The Reserve Bank of India (RBI) has introduced key policy measures in financial markets, cybersecurity, and payment systems to enhance market efficiency and security. In financial markets, RBI plans to introduce forward contracts in government securities to help long-term investors manage interest rate risks. SEBI-registered non-bank brokers will also gain direct access to the NDS-OM platform, promoting broader participation in government securities trading. Additionally, a working group will review trading and settlement timings to align with market developments such as increased electronic trading and 24/7 payment system availability.

To strengthen cybersecurity, RBI is launching exclusive domains—’bank.in’ for banks and ‘fin.in’ for non-bank financial entities—to curb fraud in digital transactions. The initiative, starting in April 2025, aims to enhance trust in online banking. In payment systems, the RBI proposes Additional Factor of Authentication (AFA) for cross-border card-not-present transactions, extending the security measures already in place for domestic transactions. These updates align with RBI’s ongoing efforts to ensure financial stability, consumer protection, and efficiency in the evolving economic landscape.

******

Reserve Bank of India

Statement on Developmental and Regulatory Policies

This Statement sets out various developmental and regulatory policy measures relating to (i) Financial Markets ; (ii) Cybersecurity ; and (iii) Payment Systems.

I. Financial Markets

1. Introduction of forward contracts in Government securities

Over the past few years, the Reserve Bank has been expanding the suite of interest rate derivative products available to market participants to manage their interest rate risks. In addition to Interest Rate Swaps, products such as Interest Rate Options, Interest Rate Futures, Interest Rate Swaptions, Forward Rate Agreements, etc. are available to market participants. We have been receiving feedback about the need to allow forward contracts in Government securities to enable further market development. Such forward contracts will enable long-term investors such as insurance funds to manage their interest rate risk across interest rate cycles. They will also enable efficient pricing of derivatives that use bonds as underlying instruments. Draft directions in this regard were issued in December 2023. The final directions, taking into account the public feedback, will be issued shortly.

2. Access of SEBI-registered non-bank brokers to NDS-OM

The Negotiated Dealing System – Order Matching (NDS-OM) is an electronic trading platform for secondary market transactions in government securities. Access to NDS-OM is, at present, available to regulated entities and to the clients of banks and standalone primary dealers. With a view to widening access, it has been decided that non-bank brokers registered with SEBI can directly access NDS-OM, on behalf of their clients. These brokers may access NDS-OM subject to the regulations and conditions laid down by the Reserve Bank in this regard. Necessary instructions are being issued separately.

3. Comprehensive review of trading and settlement timings across various market segments

Synchronized and complimentary market and settlement timings across various financial market segments can facilitate benefits of efficient price discovery and optimization of the liquidity requirements. Over the last few years, there have been several developments including increased electronification of trading, availability of forex and certain interest rate derivative markets on a 24X5 basis, increased participation of non-residents in domestic financial markets and availability of payment systems on a 24X7 basis. Accordingly, it has been decided to set up a working group with representation from various stakeholders to undertake a comprehensive review of trading and settlement timing of financial markets regulated by the Reserve Bank. The Group is expected to submit its report by April 30, 2025.

II. Cybersecurity

4. Enhancing Trust in the Financial Sector through ‘bank.in’ and ‘fin.in’ domains

Increased instances of fraud in digital payments are a significant concern. To combat the same, the Reserve Bank of India (RBI) is introducing the ‘bank.in’ exclusive Internet Domain for Indian banks. This initiative aims to reduce cyber security threats and malicious activities like phishing; and, streamline secure financial services, thereby enhancing trust in digital banking and payment services. The Institute for Development and Research in Banking’ Technology (IDRBT) will act as the exclusive registrar. The actual registrations will commence from April 2025. Detailed guidelines for banks will be issued separately. Going forward, it is planned to have an exclusive domain viz., “fin.in” for other non-bank entities in the financial sector.

III. Payment Systems

5. Enabling Additional Factor of authentication in cross-border Card Not Present transactions

Introduction of Additional Factor of Authentication (AFA) for digital payments has enhanced the safety of transactions which, in turn, provided confidence to customers to adopt digital payments. This requirement, however, is mandatory for domestic transactions only.

In order to provide a similar level of safety for online international transactions using cards issued in India, it is proposed to enable AFA for international card not present (online) transactions as well. This will provide an additional layer of security in cases where the overseas merchant is enabled for AFA. Draft circular will be issued shortly for feedback from stakeholders.

