Reserve Bank of India

Governor’s Statement

April 8, 2022

Two years ago in March 2020, we began a journey to fight the onslaught of COVID-19 on our economy with courage and determination. During the period thereafter, the Reserve Bank has successfully navigated its course through turbulent waters. While the pandemic has scarred our psyche and tested our resilience, we have responded with bold, unconventional and resolute measures to stabilise the economy through three waves of the pandemic. As the situation normalised, we have taken measures towards rebalancing liquidity conditions while ensuring that our actions are nimble and proactive but well-timed.

2. Now two years later, as we were emerging out of the pandemic situation, the global economy has seen tectonic shifts beginning 24th February, with the commencement of the war in Europe, followed by sanctions and escalating geopolitical tensions. We are confronted with new but humungous challenges – shortages in key commodities; fractures in the international financial architecture; and fears of deglobalisation. Extreme volatility characterises commodity and financial markets. While the pandemic quickly morphed from a health crisis to one of life and livelihood, the conflict in Europe has the potential to derail the global economy. Caught in the cross-current of multiple headwinds, our approach needs to be cautious but proactive in mitigating the adverse impact on India’s growth, inflation and financial conditions. We are, however, reassured by the strong buffers that we have built over the past few years, including large foreign exchange reserves, significant improvement in external sector indicators and substantial strengthening of the financial sector, all of which would help us to weather this storm. Once again, we in the RBI stand resolute and in readiness to defend the economy and navigate out of the current storm.

Decisions and Deliberations of the Monetary Policy Committee

3. Against this backdrop, the Monetary Policy Committee (MPC) met on 6th, 7th and 8th April 2022 and, based on an assessment of the macroeconomic situation and the outlook, voted unanimously to keep the policy repo rate unchanged at 4 per cent. The MPC also decided unanimously to remain accommodative while focussing on withdrawal of accommodation to ensure that inflation remains within the target going forward, while supporting growth. The marginal standing facility (MSF) rate and the Bank rate remain unchanged at 4.25 per cent. Further, it has been decided by the Reserve Bank to restore the width of the Liquidity Adjustment Facility (LAF) corridor to 50 basis points, the position that prevailed before the pandemic. The floor of the corridor will now be provided by the newly instituted standing deposit facility (SDF), which will be placed 25 basis points below the repo rate, i.e., at 3.75 per cent. I shall explain the details in this regard later in my statement.

4. Let me first dwell upon the MPC’s rationale for its decision on the policy rate and the stance. Since the MPC’s last meeting in early February 2022, the expected positive benefits from the ebbing Omicron wave have been offset by the sharp escalation in geopolitical tensions. This has significantly changed the external and domestic landscape. Concerns over protracted supply disruptions have rattled global commodity and financial markets, given the significant share of the two economies engaged in war in global production and exports of key commodities like oil and natural gas; wheat and corn; palladium, aluminium and nickel; edible oils; and fertilisers. Global crude oil prices briefly crossed US$ 130 per barrel, touching their highest level since 2008 and remain volatile at elevated levels, despite some correction. Global food prices along with metal and other commodity prices have also hardened significantly. Risk aversion towards assets of emerging market economies (EMEs) has increased, leading to large capital outflows and a depreciating bias in their currencies. These developments have, first, ratcheted up the projections of global inflation, which was already running well above targets in major countries; and second, will produce sizeable adverse impact on output across geographies.

5. The geopolitical tensions have exacerbated at a time when the global economy was grappling with a sharp rise in inflation and consequent monetary policy normalisation in major advanced economies. Global supply chain disruptions and input cost pressures are now expected to linger even longer. The resurgence of COVID-19 infections in some major economies in March and the associated lockdowns run the risk of further aggravating the global supply bottlenecks and input cost pressures. World trade and output and hence external demand are likely to be weaker than envisaged two months ago. Overall, the external developments during the past two months have led to the materialisation of downside risks to the domestic growth outlook and upside risks to inflation projections presented in the February MPC resolution. Inflation is now projected to be higher and growth lower than the assessment in February. Economic activity, although recovering, is barely above its pre-pandemic level. Against this backdrop, the MPC decided to retain the repo rate at 4 per cent. It also decided to remain accommodative while focusing on withdrawal of accommodation to ensure that inflation remains within the target going forward, while supporting growth.

