A 2023 inspection by the National Financial Reporting Authority (NFRA) of M/s Walker Chandiok & Co. LLP (WCCL) revealed a failure to adequately address deficiencies previously identified in auditor independence, audit documentation, and Engagement Quality Control Review (EQCR). The NFRA’s review, conducted in August and October 2024, also found shortcomings in the firm’s audit procedures across three selected engagements for the financial year ending March 31, 2023. Specifically, the inspection noted deficiencies in the verification of Related Party Transactions, Impairment of Non-Financial Assets, and Internal Financial Control over Financial Reporting related to revenue, areas considered to have a higher risk of material misstatement. The NFRA stated that the objective of its inspections is to evaluate an audit firm’s compliance with auditing standards, regulatory requirements, and the effectiveness of its quality control systems, while also clarifying that inspections are distinct from investigations and are not intended as a comprehensive review or a rating mechanism for audit firms.

National Financial Reporting Authority

Inspection Report 2023

Audit Firm: M/s Walker Chandiok & Co LLP

Firm Registration No.001076N/N500013

Inspection Report No.132.2-2023-06

March 28, 2025

PART -A

M/s Walker Chandiok & Co LLP – Inspection Report No.132.2-2023-06

Executive Summary

Section 132 of the Companies Act 2013 (the Act) mandates the National Financial Reporting Authority (NFRA), inter alia, to monitor compliance with Auditing Standards, to oversee the quality of service of the professions associated with ensuring compliance with such standards, and to suggest measures required for improvement in quality of their services. Under this mandate, NFRA conducted an audit quality inspection of Walker Chandiok & Co. LLP (WCCL hereinafter) in August 2024. The scope included a review of the remedial actions taken by the Firm for the deficiencies reported in the previous inspection report, and a review of three selected audit engagements of financial statements for the year ending 31.03.2023, focusing on three significant audit areas, viz., Related Party Transactions, Impairment of Non-Financial Assets and ICFR-Revenue due to their inherent higher risk of material misstatement. The inspection included an on-site visit in October 2024, discussions with the Audit Firm personnel including the engagement teams of the selected audit engagements, review of policies and procedures, and examination of documents. The key observations in this report are summarized as follows:

a. The Audit Firm has not remediated the issue related to the auditor’s independence, audit documentation, and EQCR, as noted in the previous inspection report. These issues are discussed in Part B of this report.

b. In three (3) engagement files selected for review in the current inspection cycle, deficiencies were noted in the verification of Related Party Transactions, Impairment of Non-Financial Assets, and ICFR-Revenue. These are discussed in detail in Part C of this report.

Inspection Overview

1. The overall objective of audit quality inspections is to evaluate compliance of the audit firm/auditor with auditing standards and other regulatory and professional requirements, and the sufficiency and effectiveness of the quality control systems of the audit firm/auditor, including:

a. adequacy of the governance framework and its functioning

b. effectiveness of the firm’s internal control over audit quality; and

c. system of assessment and identification of audit risks and mitigating measures

2. Inspections are intended to identify areas and opportunities for improvement in the audit firm’s system of quality control. Inspections, by nature, are distinct from investigations undertaken under section 132 (4) of the Act. However, in certain cases, test-check by the inspection teams may provide basis for or require reference of such cases/matters for enforcement or investigation under applicable provisions of the Act and Rules.

3. This year’s inspections involve a review of the remedial action taken by the Firm in response to the previous inspection observations and a test check of audit engagements performed by the Audit Firm relating to the statutory audit of financial statements for the year ending 31.03.2023.

4. Inspections are intended to identify areas and opportunities for improvement in the Audit Firm’s system of quality control. Inspections are, however, not designed to review all aspects and identify all weaknesses in the governance framework system of internal control, or audit risk assessment framework; nor are they designed to provide absolute assurance about the Audit Firm’s quality of audit work. In respect of selected audit assignments, inspections are not designed to identify all the weaknesses in the audit work performed by the auditors in the audit of the financial statements of the selected companies. Inspection reports are also not intended to be either a rating model or a marketing tool for audit firms.