(Puneet Pancholy)

Chief General Manager

Press Release: 2024-2025/2096

Governor’s Statement: February 7, 2025

The Monetary Policy Committee (MPC) met on 5th, 6th and 7th of this month. You are aware that the Governor’s Statement after the MPC meeting contains not only the resolution of the MPC with regard to the policy rate and stance but also other announcements and measures, which have a bearing on the monetary and regulatory policies. The MPC resolution is of course of interest to a large number of people from various walks of life, as it impacts the lives of virtually all citizens of the country. The resolution also provides the rationale and the thought process of the MPC, and is of relevance to businesses, economists, academicians and the finance world. Apart from these MPC related announcements, the Governor’s statement has become an important medium for the Reserve Bank to highlight its priorities on which it would like the regulated entities to focus their energies on. It is an opportunity to point out areas of concern and challenges for the stakeholders to address their attention to. It is an occasion for the Reserve Bank to articulate its views on critical areas of interest. I will continue with this practice of a detailed statement.

2. Before I come to the resolution of the MPC, allow me a moment to reflect on the experience of flexible inflation targeting (FIT) framework, introduced in the year 2016 and reviewed in 2021. I believe that it has served the Indian economy well over these years, including the challenging period since the pandemic. The average inflation has been lower post the introduction of FIT. Moreover, CPI inflation has mostly stayed aligned with the target, barring a few occasions of breaching the upper tolerance band since its inception. We will continue to improve the macroeconomic outcomes in the best interest of the economy using the flexibility embedded in the framework while responding to the evolving growth-inflation dynamics. Moreover, we will strive to further refine the building blocks of this framework by making advances in the use of new data, improving nowcasting and forecasting of key macroeconomic variables and developing more robust models.

3. On the regulatory front, I would like to mention, especially in the context of some of the proposed regulatory changes pertaining to liquidity coverage ratio (LCR), expected credit loss (ECL) framework for provisioning by banks, and the prudential norms governing projects under implementation, that we will continue to strengthen, rationalise and refine the prudential and conduct-related regulatory framework in the overall interest of the economy. The interest of the economy demands financial stability and consumer protection. Our mandate is to enhance both of them. At the same time, economic interest also warrants increasing efficiency, which too is our duty. We recognise that just like there are no free lunches, regulation to enhance stability and consumer protection too is not devoid of costs. There are trade-offs between stability and efficiency. We will keep this trade-off in mind while formulating regulations. It will be our attempt to strike the right balance, keeping in view the benefits and costs of each and every regulation. I also want to reassure all stakeholders that we will continue the consultative process in regulation-making. The suggestions of stakeholders are valuable and we will give serious consideration to them before taking any major decision. We will also ensure that the implementation of such regulations is smooth; we will give sufficient time for transition and where regulations have major implications, the implementation will be done in a phased manner.

4. The global economic backdrop remains challenging. The global economy is growing below the historical average1even though high frequency indicators suggest resilience2along with continued expansion in trade.3 Progress on global disinflation is stalling, hindered by services price inflation.

5. With receding expectations on the size and pace of rate cuts in the US, the US dollar has strenthened and bond yields have hardened. Emerging Market Economies (EMEs) have witnessed large capital outflows, leading to sharp depreciation of their currencies and tightening of financial conditions. Divergent trajectories of monetary policy across advanced economies, lingering geopolitical tensions and elevated trade and policy uncertainties have exacerbated financial market volatility. Such an uncertain global environment has posed difficult policy trade-offs for EMEs.

6. The Indian economy, though continuing to remain strong and resilient, also did not remain immune to these global headwinds, with the Indian Rupee coming under depreciation pressure in the recent months.4At the Reserve Bank, we have been employing all tools at our disposal to face the multi-pronged challenges.

Decisions of the Monetary Policy Committee (MPC)

7. In this backdrop, the MPC, after a detailed assessment of the evolving macroeconomic and financial developments and the economic outlook, decided unanimously to reduce the policy repo rate by 25 basis points from 6.50 per cent to 6.25 per cent. Consequently, the standing deposit facility (SDF) rate shall be 6.00 per cent and the marginal standing facility (MSF) rate and the Bank Rate shall be 6.50 per cent. The MPC also decided unanimously to continue with the neutral stance and remain unambiguously focussed on a durable alignment of inflation with the target, while supporting growth.