Assessment of Growth and Inflation

Growth

6. According to the second advance estimates released by the National Statistical Office (NSO) on February 28, 2022, real GDP rose by 8.9 per cent in 2021-22. Private consumption and fixed investment – key drivers of domestic demand – however, remain subdued, with these two components being only 1.2 per cent and 2.6 per cent respectively, above their pre-pandemic levels. On the supply side, contact-intensive services still trail the 2019-20 level. Nevertheless, the Indian economy is steadily reviving from its pandemic induced contraction.

7. During 2021-22, weakness in economic activity resurfaced in Q3 and got exacerbated by the emergence of the Omicron variant in January 2022. A gradual turnaround has been noticed during February, although in March 2022 a mixed picture was seen. Some contact-intensive activities have regained traction amidst declining infections and removal of restrictions. Several high frequency indicators – railway freight; GST collections; toll collections; electricity demand; fuel consumption; and imports of capital goods posted robust year-on-year expansion during February-March. With the easing of restrictions, domestic air passenger traffic rebounded in March. According to our surveys, consumer confidence is improving and households’ optimism in outlook for the year ahead has strengthened with an uptick in sentiments. Business confidence is in optimistic territory and supportive of revival in economic activity. On the other hand, passenger vehicle sales and registrations continue to contract, though at a moderating pace. Both manufacturing and services PMIs remain in the zone of expansion; while manufacturing PMI moderated slightly in March, services and composite showed improvement.

8. Going forward, robust Rabi output should support recovery in rural demand, while a pick-up in contact-intensive services should help in further strengthening urban demand. Investment activity may gain traction with improving business confidence, pick up in bank credit, continuing support from government capex and congenial financial conditions. Capacity utilisation (CU) in the manufacturing sector recovered further to 72.4 per cent in Q3:2021-22 from 68.3 per cent in the previous quarter, surpassing the pre-pandemic level of 69.9 per cent in Q4:2019-20.

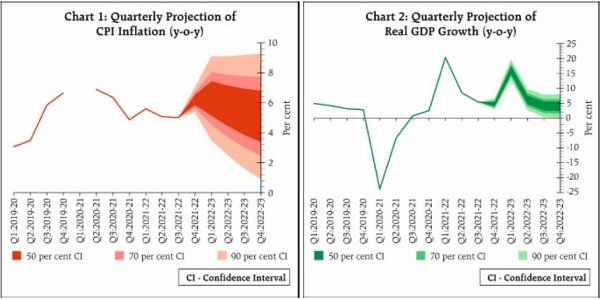

9. As the horizon was brightening up, escalating geopolitical tensions have cast a shadow on our economic outlook. Although India’s direct trade exposure to countries at the epicentre of the conflict is limited, the war could potentially impede the economic recovery through elevated commodity prices and global spillover channels. Further, financial market volatility induced by monetary policy normalisation in advanced economies, renewed COVID-19 infections in some major countries with augmented supply-side disruptions and protracted shortages of critical inputs, such as semi-conductors and chips, pose downside risks to the outlook. Taking all these factors into consideration, real GDP growth for 2022-23 is now projected at 7.2 per cent with Q1:2022-23 at 16.2 per cent; Q2 at 6.2 per cent; Q3 at 4.1 per cent; and Q4 at 4.0 per cent, assuming crude oil (Indian basket) at US$ 100 per barrel during 2022-23.

Inflation

10. The February 2022 meeting of the MPC had projected a moderating path for inflation during 2022-23. Heightened geopolitical tensions since end-February have, however, upended the earlier narrative and considerably clouded the inflation outlook for the year. On the food price front, a likely record Rabi harvest would help to keep domestic prices of cereals and pulses in check. Global factors such as the loss of wheat supply from the Black Sea region and the unprecedented high international prices of wheat could, however, put a floor under domestic wheat prices. Edible oil price pressures are likely to remain elevated in the near-term due to export restrictions by key producers as well as loss of supply from the Black Sea region. Feed cost pressures could continue due to global supply shortages, which could also have a spillover impact on poultry, milk and dairy product prices.

