Case Law Details

A V B Handling Vs C.C.E. & S.T (CESTAT Ahmedabad)

CESTAT Ahmedabad held that as the service charges are based on metric tons of the goods handled and not on the basis of wages of laborers deployed for the job, the activity of the loading, unloading of goods at port, cutting of bags, spreading of zola, cleaning of jetty is classified under Cargo Handling Service.

Facts- The appellant are engaged in providing the cargo handling service at Kandla Port to its various clients. The service includes loading, unloading of goods at port, cutting of bags, spreading of zola, cleaning of jetty. The appellant are paying service tax under the category of cargo handling services on 75% of the value of the service. The case of the department is that the appellant have deputed his labour for the aforesaid work, hence, the service is classifiable under Manpower Recruitment or Supply Agency Service u/s. 65(105). Accordingly, the demand for differential service tax amounting to Rs. 14,92,988/- was raised.

Conclusion- Held that the appellant have been charging their service charges on the basis of metric tons of the goods handled by them and not on the basis of wages of laborers deployed for the job. The above invoices supported the claim of the appellant that the service was correctly classifiable under cargo handling service and not under Manpower Recruitment or Supply Agency Service.

Held that the appellant’s service is correctly classifiable under cargo handling service as claimed by the appellant and not under manpower recruitment or supply agency service as alleged by the Revenue.

FULL TEXT OF THE CESTAT AHMEDABAD ORDER

The brief facts of the case are that the appellant are engaged in providing the cargo handling service at Kandla Port to its various clients. The service includes loading, unloading of goods at port, cutting of bags, spreading of zola, cleaning of jetty. The appellant are paying service tax under the category of cargo handling services on 75% of the value of the service. The case of the department is that the appellant have deputed his labour for the aforesaid work, hence, the service is classifiable under Manpower Recruitment or Supply Agency Service under Section 65(105). Accordingly, the demand for differential service tax amounting to Rs. 14,92,988/- was raised.

2. Shri Abhishek Doshi, Learned Chartered Accountant appearing on behalf of the appellant submits that the job performed by the appellant is loading, unloading of goods at port, cutting of bags, spreading of zola, cleaning of jetty etc. at Kandla port to various clients. The said service is correctly classifiable under Cargo Handling Service. He submits that merely because the appellant have deputed some manpower for performing his job to the client, the department has wrongly interpreted that the appellant had provided the Manpower Recruitment or Supply Agency Service. It is his submission that the contract with their client is on work basis and not on the basis of labour deputed for the job. The client is concerned with the particular job and not concerned with the number/skill of labour deployed for the job. He also submits that the control of the manpower is undisputedly with the appellant and not with the service recipient, therefore, the service is not classifiable under Manpower Recruitment or Supply Agency Service. He also refers to the confirmation letter from the various clients regarding nature of service whereby he submits that the service which the appellant had provided is particularly work at port and not Manpower Recruitment or Supply Agency Service to the client. He submits that on the identical issue in various decisions it was held that the service will not be classifiable under Manpower Recruitment or Supply Agency Service. He placed reliance on the following judgments:-

- M/s. Ritesh Enterprises & Karwar Dock & Port Labaour Cooperative Society Ltd – 2010-TIOL-539-CESTAT-BANG

- K. Damodarareddy – 2010 25 STT 69 (CESTAT- BANG)

- M/s. Divya Enterprises – 2009- TIOL-2476-CESTAT-BANG

- S. S Associates – 2010(24) STT 592 (BANG-CESTAT)

- Loomtex Exports – 2014 (306) E.L.T. 294 (Mad.)

2.1. He further submits that the demand was raised for the period 20062007 to 2010-2011 by issuing show cause notice dated 26.09.2011 invoking the extended period. It is his submission that since the appellant was registered with service tax department and was paying service tax on the same service under cargo handling service, there is no suppression of fact, therefore, the extended period could not have been invoked.

3. Shri Ajay Kumar Samota, Learned Superintendent (AR) appearing on behalf of the revenue reiterates the finding of the impugned order.

