A. PRESENT SCENARIO:

As per Regulation 23(2), (3) and (4) of SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015(“LODR Regulations”) read with Section 177 of the Companies Act, 2013, all Related Party Transactions (“RPTs*”) are required to be approved by the Audit Committee and by the Shareholders, if material.

Exemptions:

Approval of the Audit Committee / Shareholders is not required for the following transactions;

> transactions entered into between a holding company and its wholly owned subsidiary;

> transactions entered into between two wholly-owned subsidiaries of the listed holding company;

Meaning of Related Party Transaction:

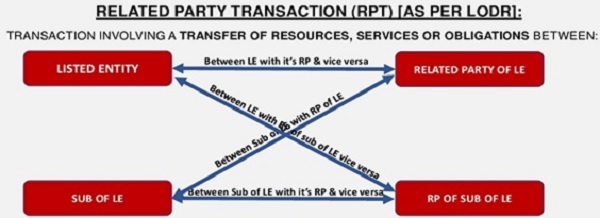

Related party transaction means a transaction involving a transfer of resources, services or obligations between:

> a listed entity or any of its subsidiaries on one hand and a related party of the listed entity or any of its subsidiaries on the other hand; or

a listed entity or any of its subsidiaries on one hand, and any other person or entity on the other hand, the purpose and effect of which is to benefit a related party of the listed entity or any of its subsidiaries.

Exclusions:

The following shall not be a Related Party Transaction:

a. Issue of specified securities on a preferential basis;

b. Corporate actions which are uniformly applicable/offered to all shareholders such as

> dividend,

> subdivision or consolidation of securities,

> Rights issue or a bonus issue or buy-back of securities.

c. Retail purchases from any listed entity or its subsidiary by its directors or its employees, without establishing a business relationship and at the terms which are uniformly applicable/offered to all employees and directors.

Meaning of material Related Party Transaction:

A transaction with a related party shall be considered material, if the transaction(s) to be entered into individually or taken together with previous transactions during a financial year, exceeds rupees one thousand crore or ten per cent of the annual consolidated turnover of the listed entity as per the last audited financial statements of the listed entity, whichever is lower.

Notwithstanding the above, a transaction involving payments made to a related party with respect to brand usage or royalty shall be considered material if the transaction(s) to be entered into individually or taken together with previous transactions during a financial year, exceed five percent of the annual consolidated turnover of the listed entity as per the last audited financial statements of the listed entity.

SEBI Master Circular dated November 11, 2024 (“Master Circular”) specify the information to be placed before the Audit Committee and Shareholders, respectively, for consideration on RPTs.

B. REVISED REGULATORY REGIME ON RPT DISCLOSURES BEFORE AUDIT COMMITTEE & SHAREHOLDERS:

In order to facilitate uniform approach and assist listed entities in complying with the above mentioned requirements SEBI vide its circular dated February 14, 2025 has formulated industry standards for minimum information to be provided for review of the audit committee and shareholders for approval of RPTs.

C. OBJECTIVE:

The objective of these Standards is to standardize the format for minimum information to be provided to the Audit Committee and Shareholders, whenever required for approval of RPTs.

As per circular, going forward the information as per standard format shall be incorporated in the agenda of the Audit Committee meeting.

D. APPLICABILITY:

These Standards shall be applicable in respect of RPTs entered into by the Listed Entity on or after 1st April, 2025.

E. PROCESS FOR APPROVAL FOR RELATED PARTY TRANSACTIONS

(i) Identification of Type of RPT

| a. Material RPT |

|

| b. Other RPT | Transaction(s) with Promoter / Promoter Group / Entities where promoter or promoter group has concern or interest, exceed lower of the following:

|

| c. Residual RPT | Other than A & B of above |

(ii) Identification of RPT items

| a. Balance Sheet items | Balance Sheet items include:

|

|||||

| b. P&L items | P&L items include:

|

(iii) Type of Disclosure

| a. Comprehensive disclosures | As per Annexure – A |

| b. Limited disclosures | As per Annexure – B |

| c. Minimum disclosures | As per Annexure – C |

(iv) Applicability of Disclosures based on transaction type:

Applicability Matrix

| Type of Transaction | Threshold | Balance Sheet / P&L Items | Approvals required | Disclosure requirement |

| Material RPT | As provided above | Both | Audit Committee

+ Shareholders |

Comprehensive disclosures |

| Other RPT, but which is with promoter or promoter group or person/ entity in which promoter or promoter group has concern or interest | Exceed the threshold provided above | Balance sheet items | Audit Committee | Comprehensive disclosures |

| P&L items | Comprehensive disclosures | |||

| Less than the threshold as provided above | Balance sheet items | Audit Committee | Comprehensive disclosures | |

| P&L items | Limited disclosures | |||

| Residual RPT | Transaction(s) with a related party to be entered into individually or taken together with previous transactions during a financial year exceeding Rs. one crore | Both | Audit Committee | Limited disclosures |

| Transaction(s) with a related party to be entered into individually or taken together with previous transactions during a financial year less than Rs. one crore | Minimum disclosures |

F. IMPORTANT NOTES:

The following points shall be considered while collecting and collating the information to be placed before the Audit Committee:

(a) Management to provide comments against each information where it is sought in the format specified in Para 4 of these Standards against transaction-based information.

Indicate ‘NA’, where the field is not applicable and ‘NIL’, where no comments have been provided.

(b) Certificates from the CEO or CFO or any other KMP of the Listed Entity and from every director of the Listed Entity who is also promoter (“promoter director”) to the effect that:

(i) the RPTs to be entered into are not prejudicial to the interest of public shareholders; and

(ii) the terms and conditions of the RPT are not unfavorable to the listed entity, compared to the terms and conditions, had similar transaction been entered into with an unrelated party.

However, if any promoter director does not provide such certificate, the same shall be informed to the Audit Committee and the shareholders, if it is a material RPT as specified in Para 1(1) of these Standards.

(c) Copy of the valuation or other report of external party, if any, shall be placed before the Audit Committee.

(d) If audited financial statements of the related party as required to be submitted to Audit Committee are not available for any financial year, the financial details shall be certified by the related party.

(e) In the case of the payment of royalty, management fees, service fees, etc., if any, shall be explicitly bifurcated and disclosed.

(f) In the case of the payment of royalty, the criteria for selecting Industry Peers shall be as follows:

(i) The Listed Entity will strive to compare the royalty payment with a minimum of three Industry Peers, where feasible. The selection shall follow the following hierarchy:

a. Preference will be given to Indian listed Industry Peers.

b. If Indian listed Industry Peers are not available, a comparison may be made with listed global Industry Peers, if available.

(ii) If no suitable Indian listed/ global Industry Peers are available, the Listed Entity may refer to the peer group considered by SEBI-registered research analysts in their publicly available research reports (“Research Analyst Peer Set”). If the Listed Entity’s business model differs from such Research Analyst Peer Set, it may provide an explanation to clarify the distinction.

(iii) In cases where fewer than three Industry Peers are available, the listed entity will disclose, that only one or two peers are available for comparison.

(g) If the Audit Committee has any comments on the line items as per the format specified in Para 4 of these Standards, it shall provide them accordingly. However, comments are required only for applicable line items, while non-applicable line items may be left blank.

G. STANDARDS FOR MINIMUM INFORMATION TO BE PROVIDED TO THE SHAREHOLDERS FOR CONSIDERATION OF MATERIAL RPTS:

(i) The explanatory statement contained in the notice sent to the shareholders for seeking their approval for an RPT shall provide the minimum information so as to enable the shareholders to take a view whether the terms and conditions of the RPT are favorable to the listed

(ii) The notice being sent to the shareholders seeking approval for any material RPT shall, in addition to the requirements under the Companies Act, 2013, include the following information as a part of the explanatory statement:

(a) Information as placed before the Audit Committee in the format as specified above of these Standards, to the extent applicable.