11. Coming to non-food items, the spike in international crude oil prices since end-February poses substantial upside risk to inflation through both direct and indirect effects. Sharp increase in domestic pump prices could trigger broad-based second round price pressures. A combination of high international commodity prices and elevated logistic disruptions could aggravate input costs across agriculture, manufacturing and services sectors. Their pass-through to retail prices, therefore, warrants continuous monitoring and pro-active supply management. Financial markets are likely to remain volatile on rising risk premia, dislocations in trade and capital flows and divergent monetary policy responses across central banks. Taking into account these factors and on the assumption of a normal monsoon in 2022 and average crude oil price (Indian basket) of US $ 100 per barrel, inflation is now projected at 5.7 per cent in 2022-23, with Q1 at 6.3 per cent; Q2 at 5.8 per cent; Q3 at 5.4 per cent; and Q4 at 5.1 per cent.

12. It may, however, be noted that given the excessive volatility in global crude oil prices since late February and the extreme uncertainty over the evolving geopolitical tensions, any projection of growth and inflation is fraught with risk, and is largely contingent upon future oil and commodity price developments.

13. In this context, continuation and deepening of supply side measures may alleviate food price pressures and also mitigate cost-push pressures across manufacturing and services. On our part, let me assure all stakeholders that as in the past, the Reserve Bank will use all its policy levers to preserve macroeconomic stability and enhance the resilience of our economy. The situation is dynamic and fast changing and our actions have to be tailored accordingly.

Liquidity and Financial Market Conditions

14. As stated earlier, the macroeconomic outlook is undergoing tectonic shifts and our policy response has to be pre-emptive and re-calibrated dynamically to the evolving outlook. The Reserve Bank will continue to adopt a nuanced and nimble footed approach to liquidity management while maintaining adequate liquidity in the system. At present, liquidity management is characterised by two-way operations: through variable rate reverse repo (VRRR) auctions of varying maturities to absorb liquidity; and variable rate repo (VRR) auctions to meet transient liquidity shortages and offset mismatches. This approach will be continued.

15. It may be noted that the interest rate for around 80 per cent of the total liquidity absorbed under the LAF during Q4:2021-22 has firmed up close to the policy repo rate due to the rebalancing of liquidity through VRRR auctions. Accordingly, financial market participants have been prepared for the eventual normalisation of the LAF corridor.

16. Further, it has now been decided to fully restore the liquidity management framework instituted in February 2020, albeit with some refinements to enhance its effectiveness. Accordingly, the following measures are being instituted:

i. The amendment to Section 17 of the RBI Act in 2018 empowered the Reserve Bank to introduce the Standing Deposit Facility (SDF). By removing the binding collateral constraint on the central bank, the SDF strengthens the operating framework of monetary policy. Accordingly, it has now been decided to introduce the SDF as the floor of the LAF corridor. This would provide symmetry to the operating framework of monetary policy by introducing a standing absorption facility at the bottom of the LAF corridor, similar to the standing injection tool at the upper end of the corridor, namely the marginal standing facility (MSF). Thus, at both ends of the LAF corridor, there will be standing facilities – one to absorb and the other to inject liquidity. Accordingly, access to SDF and MSF will be at the discretion of banks, unlike repo/reverse repo, OMO and CRR which are available at the discretion of the Reserve Bank. Notably, the SDF is also a financial stability tool in addition to its role in liquidity management.

ii. The SDF rate will be 25 bps below the policy rate, and it will be applicable to overnight deposits at this stage. It would, however, retain the flexibility to absorb liquidity of longer tenors as and when the need arises, with appropriate pricing. The MSF rate will continue to be 25 bps above the policy repo rate. Thus, the width of the LAF corridor is restored to the pre-pandemic configuration of 50 bps, symmetrically around the policy repo rate, which will be at the centre of the corridor.

iii. The fixed rate reverse repo (FRRR) rate is retained at 3.35 per cent. It will remain as part of RBI’s toolkit and its operation will be at the discretion of the RBI for purposes specified from time to time. The FRRR along with the SDF will impart flexibility to the RBI’s liquidity management framework.

iv. Both MSF and SDF will be available on all days of the week, throughout the year.

v. It has also been decided to restore the opening time for financial markets regulated by the RBI to the pre-pandemic timing of 9:00 am with effect from April 18, 2022, without any change in their closing time prevailing at present.