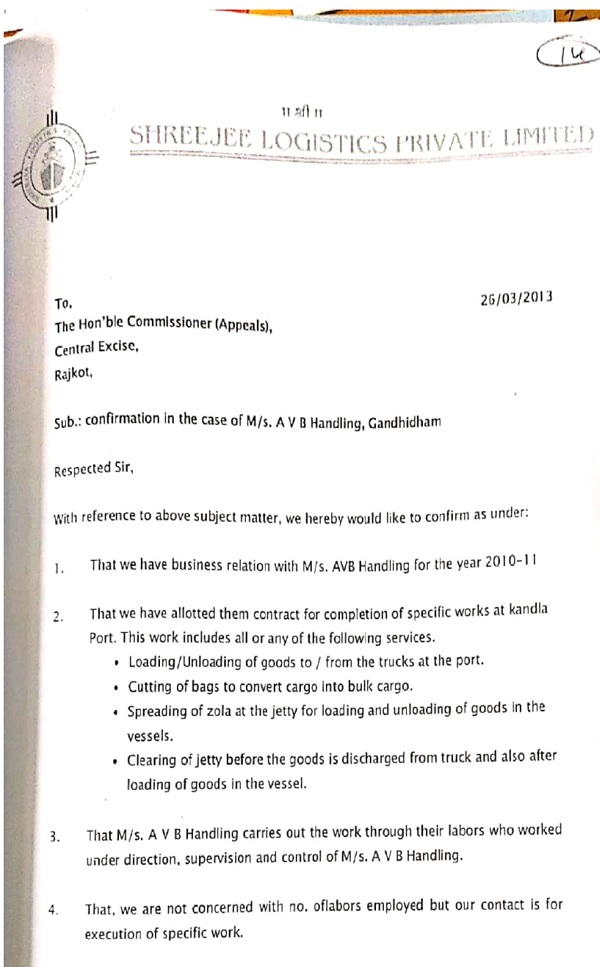

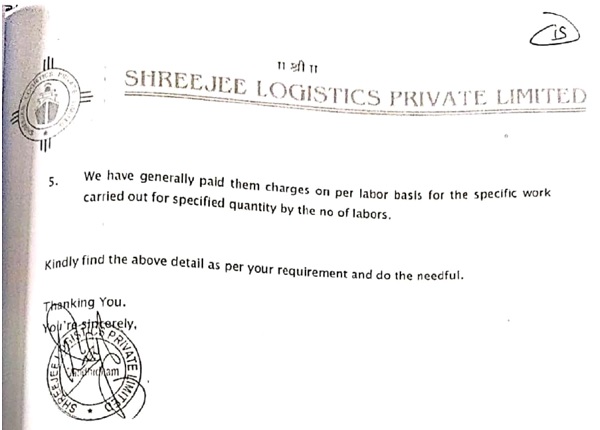

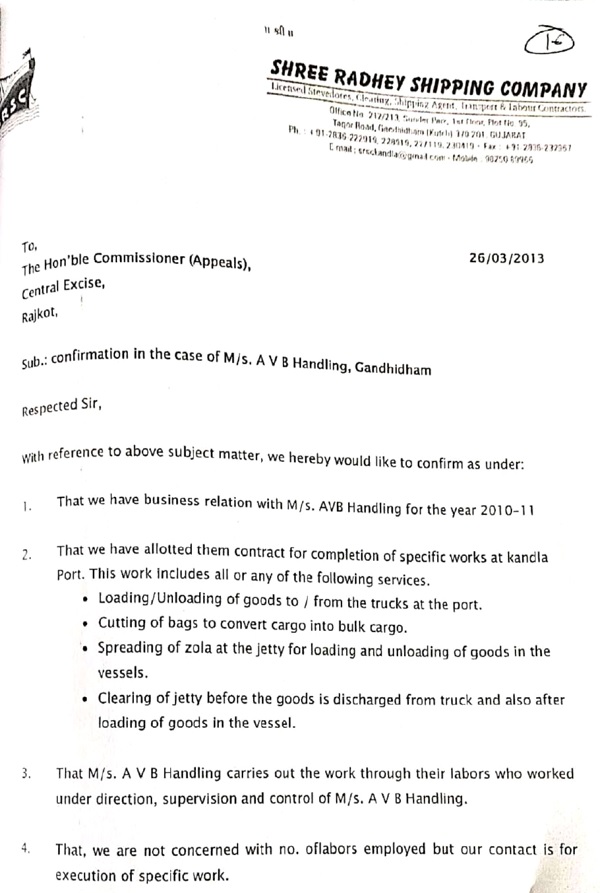

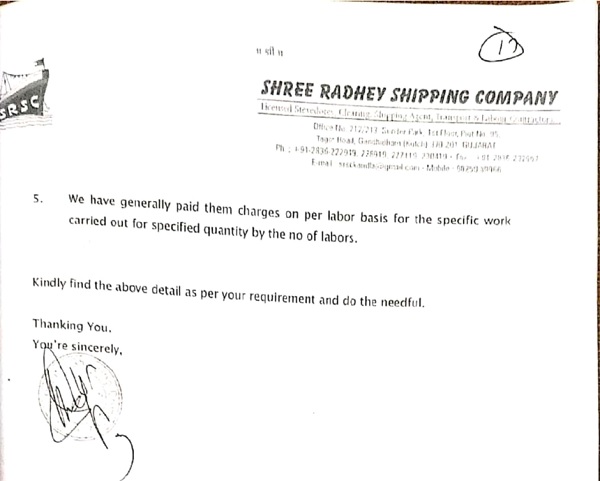

4. We have carefully considered the submission made by both sides and perused the records. We find that the issue in the present case, as per revenue is that the appellant have provided the Manpower Recruitment or Supply Agency Service to their client. To ascertain the actual nature of service we refer to the letter of the client. Some sample letters are given below:-

–

–

–

–

From the above letter it is absolutely clear that the appellant have undertaken the specific work at Kandla Port such as:-

- Loading/unloading of the goods to/from the trucks at the port

- Cutting of bag to convert cargo into bulk cargo

- Spreading Zola at the jetty for loading and unloading of goods in the vessels.

