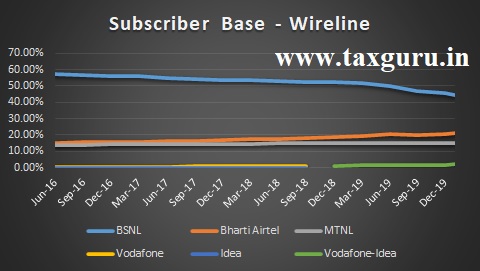

2. Wireline Telecommunication Services

BSNL & MTNL, two PSU access service providers & Bharti Airtel are leading the market. Vodafone is having a niche share in the market with less than 1.2% pre-merger and Idea is not in this business line. This evidences that merger will not have any negative impact on competition in this market. Market share over considerable period of time of dominant players along with current companies to merger is shown below

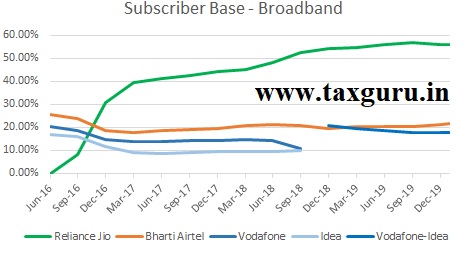

3. Broadband Services

Both Vodafone & Idea were having considerable market share till the inception of Reliance Jio. Within one year of Jio starting its services, Market share of Vodafone has fell from 20.20% to 13.67% & Idea has fell from 16.91% to 8.76% which is shown in the form of chart below. This has made them niche players in the market dominated by Reliance Jio, followed by Bharti Airtel:

4. Mobile Wallet Services

Vodafone is providing Mobile Wallet Services through M-Pesa & Idea is providing service through Idea Money – a pre-paid wallet and mobile money account. CCI has observed that parties do not have any significant presence in the market which is characterised by dominant players like PayTM, Oxigen, Airtel Money & Mobikwik etc. which evidences no negative impact on competition.

5. Enterprise Services / Retail Business

CCI has observed that retail business is further divided into various segments & sub-segments. Idea was into retail business which was a niche player and does not own material stake in any of such segments / sub-segments. Vodafone does not have any presence in it. So, CCI has concluded that there is no impact on competition in such market.

6. Passive infrastructure services through telecom towers

Neither Vodafone not Idea was directly into this business but both the companies own significant stake in Indus Towers (Idea – 11.15% stake & Vodafone – 42% stake) which was in above business. Merger of above companies will lead to controlling of the company which is considerably a big player in the market.

Vodafone has not transferred its stake to the merged entity and has informed CCI that it is in process of making arrangements to sell its stake and CCI has passed order accordingly.

Conclusion:

After above analysis, CCI has concluded that merger of players in dominant position in industry always cannot be termed as Anti-Competitive unless the same is evidenced by an Anti-Competitive objective of excluding competition / competitors which does not seem to be the current scenario after considering relevant market and competitors.

*****

Disclaimer: The contents of this article are for information purposes only and do not constitute an advice or a legal opinion and are personal views of the author. It is based upon relevant law and/or facts available at that point of time and prepared with due accuracy & reliability. Readers are requested to check and refer relevant provisions of statute, latest judicial pronouncements, circulars, clarifications etc before acting on the basis of the above write up. The possibility of other views on the subject matter cannot be ruled out. By the use of the said information, you agree that Author / TaxGuru is not responsible or liable in any manner for the authenticity, accuracy, completeness, errors or any kind of omissions in this piece of information for any action taken thereof. This is not any kind of advertisement or solicitation of work by a professional.