Learning Outcomes

> Understand meaning and scope of intangible assets.

> Recognise the criteria.

> Examine mode of acquisition.

> Measure intangible assets at initial recognition.

> Measure intangible assets after recognition.

> Evaluate amortization and useful life of intangible asset.

> De-recognition and comply with disclosure requirements of the standard.

> De-recognition and comply with disclosure requirements of the standard.

Although intangible assets are not a physical asset, they can be equally valuable for a company for its long-term success or failure. Companies from industries like IT, Consumer products, Telecom, Banking. spend a lot of money in building these intangible assets from which they expect to benefit in the future. For IT industry, training and recruiting are more prominent than investing in physical assets, Consumer product companies like Hindustan Unilever, Godrej, Colgate, Coca-Cola are highly successful because of the significant brand equity. Technology companies like Apple, Infosys, TCS, etc are successful because of their technical know-how and skilled human resource. Banking companies have invested a lot in intangible assets in form of software license, electronic trading platform.Telecom companies like Reliance Jio earn profits by their bandwidth licenses. Now the question is Intangible assets are to be recorded on the balance sheet or as an expense in profit and loss account as the costs incurred now will be matched with revenues in the future.In this article, you’ll find the short summary of the main rules in IND-AS 38 Intangible assets.

Page Contents

- What is an intangible asset?

- What assets are covered by IND-AS 38?

- When can we recognize an intangible asset?

- How to measure intangible assets?

- What about the measurement after recognition?

- How useful life of Intangible assets is determined and how are these amortized ?

- When and How to account for impairment?

- When to derecognize intangible assets?

- What Disclosures are required to be made in case of Intangible assets?

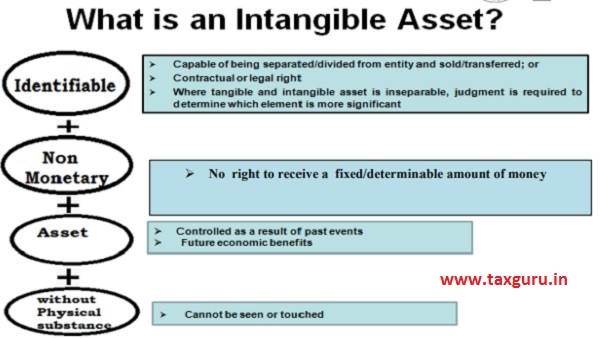

What is an intangible asset?

An intangible asset is an identifiable non-monetary asset without physical substance.

That’s the definition from IND-AS 38.People can interpret this definition in many different ways, just as they need and therefore, IAS 38 contains a good guidance on how to apply it.

What assets are covered by IND-AS 38?

The standard applies to all intangible assets except for the intangible assets covered by another standards.

- Intangible assets held for sale in ordinary course of business(IND AS 2)

- Deferred tax assets – covered by IND-AS 12,

- Goodwill arising in a business acquisition– covered by IND-AS 103

- Leases(IND-AS 17)

- assets arising form employee benefits(IND-AS 19

- Intangible assets held for sale – covered by IND-As 105Non-Current intangible Assets classified as Held For Sale,

- Financial assets – covered by IND-AS 32 Financial Instruments: Presentation

- Exploration and evaluation assets – covered by IND-AS 106 Exploration for and Evaluation of Mineral Assets,

- Expenditures for development and extraction of minerals, oils, natural gas and other non-regenerative resources, etc.

When can we recognize an intangible asset?

Sometimes it can happen that item meets all the criteria of an intangible asset, but still cannot be recognized in financial statements as it does not meet the recognition criteria.

You can recognize an intangible asset only when:

1. Future economic benefits from the asset are probable;

2. Cost can be measured reliably.

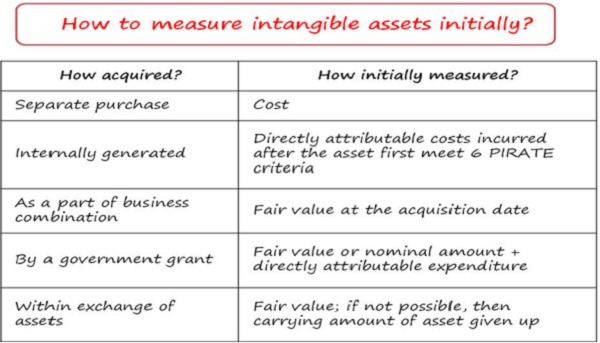

How to measure intangible assets?

> Measurement of intangible assets at initial recognition(Dependent on Mode of Acquisition)

> Measurement of intangible assets after recognition

Notes:

> Cost of separately acquired asset comprises purchase price including import duties and non-refundable purchase taxes and directly attributable cost of preparing the assets for its intended use.