- Cleaning of jetty before the goods discharged from the trucks and also after loading of the goods in the vessels.

4.1 From the above nature of works it is clear that the appellant have not provided the Manpower Recruitment or Supply Agency Service but they only performed the job as required by their client. It is also clear from the letter that the supervision and control of the manpower deputed for the aforesaid job was with the appellant and thus the client was not concerned about the number of manpower, type of manpower, Man hour etc. Therefore, the nature of work is cargo handling service provided at the port and not Manpower Recruitment or Supply Agency Service.

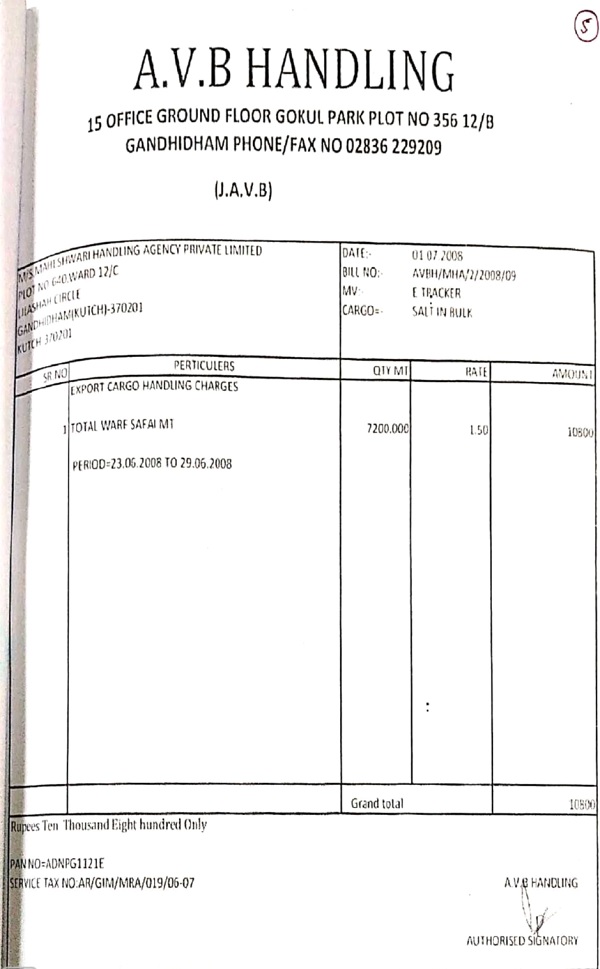

4.2 We further noticed from the invoices of the appellant raised to their client that the service is not of manpower recruitment or supply agency service. In this regard the sample of invoices are reproduced below:-