Audit Quality Inspection Approach

5. Selection of audit firms for the 2023 inspections was based upon the extent of public interest involved, as evidenced by the size, composition, and nature of the audit firm; the number of audit engagements completed in the year under review; complexity and diversity of the company’s financial statements audited by the firm and other risk indicators. M/s Walker Chandiok & Co. LLP (WCCL) was one of the audit firms selected as per the above parameters.

6. The selection of individual audit engagements of the Walker Chandiok & Co. LLP, was largely risk-based, based on financial and non-financial risk indicators identified by NFRA. Accordingly, the audit files in respect of three (3) audit engagements relating to the statutory audit of financial statements for the year ending 31.03.2023 were reviewed during the inspection.

7. The scope of the inspection was as follows:

a. Review of the remedial measures and improvements made in response to the previous inspection observations for firm-wide quality controls to evaluate the Audit Firm’s adherence to SQC 1, Code of Ethics, and the applicable laws and rules.

b. Review of individual Audit Engagement Files- A sample of three (3) individual audit engagement files pertaining to the annual statutory audit of financial statements for the year ending 31.03.2023 was selected. Three significant audit areas were identified in respect of each audit engagement viz., Related Party Transactions, Impairment of Non-Financial Assets, and ICFR -Revenue, due to their inherent higher risk of material misstatement.

The selected sample of three individual audit engagements is not representative of the Firm’s total population of the audit engagements completed by the Firm for the year under review.

Inspection Methodology

8. An entry meeting for the current year’s inspection was held with M/s Walker Chandiok & Co. LLP on 30.04.2024 at the NFRA office. Discussions were held with the engagement teams of the three audit engagements selected for review. The on-site inspection was carried out between 08.10.2024 to 10.10.2024.

Audit Firm’s Profile

9. M/s Walker Chandiok & Co. LLP (WCCL), a Limited Liability Partnership, is registered with The Institute of Chartered Accountants of India. WCCL stated that it was a part of a network1 of two audit firms, which operate through a registered office and several branch offices at different locations across India. The Firm was a statutory auditor of 293 entities falling under NFRA’s purview (Annexure-1).

10. As reported in the Inspection Report 2022 (IR 2022 hereinafter), WCCL is also a part of an international network called Grant Thornton International Limited (GTIL hereinafter). In its communication to NFRA, however, WCCL has maintained that it is not a member of the GTIL network.

Acknowledgment

11. NFRA acknowledges the cooperation of the Audit Firm during the inspection.

PART- B

Review of Firm-Wide Audit Quality Control System – Compliance with Previous Year’s Observations

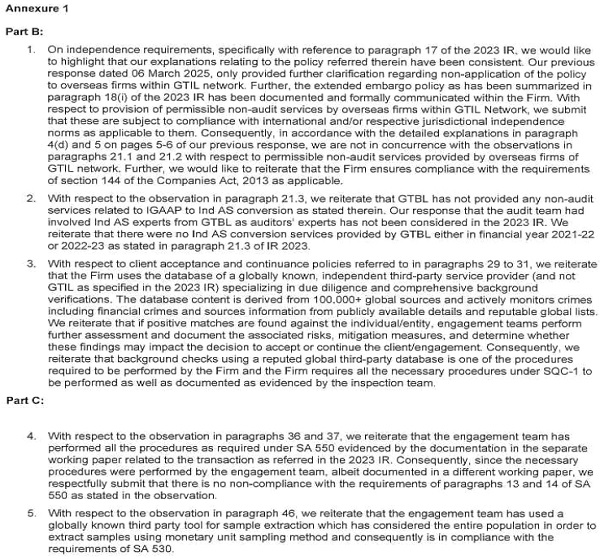

A. Independence Requirements:

12. Section 141(3) of the Act lays down the disqualifications for the appointment of the auditors of a company, aimed inter alia at ensuring the auditor’s independence vis a vis the auditee company. Similarly, section 144 of the Act lists the non-audit services that the auditors shall not render to the audited company, or its holding or subsidiary company, either directly or indirectly. The second explanation to section 144 states that the term “directly or indirectly” shall include rendering of services by the auditor, in case the auditor is a firm, either through itself, or through any of its partners, or through its parent, subsidiary, or associate entity or through any other entity, whatsoever, in which the firm or any partner of the firm has significant influence or control, or whose name or trademark or brand is used by the firm or any of its partners. Para 18 of SQC 1 requires the Audit Firm to establish policies and procedures designed to provide it with reasonable assurance that the firm, its personnel, and, where applicable, others subject to independence requirements (including experts contracted by the firm and network firm personnel) maintain independence.