8. I shall state the rationale for the decision in brief. The MPC noted that inflation has declined. Supported by a favourable outlook on food and continuing transmission of past monetary policy actions, it is expected to further moderate in 2025-26, gradually aligning with the target. The MPC also noted that though growth is expected to recover from the low of Q2 of 2024-25, it is much below that of last year. These growth-inflation dynamics open up policy space for the MPC to support growth, while remaining focussed on aligning inflation with the target. Accordingly, the MPC decided to reduce the policy repo rate by 25 basis points to 6.25 per cent.

9. At the same time, excessive volatility in global financial markets and continued uncertainties about global trade policies coupled with adverse weather events pose risks to the growth and inflation outlook. This calls for the MPC to remain watchful. Accordingly, it decided to continue with a neutral stance. This will provide MPC the flexibility to respond to the evolving macroeconomic environment.

Assessment of Growth and Inflation

Growth

10. As per the first advance estimates, real GDP growth for the current year is estimated at 6.4 per cent, a softer expansion after a robust 8.2 per cent growth last year.5Going forward, economic activity is expected to improve in the coming year. Agricultural activity remains upbeat on the back of healthy reservoir levels6and bright rabi prospects.7 Manufacturing activity is expected to recover gradually in the second half of this year and beyond.8 Early corporate results for Q3 indicate a mild recovery in the manufacturing sector.9 Mining and electricity are rebounding from monsoon related disruptions in Q2. Business expectations remain upbeat, as evidenced from the PMI manufacturing future output index.10 Services sector activity continues to be resilient.11 PMI services, however, declined from its recent peak.12

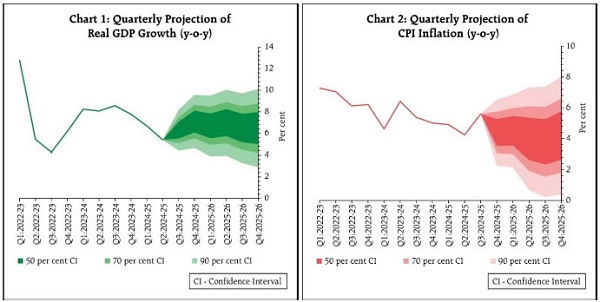

11. On the demand side, rural demand continues to be on an uptrend, while urban consumption remains subdued with high frequency indicators providing mixed signals.13Going forward, improving employment conditions,14tax relief in the Union Budget, and moderating inflation,15 together with healthy agricultural activity bode well for household consumption. Government consumption expenditure is expected to remain modest.16 Higher capacity utilisation levels,17 robust business expectations18 and government policy support augur well for growth in fixed investment.19 Continued buoyancy in services exports will support growth.20 Global headwinds, however, continue to impart uncertainty to the outlook and pose downward risks. Taking all these factors into consideration, real GDP growth for the next year is projected at 6.7 per cent with Q1 at 6.7 per cent; Q2 at 7.0 per cent; Q3 at 6.5 per cent; and Q4 at 6.5 per cent. The risks are evenly balanced.

Inflation

12. Headline inflation, after moving above the upper tolerance band in October, has since registered a sequential moderation in November and December.21Going ahead, food inflation pressures, absent any supply side shocks, should see a significant softening due to good kharifproduction,22 winter-easing in vegetable prices23 and favourable rabi crop prospects. Core inflation is expected to rise but remain moderate. Rising uncertainty in global financial markets coupled with continuing volatility in energy prices and adverse weather events presents upside risks to the inflation trajectory. 24 Taking all these factors into consideration, CPI inflation for the current financial year is projected at 4.8 per cent with Q4 at 4.4 per cent. Assuming a normal monsoon, CPI inflation for the financial year 2025-26 is projected at 4.2 per cent with Q1 at 4.5 per cent; Q2 at 4.0 per cent; Q3 at 3.8 per cent; and Q4 at 4.2 per cent. The risks are evenly balanced.