17. During the pandemic, the RBI offered liquidity facilities of the order ₹17.2 lakh crore of which ₹11.9 lakh crore was utilised. So far ₹5.0 lakh crore has been returned or withdrawn on the lapse of various facilities on their due dates. The extraordinary liquidity measures undertaken in the wake of the pandemic, combined with the liquidity injected through various other operations of the RBI have left a liquidity overhang of the order of ₹8.5 lakh crore in the system. The RBI will engage in a gradual and calibrated withdrawal of this liquidity over a multi-year time frame in a non-disruptive manner beginning this year. The objective is to restore the size of the liquidity surplus in the system to a level consistent with the prevailing stance of monetary policy. While doing so, I would like to reiterate our commitment to ensure the availability of adequate liquidity to meet the productive requirements of the economy. We also remain focussed on completion of the borrowing programme of the Government and towards this end the RBI will deploy various instruments as warranted.

External Sector

18. Despite the worsening global supply shocks slowing the recovery in the world economy, India’s merchandise exports grew robustly in 2021-22, overshooting the target of US$ 400 billion. A sharp escalation in international commodity prices in conjunction with domestic demand recovery has also led to a strong rebound in imports and a widening of trade and current account deficits. The sustained and robust growth in services exports and in-bound remittances continue to keep our invisible account balance in large surplus, which helps to offset partly the merchandise trade deficit. Despite the sharp jump in crude oil and other commodity prices, we expect the current account deficit to remain at sustainable levels which can be financed with normal capital flows.

19. Overall, our external sector indicators remain healthy and have improved significantly in recent years. Our foreign exchange reserves stand at US$ 606.5 billion as on April 1, 2022 which are further bolstered by the net forward assets of the RBI. The Reserve Bank remains committed to maintain orderly conditions in the domestic financial markets and will take appropriate steps, as needed, on an ongoing basis to contain the adverse spillovers from the global developments.

Additional Measures

20. I now propose to announce certain additional measures, the details of which are set out in the statement on developmental and regulatory policies (Part-B) of the Monetary Policy Statement. These measures are as follows:

Individual Housing Loans – Rationalisation of Risk Weights

21. The risk weights for individual housing loans were rationalised in October 2020 by linking them only with loan to value (LTV) ratios for all new housing loans sanctioned up to March 31, 2022. Recognising the importance of the housing sector and its multiplier effects, it has been decided to extend the applicability of these guidelines till March 31, 2023.This will facilitate higher credit flow for individual housing loans.

SLR holdings in HTM category

22. With a view to enable banks to better manage their investment portfolio during 2022-23, it has been decided to enhance the present limit under Held to Maturity (HTM) category from 22 percent to 23 per cent of NDTL till March 31, 2023. It has also been decided to allow banks to include eligible SLR securities acquired between April 1, 2022 and March 31, 2023 under this enhanced limit. The HTM limits would be restored from 23 per cent to 19.5 per cent in a phased manner starting from the quarter ending June 30, 2023.

Discussion Paper on Climate Risk and Sustainable Finance

23. Climate change poses certain risks that could have implications for the safety and soundness of financial institutions and as well as financial stability. To facilitate better understanding and assessment of the potential impact of climate-related financial risks by Regulated Entities, a Discussion Paper on Climate Risk and Sustainable Finance will be published shortly for feedback.

Committee for review of Customer Service Standards in RBI Regulated Entities

24. The Reserve Bank has over the years taken a number of measures to enhance consumer protection. These measures include laying down regulatory frameworks on customer service, internal grievance redress and the Ombudsman mechanisms. In view of the transformation underway in the financial landscape due to innovations in products and services, deepening of digital penetration and emergence of various service providers, it is proposed to set up a committee to examine and review the current state of customer service in the RBI Regulated Entities, adequacy of customer service regulations and suggest measure to improve the same.

Interoperable Card-less Cash Withdrawal at ATMs

25. At present, the facility of card-less cash withdrawal through ATMs is limited only to a few banks. It is now proposed to make card-less cash withdrawal facility available across all banks and ATM networks using the UPI. In addition to enhancing ease of transactions, the absence of the need for physical card for such transactions would help prevent frauds such as card skimming, card cloning, etc.

Bharat Bill Payment System – Rationalisation of Net-worth Requirement for Operating Units

26. Bharat Bill Payment System (BBPS), an interoperable platform for bill payments, has seen an increase in the volume of bill payments and billers over the years. To further facilitate greater penetration of bill payments through the BBPS and to encourage participation of a greater number of non-bank Bharat Bill Payment Operating Units in the BBPS, it is proposed to reduce the net worth requirement of such entities from ₹100 crore to ₹25 crore.