As reported in IR 20222, WCCL is also a part of the international network called Grant Thornton International Limited (GTIL). In its communication to NFRA, however, WCCL has maintained that it is not a member of the GTIL network.

13. The IR 20223 stated that there was a direct or indirect relationship among WCCL4, WCAL5, GTBL6, GTAPL7, and GTIL8, classifying them as part of a “Network” in terms of SQC 1. Mr. Vinod Chandiok controls WCCL, while his son, Mr. Vishesh Chandiok, holds majority control in GTAPL and has significant influence over GTBL. The report concluded that GTAPL and GTBL are member firms of GTIL’s global network.

14. The IR 2022 also stated that WCCL had entered into agreements with GTAPL for the usage of audit software (Voyager) and with GTBL for staff hiring. Additionally, WCCL’s EQCM has multiple references to GTIL, use of GTIL policies, procedures, software, and reliance on GTIL’s process for confidentiality, working in a foreign jurisdiction, independence check, client acceptance & continuance, archival of audit files, assessments of cyber security plans, and sharing of manpower resources between WCCL & GTIL network firms.

15. During the Inspection of 2023, the inspection team observed additional instances that further corroborate that WCCL belongs to the GTIL network. These are:

a. WCCL ‘s arrangement with GTAPL for HRD infrastructure is a cost-sharing arrangement, which falls under the meaning of “Network” as per para 6(k)9 of SQC1.

b. The Key Audit Assignments (KAA) of WCCL required GTIL’s approval before accepting audit clients, as seen in the case of Company G for FY 2022-23. As per paragraph 3.103 of the Firm’s EQCM, GTIL’s Key Assurance Assignments acceptance & reacceptance policy is designed to identify and assess those assurance assignments of GTIL and its member firms that could present a significant risk to “Their Brand”. However, WCCL stated in its letter dated 06.03.2025 that client acceptance decisions are made independently by WCCL and its partners. The Firm’s reply is not satisfactory, as GTIL’s approval was sought for Company G’s audit assignment.

c. GTBL & WCCL share a common registered address (L-41, Connaught Circus, New Delhi) as per FORM -2 (Annual Report Form) filed with the PCAOB for the 2023 annual reporting.

d. As per PCAOB requirements, if the Firm is a foreign registered public accounting firm, it is required to designate to the Commission or Board an agent in the United States upon which the Commission or the Board may serve any request to the firm under section 106 of the Sarbanes-Oxley Act, 2002. The inspection team observed that both WCCL and GTBL had declared in their annual filing10 with PCAOB for FY 2022-23 that Grant Thornton LLP was their agent under section 106 of the Sarbanes-Oxley Act, 2002. Grant Thornton LLP is a part of the GTIL network, as declared by Grant Thornton LLP in their annual filing with PCAOB for FY 202223.

16. WCCL’s reply dated 28.09.2024 (Para 8) states that (a) WCCL has adopted a policy that they will not provide audit services to listed entities where GTBL, or any of their related entities, are providing non-attest services; and (b) GTBL and its related entities have also adopted a policy that they will not provide any non-attest services to the listed audit clients of WCCL in order to maintain complete independence and uphold ethical principles. WCCL stated that it ensures that neither GTBL nor WCAL has any relationship with an audit client (as defined under the Code)11 of WCCL or the holding company of such audit client, in case of unlisted companies, which could be perceived as impairing the independence of WCCL as auditors under the Code or which would lead to the rendering of any prohibited services as given under Section 144 of the Act.

