INTRODUCTION

eXtensible Business Reporting Language (XBRL) is an emerging technology standard, which promises to bring “better, faster, cheaper” data to organizational decision-making, and specifically to business and financial reporting.

XBRL provides a computer-readable tag to identify each individual item of data, whereby, a business reporting document becomes “intelligent” data, allowing the exchange of business reporting data by encoding the information in a meaningful way.

XBRL enables computer applications to recognize the information in an XBRL document – selecting, analyzing, storing, and exchanging it with other computers and present it in a variety of ways for users.

ORIGIN

XBRL is being developed by XBRL International, an international non-profit consortium of approximately 450 major companies, organisations and government agencies working together to build the XBRL language and promote and support its adoption. This collaborative effort began in 1998 and has produced a variety of specifications and taxonomies to support the goal of providing a standard, XML-based language for digitizing business reports in accordance with the rules of accounting in each country or with other reporting regimes such as banking regulation or performance benchmarking.

ADOPTION OF XBRL BY MINISTRY OF CORPORATE AFFAIRS

XBRL is a language for the electronic communication of business and financial data that has revolutionized business reporting around the world. Its major benefits include ease in preparation, analysis and communication of business information by the corporates. It offers cost savings, greater efficiency, improved accuracy as well as reliability to all those involved in supplying or using financial data. With increased coverage, it is hoped that the XBRL data thus collected would significantly enhance the Ministry’s capabilities in policy formulation and regulatory functions for advantage of corporates as well as public and investors at large.

It is proposed to include all companies in a phase-wise manner to file their Balance Sheet and Profit and Loss account statements in XBRL from Financial Year 2011-12 onwards. With the development of taxonomies for Banks, Insurance, Non-Banking Finance Companies and Power sector, the companies operating in these sectors would also be filing their financial reports in XBRL. The taxonomies would be updated and maintained with applicability of revised Schedule VI from 01.04.2011. Training programs, seminars, conferences, etc would also be organized in tier-II and tier-III cities by the Ministry in association with professional institutes and industry bodies. Cost Audit Report and Compliance Report from eligible companies as per Cost Accounting Record Rules, 2011 would be captured from FY 2011-12 onwards.

STATUROTY REQUIREMENT FOR XBRL FILING UNDER COMPANIES ACT

Pursuant to the provisions of Section 137 of the Companies Act, 2013 and the provisions of the Companies (Filing of Documents and Forms in XBRL) Rules, 2015, the financial statements, audit report and directors report of below mentioned companies as specified by Ministry of Corporate Affairs shall be filed with the Registrar of Companies in Form AOC-4 XBRL within 30 days of Annual General Meeting of the Company:

A. Companies Listed with Stock Exchanges in India and their Indian Subsidiaries;

B. Companies having paid up capital of Rupees Five Crore (Rs. 5 Crore) or above;

C. Companies having turnover of Rupees One Hundred Crore (Rs. 100 Crore) or above.

D. All companies which are required to prepare their financial statements in accordance with Companies (Indian Accounting Standards) Rules, 2015.

NOTE: Non-Banking Financial Companies, Housing Finance Companies and Companies engaged in the business of Banking and Insurance sector are exempted from filing of financial statements in XBRL Format.

IMPORTANT TERMS UNDER XBRL

- TAXONOMY

Taxonomy means in XBRL, an electronic dictionary for reporting the business data as approved by the Central Government in respect of any documents or forms. Different taxonomies are required for different business reporting purposes.

There are following taxonomies as approved by MCA till date:

1. C&I 2016

2. C&I 2012

3. C&I 2011

4. IND-AS 2017

- MAPPING

Mapping is the process of comparing the concepts in the financial statements to the elements in the published taxonomy, assigning a taxonomy element to each accounting concept published by the company.

- TAGGING

XBRL, or eXtensible Business Reporting Language, is an XML standard for tagging business and financial reports to increase the transparency and accessibility of business information by using a uniform format.

Tagging is the process of applying the entity’s unique financial data to an element within the taxonomy. The tagging process is performed during the creation of an instance document.

The first step in creation of an instance document is to do tagging of the XBRL taxonomy elements with the various accounting heads in the books of accounts of the company. This would create the mapping of the taxonomy elements with the accounting heads so that the accounting information can be converted into XBRL form.