(b) The Audit Committee can approve redaction of commercial secrets and such other information that would affect competitive position of listed entity from disclosures to shareholders. Further, the Audit Committee shall certify that, in its assessment, the redacted disclosures still provide all the necessary information to the public shareholders for informed decision-making.

(c) Justification as to why the proposed transaction is in the interest of the listed

(d) Statement of assessment by the Audit Committee that relevant disclosures for decision- making were placed before them, and they have determined that the promoter(s) will not benefit from the RPT at the expense of public shareholders.

(e) Disclose the fact that the Audit Committee had reviewed the certificate provided by the CEO or CFO or any other KMP as well as the certificate provided by the promoter directors of the Listed Entity as required under Para 3(2)(b) of these Standards.

(f) Copy of the valuation report or other reports of external party, if any, considered by Audit Committee while approving the RPT.

(g) In case of sale, purchase, or supply of goods or services [as provided in B(2) in the format as specified in Para above of these Standards], or the sale, lease, or disposal of assets of a subsidiary, unit, division, or undertaking of the listed entity [as provided in B(7) in the format as specified in Para above of these Standards], if the Audit Committee has reviewed the terms and conditions of bids from unrelated parties then such fact shall be In case bids have not been invited, the fact shall be disclosed along with the justification thereof, and in case comparable bids are not available, state the basis for recommending that the terms of the RPT are beneficial to the shareholders.

(h) Comments of the Board/ Audit Committee of the listed entity, if

(i) Any other information that may be

Annexure – A

Format for Comprehensive Disclosure

| S.

No. |

Particulars of the information | Information provided by the management | Comments of the Audit Committee | Remarks |

| A. Details of the related party and transactions with the related party | ||||

| A(1). Basic details of the related party | ||||

| 1. | Name of the related party | |||

| 2. | Country of incorporation of the related party | |||

| 3. | Nature of business of the related party | |||

| A(2). Relationship and ownership of the related party | ||||

| 4. | Relationship between the listed entity/subsidiary (in case of transaction involving the subsidiary) and the related party. | |||

| 5. | Shareholding or contribution % or profit & loss sharing % of the listed entity/ subsidiary (in case of transaction involving the subsidiary), whether direct or indirect, in the related party.

Explanation: Indirect shareholding shall mean shareholding held through any person, over which the listed entity or subsidiary has control. |

% Shareholding

% Contribution % P&L Sharing |

||

| 6. | Shareholding of the related party, whether direct or indirect, in the listed entity/subsidiary (in case of transaction involving the subsidiary). Explanation: Indirect shareholding shall mean shareholding held through any person, over which the related party has control. While calculating indirect shareholding, shareholding held by relatives shall also be considered. | % Shareholding | ||

| A(3). Financial performance of the related party | ||||

| 7. | Standalone turnover of the related party for each of the last three financial years: | |||

| FY 20xx-20xx | ||||

| FY 20xx-20xx | ||||

| FY 20xx-20xx | ||||

| 8. | Standalone net worth of the related party for each of the last three financial years: | |||

| FY 20xx-20xx | ||||

| FY 20xx-20xx | ||||

| FY 20xx-20xx | ||||

| 9. | Standalone net profits of the related party for each of the last three financial years: | |||

| FY 20xx-20xx | ||||

| FY 20xx-20xx | ||||

–

| FY 20xx-20xx | ||||||||

| A(4). Details of previous transactions with the related party | ||||||||

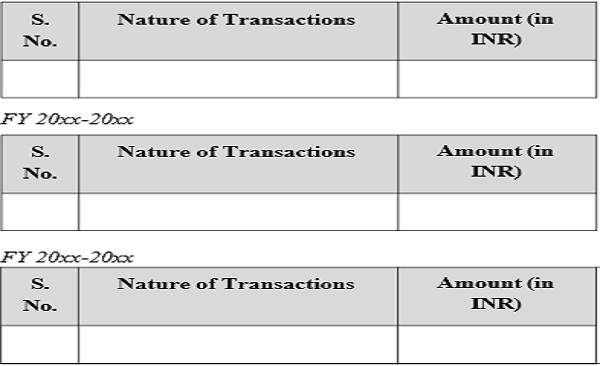

| 10. | Total amount of all the transactions undertaken by the listed entity or subsidiary with the related party during each of the last three financial years.

Note: Details need to be disclosed separately for listed entity and its subsidiary. |

|||||||

| FY 20xx-20xx

FY 20xx-20xx FY 20xx-20xx |

||||||||

| S.

No. |

Nature of Transactions | Amount (in INR) | ||||||

–

| FY 20xx-20xx | ||||||||

| A(4). Details of previous transactions with the related party | ||||||||

| 10. | Total amount of all the transactions undertaken by the listed entity or subsidiary with the related party during each of the last three financial years.

Note: Details need to be disclosed separately for listed entity and its subsidiary. |

|||||||

|

||||||||

| S.

No. |

Nature of Transactions | Amount (in INR) | ||||||

–

| 11. | Total amount of all the transactions undertaken by the listed entity or subsidiary with the related party during the current financial year (till the date of approval of the Audit Committee / shareholders). | |||

| 12. | Whether prior approval of Audit Committee has been taken for the above mentioned transactions? | |||

| 13. | Any default, if any, made by a related party concerning any obligation undertaken by it under a transaction or arrangement entered into with the listed entity or its subsidiary during the last three financial years. | |||

| A(5). Amount of the proposed transactions (All types of transactions taken together) | ||||

| 14. | Total amount of all the proposed transactions being placed for approval in the current meeting. | |||

| 15. | Whether the proposed transactions taken together with the transactions undertaken with the related party during the current financial year is material RPT in terms of Para 1(1) of these Standards? | |||

| 16. | Value of the proposed transactions as a percentage of the listed entity’s annual consolidated turnover for the immediately preceding financial year | % | ||

| 17. | Value of the proposed transactions as a percentage of subsidiary’s annual standalone turnover for the immediately preceding financial year (in case of a transaction involving the subsidiary, and where the listed entity is not a party to the transaction) | % | ||

| 18. | Value of the proposed transactions as a percentage of the related party’s annual standalone turnover for the immediately preceding financial year. | % | ||

| B. Details for specific transactions | ||||

| B(1). Basic details of the proposed transaction

(In case of multiple types of proposed transactions, details to be provided separately for each type of the proposed transaction – for example, (i) sale of goods and purchase of goods to be treated as separate transactions; (ii) sale of goods and sale of services to be treated as separate transactions; (iii) giving of loans and giving of guarantee to be treated as separate transactions) |

||||

| 1. | Specific type of the proposed transaction (e.g. sale of goods/services, purchase of goods/services, giving loan, borrowing etc.) | |||

| 2. | Details of the proposed transaction | |||

| 3. | Tenure of the proposed transaction (tenure in number of years or months to be specified) | |||

| 4. | Indicative date / timeline for undertaking the transaction | |||

| 5. | Whether omnibus approval is being sought? | |||

| 6. | Value of the proposed transaction during a financial year. In case approval of the Audit Committee is sought for multi-year contracts, also provide the aggregate value of transactions during the tenure of the contract.