–

–

4.3 From the above sample invoices, it is clear that the appellant have been charging their service charges on the basis of metric tons of the goods handled by them and not on the basis of wages of laborers deployed for the job. The above invoices supported the claim of the appellant that the service was correctly classifiable under cargo handling service and not under Manpower Recruitment or Supply Agency Service. The appellant have admittedly paid service tax on cargo handling services except in case of export of cargo which is not taxable.

4.4 The identical issue has been considered in various judgments wherein it was viewed that in case the contract is for a job and not for supply of manpower their services cannot be classifiable under manpower recruitment or supply agency service. Some of the judgments are reproduced below:-

- M/s. Ritesh Enterprises & Karwar Dock & Port Labaour Cooperative Society Ltd – 2010-TIOL-539-CESTAT-BANG

“6. We have considered the submissions made at length by both sides and perused the records. The question that arises for consideration is whether the services rendered by the appellants are classifiable under the heading “manpower recruitment & supply agency”?

7. The definition of the manpower recruitment or supply agency under Section 65(105) reads as under :-

“any commercial concern engaged in providing any service, directly or indirectly, in any manner for recruitment or supply of manpower, temporarily or otherwise, to a client.”

The taxable service liable for Service tax is also defined under Section 65(105)(K) which is as under :

“any service provided to a client, by a manpower recruitment or supply agency in relation to the recruitment or supply of manpower, temporarily or otherwise, in any manner.”

From the plain reading of the above reproduced definitions in the Finance Act, 1994, we find that the activity should be providing of any service directly or indirectly in any manner for recruitment or supply of man-power temporarily or otherwise to a client in order to get covered under the said definition. There should be either a recruitment or supply of manpower temporarily or otherwise.

We find from the records that M/s. Aspin Wall & Co. had given the contract as under :

“Work Order No. 005/RE/2004-05 dated 20-11-2004

M/s. Ritesh Enterprises,

Vjaya Mahal

Surathkal 594158.

Dear Sir,

Godown handling operation at our Bagging Plant, Maroli

We refer to work order of even number dated 20-11-2003 and further Discussions had with you on the handling of bulk bagged fertilizers in our Bagging Plant. We have pleasure in awarding you the handling job for a period of further two years as per the following rates, terms and conditions :

Inside the Plant :-

| Feeding bags for filling bulk, stitching shifting bagged cargo and Stacking | Rs.13.75 per mt |

| De stacking and loading bagged cargo on to long trucks | Rs.06.00 per mt |

| De stacking and loading onto trucks for wagon loading | Rs.09.00per mt |

| High stacking above 15 tier | Rs.03.00 per mt |

| Employment of casuals for tipper cleaning, and in the plant, Providing shovels buckets etc | Rs.03.00 per mt |

| Service charges | Rs.03.50per mt |

Side godowns :

| Unloading and stacking wagon cargo | Rs.12.75 per mt |

| Dc stacking and loading | Rs.10.00per mt |

| Re standardization of c/t

bags |

Rs. 25.00per mt

|

| Casuals for sweeping collection | Rs. 00.50permt

|

| Service Charges | Rs. 03.00per mt |

Gunny handling

| Unloading HDPE Bales | Rs. 04.00per bale |

| Reloading of HDPE ales | Rs. 04.00per bale |

1. The rates given above shall be firm without any escalation during the tenure of this work order. However the company reserves its right to extend the same for further period on mutual agreement.”

2. The company is at liberty to enter into parallel contract with any other party, if required.

3. The overall interest of the company should be safeguarded by you and loss/damage to the company due to your negligence/fault shall be recovered from you.