External Sector

13. Coming to the external sector, India’s current account deficit (CAD) moderated from 1.3 per cent of GDP in Q2 of last year to 1.2 per cent in Q2 of this year.25According to the World Bank, India, with an estimated inflow of 129.1 billion US dollars, continues to remain the largest recipient of remittances globally in 2024.26The CAD for this year is expected to remain well within the sustainable level. As on 31st January this year, India’s foreign exchange reserves stood at 630.6 billion US dollars, providing an import cover of over 10 months.27 Overall, India’s external sector remains resilient as key indicators stay robust.28

14. I would like to mention here that the Reserve Bank’s exchange rate policy has remained consistent over the years. Our stated objective is to maintain orderliness and stability, without compromising market efficiency. Accordingly, our interventions in the forex market focus on smoothening excessive and disruptive volatility rather than targeting any specific exchange rate level or band. The exchange rate of the Indian Rupee is determined by market forces.

Liquidity and Financial Market Conditions

15. After remaining in surplus from July to November 2024, system liquidity – as measured by the average net position under the liquidity adjustment facility (LAF) – turned into deficit during December 2024 and January 2025. The drainage of liquidity is mainly attributed to advance tax payments in December 2024, capital outflows, forex operations and a significant pickup in currency in circulation in January this year.

16. It has been observed that some banks are reluctant to onlend in the uncollateratised call money market; instead, they are passively parking funds with the Reserve Bank. We urge the banks to actively trade among themselves in the uncollateratised call money market to make it deeper and vibrant for better signal extraction from the weighted average call money rate (WACR).

17. The Reserve Bank is committed to provide sufficient system liquidity. We have taken a number of steps in this regard.29We will continue to monitor the evolving liquidity and financial market conditions and proactively take appropriate measures to ensure orderly liquidity conditions.

Financial Stability

18. The system-level financial parameters for Scheduled Commercial Banks (SCBs) continue to be healthy.30The Credit Deposit Ratio (CD ratio) for the banking system at the end of January 2025 was at 80.8 per cent, broadly similar to that on 30th September, 2024. Bank liquidity buffers are sufficient. Though the net interest margin (NIM) moderated, return on assets (RoA) and return on equity (RoE) are robust. The system-level parameters for NBFCs too are healthy.31

19. The Reserve Bank has been observing Financial Literacy Week annually since 2016 to enhance financial education. Last year, the campaign focused on empowering young adults. This year, recognising the critical and multifaceted role of women in society, the campaign will emphasise on women’s role in financial decision-making and household budgeting. I urge all banks to actively participate in the campaign on the theme “Financial Literacy: Women’s Prosperity”, starting from 24th of this month.

Additional Measures

20. I shall now announce certain additional measures. Necessary directions and circulars for their implementation shall be issued separately.

Digital security

21. First, the rapid digitalisation of financial services has brought convenience and efficiency but has also increased exposure to cyber threats and digital risks, which are getting sophisticated day by day. The surge in digital frauds is a matter of concern, warranting action by all stakeholders.

22. The Reserve Bank has been taking various measures to enhance digital security in the banking and payments system. Introduction of Additional Factor of Authentication (AFA) for domestic digital payments is one such measure. It is proposed to extend AFA to online international digital payments made to offshore merchants, who are enabled for such authentication.

23. Second, the Reserve Bank shall implement the ‘bank.in’ exclusive Internet Domain for Indian banks. Registration of this domain name will commence from April this year. This will help avoid banking frauds. This will be followed by the ‘fin.in’ domain for the financial sector.

24. Banks and NBFCs must continuously improve preventive and detective controls to mitigate cyber risks. They must develop robust incident response and recovery mechanisms, reinforced through periodic testing, for operational resilience.

Introduction of forward contracts in Government Securities

25. Third, over the past few years, we have expanded the suite of interest rate derivative products available to market participants to manage their interest rate risks. We shall now include forward contracts in Government securities to this suite. This would facilitate long-term investors such as insurance funds to manage their interest rate risk across interest rate cycles. It will also enable efficient pricing of derivatives that use Government securities as underlying instruments.

Access of SEBI-registered non-bank brokers to NDS-OM

26. Fourth, to enhance access of retail investors to government securities, the Reserve Bank shall expand the access of NDS-OM, the electronic trading platform for secondary market transactions in government securities, to non-bank brokers registered with SEBI.

Review of trading and settlement timings across various market segments

27. Fifth, in view of the various developments in financial markets and market infrastructure over the past few years, we shall set up a working group with representation from various stakeholders to undertake a comprehensive review of trading and settlement timing of markets regulated by the Reserve Bank. The Group shall submit its report by 30th April of this year.

