Onosetale P Aigbe

ABSTRACT: The Research and Development (‘R&D’) Tax Credit is an incentive United States Congress initialized to reward businesses in their research and experimental endeavors for their contributions to the U.S. economy. The R&D Tax Credit was introduced in the Economic Recovery Tax Act of 1981 and since its creation, it has evolved over the years and has been subject to several law changes, including but not limited to the computation of the credit, additional memorandum requirements and the qualification criteria for businesses. There has been analysis performed throughout the ‘years’ to conclude if the R&D Tax Credit stimulates R&D in the U.S., but there has not been much correlation, rather there is trend between the R&D Tax Credit and R&D Investment. Changes to Revenue Procedure Section 174, in 2022 was the most recent policy change that has affected many companies looking to claim the R&D tax Credit to lower tax burdens.

This article discusses the background of the R&D Tax Credit, qualification requirements and the computation of the credit for businesses. The gradual recognition of the credit since 1981 and the effects of Section 174 on the R&D Tax Credit are reviewed in the text.

- What is the history of the R&D Tax Credit?

- How do companies qualify for the R&D Tax Credit?

- What is the purpose of the R&D Tax Credit?

- How to calculate the R&D Tax Credit?

- How has the awareness and impact of the R&D Tax Credit grown over the years?

- What is the impact of changes to Section 174 and the implications on businesses claiming the R&D Tax Credit in 2022?

What is the history of the R&D Tax Credit?

Before officially establishing the R&D Tax Credit in 1954, the U.S. Congress allowed taxpayers, under Internal Revenue Code (‘IRC’) Section 174, to deduct research or experimental expenses associated with a business. However, in 1981, there was an inadequate spending on costs in research and experimental expenses in the U.S. The U.S. Congress perceived an economic slowdown in the country due to many companies continuously outsourcing technical development internationally.

In response to the slowdown, the federal R&D Tax Credit, formally known as the Credit for Increasing Research Activities, was enacted as a reward for American businesses that kept research and development efforts ‘in-house’- on U.S. soil. The R&D Tax Credit is an incentive used to stimulate innovation and research in the U.S. Originally for businesses to qualify for the credit, they needed to develop a new or improved business component (a business component can be a product, process, formula, invention, software and technique) that yielded to the Discovery Rule. The Discovery Rule dictated that research activities be undertaken to ‘obtain knowledge that exceeds, expands, or refines the common knowledge of a skilled professional.’

In 2003, the Discovery Rule was removed and the qualification for the R&D credit became less stringent for businesses to qualify for. Now, taxpayers need to engage in research activities that are ‘new to the taxpayer’ to qualify for the R&D Tax Credit. This allowed for more companies to qualify and claim the R&D Tax Credit.

How do companies qualify for the R&D Tax Credit?

Many companies belonging to different industries can qualify for the R&D Tax Credit. The chart below shows a list of some of the industries that can qualify for the R&D Tax Credit.

Regardless of the industry, a taxpayer must engage in research activities that meet the ‘4 Part Test’ according to IRC Section 41 (d) (4). A taxpayer must perform activities that satisfy the following test, to qualify the activity and claim the appropriate allowable expenses. The four parts of the tests are:

1. New or Improved Business Component – The taxpayer must perform activities that relate to the making of a new or improved product, process, software, technique, formula, and invention for a permitted purpose.

*A Permitted purpose relates to the functionality, performance, quality, or reliability of the business component.

2. Elimination of Technical Uncertainty – The uncertainty relating to the development of the business component must be regarding the appropriate design, the capability or methodology of designing and improving the business component.

3. Process of Experimentation – The taxpayer must engage in an evaluative process that can identify and evaluate one or more alternatives to achieve a result. This may include modelling, simulation or a systematic trial and error methodology.

4. Technological in Nature – The basis of the activities performed must be based on principles of a hard science like engineering, physics, or mathematics and not based on social sciences or arts.

What is the purpose of the R&D Tax Credit?

The purpose of the R&D Tax Credit is to serve as an incentive to firms in the U.S. that are partaking in research and experimentation. When businesses invest in

- wages for employees to conduct R&D,

- third-party U.S. contractors to assist in R&D endeavors,

- supplies and raw materials and

- cloud hosting expenses used in research and development,

the U.S. government seeks to reward them for their innovation. The R&D Tax Credit is a non-refundable credit used to offset a dollar-to-dollar tax reduction from federal and/or state tax liability. With a lower tax burden, U.S. companies and business owners can invest back in their business and in their R&D efforts. R&D Tax Credits can provide the resources and ability for qualified companies to hire more technical personnel, acquire materials and cutting-edge technology to continue in original and advanced innovation.

How to calculate the R&D Tax Credit?

Businesses can calculate their R&D Tax Credit value using two popular methods provided by IRC Section 41 (a) and Section 41 (c): the Regular Credit and the Alternative Simplified Credit (‘ASC’), respectively. The Regular credit method was the original method of calculating the R&D Tax Credit. Regular Credit is the product of twenty percent of the lesser of the current qualified research expenses (QREscy) and base amount (BA). The base amount is dependent on historical gross receipts that can go as far as the inception of the company and is also dependent on the qualified research expenses during both the conception years and current year of the company.

|

Regular Credit = 20% (QREscy– BA) |

Seeing that the Regular Credit caused a lot of obstacles for some companies who did not have access to their bookkeeping from inception or thereabout, Congress enacted the Alternative Simplified Calculation (ASC) in the Tax Relief and Health Care Act of 2006. The ASC is the product of the twenty percent and the qualified research expenses of the current year (QREscy) less the base amount (BA). The base amount for the ASC is solely dependent on the qualified research expenses for the prior three years and the current year.

|

ASC = 14% (QREscy – BA) |

How has the awareness and impact of the R&D Tax Credit grown over the years?