If omnibus approval is being sought, the maximum value of a single transaction during a financial year. |

|||

| 7. | Whether the RPTs proposed to be entered into are:

(i) not prejudicial to the interest of public shareholders, and (ii) going to be carried out on the same terms and conditions as would be applicable to any party who is not a related party |

Certificate from the CEO or CFO or any other KMP of the listed entity and also from promoter directors of the listed entity (as referred in Para 3(2)(b) of these Standards) | ||

| 8. | Provide a clear justification for entering into the RPT, demonstrating how the proposed RPT serves the best interests of the listed entity and its public shareholders. | |||

| 9. | Details of the promoter(s)/ director(s) / key managerial personnel of the listed entity who have interest in the transaction, whether directly or indirectly.

The details shall be provided, where the shareholding or contribution or % sharing ratio of the promoter(s) or director(s) or KMP in the related party is more than 2%. Explanation: Indirect interest shall mean interest held through any person over which an individual has control including interest held through relatives. |

|||

| a. Name of the director / KMP | ||||

| b. Shareholding of the director / KMP, whether direct or indirect, in the related party | % Shareholding | |||

| 10. | Details of shareholding (more than 2%) of the director(s) / key managerial personnel/ partner(s) of the related party, directly or indirectly, in the listed entity.

Explanation: Indirect shareholding shall mean shareholding held through any person over which an individual has control including shareholding held through relatives. |

|||

| a. Name of the director / KMP/ partner | ||||

| b. Shareholding of the director / KMP/ partner, whether direct or indirect, in the listed entity | % Shareholding | |||

| 11. | A copy of the valuation or other external party report, if any, shall be placed before the Audit Committee. | If any such report has been considered, it shall also be stated whether the Audit Committee has reviewed the basis for valuation contained in the report and found it to be satisfactory based on their independent evaluation. | ||

| 12. | Other information relevant for decision making. | |||

| B(2). Additional details for proposed transactions relating to sale, purchase or supply of goods or services or any other similar business transaction | ||||

| 13. | Number of bidders / suppliers / vendors / traders / distributors / service providers from whom bids / quotations were received with respect to the proposed transaction along with details of process followed to obtain bids. | If the number is less than 3, Audit Committee to comment upon whether the number of bids / quotations received are sufficient | ||

| 14. | Best bid / quotation received.

If comparable bids are available, disclose the price and terms offered. |

Audit committee to provide justification for rejecting the best bid

/quotation and for selecting the related party for the transaction |

||

| 15. | Additional cost / potential loss to the listed entity or the subsidiary in transacting with the related party compared to the best bid / quotation received. | Audit committee to justify the additional cost to the listed entity or the subsidiary | ||

| 16. | Where bids were not invited, the fact shall be disclosed along with the justification for the same. | |||

| 17. | Wherever comparable bids are not available, state what is basis to recommend to the Audit Committee that the terms of proposed RPT are beneficial to the shareholders. | |||

| B(3). Additional details for proposed transactions relating to any loans, inter-corporate deposits or advances given by the listed entity or its subsidiary | ||||

| 18. | Source of funds in connection with the proposed transaction.

Explanation: This shall not be applicable to listed banks/ NBFCs. |

|||

| 19. | Where any financial indebtedness is incurred to give loan, inter-corporate deposit or advance, specify the following:

Explanation: This shall not be applicable to listed banks/ NBFCs. |

|||

| a. Nature of indebtedness | ||||

| b. Total cost of borrowing | ||||

| c. Tenure | ||||

| d. Other details | ||||

| 20. | Material covenants of the proposed transaction | |||

| 21. | Interest rate charged on loans / inter- corporate deposits / advances by the listed entity (or its subsidiary, in case of transaction involving the subsidiary) in the last three financial years:

• To any party (other than related party): • To related party.

Explanations: Comparable rates shall be provided for similar nature of transaction, for e.g., long term vis-a- vis long term etc. |

If the interest rate charged to the related party is less than the average rate charged, then Audit Committee to provide justification for the low interest rate charged. | ||

| 22. | Rate of interest at which the related party is borrowing from its bankers or the rate at which the related party may be able to borrow given its credit rating or credit score and its standing and financial position | |||

| 23. | Rate of interest at which the listed entity or its subsidiary is borrowing from its bankers or the rate at which the listed entity may be able to borrow given its credit rating or credit score and its standing and financial position | |||

| 24. | Proposed interest rate to be charged by listed entity or its subsidiary from the related party. | |||

| 25. | Maturity / due date | |||

| 26. | Repayment schedule & terms | |||

| 27. | Whether secured or unsecured? | |||

| 28. | If secured, the nature of security & security coverage ratio | |||

| 29. | The purpose for which the funds will be utilized by the ultimate beneficiary of such funds pursuant to the transaction. | |||

| 30. | Latest credit rating of the related party (other than structured obligation rating (SO rating) and credit enhancement rating (CE rating)) | If credit rating of the related party is not available, Audit Committee to comment on credit worthiness of the related party | ||

| 31. | Amount of total borrowings (long- term and short-term) of the related party over the last three financial years | |||

| FY 20xx-20xx | ||||

| FY 20xx-20xx | ||||

| FY 20xx-20xx | ||||

| 32. | Interest rate paid on the borrowings by the related party from any party in the last three financial years.

Explanation: Comparable rates shall be provided for similar nature of transaction, for e.g., long term vis-a- vis long term etc. |

If the interest rate charged to the related party is less than the average rate paid by the related party, then the Audit Committee to provide justification for the low interest rate charged. | ||

| 33. | Default in relation to borrowings, if any, made during the last three financial years, by the related party from the listed entity or any other person. | In case of defaults by the related party over the last three financial years, in relation to which the Listed Entity or any of its subsidiary has previously provided guarantee, indemnity or other such obligation, the management has to submit justification to Audit Committee for the proposed transaction and the capacity of the related party to service the debt (loan, deposit or advance) proposed to be given by the listed entity or its subsidiary.

Audit Committee to comment on the justification provided by Management. |

||

| FY 20xx-20xx | ||||

| FY 20xx-20xx | ||||

| FY 20xx-20xx | ||||

| Additional details relating to advances other than loan given by the listed entity or its subsidiary | ||||

| 34. | Advances provided, their break-up and duration. | |||

–

| S. No. | Particulars of the information | Information provided by the management | Comments of the Audit Committee | Remarks | |||||

| S. No. | Advance given to | Amount | Duration of advance given | ||||||

| 1 | |||||||||

| 2 | |||||||||

| 35. | Advance as % of the total loan given during the preceding 12 months | % | |||||||

| B(4). Additional details for proposed transactions relating to any investment made by the listed entity or its subsidiary | |||||||||

| 36. | Source of funds in connection with the proposed transaction.

Explanation: This shall not be applicable to listed banks/ NBFCs. |

||||||||

| 37. | Purpose for which funds shall be utilized by the investee company. | ||||||||

| 38. | Where any financial indebtedness is incurred to make investment, specify the following:

Explanation: This shall not be applicable to listed banks/ NBFCs. |

||||||||

| a. Nature of indebtedness | |||||||||

| b. Total cost of borrowing | |||||||||

| c. Tenure | |||||||||

| d. Other details | |||||||||

| 39. | Material covenants of the proposed transaction | ||||||||

–

| 40. | Latest credit rating of the related party (other than structured obligation rating (SO rating) and credit enhancement rating (CE rating))

Explanation: This shall be applicable in case of investment in debt instruments. |