Concluding Remarks

28. To conclude, considering the existing growth-inflation dynamics, the MPC, while continuing with the neutral stance, felt that a less restrictive monetary policy is more appropriate at the current juncture. The MPC will take a decision in each of its future meetings based on a fresh assessment of the macroeconomic outlook.

29. We are committed to conduct monetary policy and take such measures, as appropriate, which are timely, carefully calibrated and clearly communicated, to facilitate conducive macroeconomic conditions that reinforce price stability, sustained economic growth and financial stability.

Thank you. Namaskar and Jai Hind.

(Puneet Pancholy)

Chief General Manager

Press Release: 2024-2025/2095

Notes:

1 According to the World Economic Outlook update, IMF (January 2025), global growth is projected at 3.3 per cent both in 2025 and 2026, below the historical (2000-19) average of 3.7 per cent.

2 The global composite PMI at 51.8 in January 2025 remained in the expansion zone even as services sector activity eased. The global manufacturing PMI at 50.1 also returned to the expansion zone after six months of contraction.

3 World merchandise trade volume grew by 3.6 per cent (y-o-y) in November as per CPB Netherlands, World Trade Monitor.

4 The Indian rupee (INR) depreciated by 3.2 per cent against the US dollar since November 6, 2024, the day the presidential election results were announced in the US, largely mirroring the 2.4 per cent appreciation in the dollar index during the same period.

5 GVA of mining and quarrying, manufacturing, and electricity, gas and water supply is estimated to expand by 2.9 per cent, 5.3 per cent, and 6.8 per cent, respectively in 2024-25. Gross fixed capital formation (GFCF), the dominant component of real investment, is estimated to expand by 6.4 per cent as against 9.0 per cent growth in the last year. Private final consumption expenditure (PFCE) is estimated to grow at a robust pace of 7.3 per cent in 2024-25 vis-à-vis 4.0 per cent in the previous year. GVA of agriculture and allied activities accelerated to 3.8 per cent in 2024-25 from 1.4 per cent in the previous year. During April-December 2024, wholesale two-wheeler sales recorded 11.6 per cent growth. Work demand under MGNREGA contracted by 9.2 per cent during April-January 2024-25.

6 All-India water storage in 155 major reservoirs stands at 64 per cent of the total capacity as of January 30, 2025, as against 52 per cent a year ago and decadal average of 55 per cent.

7 As on January 31, 2025, rabi sowing has surpassed last year’s level as well as normal sowing acreage by 1.5 per cent and 4.1 per cent, respectively.

8 Manufacturing GVA growth decelerated in Q2:2024-25 on account of subdued results of petroleum products, iron and steel, and cement companies.

9 Operating profit of 393 listed private manufacturing companies expanded modestly by 0.9 per cent (y-o-y) during Q3:2024-25 as against a contraction of 5.4 per cent observed in Q2:2024-25.

10 PMI Manufacturing Future Output Index in January 2025 expanded to 65.1 from 62.5 in December 2024. Future Output Index has hovered above 60.0 since April 2023.

11 E-way bills increased by 17.6 per cent in December 2024. GST revenues at ₹1.96 lakh crore rose by 12.3 per cent and toll collections expanded by 14.8 per cent during January 2025. Petroleum products consumption expanded by 2.1 per cent in December 2024. Aggregate bank credit and deposits registered growth of 12.5 per cent and 10.6 per cent, respectively, as on January 24, 2025.

12 PMI services for January 2025 moderated to 56.5 from 59.3 in December 2024.

13 Domestic air passengers traffic rose by 10.8 per cent in December 2024 and 14.2 per cent in January 2025 so far.

14 According to quarterly periodic labour force survey (PLFS), urban unemployment rate dipped to 6.4 per cent in Q2:2024-25 from 6.6 per cent in the same quarter last year.

15 Combined consumer price index-based inflation moderated to 5.2 per cent in December 2024 from 6.2 per cent in October 2024.

16 Central government revenue expenditure (net of interest payments and subsidies) is budgeted to grow at 5.0 per cent in 2025-26 as against 7.9 per cent growth in 2024-25 (Revised Estimates).