17. Through reply dated 06.03.2025, WCCL mentioned that this policy applies only within India i.e. WCCL will not audit listed entities where GTBL or its related entities in India provide non-attest services. GTBL and its related entities in India will likewise not provide non-attest services to WCCL’s listed audit clients. WCCL further stated that this voluntary embargo does not extend to extra-territorial jurisdictions, more specifically to any other member firms of GTIL globally. However, this policy is not formally documented and is different from the earlier reply dated 28.09.2024 (Para16). As the latest reply restricts the application of the policy within India.

18. WCCL, by letter dated 06.03.2025, proposes the following voluntary actions to address NFRA’s concerns:

i. WCCL proposes extending the firm’s voluntary embargo on permissible non-attest services to all entities under Rule 3(1) of the NFRA Rules, 2018, in addition to listed companies, effective for engagements proposed on or after 1 April 2025. WCCL will also request GTBL and GTAPL to adopt and enforce this expanded policy.

ii. WCCL also proposes obtaining Audit Committee/Board approval, as per Section 144 of the CA 2013, for any attest services by GTBL or GTAPL to NFRA-governed audit clients of WCCL from 1 April 2025. A formal policy/process will be developed with GTBL and GTAPL to ensure implementation and compliance.

iii. WCCL proposes to establish a process to receive, collate, and monitor information on any non-audit services proposed/ provided by GTBL/ GTAPL to the audit clients of WCCL to demonstrate permissibility and completeness of its assertion, including in respect of our voluntary embargo policy.

iv. WCCL will incorporate the existing as well the proposed policies as a part of the Firm’s EQCM, communicate the decision to all partners and employees of the Firm and take adequate measures to ensure and monitor compliance with the same.

19. However, in the absence of any clear recognition by WCCL that all the network entities of GTIL of which they are a part, are needed to be considered while determining the compliance with the independence requirements, there is no assurance that WCCL complies with the independence requirements of the Companies Act 2013, the Code of Ethics and SQC1. The Firm should ensure full compliance with Section 144 of the Companies Act, 2013.

Sharing of Client details between WCCL & GTIL’s Network & Provision of Non-Audit services by the WCCL & its Network entities

20. The inspection team noticed through the International Relationship Checking (IRC) tool that GTBL and its related entities have provided non–attest services to the audit clients of WCCL despite their stated policy (Policy referred by letter dated 28.09.2024). These services provided by GTBL and its related entities to audit clients of WCCL have compromised WCCL’s independence as required by law. Some cases seen by the inspection team are discussed below.

21. The inspection team selected a sample of 13 cases to assess compliance with independence requirements. Of these 3 cases revealed instances where services provided by GTBL and its related entities to WCCL’s audit clients compromised WCCL’s independence, as detailed below.

(a) Services against WCCL’s stated policy (Policy referred by letter dated 28.09.2024) 21.1 In the case of Company A where the WCCL was the statutory auditor for the FY 2022-23, Overseas member firm of GTIL in Country A provided tax advisory services to Company B which is a subsidiary of Company A. The ET concluded in their assessment of International relationship conflicts (IRC) Check that tax advisory services provided by Overseas member firm of GTIL in Country A to Company B and similar services were also reported in earlier years; hence, there was no independence conflict. The ET’s assessment of the conflict in independence was not sufficient and also against the policy adopted by WCCL regarding non-attest services.

21.2 In the case of Company C, WCCL was the statutory auditor for FY 2022-23. Direct & indirect tax compliance services were provided by Overseas member firm of GTIL in Country B to Company D, a Step-down Subsidiary of Company C, in violation of the policy stated by WCCL. The ET, in its assessment of the international relationship conflicts (IRC Response), had concluded that tax compliance services provided by Overseas member firm of GTIL in Country B to Company D would not have any independence conflict as the ET providing assurance services was different from the ET providing tax compliance services. The ET’s assessment regarding independence was not sufficient and also violated the non–attest services policy adopted by WCCL.

The firm, by letter dated 06.03.2025, informed NFRA that the Firm’s voluntary embargo12 does not extend to extra-territorial jurisdictions, more specifically to any other member firms of GTIL globally. Hence, this embargo cannot be applied to such overseas firms. Accordingly, the engagement team was not required to include any documentation regarding the evaluation of independence threats resulting from the services provided by such overseas firms, i.e., other members of GTIL globally.