If credit rating of the related party is not available, Audit Committee to comment on credit worthiness of the related party |

|

||||

| 41. | Expected annualised returns

Explanation: This shall be applicable in case of investment in debt instruments. |

||||||

| 42. | Returns on past investments in the related party over the last three financial years | Return on Equity | In case of diminishing value of investments (negative returns) over the last three financial years, Audit Committee to provide justification for the proposed investment |

|

|||

| 43. | Details of asset-liability mismatch position, if any, post investment

Explanation: This shall be applicable in case of investment in debt instruments. |

||||||

| 44. | Whether any regulatory approval is required. If yes, whether the same has been obtained. | ||||||

| B(5). Additional details for proposed transactions relating to any guarantee (excluding performance guarantee), surety, indemnity or comfort letter, by whatever name called, made or given by the listed entity or its subsidiary | |||||||

|

S. No. |

Particulars of the information | Information provided by the management | Comments of the Audit Committee | Remarks | |||

|

45. |

Rationale for giving guarantee, surety, indemnity or comfort letter | ||||||

|

46. |

Material covenants of the proposed transaction including (i) commission, if any to be received by the listed entity or its subsidiary; (ii) contractual provisions on how the listed entity or its subsidiary will recover the monies in case such guarantee, surety, indemnity or comfort letter is invoked. | ||||||

|

47. |

The value of obligations undertaken by the listed entity or any of its subsidiary, for which a guarantee, surety, indemnity, or comfort letter has been provided by the listed entity or its subsidiary. Additionally, any provisions required to be made in the books of account of the listed entity or any of its subsidiary shall also be specified. | ||||||

|

48. |

Latest credit rating of the related party (other than structured obligation rating (SO rating) and credit enhancement rating (CE rating)), if guarantee, surety, indemnity or comfort letter is given in connection with the borrowing by a related party | If credit rating of the related party is not available, Audit Committee to comment on credit worthiness of the related party | |||||

|

49. |

Details of solvency status and going concern status of the related party during the last three financial years: | ||||||

|

|

FY 20xx-20xx | ||||||

|

|

FY 20xx-20xx | ||||||

–

| S.

No. |

Particulars of the information | Information provided by the management | Comments of the Audit Committee | Remarks |

| FY 20xx-20xx | ||||

| 50. | Default on borrowings, if any, over the last three financial years, by the related party from the listed entity or any other person. | In case of defaults by the related party over the last three financial years, in relation to which the Listed Entity or any of its subsidiary has previously provided guarantee, indemnity or other such obligation, the management has to submit justification to Audit Committee for the proposed transaction and the capacity of the related party to service the debt (loan, deposit or advance) proposed to be given by the listed entity.

Audit Committee to comment on the justification provided by Management. |

||

| FY 20xx-20xx | ||||

| FY 20xx-20xx | ||||

| FY 20xx-20xx | ||||

| B(6). Additional details for proposed transactions relating to borrowings by the listed entity or its subsidiary | ||||

| 51. | Material covenants of the proposed transaction | |||

–

| S.

No. |

Particulars of the information | Information provided by the management | Comments of the Audit Committee | Remarks |

| 52. | Interest rate (in terms of numerical value or base rate and applicable spread) | |||

| 53. | Cost of borrowing (This shall include all costs associated with the borrowing) | |||

| 54. | Maturity / due date | |||

| 55. | Repayment schedule & terms | |||

| 56. | Whether secured or unsecured? | |||

| 57. | If secured, the nature of security & security coverage ratio | |||

| 58. | The purpose for which the funds will be utilized by the listed entity / subsidiary | |||

| 59. | Debt to Equity Ratio of the listed entity or its subsidiary based on last audited financial statements

Explanation: This shall not be applicable to listed banks. |

|||

| a. Before transaction | ||||

| b. After transaction | ||||

| 60. | Debt Service Coverage Ratio of the listed entity or its subsidiary based on last audited financial statements

Explanation: This shall not be applicable to listed banks. |

|||

| a. Before transaction | ||||

| b. After transaction | ||||

| B(7). Additional details for proposed transactions relating to sale, lease or disposal of assets of subsidiary or of unit, division or undertaking of the listed entity, or disposal of shares of subsidiary or associate | ||||

| 61. | Number of bidders / suppliers / vendors / traders / distributors / service providers from whom bids / quotations were received with respect to the proposed transaction along with details of process followed to obtain bids. | If the number is less than 3, Audit Committee to comment upon whether the number of bids / quotations received are sufficient | ||

| 62. | Best bid / quotation received

If comparable bids are available, disclose the price and terms offered. |

Audit Committee to provide justification for rejecting the best bid / quotation and for selecting the related party for the transaction | ||

| 63. | Additional cost / potential loss to the listed entity or the subsidiary in transacting with the related party compared to the best bid / quotation received. | Audit committee to justify the additional cost to the listed entity or the subsidiary | ||

| 64. | Where bids were not invited, the fact shall be disclosed along with the justification for the same. | |||

| 65. | Wherever comparable bids are not available, state what is the basis to recommend to the Audit Committee that the terms of proposed RPT are beneficial to the shareholders. | |||

–

| 66. | Reasons for sale, lease or disposal of assets of subsidiary or of unit, division or undertaking of the listed entity, or disposal of shares of subsidiary or associate. | ||||||||

| 67. | Financial track record of the subsidiary

/ undertaking that is being sold (in case of sale of undertaking, segment level data to be provided) during the last three financial years: |

||||||||

| FY 20xx-20xx | FY 20xx-20xx | FY 20xx-20xx | |||||||

| Turnover | |||||||||

| Net worth | |||||||||

| Net Profit | |||||||||

| Net Profit Margin | |||||||||

| Operating Cash Flow Margin | |||||||||

| Return on Assets (RoA) | |||||||||

| 68. | Expected financial impact on the consolidated turnover, net worth and net profits of the listed entity or its subsidiary due to sale of the subsidiary

/ undertaking |

||||||||

| a. Expected impact on turnover | |||||||||

| b. Expected impact on net worth | |||||||||

| c. Expected impact on net profits | |||||||||

–

| 69. | Details of earlier sale, lease or disposal of assets of the same subsidiary or of the unit, division or undertaking of the listed entity, or disposal of shares of the same subsidiary or associate to any related party during the preceding twelve months. | |||

| 70. | Whether the transaction would result in issue of securities or consideration in kind to a related party? If yes, please share the relevant details. | |||

| 71. | Would the transaction result in eliminating a segment reporting by the listed entity or any of its subsidiary? | |||

| 72. | Does it involve transfer of key intangible assets or key customers which are critical for continued business of the listed entity or any of its subsidiary? | |||

| 73. | Are there any other major non- financial reasons for going ahead with the proposed transaction? | |||

| B(8). Additional details for transactions relating to payment of royalty | ||||

| 74. | Gross amount of royalty paid by the listed entity or subsidiary to the related party during each of the last three financial years | Gross amount of royalty paid by the listed entity or subsidiary to the related party during each of the last three financial years | ||

| FY 20xx-20xx | Amount of royalty | |||

| FY 20xx-20xx | Amount of royalty | |||

| FY 20xx-20xx | Amount of royalty | |||

| 75. | Purpose for which royalty was paid to the related party during the last three financial years. | For companies with a composite license agreement that includes a bundle of intellectual property rights (IPRs) such as brands, patents, technology, and know- how, it is essential to understand the key components of such agreements and the reasons why these cannot be disclosed separately. | ||

| a. For use of brand name / trademark | As a % of aggregate amount of royalty for the last 3 FYs | |||

| b. For transfer of technology know- how | As a % of aggregate amount of royalty for the last 3 FYs | |||

| c. For professional fee, corporate management fee or any other fee | As a % of aggregate amount of royalty for the last 3 FYs | |||

| d. Any other use (specify) | As a % of aggregate amount of royalty for the last 3 FYs | |||

| 76. | Purpose for which royalty is proposed to be paid to the related party in the current financial year | |||

| a. For use of brand name / trademark | As a % of total royalty proposed to be paid | |||

| b. For transfer of technology know- how | As a % of total royalty proposed to be paid | |||

| c. For professional fee, corporate management fee or any other fee | As a % of total royalty proposed to be paid | |||