4. Proper accounts of the cargo/empty bags shall have to be furnished to us on completion of each operations.

5. You have to arrange round the clock work in the Plant and keep in touch with our officials, supervisors for better coordination in arrival of bulk prompt standardization etc.,

6. The labour utilized by you for the handling operations under this work order shall be treated as your employees and the company shall have no responsibility whatsoever in this regard. You shall comply with all statutory requirements, government regulations etc. and shall fully indemnify the company against any claims arising as a result of your failure to comply with such formalities.

7. Only 90% of the charges at the maximum will be paid to you for the completed work on weekly basis. The balance shall be released on satisfactory completion of the work shipwise/commodity wise and on your submitting the relevant bills. The company shall deduct 5% from your bills towards security deposit and the same shall be kept in your running account till a total security of 1.5 lakhs is maintained.

8. The Company reserves its right to terminate this work order without assigning any reason by giving you one week’s notice.

Please sign and return duplicate copy of this work order as a token of your acceptance of the rates terms and conditions mentioned hereinabove.”

Contract awarded by Central Warehousing Corporation is as under :

“No. H-700 (22) MLR-RI/2005/6473

Date 28-12-2004

M/s. Ritesh Enterprises

Vijay Mahal,

Suratkal-574158.

Sub : Appointment of H&T contract on adhoc basis at CW. Mangalore – Reg.

Ref: 1. Tender No CWC/BLR/H-700(22)/04 dated 7-10-2004

2. Telegram dated 27-12-2004.

Sir,

Please refer to your tender referred above submitted and opened on 18-10-2004 and negotiations had on 23-12-2004 at this office for adhoc handling and transport contract at Central Warehouse, Mannangudda, Mangalore.

We are pleased to award the contract at the above centre with effect from 1-12005 for a period of 3 (three) months with a provision to extend for a further period of three months at the following negotiated rate :-

1. Handling Services, Above Schedule of Rates (Appendix VI) : 162% (one hundred sixty-two percent);

2. Transportation to and from goodshed to Warehouse and vice versa: Rs. 54/- (Rupees fifty four only) per MT ONLY ON POINT TO POINT BASIS.

3. Internal Transportation : Rs. 20/- (rupees twenty only) per MT only on point to point Basis.

You are advised to comply with the following requirements by 31-12-2004 :-

1. Execute an agreement on a stamp paper of appropriate value but not less than Rs. 100/- as per the latest stipulation of Government of Karnataka along with two witnesses to the agreement.

2. The Security Deposit of Rs. 60,000/- (Rupees sixty thousand only) in the form of Demand Draft.

3. Obtain the license under Contract Labour (R&A) Act, 1970 from the concerned – RLC(C)/ALC(C) in case 20 or more labourers are engaged on any day during the tenure of the contract.”

8. As regards the works executed by the appellant M/s. Karwar Dock & Port Labour Cooperative Society Ltd., we find from the records and the documents produced before us that they were intimated about the berthing of vessels at various ports and they were given a lump sum contract for cargo handling i.e. loading and unloading of the goods into the said vessels. We perused the invoices issued by the appellant M/s. Karwar Dock & Port Labour Cooperative Society Ltd., which is annexed at Page Nos. 170 and 171 of the appeal memoranda and noted that the invoices are raised as “cargo handling for granite export loading of Indian rough granite blocks” for a lump sum amount, charged per Metric Tonne.

9. On a careful consideration of the above reproduced facts from the entire case papers, we find that the contract which has been given to the appellants is for the execution of the work of loading, unloading, bagging, stacking destacking etc., In the entire records, we find that there is no whisper of supply manpower to the said M/s. Aspin Wall & Co. or to CWC or any other recipient of the services in both these appeals. As can be seen from the reproduced contracts and the invoices issued by the appellants that the entire essence of the contract was an execution of work as understood by the appellant and the recipient of the services. We find that the Hon’ble Supreme Court in the case of Super Poly Fabriks Ltd. v. CCE, Punjab (supra) in paragraph 8 has specifically laid down the ratio which is as under :

“There cannot be any doubt whatsoever that a document has to be read as a whole. The purport and object with which the parties thereto entered into a contract ought to be ascertained only from the terms and conditions thereof. Neither the nomenclature of the document nor any particular activity undertaken by the parties to the contract would be decisive.”