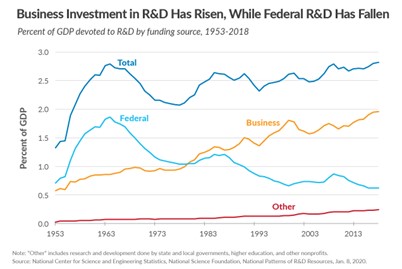

From the introduction of the R&D Tax Credit in the Economic Recovery Tax Act of 1981, the R&D credit has gained momentum through the years. The R&D Tax Credit was intended to last for 5 years with an expiration on December 31, 1985, but the credit was extended about fifteen times until it was made permanent in 2015. It has now been eight years since the R&D Tax Credit was made permanent and studies show that many private sectors compared to public sectors have begun seeking to claim the R&D Tax Credit. The graph (Figure 1) below compares the trend of the Gross Domestic Product in the U.S. from years 1953 – 2018. There is an increase in the development of products and services in the private sectors compared to the public federal sector. Since the introduction of the R&D Tax Credit in 1981, there has been an increase in R&D in the United States in the many small and medium sized businesses. There is no confirmation that the R&D Tax Credit causes the increase in the R&D activities, but there have been studies to show the extent to which the R&D Tax Credit increases the value in R&D expenses a company might spend on R&D costs.

A 2021 article, Reviewing the Federal Tax Treatment of Research & Development Expenses, summarizes some literature and analysis on the impact on the R&D Tax Credit and the amount of R&D spending’s [1]. Since 1989, there has been research and published articles drawing a relationship between the R&D Tax Credit and the amount businesses spend on R&D costs. A literature review in 1989 stated an estimate of 35 cents to 93 cents of new research spending generated from $1 of R&D tax credit [2]. As the R&D tax credit changed after the Omnibus Budget Reconciliation Act of 1989, studies showed that with $1 of R&D tax credit identified it stimulated $2.08 in investing R&D expenses [3]. As of 2017, an analysis in the Review of Economic and Statistics found that $1 of R&D tax credit can yield $4 in R&D spending [4].

Figure 1: Trends in U.S. GDP from 1953 for Public and Private Sectors [1]

What is the impact of changes to Section 174 and the implications on businesses claiming the R&D Tax Credit in 2022?

Section 174 Research and Experimentation (R&E) expenses differ from Research and Development (R&D) expenses. Section 174 costs are inclusive of all R&D expenses, but have additional expenses like overhaul costs, rent, utilities that are qualified under Section 174. Initially taxpayers had the option to deduct full R&E costs or capitalize and amortize them over a period of 5 years. In late December 2022, Revenue Procedure 2023-11 was enacted and revised the Tax Cuts and Job Acts. Revenue Procedure 2023-11, removed the option for taxpayers to deduct the total 174 expenses, rather, Section 174 expenses must be amortized over 5 years and 15 years for costs for foreign research outside the U.S.

Because of Section 174’s implication of amortization, taxpayers have become hesitant and reluctant in claiming the R&D Tax Credit, even though ironically, the changes to Section 174 do not affect the R&D Tax Credit. R&E expenditures for the R&D Tax Credit under Section 41 must first be included in specified R&E expenditures under Section 174. In 2023, many companies did not desire to claim the R&D expenses since it would serve as a starting value for the R&E expenditures that taxpayer would be required to amortize. Amortizing the expenses will increase the taxable income since only about 10% the R&E expenses can be deducted initially.

References

[1] Muresianu, A., & Watson, G. (2023, July 24). Reviewing the Federal Tax Treatment of Research & Development Expenses. Tax Foundation. https://taxfoundation.org/research/all/federal/research-and-development-tax/#_ftn21

[2] Cordes, J. J., 1981, A., Chirinko, R., Baily, M., Barth, J., Associates, C. R., Collins, E., Cordes, J., Eisner, R., & Ellis, L. (2002, March 12). Tax Incentives and R&D Spending: A Review of the Evidence. Research Policy. https://www.sciencedirect.com/science/article/pii/0048733389900012

[3] Gupta, S., Hwang, Y., & Schmidt, A. (1970, January 1). Structural Change in the Research and Experimentation Tax Credit: Success or Failure. National Tax Journal. https://ideas.repec.org/a/ntj/journl/v64y2011i2p285-322.html

[4] Thomson, R. (n.d.). “The Effectiveness of R&D Tax Credits,” The Review of Economics and Statistics 99:3. Direct.mit.edu. https://direct.mit.edu/rest/article-abstract/99/3/544/58438/The-Effectiveness-of-R-amp-D-Tax-Credits?redirectedFrom=fulltext

Thanks for sharing this informative piece Onosetale. I’ll be interested to see how the 2022 changes play out in terms of R&D investments and economic outcomes. It’s definitely an area worth monitoring.