| d. Any other use (specify) | As a % of total royalty proposed to be paid | |||

| 77. | Royalty paid in last 3 FYs as % of Net Profits of previous FYs | |||

| FY 20xx-20xx | % | |||

| FY 20xx-20xx | % | |||

| FY 20xx-20xx | % | |||

| 78. | Dividend paid in last 3 FYs as % of Net Profits of previous FYs | Audit Committee to comment on the reasons for less dividend payment than royalty payment, if so. | ||

| FY 20xx-20xx | % | |||

| FY 20xx-20xx | % | |||

| FY 20xx-20xx | % | |||

| 79. | Royalty and dividend paid or proposed to be paid during the current FY

Explanation: The dividend proposed to be paid shall mean dividend that has been declared but not been paid yet. |

|||

| 80. | Rate at which royalty has increased in the past 5 years, if any, vis-à-vis rate at which the turnover, profits after tax and dividends have increased during the same period. | |||

| 81. | In case of new technology i.e. first year of technology transfer (to be provided separately for each new technology): | |||

| a. Expected duration of technology transfer | in years | |||

| b. Benefits derived from the technology transfer | ||||

| 82. | In case of existing technology i.e. technology being imported (to be provided separately for each existing technology): | |||

| a. Years since technology transfer initiated | in years | |||

| b. Expected duration of technology transfer | in years | |||

| c. Benefits derived from the technology transfer | ||||

| 83. | Details of in-house research & development, if any: | |||

| a. Total expenses incurred during the preceding financial year | ||||

| b. Benefits derived | ||||

| c. If any in-house R&D undertaken by the listed entity or its subsidiary that will reduce or eliminate the royalty currently paid for any technology or technical know-how. Additionally, the absolute value of R&D expenditure incurred by the listed entity or its subsidiary on such in-house R&D, along with the period required for completing the research to achieve the reduction or elimination of royalty, shall be disclosed to the Audit Committee. | If no expenses were incurred, the Audit Committee shall provide justification or comment on the same. | |||

| 84. | If royalty is paid to the parent company, disclose royalty received by the parent company from foreign entities:

· Minimum rate of royalty charged along with corresponding absolute amount · Maximum rate of royalty charged along with corresponding absolute amount

Explanation: a) The disclosure shall be made on a gross basis (Cost to the Company), including taxes paid on behalf of the recipient of royalty. b) The listed entity may confirm whether the parent company charges royalty at a uniform rate from all group companies. If so, this row shall not be applicable. |

% | ||

–

| 85. | Sunset Clause for Royalty payment | ||||||||||

| 86. | Peer Comparison:

Listed entity or its subsidiary paying royalty for any purpose shall also disclose whether any Industry Peer pays royalties for the same purpose, which is disclosed in its audited annual financial statements for the relevant period: |

||||||||||

| Listed Entity / Subsidiary | Peer 1 | Peer 2 | Peer 3 | ||||||||

| Royalty payment over last 3 years | Aggregate amount | Aggregate amount | Aggregate amount | Aggregate amount | |||||||

| Royalty paid as a % of net profits over the last 3 years | % | % | % | % | |||||||

| Annual growth rate of Turnover over last 3 years | % | % | % | % | |||||||

| 87. | Royalty paid or payable for imported technology, along with the turnover attributable to such technology. | ||||||||||

| 88. | Royalty paid or payable for brands or other intangible assets, along with the turnover attributable to their use. | ||||||||||

Annexure – B

Format for Limited Disclosure

| S.

No. |

Particulars of the information | Information provided by the management | Comments of the Audit Committee | Remarks | ||||||

| A. Details of the related party and transactions with the related party | ||||||||||

| A(1). Basic details of the related party | ||||||||||

| 1. | Name of the related party | |||||||||

| 2. | Country of incorporation of the related party | |||||||||

| 3. | Nature of business of the related party | |||||||||

| A(2). Relationship and ownership of the related party | ||||||||||

| 4. | Relationship between the listed entity/subsidiary (in case of transaction involving the subsidiary) and the related party. | |||||||||

| 5. | Shareholding or contribution % or profit & loss sharing % of the listed entity/ subsidiary (in case of transaction involving the subsidiary), whether direct or indirect, in the related party.

Explanation: Indirect shareholding shall mean shareholding held through any person, over which the listed entity or subsidiary has control. |

% Shareholding

% Contribution % P&L Sharing |

||||||||

| S.

No. |

Particulars of the information | Information provided by the management | Comments of the Audit Committee | Remarks | ||||||

| 6. | Shareholding of the related party, whether direct or indirect, in the listed entity/subsidiary (in case of transaction involving the subsidiary).

Explanation: Indirect shareholding shall mean shareholding held through any person, over which the related party has control. While calculating indirect shareholding, shareholding held by relatives shall also be considered. |

% Shareholding | ||||||||

| A(3). Financial performance of the related party | ||||||||||

| 7. | Standalone turnover of the related party for each of the last three financial years: | |||||||||

| FY 20xx-20xx | ||||||||||

| FY 20xx-20xx | ||||||||||

| FY 20xx-20xx | ||||||||||

| 8. | Standalone net worth of the related party for each of the last three financial years: | |||||||||

| FY 20xx-20xx | ||||||||||

| FY 20xx-20xx | ||||||||||

| FY 20xx-20xx | ||||||||||

| 9. | Standalone net profits of the related party for each of the last three financial years: | |||||||||

| FY 20xx-20xx | ||||||||||

| FY 20xx-20xx | ||||||||||

–

| S.

No. |

Particulars of the information | Information provided by the management | Comments of the Audit Committee | Remarks | ||||

| FY 20xx-20xx | ||||||||

| A(4). Details of previous transactions with the related party | ||||||||

| 10. | Total amount of all the transactions undertaken by the listed entity or subsidiary with the related party during each of the last three financial years.

Note: Details need to be disclosed separately for listed entity and its subsidiary. |

|||||||

|

|

||||||||

| 11. | Total amount of all the transactions undertaken by the listed entity or subsidiary with the related party during the current financial year (till the date of approval of the Audit Committee / shareholders). | |||||||

| 12. | Whether prior approval of Audit Committee has been taken for the above mentioned transactions? | |||||||

| 13. | Any default, if any, made by a related party concerning any obligation undertaken by it under a transaction or arrangement entered into with the listed entity or its subsidiary during the last three financial years. | |||||||

| A(5). Amount of the proposed transactions (All types of transactions taken together) | ||||||||

| 14. | Total amount of all the proposed transactions being placed for approval in the current meeting. | |||||||

| 15. | Whether the proposed transactions taken together with the transactions undertaken with the related party during the current financial year is material RPT in terms of Para 1(1) of these Standards? | |||||||

| 16. | Value of the proposed transactions as a percentage of the listed entity’s annual consolidated turnover for the immediately preceding financial year | % | ||||||

| 17. | Value of the proposed transactions as a percentage of subsidiary’s annual standalone turnover for the immediately preceding financial year (in case of a transaction involving the subsidiary, and where the listed entity is not a party to the transaction) | % | ||||||

| 18. | Value of the proposed transactions as a percentage of the related party’s annual standalone turnover for the immediately preceding financial year. | % | ||||||

| B. Details for specific transactions | ||||||||

| B(1). Basic details of the proposed transaction

(In case of multiple types of proposed transactions, details to be provided separately for each type of the proposed transaction – for example, (i) sale of goods and purchase of goods to be treated as separate transactions; (ii) sale of goods and sale of services to be treated as separate transactions; (iii) giving of loans and giving of guarantee to be treated as separate transactions) |

||||||||

| 1. | Specific type of the proposed transaction (e.g. sale of goods/services, purchase of goods/services, giving loan, borrowing etc.) | |||||||

| 2. | Details of the proposed transaction | |||||||

| 3. | Tenure of the proposed transaction (tenure in number of years or months to be specified) | |||||||

| 4. | Indicative date / timeline for undertaking the transaction | |||||||

| 5. | Whether omnibus approval is being sought? | |||||||

| 6. | Value of the proposed transaction during a financial year. In case approval of the Audit Committee is sought for multi-year contracts, also provide the aggregate value of transactions during the tenure of the contract.