The firm’s contention is not acceptable. Being a part of GTIL’s network13, the firm is required to consider other member firms of GTIL for evaluation of independence, and self-interest threat is to be evaluated by treating the GT Global network as a single entity. Further, such relationships do not meet the test of independence in appearance.

Prohibited services covered u/s 144 of the Companies Act, 2013

21.3 For Company E, WCCL served as the statutory auditor for FY 2022-23. During this period, GTBL provided non-audit services related to IGAAP to Ind AS conversion adjustments (CFO Advisory), which are prohibited under section 144 of the Companies Act, 2013. This also contravened the policy adopted by WCCL/GTBL. The ET had incorrectly concluded that no conflict of interest existed.

The IR 2022 pointed out that the EQCM of WCCL did not prohibit certain non– audit services as outlined under section 144 of the Companies Act, 2013. These included:

(i) Investment advisory services

(ii) Investment banking services

(iii) Outsourced financial services

(iv) Management services

In response, WCCL stated in a letter dated 28.09.2024 that it had updated its EQCM to include the prohibited services previously omitted, as identified in the inspection report. However, despite these updates, the firm has continued to provide prohibited non-audit services.

The Firm, by letter dated 06.03.2025, informed NFRA that Company E had transitioned to Ind AS during the financial year ending 31.03.2022. Hence, the question of transition or conversion to Ind As does not arise for the year ended 31.03.2023.

In this regard, it is noted that WCCL had served as statutory auditor for Company E in both FY 2021-22 and 2022-23. Its independence was compromised due to GTBL providing IGAAP to Ind As conversion (CFO Advisory).

Engagement Team’s Independence

Sign-offs regarding Independence Confirmation were not obtained from the ET members

22. The IR 2022 highlighted some instances of non-compliance concerning independence declarations in e-audit files, involving the engagement teams (ET), engagement partners (EP), and engagement quality control review (EQCR) partners. During the present inspection period also NFRA noticed similar non-compliances in the case of three audit engagements. As brought out below, WCCL needs to strengthen its internal monitoring mechanism in this area.

23. The inspection team observed that in the case of Company G, while email confirmations for independence declarations were received from 43 individuals, only 13 out of 18 engagement team members had signed off in Voyager. For Company E, the independence declaration emails were not sent to all individuals involved with the engagement nor did all engagement team members sign off in Voyager. Only 8 out of 14 engagement team members had signed off in Voyager. Similarly, in Company H’s case, although independence declarations were received from 45 individuals, only 4 out of 28 members had signed off in Voyager. These examples show that gaps in the independence confirmation process continue to exist.

24. The Firm, by letter dated 06.03.2025, acknowledged the observation and stated that they have developed a new cloud-enabled audit documentation tool (LEAP) in a phased manner from the year ended 31.03.2024, which eliminates the issue relating to independence signoff. We will continue to monitor the progress made by the Audit Firm in subsequent inspection cycles.

B. Audit Documentation

25. The IR 2022 observed that the Audit Firm maintains audit documentation both electronically and in physical form (hard files). The audit documentation up to the time of its archival (within the 60-day timeframe stipulated in SQC 1) lacks integrity as required under Paras 77, 79, and 80 of SQC 1. The physical files are neither scanned and incorporated in the electronic files nor cross-referenced to the electronic files, making it difficult to demonstrate the completeness of the audit file and ascertain whether it was compiled within the 60-day timeframe stipulated in SQC 1.

26. The inspection team observed non-compliance pertaining to audit documentation stipulated in SQC1 in the case of Company A, Company E, Company G, Company H, and Company I, for the FY 2022-23.

27. The Firm, by letter dated 06.03.2025, stated to NFRA that it acknowledged that indexation and cross-references need to be further strengthened. The Firm also reiterated that electronic scanning of all original hard copy documents may not always be practical or feasible, especially when the volume and nature of the documents make it more suitable for engagement teams to maintain them in hard copy with necessary cross-references in the work papers.

28. This duality of audit documentation and the lack of integration between electronic and paper files poses risks of non-compliance with SQC 1 and other Standards on Auditing (SAs) and raises concerns about the reliability of audit documentation. It is recommended that, going forward, all hard-copy documents should be stored in the Voyager software before archival.

