Deeksha Sharma

With the expansion of technology many companies have now started to compete on a global scale by providing or availing the services across the borders. In this article we will discuss the implications of GST on import of services from related persons:

As per Section 7(1)(b) of CGST Act, 2017

Supply includes import of services for a consideration whether or not in the course or furtherance of business.

However, clause 4 of schedule 1 of CGST Act, 2017 which provides consideration is not required if

Import of services by a taxable person from a related person or from any of his establishments outside India in the course or furtherance of business.

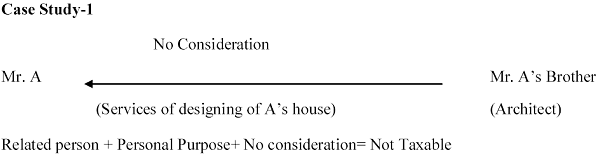

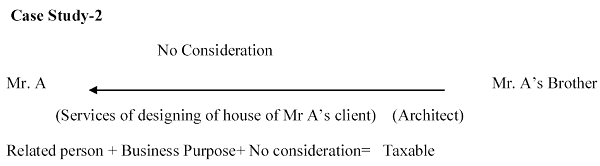

Analysis: Import of services from unrelated person would be taxable only if consideration is involved. However, services imported in the course or furtherance of business from a related person would be taxable even if no consideration is involved.

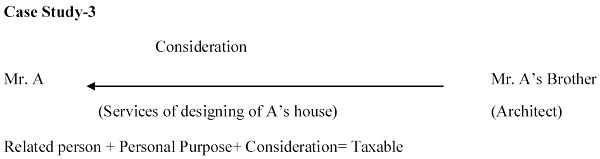

In other words, services imported from related person for personal purpose would be taxable only if consideration is involved.

Let us understand the above analysis by the following case studies:

For the ease of understanding the above provisions have been tabulated below:

| Driving factors | Related Person | Unrelated Person |

| Consideration + Furtherance of Business | Taxable | Taxable |

| Consideration+ Personal Purpose | Taxable | Taxable |

| No Consideration + Furtherance of Business | Taxable | Not Taxable |

| No Consideration+ Personal Purpose | Not Taxable | Not Taxable |

Conclusion: Provisions related to GST for import of service from related person is very harsh as it will cover all the transactions even if consideration is not involved. Valuation will be a major problem for such cases and it may lead to litigation also. Companies need to be more cautious while availing any consultancy or support services from any of their establishment located outside India as it would be covered under the ambit of GST.

Great Analysis.

What about the exemption provided under Serial no. 10 of the IGST Notification 9/2017 which states that services received from a provider of service located in NTT by an individual in relation to any purpose other than commerce, industry or any other business or profession is exempt, i.e. import of services for personal purpose is exempt acc. to this notification.