- INSTANCE DOCUMENT

An instance document is the file that includes the company specific business reporting information in a structured manner that computers can intelligently recognize and exchange. The instance document is an XML file where everything comes together; here the entity specific data links (tags) to the elements in the taxonomies to form the XBRL document that can be validated and transmitted automatically for utilization by numerous consumers.

XBRL TOOLS

In order to work in XBRL, you will need software. There are a number of XBRL tools in the marketplace today. You can refer to the following web link “http://mca.gov.in/XBRL/software_vendor.html” for details on vendors that support XBRL.

MCA XBRL VALIDATION TOOL

MCA XBRL Validation Tool ensures that only those XBRL documents; that satisfy the requirements of Taxonomy and Business Rules, are filed with MCA under section 137 of the Companies Act, 2013. MCA Validation Tool is an important mean for improving the quality of financial information/disclosures in XBRL. Successful validation of the instance document is a pre-requisite before filing the balance sheet and profit & loss account on MCA portal.

It may, however, be noted that mere successful validation of an XBRL document by the MCA Validation Tool does not mean that the provisions under section 129 of the Companies Act, 2013 have fully been complied with. It is important to ensure that this ‘validated’ XBRL document also provides a true and fair view of the state of affairs of the company as per financial statements adopted in the AGM.

MCA XBRL Validation Tool also provides the ‘human-readable’ pdf version of the XBRL document for ease in authentication and certification of the XBRL document being filed by the company to MCA. The validation tool of MCA can be downloaded from following web link:

http://mca.gov.in/XBRL/XBRL TOOL/MCA XBRL Validation Tool Version 4.5.zip

LIST OF DOCUMENTS REQUIRED FOR XBRL FILING UNDER COMPANIES ACT

The following documents are required to process the XBRL filing :

- Financial Statement including Balance Sheet, Profit & Loss Account, Cash Flow Statement, Schedules related to Balance Sheet and Profit & Loss Statement, Notes to Accounts (In excel)

- Significant Accounting Policies (In Word)

- Audit Report including report on CARO (In Word)

- Directors’ Report (In Word)

- MGT-9 (In Excel)

- AOC-1, AOC-2, Secretarial Audit Report (In Word)

- Corporate Governance Report (In Word)

- Complete Annual Report (In Word)

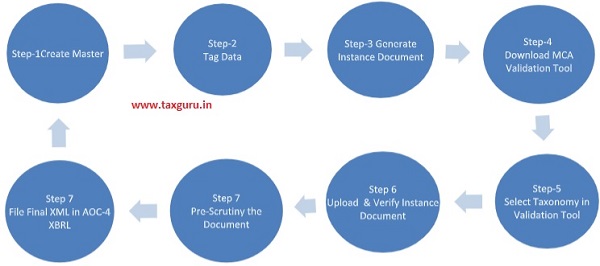

STEPS INVOLVED IN PROCESS OF XBRL

1. Avail the XBRL Tool from the authorised Vendors.

2. Create the Master Data of Company, Directors and Auditor in the tool.

3. Tag the complete Financials, Notes, Schedules, Audit Report, Directors Report, Annual Report in the XBRL Format.

4. Generate the Instance Document in XML Format

5. Download the Validation Tool from MCA and select the applicable Taxonomy.

6. Upload the instance document at validation tool and map and verify the document through validation tool.

7. Once Document verified or mapped, pre-scrutinise the same with the help of validation tool

8. Attach the pre-scrutinised instance document in Form AOC-4 XBRL and file the same with the Registrar within 30 days of Annual General Meeting.

PENALTY PROVISIONS:

If you fails to file the copy of the Financial Statements to ROC within prescribed time limit

- For Company : Penalty of Rupees One Thousand (Rs. 1000/-) for every day during which the failure continues but which shall not be more than Rupees Ten Lakh (Rs.10,00,000/-).

- For Directors : Penalty of Rupees One Lakh (Rs. 1,00,000/-) and in case of continuing failure, with further penalty of Rupees One Hundred (Rs.100/-) for each day after the first during which such failure continues, subject to a maximum of Rupees Five Lakh (Rs.5,00,000/-).

Anyone having any query regarding XBRL Filing or any other query regarding any corporate law can reach CS HITESH JHAMB (JHAMB & ASSOCIATES) at jassociates.cs@gmail.com and also at 9953001339 / 9654080119.

Author Bio

Hello sir,

MCA recently change it’s XBRL Validation Tool Version 4.5 to 4.6 but I could not found what was the new validation put in new 4.6 version. can you guild me or share with me this list of new validation in version 4.6