17 As per the quarterly order books, inventories, and capacity utilisation (OBICUS) survey of the RBI, seasonally adjusted capacity utilisation (CU) of the manufacturing sector at 74.7 per cent in Q2:2024-25 is above the long-term average of 73.8 per cent.

18 As per the Industrial Outlook Survey (IOS) of RBI, manufacturing firms assessed marginal improvement in demand conditions in Q3:2024-25. Further, firms expect marginal improvement in Q4:2024-25 and significant improvement in H1:2025-26.

19 As per the Union Budget 2025-26, the central government’s capex is budgeted to expand by 10.1 per cent during 2025-26. Effective capital expenditure (including grants-in-aid to state governments for capital expenditure) is budgeted to grow at 17.4 per cent during the financial year.

20 During April-December 2024, services export expanded by 13.3 per cent as compared with 5.1 per cent recorded in the same period previous year.

21 The CPI headline inflation moderated by 98 basis points between October and December 2024.

22 As per the first advance estimates of kharif production for 2024-25 released on November 5, 2024, rice production is expected to increase by 5.9 per cent, while tur and moong dal production is expected to be higher by 2.5 per cent and 19.8 per cent, respectively in 2024-25, compared to 2023-24.

23 High frequency food price data from Department of Consumer Affairs (DCA) points to a significant month-on-month correction in prices of tomatoes, onions, and potatoes in January 2025.

24 Indian basket crude oil prices registered a month-on-month decline of around (-) 2.8 per cent in November 2024, while it increased marginally by 0.4 per cent in December. In January 2025, Indian basket crude oil prices at US$ 80 per barrel registered an increase of 9.4 per cent over December 2024.

25 India’s current account deficit (CAD) moderated marginally to US$ 11.2 billion (1.2 per cent of GDP) in Q2:2024-25 from US$ 11.3 billion (1.3 per cent of GDP) in Q2:2023-24.

26 https://blogs.worldbank.org/en/peoplemove/in-2024–remittance-flows-to-low–and-middle-income-countries-ar

27 Based on actual merchandise imports (on a BoP basis) during the four quarters period (Q3:2023-24 to Q2:2024-25).

28 India’s external debt to GDP ratio stood at 19.4 per cent at end-September 2024 (18.8 per cent at end-June 2024), while the net international investment position (IIP) moderated to (-) 9.6 per cent of GDP at end-September 2024 from (-) 10.3 per cent of GDP at end-June 2024.

29 These included daily Variable Rate Repo auctions from 16th January 2025 and purchase of government securities of 58,835 crore rupees through open market operations (OMOs) in January. In addition, a package of measures was announced on 27th January 2025 to inject durable liquidity through OMOs, forex buy-sell swap and a 56-day variable rate repo to be conducted later today.

30 SCB Parameters: The outstanding credit and deposit on a y-o-y basis increased by 11.4 per cent and 10.3 per cent respectively as of January 24, 2025. The system-level CRAR of 16.7 per cent in September 2024 was well above the regulatory minimum level. GNPA ratio at 2.5 per cent in September 2024 improved by 72 bps over September 2023. SMA-2 Ratio was 0.8 per cent in September 2024. LCR was 128.6 per cent as of September 2024. ROA was 1.4 per cent and RoE was 14.6 per cent in September 2024. The NIM was 3.5 per cent in September 2024 vis-à-vis 3.7 per cent in September 2023.

31 NBFC Parameters: Total CRAR of NBFCs is 26.5 per cent and Tier I CRAR is 24.4 per cent, as on 30th, September 2024. GNPA ratio improved from 2.9 per cent in September 2023 to 2.6 per cent in September 2024. The RoA improved from 2.9 per cent in September 2023 to 3.2 per cent in September 2024. YoY growth in advances was 16.4 per cent in September 2024 as compared to 22.5 per cent in September 2023.

Monetary Policy Statement, 2024-25 Resolution of the Monetary Policy Committee February 5 to 7, 2025

Monetary Policy Decisions

The Monetary Policy Committee (MPC) held its 53rd meeting from February 5 to 7, 2025 under the chairmanship of Shri Sanjay Malhotra, Governor, Reserve Bank of India. The MPC members Dr. Nagesh Kumar, Shri Saugata Bhattacharya, Prof. Ram Singh, Dr. Rajiv Ranjan, and Shri M. Rajeshwar Rao attended the meeting. After assessing the current and evolving macroeconomic situation, the MPC unanimously decided to:

- reduce the policy repo rate under the liquidity adjustment facility (LAF) by 25 basis points to 6.25 per cent with immediate effect; consequently, the standing deposit facility (SDF) rate shall stand adjusted to 6.00 per cent and the marginal standing facility (MSF) rate and the Bank Rate to 6.50 per cent;

- continue with the neutral monetary policy stance and remain unambiguously focussed on a durable alignment of inflation with the target, while supporting growth.