If omnibus approval is being sought, the maximum value of a single transaction during a financial year. |

|||||||

| 7. | Whether the RPTs proposed to be entered into are:

(iii) not prejudicial to the interest of public shareholders, and (iv) going to be carried out on the same terms and conditions as would be applicable to any party who is not a related party |

Certificate from the CEO or CFO or any other KMP of the listed entity and also from promoter directors of the listed entity (as referred in Para 3(2)(b) of these Standards) | ||||||

| 8. | Provide a clear justification for entering into the RPT, demonstrating how the proposed RPT serves the best interests of the listed entity and its public shareholders. | |||||||

| 9. | Details of the promoter(s)/ director(s) / key managerial personnel of the listed entity who have interest in the transaction, whether directly or indirectly.

The details shall be provided, where the shareholding or contribution or % sharing ratio of the promoter(s) or director(s) or KMP in the related party is more than 2%. Explanation: Indirect interest shall mean interest held through any person over which an individual has control including interest held through relatives. |

|||||||

| a. Name of the director / KMP | ||||||||

| b. Shareholding of the director / KMP, whether direct or indirect, in the related party | % Shareholding | |||||||

| 10. | Details of shareholding (more than 2%) of the director(s) / key managerial personnel/ partner(s) of the related party, directly or indirectly, in the listed entity.

Explanation: Indirect shareholding shall mean shareholding held through any person over which an individual has control including shareholding held through relatives. |

|||||||

| a. Name of the director / KMP/ partner | ||||||||

| b. Shareholding of the director / KMP/ partner, whether direct or indirect, in the listed entity | % Shareholding | |||||||

| 11. | A copy of the valuation or other external party report, if any, shall be placed before the Audit Committee. | If any such report has been considered, it shall also be stated whether the Audit Committee has reviewed the basis for valuation contained in the report and found it to be satisfactory based on their independent evaluation. | ||||||

| 12. | Other information relevant for decision making. | |||||||

| B(3). Additional details for proposed transactions relating to any loans, inter-corporate deposits or advances given by the listed entity or its subsidiary | ||||||||

| 18. | Source of funds in connection with the proposed transaction.

Explanation: This shall not be applicable to listed banks/ NBFCs. |

|||||||

| 19. | Where any financial indebtedness is incurred to give loan, inter-corporate deposit or advance, specify the following:

Explanation: This shall not be applicable to listed banks/ NBFCs. |

|||||||

| a. Nature of indebtedness | ||||||||

| b. Total cost of borrowing | ||||||||

| c. Tenure | ||||||||

| d. Other details | ||||||||

–

| 20. | Material covenants of the proposed transaction | |||

| 21. | Interest rate charged on loans / inter- corporate deposits / advances by the listed entity (or its subsidiary, in case of transaction involving the subsidiary) in the last three financial years:

Explanations: Comparable rates shall be provided for similar nature of transaction, for e.g., long term vis-a- vis long term etc. |

If the interest rate charged to the related party is less than the average rate charged, then Audit Committee to provide justification for the low interest rate charged. | ||

| 22. | Rate of interest at which the related party is borrowing from its bankers or the rate at which the related party may be able to borrow given its credit rating or credit score and its standing and financial position | |||

| 23. | Rate of interest at which the listed entity or its subsidiary is borrowing from its bankers or the rate at which the listed entity may be able to borrow given its credit rating or credit score and its standing and financial position | |||

| 24. | Proposed interest rate to be charged by listed entity or its subsidiary from the related party. |

–

| S.

No. |

Particulars of the information | Information provided by the management | Comments of the Audit Committee | Remarks |

| 25. | Maturity / due date | |||

| 26. | Repayment schedule & terms | |||

| 27. | Whether secured or unsecured? | |||

| 28. | If secured, the nature of security & security coverage ratio | |||

| 29. | The purpose for which the funds will be utilized by the ultimate beneficiary of such funds pursuant to the transaction. | |||

| 30. | Latest credit rating of the related party (other than structured obligation rating (SO rating) and credit enhancement rating (CE rating)) | If credit rating of the related party is not available, Audit Committee to comment on credit worthiness of the related party | ||

| 31. | Amount of total borrowings (long- term and short-term) of the related party over the last three financial years | |||

| FY 20xx-20xx | ||||

| 32. | Interest rate paid on the borrowings by the related party from any party in the last three financial years.

Explanation: Comparable rates shall be provided for similar nature of transaction, for e.g., long term vis-a- vis long term etc. |

If the interest rate charged to the related party is less than the average rate paid by the related party, then the Audit Committee to provide justification for the low interest rate charged. |

–

| S.

No. |

Particulars of the information | Information provided by the management | Comments of the Audit Committee | Remarks |

| 33. | Default in relation to borrowings, if any, made during the last three financial years, by the related party from the listed entity or any other person. | In case of defaults by the related party over the last three financial years, in relation to which the Listed Entity or any of its subsidiary has previously provided guarantee, indemnity or other such obligation, the management has to submit justification to Audit Committee for the proposed transaction and the capacity of the related party to service the debt (loan, deposit or advance) proposed to be given by the listed entity or its subsidiary.

Audit Committee to comment on the justification provided by Management. |

||

| FY 20xx-20xx | ||||

| FY 20xx-20xx | ||||

| FY 20xx-20xx | ||||

| Additional details relating to advances other than loan given by the listed entity or its subsidiary | ||||

| 34. | Advances provided, their break-up and duration. | |||

–

| S. No. | Particulars of the information | Information provided by the management | Comments of the Audit Committee | Remarks | |||||

| S. No. | Advance given to | Amount | Duration of advance given | ||||||

| 1 | |||||||||

| 2 | |||||||||

| 35. | Advance as % of the total loan given during the preceding 12 months | % | |||||||

| B(4). Additional details for proposed transactions relating to any investment made by the listed entity or its subsidiary | |||||||||

| 36. | Source of funds in connection with the proposed transaction.

Explanation: This shall not be applicable to listed banks/ NBFCs. |

||||||||

| 37. | Purpose for which funds shall be utilized by the investee company. | ||||||||

| 38. | Where any financial indebtedness is incurred to make investment, specify the following:

Explanation: This shall not be applicable to listed banks/ NBFCs. |

||||||||

| a. Nature of indebtedness | |||||||||

| b. Total cost of borrowing | |||||||||

| c. Tenure | |||||||||

| d. Other details | |||||||||

| 39. | Material covenants of the proposed transaction | ||||||||

–

| S.

No. |

Particulars of the information | Information provided by the management | Comments of the Audit Committee | Remarks | |||||

| 40. | Latest credit rating of the related party (other than structured obligation rating (SO rating) and credit enhancement rating (CE rating))

Explanation: This shall be applicable in case of investment in debt instruments. |

If credit rating of the related party is not available, Audit Committee to comment on credit worthiness of the related party |

|

||||||

| 41. | Expected annualised returns

Explanation: This shall be applicable in case of investment in debt instruments. |

||||||||

| 42. | Returns on past investments in the related party over the last three financial years | Return on Equity | In case of diminishing value of investments (negative returns) over the last three financial years, Audit Committee to provide justification for the proposed investment | ||||||

| 44. | Whether any regulatory approval is required. If yes, whether the same has been obtained. | ||||||||

| B(5). Additional details for proposed transactions relating to any guarantee (excluding performance guarantee), surety, indemnity or comfort letter, by whatever name called, made or given by the listed entity or its subsidiary | |||||||||

| S.