> In case of internally generated assets,

1. Expenses incurred on research are not to be capitalised and need to expense it in profit or loss as incurred.

2. Expenses incurred on development are to be capitalised if following criteria is met

♦ Probable future economic benefits,

♦ Intention to complete and use or sell the asset,

♦ Resources adequate and available to complete and use or sell the asset,

♦ Ability to use or sell the asset,

♦ Technical feasibility,

♦ Expenditures can be reliably measured.

3. Internally generated goodwill is not capitalised.

4. Other intangible assets, like brands, customer lists, publishing titles, mastheads or similar. are also not to be capitalised as it’s hard if not impossible to measure their cost reliably.

What about the measurement after recognition?

An entity can chose from 2 models:

1. Cost model: The intangible asset is carried at its cost less accumulated amortization (similar as depreciation) less any accumulated impairment loss.

2. Revaluation model: The intangible asset is carried at its fair value at the revaluation date less accumulated amortization less any accumulated impairment loss.

For applying revaluation model for intangible assets there must be an active market – which is rare.Also for brands, mastheads, patents, trademarks and similar assets , revaluation model is inapplicable as these assets are very specific and unique and there’s no active market.

How useful life of Intangible assets is determined and how are these amortized ?

> In case asset has Finite useful life : Depreciate amount of intangible asset with a finite useful life allocated on systematic basis over its useful life. Amortisation is usually recognised in profit and loss account.

> In case asset has an Indefinite useful life: Do NOT amortize it..However it is necessary to revise the asset’s useful life at the end of each financial year and seek for impairment.

When and How to account for impairment?

IND AS 36 explains how and when an entity reviews the carrying amount of its assets, how it determines the recoverable amount and when it recognises or reverses an impairment loss. In case of intangible assets with indefinite life ,impairment review is required at least annually.

When to derecognize intangible assets?

The intangible asset is derecognised either:

- When it is dispose of(sale/financial lease/donation etc.),or

- When no more future economic benefits are expected from the asset.

The gain or loss on derecognition of intangibles is determined as:

- Net disposal proceeds, less

- Asset’s carrying amount

Gain or loss are recognized in profit or loss and not classified as revenue.

What Disclosures are required to be made in case of Intangible assets?

For each class of intangible asset distinguishing internally generated and other intangibles:

√ Whether useful lives are definite or indefinite

√ Useful lives or amortization rate and method used

√ Gross carrying amount and accumulated amortization at the beginning and at the end of the period

√ Reconciliation of carrying amount at the beginning and at the end of the period

√ Amount of R & D expensed out

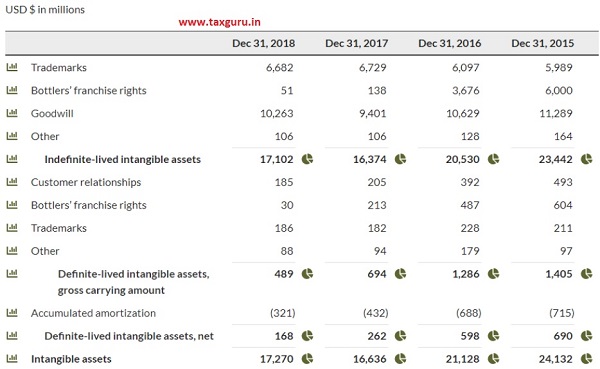

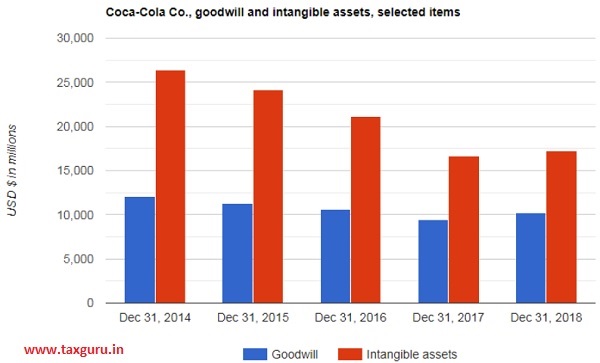

Disclosures of Intangible Assets: Coca Cola Ltd.

Coca-Cola Company (KO) is an example of an intangible asset with the value of its highly recognized brand name is virtually inestimable and is a critical driver in the Coca-Cola Company’s success and earnings.

Source: NYSE

Source: NYSE

Coca-Cola Co.’s goodwill declined from 2016 to 2017 but then increased from 2017 to 2018 not reaching 2016 level. Coca-Cola Co.’s intangible assets declined from 2016 to 2017 but then slightly increased from 2017 to 2018.

Author Bio