Cyber Resilience and Payment Security Controls of Payment System Operators (PSOs)

27. Payment systems play a catalytic role in facilitating financial inclusion and promoting financial stability. To ensure that our payment systems remain resilient to conventional and emerging risks, specifically those relating to cyber security, it is proposed to issue guidelines on Cyber Resilience and Payment Security Controls for Payment System Operators.

Concluding Remarks

28. The last two years have seen turbulence and uncertainty of epic proportions. At the Reserve Bank, we have worked unrestingly to mitigate their impact on our economy. When I look back, I see that we have traversed an arduous path with candour, courage and the conviction that a brighter future lies ahead.

29. The conflict in Europe now poses a new and overwhelming challenge, complicating an already uncertain global outlook. As the daunting headwinds of the geopolitical situation challenge us, the RBI is braced up and prepared to defend the Indian economy with all instruments at its command. As we have demonstrated over the last two years, we are not hostage to any rulebook and no action is off the table when the need of the hour is to safeguard the economy. Our goals of price stability, sustained growth and financial stability are mutually reinforcing and we continue to be guided by this approach.

30. The sky today may be overcast with clouds, but we will use all our energies, resolve and resources to let the sunlight illuminate India’s future. Let me end by recalling what the Father of our nation, Mahatma Gandhi said long ago: “It is faith that steers us through stormy seas, faith that moves mountains and faith that jumps across the ocean.”1

Thank you. Stay safe. Stay well. Namaskar.

(Yogesh Dayal)

Chief General Manager

Press Release: 2022-2023/37

Statement on Developmental and Regulatory Policies

This Statement sets out various developmental and regulatory policy measures relating to (i) liquidity measures; (ii) regulation and supervision; and (iii) payment and settlement systems.

I. Liquidity Measures

1. Introduction of the Standing Deposit Facility

In 2018, the amended Section 17 of the RBI Act empowered the Reserve Bank to introduce the Standing Deposit Facility (SDF) – an additional tool for absorbing liquidity without any collateral. By removing the binding collateral constraint on the RBI, the SDF strengthens the operating framework of monetary policy. The SDF is also a financial stability tool in addition to its role in liquidity management.

Accordingly, it has been decided to institute the SDF with an interest rate of 3.75 per cent with immediate effect. The SDF will replace the fixed rate reverse repo (FRRR) as the floor of the LAF corridor. Both the standing facilities viz., the MSF and the SDF will be available on all days of the week, throughout the year.

The fixed rate reverse repo (FRRR) rate is retained at 3.35 per cent. It will remain as part of the RBI’s toolkit and its operation will be at the discretion of the RBI for purposes specified from time to time. The FRRR along with the SDF will impart flexibility to the RBI’s liquidity management framework.

2. Restoration of the Symmetric LAF Corridor

In 2020 during the pandemic, the width of the LAF corridor was widened to 90 basis points (bps) by asymmetric adjustments in the reverse repo rate vis-à-vis the policy repo rate. With a view to fully restore the pre-pandemic liquidity management framework of February 2020 and in view of the gradual return to normalcy in financial markets, it has now been decided to restore the width of the LAF corridor to its pre-pandemic level. With the introduction of the SDF at 3.75 per cent, the policy repo rate being at 4.00 per cent and the MSF rate at 4.25 per cent, the width of the LAF corridor is restored to its pre-pandemic configuration of 50 bps. Thus, the LAF corridor will be symmetric around the policy repo rate with the MSF rate as the ceiling and the SDF rate as the floor with immediate effect.

II. Regulation and Supervision

3. Individual Housing Loans – Rationalisation of Risk Weights

The Reserve Bank vide circular dated October 12, 2020 had rationalised the risk weights for individual housing loans by linking them only with loan to value (LTV) ratios for all new housing loans sanctioned up to March 31, 2022. Recognising the importance of the housing sector, its multiplier effects and its role in supporting the overall credit growth, it has been decided that the risk weights as prescribed in the circular ibid shall continue for all new housing loans sanctioned up to March 31, 2023.