We will continue to monitor the Audit Firm for remediation of these lapses in subsequent inspection cycles.

29. Client Acceptance & Continuance Policies

29. The IR 2022 stated that the WCCL has a practice of requesting background checks on the auditee companies from a database of GTIL for integrity testing. Where background check responses from GTIL were not positive, the Firm did not perform any alternative procedures to assess the prospective/existing client’s integrity before accepting/continuing the audit engagement. The Firm’s reliance solely on a single source, GTIL, for assessing the integrity of client personnel is insufficient and does not fulfill the requirements of Para 28 of SQC 1.

30. The Firm stated in a letter dated 06.03.2025 that background checks are performed using a third-party service provider, and not by GTIL. The EQCM includes policies and procedures with respect to integrity considerations. The Firm also stated that in case where no positive match is found it signifies that no sanctions or adverse findings exist against the entity or individual being assessed.

31. The Firm’s response is unsatisfactory, as email correspondence reviewed by the inspection team confirms that the requisite information for background checks was shared with GTIL. Third-party service provider identified a positive match, which was communicated by GTIL to WCCL and subsequently evaluated by WCCL’s team. Further, the Firm considers only the positive matches, and no alternative procedures are performed to assess the prospective/existing client’s integrity before accepting/continuing the audit engagement in cases where no positive match is identified by third -party service provider.

We will continue to monitor the audit firm to remediate these lapses in subsequent inspection cycles.

D. Engagement Quality Control Review

32. As per IR 2022, there were some instances where EQCR review & sign-off were after the date of issue of audit report.

33. The EQCM of the Firm requires the EQCR partner to review and sign off on, at the minimum, some AWPs viz. Audit Plan and Risk Assessment, Summary of Significant Matters, Summary of Control Deficiencies, Financial Statement Disclosure Questionnaire and Audit Adjustments, etc.

The Firm stated that they have configured the audit software to require mandatory review & sign-off by the EQCR Partner. However, the inspection team observed that in three cases, (Company C, E, and H) the dates of EQCR signoff were after the date of the audit report.

34. The Firm, by letter dated 06.03.2025, stated that these delays in sign-off were only an account of certain administrative work performed on the engagement files. Further, for compliance with para 61 of SQC1 in the subsequent period the Firm will adopt new audit documentation software (LEAP) in a phased manner from the financial year ended 31 March 2024.

We will continue to monitor the Audit Firm for remediating these lapses in subsequent inspection cycles.

PART -C

Review of Individual Audit Engagement Files Focusing on Selected Areas of Audit

35. This section discusses deficiencies observed in a few selected audit engagements. The inspection covered three individual audit engagements and focused on three audit areas viz., related party transactions, internal control over financial reporting pertaining to revenue, and impairment of non-financial assets for detailed review. Certain critical audit procedures performed by the Firm’s engagement teams with respect to these audit areas were reviewed. The observations are discussed below-

A. Related Party Transactions

Company C

36. Related party transactions in respect of one related party disclosed by the company were not identified by ET in their audit work paper. The amount was greater than the performance materiality as per SA 320.

37. The Firm’s reply, dated 06.03.2025, stated that the documentation was appropriately maintained in a separate AWP but was inadvertently omitted from the related party transaction work paper. This omission constitutes non-compliance with the requirements of para 13 & 14 of SA 550 as the Firm failed to identify the related party transaction.

Company J

38. The Audit work paper (AWP) and financial statements reveal that loan amounting to ₹ 78.97 crore was given during the year to a subsidiary of Company J. However, this was not reported under clause iii (a) of CARO17 2020 despite exceeding the materiality threshold of ₹ 75.30 crore.

39. In response, the ET clarified that ₹78.51 crore out of the ₹78.97 crore represents the amount paid by the company to the bank on July 21, 2022, following the invocation of a guarantee for a Standby Letter of Credit (SBLC) issued on behalf of the subsidiary’s loan. This amount was subsequently recovered from a subsidiary. Although the transaction is properly reported in the related party disclosures as a loan given to a subsidiary and repaid by the subsidiary with a closing balance of NIL, the ET should have reported this under Clause iii(a) of CARO 2020.