No. |

Particulars of the information | Information provided by the management | Comments of the Audit Committee | Remarks | |||||

| 45. | Rationale for giving guarantee, surety, indemnity or comfort letter | ||||||||

| 46. | Material covenants of the proposed transaction including (i) commission, if any to be received by the listed entity or its subsidiary; (ii) contractual provisions on how the listed entity or its subsidiary will recover the monies in case such guarantee, surety, indemnity or comfort letter is invoked. | ||||||||

| 47. | The value of obligations undertaken by the listed entity or any of its subsidiary, for which a guarantee, surety, indemnity, or comfort letter has been provided by the listed entity or its subsidiary. Additionally, any provisions required to be made in the books of account of the listed entity or any of its subsidiary shall also be specified. | ||||||||

| 48. | Latest credit rating of the related party (other than structured obligation rating (SO rating) and credit enhancement rating (CE rating)), if guarantee, surety, indemnity or comfort letter is given in connection with the borrowing by a related party | If credit rating of the related party is not available, Audit Committee to comment on credit worthiness of the related party | |||||||

| 49. | Details of solvency status and going concern status of the related party during the last three financial years: | ||||||||

| FY 20xx-20xx | |||||||||

| FY 20xx-20xx | |||||||||

–

| FY 20xx-20xx | |||||||||

| 50. | Default on borrowings, if any, over the last three financial years, by the related party from the listed entity or any other person. | In case of defaults by the related party over the last three financial years, in relation to which the Listed Entity or any of its subsidiary has previously provided guarantee, indemnity or other such obligation, the management has to submit justification to Audit Committee for the proposed transaction and the capacity of the related party to service the debt (loan, deposit or advance) proposed to be given by the listed entity.

Audit Committee to comment on the justification provided by Management. |

|||||||

| FY 20xx-20xx | |||||||||

| FY 20xx-20xx | |||||||||

| FY 20xx-20xx | |||||||||

| B(6). Additional details for proposed transactions relating to borrowings by the listed entity or its subsidiary | |||||||||

| 51. | Material covenants of the proposed transaction | ||||||||

| 52. | Interest rate (in terms of numerical value or base rate and applicable spread) | ||||||||

| 53. | Cost of borrowing (This shall include all costs associated with the borrowing) | ||||||||

| 54. | Maturity / due date | ||||||||

| 55. | Repayment schedule & terms | ||||||||

| 56. | Whether secured or unsecured? | ||||||||

| 57. | If secured, the nature of security & security coverage ratio | ||||||||

| 58. | The purpose for which the funds will be utilized by the listed entity / subsidiary | ||||||||

| 59. | Debt to Equity Ratio of the listed entity or its subsidiary based on last audited financial statements

Explanation: This shall not be applicable to listed banks. |

||||||||

| a. Before transaction | |||||||||

| b. After transaction | |||||||||

| 60. | Debt Service Coverage Ratio of the listed entity or its subsidiary based on last audited financial statements

Explanation: This shall not be applicable to listed banks. |

||||||||

| a. Before transaction | |||||||||

| b. After transaction | |||||||||

| B(7). Additional details for proposed transactions relating to sale, lease or disposal of assets of subsidiary or of unit, division or undertaking of the listed entity, or disposal of shares of subsidiary or associate | |||||||||

| 61. | Number of bidders / suppliers / vendors / traders / distributors / service providers from whom bids / quotations were received with respect to the proposed transaction along with details of process followed to obtain bids. | If the number is less than 3, Audit Committee to comment upon whether the number of bids / quotations received are sufficient | |||||||

| 62. | Best bid / quotation received If comparable bids are available, disclose the price and terms offered. | Audit Committee to provide justification for rejecting the best bid / quotation and for selecting the related party for the transaction | |||||||

| 63. | Additional cost / potential loss to the listed entity or the subsidiary in transacting with the related party compared to the best bid / quotation received. | Audit committee to justify the additional cost to the listed entity or the subsidiary | |||||||

| 64. | Where bids were not invited, the fact shall be disclosed along with the justification for the same. | ||||||||

| 65. | Wherever comparable bids are not available, state what is the basis to recommend to the Audit Committee that the terms of proposed RPT are beneficial to the shareholders. | ||||||||

| 66. | Reasons for sale, lease or disposal of assets of subsidiary or of unit, division or undertaking of the listed entity, or disposal of shares of subsidiary or associate. | ||||||||

| 67. | Financial track record of the subsidiary

/ undertaking that is being sold (in case of sale of undertaking, segment level data to be provided) during the last three financial years: |

||||||||

| FY 20xx-20xx | FY 20xx-20xx | FY 20xx-20xx | |||||||

| Turnover | |||||||||

| Net worth | |||||||||

| Net Profit | |||||||||

| Net Profit Margin | |||||||||

| Operating Cash Flow Margin | |||||||||

| Return on Assets (RoA) | |||||||||

| 68. | Expected financial impact on the consolidated turnover, net worth and net profits of the listed entity or its subsidiary due to sale of the subsidiary

/ undertaking |

||||||||

| a. Expected impact on turnover | |||||||||

| b. Expected impact on net worth | |||||||||

| c. Expected impact on net profits | |||||||||

–

| S. No. | Particulars of the information | Information provided by the management | Comments of the Audit Committee | Remarks |

| 69. | Details of earlier sale, lease or disposal of assets of the same subsidiary or of the unit, division or undertaking of the listed entity, or disposal of shares of the same subsidiary or associate to any related party during the preceding twelve months. | |||

| 70. | Whether the transaction would result in issue of securities or consideration in kind to a related party? If yes, please share the relevant details. | |||

| 71. | Would the transaction result in eliminating a segment reporting by the listed entity or any of its subsidiary? | |||

| 72. | Does it involve transfer of key intangible assets or key customers which are critical for continued business of the listed entity or any of its subsidiary? | |||

| 73. | Are there any other major non- financial reasons for going ahead with the proposed transaction? | |||

| B(8). Additional details for transactions relating to payment of royalty | ||||

| 74. | Gross amount of royalty paid by the listed entity or subsidiary to the related party during each of the last three financial years | |||

| FY 20xx-20xx | Amount of royalty | |||

| FY 20xx-20xx | Amount of royalty | |||

| FY 20xx-20xx | Amount of royalty | |||

| 75. | Purpose for which royalty was paid to the related party during the last three financial years. | For companies with a composite license agreement that includes a bundle of intellectual property rights (IPRs) such as brands, patents, technology, and know- how, it is essential to understand the key components of such agreements and the reasons why these cannot be disclosed separately. | ||

| a. For use of brand name / trademark | As a % of aggregate amount of royalty for the last 3 FYs | |||

| b. For transfer of technology know- how | As a % of aggregate amount of royalty for the last 3 FYs | |||

| c. For professional fee, corporate management fee or any other fee | As a % of aggregate amount of royalty for the last 3 FYs | |||

| d. Any other use (specify) | As a % of aggregate amount of royalty for the last 3 FYs | |||

| 76. | Purpose for which royalty is proposed to be paid to the related party in the current financial year | – | ||

| a. For use of brand name / trademark | As a % of total royalty proposed to be paid | |||

| b. For transfer of technology know- how | As a % of total royalty proposed to be paid | |||

| c. For professional fee, corporate management fee or any other fee | As a % of total royalty proposed to be paid | |||