4. SLR Holdings in HTM category

The Reserve Bank had increased the limits under Held to Maturity (HTM) category from 19.5 per cent to 22 per cent of net demand and time liabilities (NDTL) in respect of statutory liquidity ratio (SLR) eligible securities acquired on or after September 1, 2020, up to March 31, 2022. This dispensation of enhancement in HTM limit was made available up to March 31, 2023. With a view to enable banks to better manage their investment portfolio in FY 2022-23, it has now been decided to enhance the limit for inclusion of SLR eligible securities in the HTM category to 23 per cent of NDTL and allow the banks to include securities acquired between April 1, 2022 and March 31, 2023 under the enhanced limit of 23 per cent. The HTM limits would be restored from 23 per cent to 19.5 per cent in a phased manner starting from the quarter ending June 30, 2023.

5. Discussion Paper on Climate Risk and Sustainable Finance

Climate change may result in physical and transition risks that could have implications for the safety and soundness of individual Regulated Entities (REs) as well as financial stability. Thus, there is a need for REs to develop and implement a sound process for understanding and assessing the potential impact of climate-related financial risks in their business strategy and operations. This would require, among other things, an appropriate governance structure and a strategic framework to effectively manage and address these risks. Further, some regulatory initiatives in the area of climate risk and sustainable finance would also help the REs to better handle climate risk and guide them in the transition period. A Discussion Paper on Climate Risk and Sustainable Finance covering the above aspects will be placed shortly on the RBI’s website for comments of stakeholders.

6. Committee for Review of Customer Service Standards in RBI Regulated Entities

RBI has progressively taken a number of measures, including laying down an elaborate regulatory framework on customer service and internal grievance redress at regulated entities (REs) as also putting in place the Ombudsman framework as far back as 1995, to ensure overarching protection for the customers of its REs. Regulatory instructions are issued to REs based on the conditions prevailing in the financial system, findings of conduct supervision, analysis of complaints received, and recommendations received from various Committees set up for this purpose. The important committees set up by RBI on customer service over the years include (i) Talwar Committee on Customer Service (1975), (ii) Goiporia Committee (1990), (iii) Tarapore Committee on Procedures and Performance Audit on Public Services (CPPAPS, 2004) and (iv) Damodaran Committee on Customer Service (2010).

The financial landscape is undergoing a revolutionary transformation consequent to the rising customer base of the banks, advent of digital products, technology platforms and service providers as also the rising volumes of digital transactions emerging from innovations in payment systems. Accordingly, it is proposed to set up a committee to examine and review the state of customer service in the REs and adequacy of customer service regulations and suggest measure to improve the same.

III. Payment and Settlement Systems

7. Interoperable Card-less Cash Withdrawal (ICCW) at ATMs

Card-less cash withdrawal through ATMs is a permitted mode of transaction offered by a few banks in the country on an on-us basis (for their customers at their own ATMs). The absence of need for a card to initiate cash withdrawal transactions would help in containing frauds like skimming, card cloning, device tampering, etc. To encourage card-less cash withdrawal facility across all banks and all ATM networks / operators, it is proposed to enable customer authorisation through the use of Unified Payments Interface (UPI) while settlement of such transactions would happen through the ATM networks. Separate instructions would be issued to NPCI, ATM networks and banks shortly.

8. Bharat Bill Payment System – Rationalisation of Net-worth Requirement for Operating Units

Bharat Bill Payment System (BBPS) is an interoperable platform for bill payments and the scope and coverage of BBPS extends to all categories of billers who raise recurring bills. Users of BBPS enjoy benefits like standardised bill payment experience, centralised customer grievance redressal mechanism, prescribed customer convenience fee, etc. BBPS has seen an increase in the volume of transactions as well as number of onboarded billers.

It is observed that there has not been a corresponding growth in the number of non-bank Bharat Bill Payment Operating Units (BBPOUs). The current requirement of net worth for a non-bank BBPOU to obtain authorisation is ₹100 crore and it is viewed as a constraint to greater participation. It is, therefore, proposed to align the net worth requirement of non-bank BBPOUs with that of other non–bank participants who handle customer funds (like Payment Aggregators) and have a similar risk profile. Accordingly, the net worth requirement for non-bank BBPOUs is being reduced to ₹25 crore. The necessary amendment to regulations will be carried out shortly.