40. The ET failed to perform arm’s length price testing for related party transactions (Loans, Investments, Borrowings, and Intercompany Revenue) as required by para 24 of SA 55018.

41. The Firm stated that Borrowings and Loans were raised from a fellow subsidiary at an interest rate of 12.25%, which was the company’s average borrowing rate. The company’s external borrowing rate from LIC was 12.15%, confirming an arm’s length transaction. Loans provided to group companies had interest rates ranging from 12.25% to 12.50%, indicating arm’s length terms for inter-corporate borrowings and loans.

42. We noted that the evaluations were not documented in their audit working papers, and there is no evidence supporting the stated average borrowing rate of 12.25. The inspection team also observed a loan from a subsidiary 19at a 0% interest rate, and a loan to a subsidiary20 at 8.50%, both were below the average borrowing rate and external borrowing rate from LIC.

Regarding investments, no valuation report was found in the audit file to support the fair valuation of a stake21in a subsidiary, contrary to ET’s claim.

B. Impairment of Non-Financial Assets

Company J

44. The ET did not enquire with management and identify whether any indicators of impairment for PPE as per IND AS 36 existed in order to determine the appropriateness of the planned substantive procedures in their AWP22. It is noted that the carrying amount of PPE as on 31.03.2023 was ₹ 88.49 crore, which is greater than materiality determined at ₹ 75.30 crore as per SA 320.

45. The Firm, by letter dated 06.03.2025, acknowledged the observation and stated that the documentation in this regard could have been more explicit and robust.

Company J

46. It was noted that while performing budget testing for Contract 1 and Contract 2, the ET selected 5 samples, which accounted for approximately 1 % of the total population size. The population stratification approach adopted by ET was inappropriate to enable greater audit effort towards the larger value items (Appendix I and para A8 of SA 530, Audit Sampling). The ET stated that they had applied monetary unit sampling (MUS), a value-weighted selection method. However, it was noted that they had failed to consider the large-value items despite applying MUS because they considered only the quantity i.e (a) Scope Total Qty, (b) Expected to be completed up to June 2022, and (c) Balance Total Qty (Scope Total Qty – Expected to be completed up to June 2022) without considering their respective budgeted rates. Hence, they failed to consider the monetary value of the transaction for the sample selection.

PART- D

Chronology of Events

| Sr. No | Date | Event/Correspondence |

| 1. | 29.12.2023 | Publication of Inspection Report 2022 on the website of NFRA as per Rule 8 of NFRA Rules 2018 |

| 2. | 26.03.2024 | Intimation of follow–up / thematic Inspection from NFRA to the Audit Firm |

| 3. | 05.04.2024 | Audit firm submitted three engagement files to the NFRA office |

| 4. | 30.04.2024

02.05.2024 13.06.2024 |

Briefing Meeting with WCCL held at NFRA office |

| 5. | July -August 2024 | Off-Site Inspection |

| 6. | 19.08.2024 | NFRA communication to Audit Firm regarding the Action taken in previous inspection observations |

| 7. | 02.08.2024

14.08.2024 21.08.2024 |

Communication of Engagement – Specific Observations |

| 8. | 11.09.2024 & 13.09.2024 | Response on engagement-specific observations received from the Audit Firm |

| 9. | 08.10.2024 to 10.10.2024 | On-site inspection & discussion of engagement observation with engagement teams |

| 10. | 04.02.2025 | Inspection Report sent by NFRA to the Audit Firm |

| 11. | 06.03.2025 | Submission of reply by WCCL to Draft Inspection Report |

| 12. | 26.03.2025 | Print Ready Version of Inspection Report sent by NRFA to Audit Firm |

| 13. | 28.03.2025 | Publication of Inspection Report on the website of NFRA as per Rule 8 of NFRA Rules 2018 |