An identical view was taken up by Hon’ble Supreme Court in the case of State of A.P. v. Kone Elevators India Ltd. (supra) and UOI v. Mahindra and Mahindra in a similar issues. The ratio of all the three judgments of the Hon’ble Supreme Court, is that the tenor of agreement between the parties has to be understood and interpreted on the basis that the said agreement reflected the role of parties. The said ratio applies to the current cases in hand. We find that the entire tenor of the agreement and the purchase orders issued by the appellants’ service recipient clearly indicates the execution of a lump-sum work. In our opinion this lump-sum work would not fall under the category of providing of service of supply of manpower temporarily or otherwise either directly or indirectly.

10. On perusal of the records and the submissions of learned SDR on the Master Circular dated 23-8-2007, we find that the issue is raised at clause 010.02 is as under :

|

Business or industrial organizations engage services of manpower recruitment or supply agencies for temporary supply of manpower which is engaged for a specified period or for completion of particular projects or tasks. Whether Service tax is liable on such services under Manpower recruitment or supply agency’s services?

|

In the case of supply of manpower individuals are contractually employed by the manpower recruitment or supply agency. The agency agrees for use for the services of an individual, employed by him to another person for a consideration.

Employer-employee relationship in such case exists between the agency and the individual and not between the individual and the person who uses the services of the individual.

Such cases are covered within the scope of the definition of the taxable service Section 65(105)(k) and, since they act as supply agency, they fall within the definition of “manpower recruitment or supply agency” Section 65(68) and are liable to service tax. |

11. It can be seen from the above reproduced portion of the Master Circular that it is in respect of supply of manpower which is engaged for specified period or for completion of particular projects or tasks. The clarification, is in case of supply of man power, it can be seen that the clarification specifically reads that the agency agrees for use of services of an individual to another person for a consideration as supply of manpower. In the cases in hand, there is no agreement for utilization of services of an individual but a job/lump-sum work given to the appellants for execution. The said clarification issued by the Board would be appropriate in the case where services of man power recruitment & supply agency, had been temporarily taken by the Business or the industrial association for supplying of manpower and may/may not be for execution of a specific work. We are of the considered view that the reliance placed by the learned SDR and the learned Commissioner on the circular will not carry the case of the Revenue any further.

12. Accordingly in view of the above findings, we are of the view that the impugned orders are liable to be set aside and we do so. The appeals are allowed with consequential relief if any. Since we have disposed of the appeals on merits itself, no findings are recorded on other submissions made by both sides in these appeals.”

- M/s. Divya Enterprises – 2009- TIOL-2476-CESTAT-BANG

“6. We have considered the submission is made at length by both sides and perused the records. The question that arises for consideration is whether the services rendered by the appellant are classifiable under the heading “manpower recruitment & supply agency”?

7. The definition of the manpower recruitment or supply agency under Section 65(105) reads as under :-

“any commercial concern engaged in providing any service, directly or indirectly, in any manner for recruitment or supply of manpower, temporarily or otherwise, to a client.”

The taxable service liable for Service tax is also defined under Section 65(105)(k) which is as under :

“any service provided to a client, by a manpower recruitment or supply agency in relation to the recruitment or supply of manpower, temporarily or otherwise, in any manner.”

From the plain reading of the above reproduced definitions in the Finance Act, 1994, we find that the activity should be providing of any service directly or indirectly in any manner for recruitment or supply of man-power temporarily or otherwise to a client in order to get covered under the said definition. There should be either a recruitment or supply of manpower temporarily or otherwise. We find from the records that M/s. Aspin Wall & Co. had given the contract as under :

“W.O. No . 004/03-04

M/s. Divya Enterprises,

Bykampady,

Mangalore

Dear Sirs

We refer to the various discussions we had with your partners regarding the godown handling operations at Bykampady location. Accordingly, we are pleased to award you the godown handling work in the following godowns with retrospective effect from the handling of my MARIUPOL that arrived new Mangalore Port on 3-10-2003.