These decisions are in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4 per cent within a band of +/- 2 per cent, while supporting growth.

Growth and Inflation Outlook

2. The global economy is growing below the historical average even though high frequency indicators suggest resilience amidst continued expansion in world trade. The world economic landscape remains challenging with slower pace of disinflation, lingering geopolitical tensions and policy uncertainties. The strong dollar, inter alia, continues to strain emerging market currencies and enhance volatility in financial markets.

3. On the domestic front, as per the First Advance Estimates (FAE), real gross domestic product (GDP) is estimated to grow at 6.4 per cent (y-o-y) in 2024-25 supported by a recovery in private consumption. On the supply side, growth is supported by the services sector and a recovery in agriculture sector, while tepid industrial growth is a drag.

4. Looking ahead, healthy rabi prospects and an expected recovery in industrial activity should support economic growth in 2025-26. Among the key drivers on the demand side, household consumption is expected to remain robust aided by the tax relief in the Union Budget 2025-26. Fixed investment is expected to recover, supported by higher capacity utilisation levels, healthy balance sheets of financial institutions and corporates, and Government’s continued emphasis on capital expenditure. This is corroborated by positive business sentiments highlighted in the Reserve Bank’s enterprise surveys and PMIs. Resilient services exports will continue to support growth. However, headwinds from geo-political tensions, protectionist trade policies, volatility in international commodity prices and financial market uncertainties, continue to pose downside risks to the outlook. Taking all these factors into consideration, real GDP growth for 2025-26 is projected at 6.7 per cent with Q1 at 6.7 per cent; Q2 at 7.0 per cent; and Q3 and Q4 at 6.5 per cent each (Chart 1). The risks are evenly balanced.

5. Headline inflation softened sequentially in November-December 2024 from its recent peak of 6.2 per cent in October. The moderation in food inflation, as vegetable price inflation came off from its October high, drove the decline in headline inflation. Core inflation remained subdued across goods and services components and the fuel group continued to be in deflation.

6. Going ahead, food inflation pressures, absent any supply side shock, should see a significant softening due to good kharif production, winter-easing in vegetable prices and favourable rabi crop prospects. Core inflation is expected to rise but remain moderate. Continued uncertainty in global financial markets coupled with volatility in energy prices and adverse weather events presents upside risks to the inflation trajectory. Taking all these factors into consideration, CPI inflation for 2024-25 is projected at 4.8 per cent with Q4 at 4.4 per cent. Assuming a normal monsoon next year, CPI inflation for 2025-26 is projected at 4.2 per cent with Q1 at 4.5 per cent; Q2 at 4.0 per cent; Q3 at 3.8 per cent; and Q4 at 4.2 per cent (Chart 2). The risks are evenly balanced.

Rationale for Monetary Policy Decisions

7. The MPC noted that inflation has declined. Supported by a favourable outlook on food and continuing transmission of past monetary policy actions, it is expected to further moderate in 2025-26, gradually aligning with the target. The MPC also noted that though growth is expected to recover from the low of Q2:2024-25, it is much below that of last year. These growth-inflation dynamics open up policy space for the MPC to support growth, while remaining focussed on aligning inflation with the target. Accordingly, the MPC unanimously voted to reduce the policy repo rate by 25 basis points to 6.25 per cent.

8. At the same time, excessive volatility in global financial markets and continued uncertainties about global trade policies coupled with adverse weather events pose risks to the growth and inflation outlook. This calls for the MPC to remain watchful. Accordingly, the MPC unanimously voted to continue with a neutral stance. This will provide MPC the flexibility to respond to the evolving macroeconomic environment.

9. The minutes of the MPC’s meeting will be published on February 21, 2025.

10. The next meeting of the MPC is scheduled during April 7 to 9, 2025.

(Puneet Pancholy)

Chief General Manager

Press Release: 2024-2025/2094