| d. Any other use (specify) | As a % of total royalty proposed to be paid | |||

| 77. | Royalty paid in last 3 FYs as % of Net Profits of previous FYs | |||

| FY 20xx-20xx | % | |||

| FY 20xx-20xx | % | |||

| FY 20xx-20xx | % | |||

| 80. | Rate at which royalty has increased in the past 5 years, if any, vis-à-vis rate at which the turnover, profits after tax and dividends have increased during the same period. | |||

| 81. | In case of new technology i.e. first year of technology transfer (to be provided separately for each new technology): | |||

| a. Expected duration of technology transfer | in years | |||

| b. Benefits derived from the technology transfer | ||||

| 82. | In case of existing technology i.e. technology being imported (to be provided separately for each existing technology): | |||

| a. Years since technology transfer initiated | in years | |||

| b. Expected duration of technology transfer | in years | |||

| c. Benefits derived from the technology transfer | ||||

| 83. | Details of in-house research & development, if any: | |||

| a. Total expenses incurred during the preceding financial year | ||||

| b. Benefits derived | ||||

| c. If any in-house R&D undertaken by the listed entity or its subsidiary that will reduce or eliminate the royalty currently paid for any technology or technical know-how. Additionally, the absolute value of R&D expenditure incurred by the listed entity or its subsidiary on such in-house R&D, along with the period required for completing the research to achieve the reduction or elimination of royalty, shall be disclosed to the Audit Committee. | If no expenses were incurred, the Audit Committee shall provide justification or comment on the same. | |||

| 85. | Sunset Clause for Royalty payment | |||

| 87. | Royalty paid or payable for imported technology, along with the turnover attributable to such technology. | |||

| 88. | Royalty paid or payable for brands or other intangible assets, along with the turnover attributable to their use. | |||

Annexure – C

Format for Minimum Disclosures

| S.

No. |

Particulars of the information | Information provided by the management | Comments of the Audit Committee | Remarks | ||||||

| A. Details of the related party and transactions with the related party | ||||||||||

| A(1). Basic details of the related party | ||||||||||

| 1. | Name of the related party | |||||||||

| 2. | Country of incorporation of the related party | |||||||||

| 3. | Nature of business of the related party | |||||||||

| A(2). Relationship and ownership of the related party | ||||||||||

| 4. | Relationship between the listed entity/subsidiary (in case of transaction involving the subsidiary) and the related party. | |||||||||

| 5. | Shareholding or contribution % or profit & loss sharing % of the listed entity/ subsidiary (in case of transaction involving the subsidiary), whether direct or indirect, in the related party.

Explanation: Indirect shareholding shall mean shareholding held through any person, over which the listed entity or subsidiary has control. |

% Shareholding

% Contribution % P&L Sharing |

||||||||

| S.

No. |

Particulars of the information | Information provided by the management | Comments of the Audit Committee | Remarks | ||||||

| 6. | Shareholding of the related party, whether direct or indirect, in the listed entity/subsidiary (in case of transaction involving the subsidiary).

Explanation: Indirect shareholding shall mean shareholding held through any person, over which the related party has control. While calculating indirect shareholding, shareholding held by relatives shall also be considered. |

% Shareholding | ||||||||

–

| S.

No. |

Particulars of the information | Information provided by the management | Comments of the Audit Committee | Remarks |

| A(4). Details of previous transactions with the related party | ||||

| 10. | Total amount of all the transactions undertaken by the listed entity or subsidiary with the related party during each of the last three financial years.

Note: Details need to be disclosed separately for listed entity and its subsidiary. |

|||

|

||||

| 11. | Total amount of all the transactions undertaken by the listed entity or subsidiary with the related party during the current financial year (till the date of approval of the Audit Committee / shareholders). | |||

| 12. | Whether prior approval of Audit Committee has been taken for the above mentioned transactions? | |||

| 13. | Any default, if any, made by a related party concerning any obligation undertaken by it under a transaction or arrangement entered into with the listed entity or its subsidiary during the last three financial years. | |||

| A(5). Amount of the proposed transactions (All types of transactions taken together) | ||||

| 14. | Total amount of all the proposed transactions being placed for approval in the current meeting. | |||

| 15. | Whether the proposed transactions taken together with the transactions undertaken with the related party during the current financial year is material RPT in terms of Para 1(1) of these Standards? | |||

| 16. | Value of the proposed transactions as a percentage of the listed entity’s annual consolidated turnover for the immediately preceding financial year | % | ||

| 17. | Value of the proposed transactions as a percentage of subsidiary’s annual standalone turnover for the immediately preceding financial year (in case of a transaction involving the subsidiary, and where the listed entity is not a party to the transaction) | % | ||

| 18. | Value of the proposed transactions as a percentage of the related party’s annual standalone turnover for the immediately preceding financial year. | % | ||

| B. Details for specific transactions | ||||

| B(1). Basic details of the proposed transaction

(In case of multiple types of proposed transactions, details to be provided separately for each type of the proposed transaction – for example, (i) sale of goods and purchase of goods to be treated as separate transactions; (ii) sale of goods and sale of services to be treated as separate transactions; (iii) giving of loans and giving of guarantee to be treated as separate transactions) |

||||

| 1. | Specific type of the proposed transaction (e.g. sale of goods/ services, purchase of goods/services, giving loan, borrowing etc.) | |||

| 2. | Details of the proposed transaction | |||

| 3. | Tenure of the proposed transaction (tenure in number of years or months to be specified) | |||

| 4. | Indicative date / timeline for undertaking the transaction | |||

| 5. | Whether omnibus approval is being sought? | |||

| 6. | Value of the proposed transaction during a financial year. In case approval of the Audit Committee is sought for multi-year contracts, also provide the aggregate value of transactions during the tenure of the contract.

If omnibus approval is being sought, the maximum value of a single transaction during a financial year. |

|||

| 7. | Whether the RPTs proposed to be entered into are:

(v) not prejudicial to the interest of public shareholders, and (vi) going to be carried out on the same terms and conditions as would be applicable to any party who is not a related party |

Certificate from the CEO or CFO or any other KMP of the listed entity and also from promoter directors of the listed entity (as referred in Para 3(2)(b) of these Standards) | ||

| 8. | Provide a clear justification for entering into the RPT, demonstrating how the proposed RPT serves the best interests of the listed entity and its public shareholders. | |||

jkglkjhkhjkjhkjhk

| S.

No. |

Particulars of the information | Information provided by the management | Comments of the Audit Committee | Remarks |

| 9. | Details of the promoter(s)/ director(s) / key managerial personnel of the listed entity who have interest in the transaction, whether directly or indirectly.

The details shall be provided, where the shareholding or contribution or % sharing ratio of the promoter(s) or director(s) or KMP in the related party is more than 2%.

Explanation: Indirect interest shall mean interest held through any person over which an individual has control including interest held through relatives. |

|||

| a. Name of the director / KMP | ||||

| b. Shareholding of the director / KMP, whether direct or indirect, in the related party | % Shareholding | |||

| 10. | Details of shareholding (more than 2%) of the director(s) / key managerial personnel/ partner(s) of the related party, directly or indirectly, in the listed entity.

Explanation: Indirect shareholding shall mean shareholding held through any person over which an individual has control including shareholding held through relatives. |

|||

| a. Name of the director / KMP/ partner | ||||

| b. Shareholding of the director / KMP/ partner, whether direct or indirect, in the listed entity | % Shareholding | |||

| 11. | A copy of the valuation or other external party report, if any, shall be placed before the Audit Committee. | If any such report has been considered, it shall also be stated whether the Audit Committee has reviewed the basis for valuation contained in the report and found it to be satisfactory based on their independent evaluation. | ||

| 12. | Other information relevant for decision making. |