BALENJA/SOMAYAJI/PORT WORKSHOP godowns

|

Filling bulk fertilizers into bags, weighing, standardization stacking, and reloading to trucks |

Rs. 47.50 per mt.

|

| High stacking above 15 height | Rs. 5.00 per mt. |

| Unloading bagged cargo from wagons and reloading (each operation) Truck/godown cleaning casuals, tarex mamool etc., at Actual as certified by our godown supervisor. | Rs. 16.00 mt.

|

| Socks & gloves for urea at actuals Bale unloading if full truck load unloaded | Rs. 5.00 per bale

|

| Restandardisation of bags | Rs. 25 00 per mt.

|

| Service charges | Rs. 3.00 per mt. |

The rates given above shall be firm without any escalation during the tenure of this work order. However the company reserve its right to extend the same for farther period on mutual agreement.”

The company is at liberty to enter into parallel contract with any other party, if required.

The overall interest of the company should be safeguarded by you and loss/damage to the company due to your negligence/fault shall be recovered from you.

Please sign and return duplicate copy of this work order as a token of your acceptance of the rates terms and conditions mentioned hereinabove.”

9. On a careful consideration of the above reproduced letter and facts from the entire case papers, we find that the contract which has been given to the appellants is for the execution of the work of loading, unloading, bagging, stacking destacking etc., In the entire records, we find that there is no whisper of supply manpower to the said M/s. Aspin Wall & Co. or any other recipient of the services in both these appeals. As can be seen from the reproduced contracts and the invoices issued by the appellant that the entire essence of the contract was an execution of work as understood by the appellant and the recipient of services. We find that the Hon’ble Supreme Court in the case of Super Poly Fabriks Ltd. v. CCE, Punjab (supra) in paragraph 8 has laid down the ratio which is as under :

“There cannot be any doubt whatsoever that a document has to be read as a whole. The purport and object with which the parties thereto entered into a contract ought to be ascertained only from the terms and conditions thereof. Neither the nomenclature of the document nor any particular activity undertaken by the parties to the contract would be decisive. “

An identical view was taken by Hon’ble Supreme Court in the case of State of AP v. Kone Elevators (India) Ltd. (supra) and UOI v. Mahindra and Mahindra (supra) in a similar issue. The ratio of all the three judgments of the Hon’ble Supreme Court, is that the tenor of agreement between the parties has to be understood and interpreted on the basis that the said agreement reflected the role and understanding of the parties. The said ratio applies to the current case in hand. We find that the entire tenor of the agreement and the purchase orders issued by the appellants’ service recipient clearly indicates the execution of a lump-sum work. In our opinion this lump-sum work would not fall under the category of providing of service of supply of manpower temporarily or otherwise either directly or indirectly.

10. On perusal of the records and the submissions of learned SDR on the Master Circular dated 23-8-2007, we find that the issue raised at clause 010.02 is as under :

|

Business or industrial organizations engage services of manpower recruitment or supply agencies for temporary supply of manpower which is engaged for a specified period or for completion of particular projects or tasks. Whether Service tax is liable on such services under manpower recruitment or supply agency’s ser ices

|

In the case of supply of manpower individuals are Contractually employed by the Manpower recruitment or supply agency. The agency agrees for use for the services of an individual, employed by him to another person for a consideration. Employer employee relationship in such case exists between the agency and the individual and not between the individual and the person who uses the services of the individual.

Such cases are covered within the scope of the definition of the taxable service (Section 65 (105)(k) since they act as supply agency, they fall within the definition of “manpower recruitment or supply agency” (section 65(68) and are liable to Service tax |

11. It can be seen from the above reproduced portion of the Master Circular that it is in respect of supply of manpower which is engaged for specified period or for completion of particular projects or tasks. The clarification, is in case of supply of man power, it can be seen that the clarification specifically needs that the agency agrees for use of services of an individual to another person for a consideration as supply of manpower. In the cases in hand, there is no agreement for utilization of services of an individual but a job/lump-sum work given to the appellants for execution. The said clarification issued by the Board would be appropriate in the case where services of man power recruitment & supply agency, had been temporarily taken by the Business or the industrial association for supplying of manpower and may not be for execution of a specific work. We are of the considered view that the reliance placed by the learned SDR and the learned Commissioner on the circular will not carry the case of the Revenue any further.