9. Cyber Resilience and Payment Security Controls of Payment System Operators (PSOs)

Payment systems play a catalytic role in promoting financial stability and facilitating financial inclusion. Maintaining the safety and security of these systems is a key objective of RBI. With greater adoption of digital payment modes, it is important to ensure that payment system infrastructures are not only efficient and effective but also resilient to conventional and emerging risks, specifically those relating to cyber security. RBI has prescribed the necessary security controls for digital payment products and services offered by banks and credit card issuing NBFCs. It is proposed to issue similar directions for Payment System Operators (PSOs), covering robust governance mechanism for identification, assessment, monitoring and management of cybersecurity risks including information security risks and vulnerabilities, and specify baseline security measures for ensuring safe and secure digital payment transactions. The directions will be issued shortly.

(Yogesh Dayal)

Chief General Manager

Press Release: 2022-2023/39

Monetary Policy Statement, 2022-23 Resolution of the Monetary Policy Committee (MPC) April 6-8, 2022

On the basis of an assessment of the current and evolving macroeconomic situation, the Monetary Policy Committee (MPC) at its meeting today (April 8, 2022) decided to:

- keep the policy repo rate under the liquidity adjustment facility (LAF) unchanged at 4.0 per cent.

The marginal standing facility (MSF) rate and the Bank Rate remain unchanged at 4.25 per cent. The standing deposit facility (SDF) rate, which will now be the floor of the LAF corridor, will be at 3.75 per cent.

- The MPC also decided to remain accommodative while focusing on withdrawal of accommodation to ensure that inflation remains within the target going forward, while supporting growth.

These decisions are in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4 per cent within a band of +/- 2 per cent, while supporting growth.

The main considerations underlying the decision are set out in the statement below

Assessment

Global Economy

2. Since the MPC’s meeting in February 2022, the global economic and financial environment has worsened with the escalation of geopolitical conflict and accompanying sanctions. Commodity prices have shot up substantially across the board amidst heightened volatility, with adverse fallouts on net commodity importers. Financial markets have exhibited increased volatility. Crude oil prices jumped to 14-year high in early March; despite some correction, they remain volatile at elevated levels. Supply chain pressures, which were set to ease, are rising again. The broad-based jump in global commodity prices has exacerbated inflationary pressures across advanced economies (AEs) and emerging market economies (EMEs) alike causing a sharp revision in their inflation projections. The global composite purchasing managers’ index (PMI) eased to 52.7 in March from 53.5 in February with output growth slowing in both manufacturing and services sectors. World merchandise trade momentum has weakened.

3. Several central banks, especially systemic ones, continue to be on the path of normalisation and tightening of monetary policy stances. Resultantly, sovereign bond yields in major AEs have been hardening. Bullion prices had buoyed to near 2020 highs on safe haven flows, with some recent correction as bond yields rose. Global equity markets fell, although more recently they have recovered some ground. In recent weeks, strong capital outflows from the EMEs have moderated thus curbing the downward pressures on their currencies, even as the US dollar has strengthened. Overall, the global economy faces major headwinds from several fronts, including continuing uncertainty about the pandemic’s trajectory.

Domestic Economy

4. The second advance estimates (SAE) for 2021-22 released by the National Statistical Office (NSO) on February 28, 2022 placed India’s real gross domestic product (GDP) growth at 8.9 per cent, 1.8 per cent above the pre-pandemic (2019-20) level. On the supply side, real gross value added (GVA) rose by 8.3 per cent in 2021-22, with its major components, including services, exceeding pre-pandemic levels. GDP growth in Q3:2021-22 decelerated to 5.4 per cent.

5. In Q4:2021-22, available high frequency indicators exhibit signs of recovery with the fast ebbing of the third wave but the picture is mixed. Urban demand reflected in domestic air traffic rebounded in March and the pace of contraction in passenger vehicle sales moderated in February. On the other hand, rural demand mirrored in two-wheeler and tractor sales contracted in February. Import of capital goods increased robustly in February, although domestic production continued to contract. Merchandise exports remained buoyant and clocked double-digit growth for the thirteenth successive month in March 2022 and reached US$ 417.8 billion in 2021-22 surpassing the target of US$ 400 billion. All categories of imports, however, have risen even faster, leading to merchandise trade deficit at a record annual level of US $ 192 billion in 2021-22 or 6.1 per cent of GDP.

6. On the supply side, foodgrains production touched a new record in 2021-22, with both kharif and rabi output crossing the final estimates for 2020-21 as well as the targets set for 2021-22. The manufacturing PMI remained in expansion zone in March, although it moderated somewhat to 54.0 from 54.9 in February. Services sector indicators – railway freight; e-way bills; GST collections; toll collections; fuel consumption; and electricity demand – were in expansion in February-March. The services PMI continued in expansion mode, inching up to 53.6 in March from 51.8 in the preceding month.