Annexures

Annexure -1 The table below presents an overview of the firm’s profile provided by WCCL

| Date of Establishment | 01-01-1935 |

| Date of Conversion to LLP | 25-03-2014 |

| Registrations and empanelment | The Institute of Chartered Accountants of India Public Company Accounting Oversight Board Comptroller and Auditor General of India |

| Registered office | L-41, Connaught Circus, New Delhi-110001 |

| Number of partners* | 66 |

| Number of qualified staff* | 930+ |

| Number of trainees* | 490+ |

| Number of other employees* | 540+ |

| Total number of partners and staff | 2026+ |

| Number and Location of Offices* | 15 [Bengaluru, Chandigarh, Chennai, Delhi (2 offices including head office) Gurgaon, Hyderabad, Kolkata, Mumbai (2 offices), Noida, Pune, Kochi, Dehradun and Ahmedabad] |

| Audit clients of WCCL under the purview of Rule 3 of NFRA Rules | 293* |

*As of 31 March 2023

Firm’s response to this inspection report

Pursuant to Section 132(2) of the Companies Act, 2013 and Rule 8 of NFRA Rules, 2018, the Authority is publishing its findings relating to non-compliance with SAs and the sufficiency of the Audit Firm’s quality control system. As part of this process, the Audit Firm provided a written response to the Inspection Report, which is attached hereto. NFRA, based on the request of the Audit Firm, has excluded the information from this report which was considered proprietary.

–

Notes:

1 1. M/s Walker Chandiok & Co., LLP(WCCL) 2. M/s Walker Chandiok & Associates LLP(WCAL)

2 https://cdnbbsr.s3waas.gov.in/s3e2ad76f2326fbc6b56a45a56c59fafdb/uploads/2023/12/202312291554814653.pdf

3 Para 15 and 16 of Inspection Report 2022

4 M/s Walker Chandiok & Co., LLP

5 M/s Walker Chandiok & Associates LLP

6 Grant Thornton Bharat LLP

7 Grant Thornton Advisory Private Ltd

8 Grant Thornton International Ltd

9 Network – A larger structure: (i) That is aimed at cooperation, and (ii) That is clearly aimed at profit or cost-sharing or shares common ownership, control or management, common quality control policies and procedures, common business strategy, the use of a common brand name, or a significant part of professional resources

10 As per Form-2 filed with PCAOB by WCCL & GTBL for the period 2022-23

11 The code of ethics (Code) contains the following definition Audit client – An entity in respect of which a firm conducts an audit engagement. When the client is a listed entity, the audit client will always include its related entities. When the audit client is not a listed entity, the audit client includes those related entities over which the client has direct or indirect controls. (see also paragraph R400.20) In part 4A, the term “audit client” applies equally to “review client”. Related entity – An entity that has any of the following relationships with the client: (a) An entity that has direct or indirect control over the client if the client is material to such entity; (b) An entity with a direct financial interest in the client if that entity has significant influence over the client and the interest in the client is material to such entity; (c) An entity over which the client has direct or indirect control; (d) An entity in which the client, or an entity related to the client under (c) above, has a direct financial interest that gives it significant influence over such entity and the interest is material to the client and its related entity in (c); and (e) An entity which is under common control with the client (a “sister entity”) if the sister entity and the client are both material to the entity that controls both the client and sister entity.

12 WCCL has adopted a policy that the firm will not provide audits to listed entities where GTBL or any of its related entities in India are engaged to provide non – attest services. GTBL and its related entities in India have also accepted and adopted a policy that they will not provide any non-attest services to the listed audit clients of WCCL.

13 Section 144 of the Act lists the non-audit services that the auditors shall not render to the audited company, or its holding or subsidiary company, either directly or indirectly. The second explanation to section 144 states that the term “directly or indirectly” shall include rendering of services by the auditor, in case the auditor is a firm, either through itself, or through any of its partners, or through its parent, subsidiary, or associate entity or through any other entity, whatsoever, in which the firm or any partner of the firm has significant influence or control, or whose name or trademark or brand is used by the firm or any of its partners.

17 The Companies (Auditor’s Report) Order, 2020

18 SA 550 Related parties

19 Subsidiary L of Company J Ltd

20 Subsidiary M of Company J Ltd

21 Subsidiary O of Company J Ltd

22 Voyager>Respond to risks>Respond to risks PPE including intangible