12. Accordingly in view of the above findings, we are of the view that the impugned order is liable to be set aside and we do so. The appeal is allowed with consequential relief if any. Since we have disposed of the appeal on merits itself, no findings are recorded on other submissions made by both sides in this appeal.”

- K. Damodarareddy – 2010 25 STT 69 (CESTAT- BANG)

“This appeal filed by Shri K. Damodarareddy (KDR for short) seeks to vacate the demand of service tax of Rs. 20,90,772/- under the head “manpower recruitment and supply agency” services found to have been rendered by it during the period 16-6-2005 to 31-8-2006, applicable interest on the service tax demanded and the penalties of Rs. 1,30,907/-, Rs. 1000/- u/s 77 and Rs. 20,90,772/- u/s 78.

2. Vide the impugned order the Commissioner found that DRC had undertaken the following work and at the rates prescribed in the contract it had entered into with M/s. India Cements Ltd.,

|

Loading of cement bags into closed wagons |

@ Rs. 14.10 per MT | |

| Wagon door cleaning, sealing and riveting etc. |

Rs. 1500/- per rake consisting of 30 boxes. Rs. 1950/- per rake consisting of more than 30 boxes | |

| Complete spillage recovery (3%) of total quantity |

Rs. 38/- per M.T | |

| Drawing of bags to the stenciling floor | Rs. 40/- when conveyed through conveyor. Rs. 48/50 when conveyed manually | |

| Wagon door opening/wagon cleaning | Rs. 95/- per day Rs. 75/- per day |

As per Section 65(68) of the Finance Act, 1994 “manpower recruitment or supply agency’ with effect from 16-6-2005 meant “any commercial concern engaged in providing any service, directly or indirectly, in any manner for recruitment or supply of manpower temporarily or otherwise, to a client.” As per the same Section, “manpower recruitment or supply agency” with effect form 1-5-2006 meant “any person engaged in providing any service, directly or indirectly, in any manner for recruitment or supply of manpower, temporarily or otherwise, to a client.”

4. After due process of law, the Commissioner found that the appellants had rendered taxable services classifiable under the category “Manpower recruitment or supply agency” of clause 68 of Section 65 of the Act during the material period without following the statutory formalities including payment of service tax. Hence the demand and penalties.

5. The appellant has sought to vacate the impugned order and to determine its liability under the appropriate categories of various services involved in the impugned activity. It is submitted before us that cleaning was classifiable separately and stenciling was classifiable under “business auxiliary services.” Various services involved had to be decided and service tax liability quantified correctly. Assessee had paid service tax and education cess involved before the issue of show cause notice and hence penalty and interest could not have been levied. The matter required to be remanded.

6. We have heard both sides. We find that the appellant had carried out the activities of loading of cement bags into wagons, spillage cleaning, stenciling, wagon door opening/closing, wagon cleaning etc., for M/s. India Cements Ltd., during the material period. We find that the appellants were compensated for the various items of work at separate rates prescribed under the contract. The appellants did not supply manpower charging for the labour provided on man-day basis or man-hour basis. The appellants carried out the work as a contractor employing its own labour. Such an activity is not classifiable as “manpower recruitment or supply agency.” In the circumstances, we vacate the impugned order and allow the appeal by way of remand. The liability of the appellant shall be determined afresh after hearing the parties. Appeal is allowed by way of remand to the original authority.”

4.5. From the fact in the present case vis-a-vis judgements cited above it is clear that the appellant’s service is correctly classifiable under cargo handling service as claimed by the appellant and not under manpower recruitment or supply agency service as alleged by the Revenue.

5. As regard the limitation, we find that the appellant have been paying service tax on the same service under cargo handling service and discharged the service tax. The details of nature of service, payment of service tax etc. was declared in their ST-3 return. Nothing prevents the department from taking action against the appellant on the basis of the details provided in ST-3 returns, therefore, there is absolutely no suppression of fact on the part of the appellant. Hence, the demand is also hit by limitation for the extended period.

6. As per our above discussion and finding we are of the considered view that the demand of differential service tax confirmed by the lower authorities is not sustainable. Hence, the impugned order is set aside. Appeal is allowed.

(Pronounced in the open court on 25.08.2023 )