7. Headline CPI inflation edged up to 6.0 per cent in January 2022 and 6.1 per cent in February, breaching the upper tolerance threshold. Pick-up in food inflation contributed the most in headline inflation, with inflation of cereals, vegetables, spices and protein-based food items like eggs, meat and fish being the key drivers. Fuel inflation moderated on continuing deflation in electricity and steady LPG prices. Core inflation, i.e., CPI inflation excluding food and fuel remained elevated, though there was some moderation from 6.0 per cent in January to 5.8 per cent in February primarily due to the easing of inflation in transport and communication; pan, tobacco and intoxicants; recreation and amusement; and health.

8. Overall system liquidity remained in large surplus, with average daily absorption (through both the fixed and variable rate reverse repos) under the LAF at ₹7.5 lakh crore in March, marginally lower than ₹7.8 lakh crore in January-February 2022. Reserve money (adjusted for the first-round impact of the change in the cash reserve ratio) expanded by 10.9 per cent (y-o-y) on April 1, 2022. Money supply (M3) and bank credit by commercial banks rose (y-o-y) by 8.7 per cent and 9.6 per cent, respectively, as on March 25, 2022. India’s foreign exchange reserves increased by US$ 30.3 billion to US$ 607.3 billion in 2021-22.

Outlook

9. Looking ahead, the inflation trajectory will depend critically upon the evolving geopolitical situation and its impact on global commodity prices and logistics. On food prices, domestic prices of cereals have registered increases in sympathy with international prices, though record foodgrains production and buffer stock levels should prevent a major flare up in domestic prices. Elevated global price pressures in key food items such as edible oils, and in animal and poultry feed due to global supply shortages impart high uncertainty to the food price outlook, warranting continuous monitoring.

10. In this scenario, pro-active supply management is critical to contain inflation. International crude oil prices remain volatile and elevated, with considerable uncertainties surrounding global supplies. With the broad-based surge in prices of key industrial inputs and global supply chain disruptions, input cost push pressures appear likely to persist for longer than expected earlier. Their pass-through to retail prices, though limited till now given the continuing slack in the economy, needs to be monitored carefully. Manufacturing sector firms polled in the Reserve Bank’s industrial outlook survey expect higher input and output price pressures going forward. Taking into account these factors and on the assumption of a normal monsoon in 2022 and average crude oil price (Indian basket) of US$ 100 per barrel, inflation is now projected at 5.7 per cent in 2022-23, with Q1 at 6.3 per cent; Q2 at 5.8 per cent; Q3 at 5.4 per cent; and Q4 at 5.1 per cent (Chart 1).

11. Going forward, good prospects of rabi output augur well for rural demand. With the ebbing of the third wave and expanding vaccination coverage, the pick-up in contact-intensive services and urban demand is expected to be sustained. The government’s thrust on capital expenditure coupled with initiatives such as the production linked incentive (PLI) scheme should bolster private investment activity, amidst improving capacity utilisation, deleveraged corporate balance sheets, higher offtake of bank credit and congenial financial conditions. At the same time, the escalation of the geopolitical situation and the accompanying surge in international crude oil and other commodity prices, tightening of global financial conditions, persistence of supply-side disruptions and significantly weaker external demand pose downside risks to the outlook. The future course of the pandemic and the uncertainties about the pace of monetary policy normalisation in major advanced economies also weigh on the outlook. Taking all these factors into consideration, the real GDP growth for 2022-23 is now projected at 7.2 per cent, with Q1 at 16.2 per cent; Q2 at 6.2 per cent; Q3 at 4.1 per cent; and Q4 at 4.0 per cent, with risks broadly balanced (Chart 2).

12. The MPC is of the view that since the February meeting, the ratcheting up of geopolitical tensions, generalised hardening of global commodity prices, the likelihood of prolonged supply chain disruptions, dislocations in trade and capital flows, divergent monetary policy responses and volatility in global financial markets are imparting sizeable upside risks to the inflation trajectory and downside risks to domestic growth.

13. Given the evolving risks and uncertainties, the MPC has decided to keep the policy repo rate unchanged at 4 per cent. The MPC also decided to remain accommodative while focusing on withdrawal of accommodation to ensure that inflation remains within the target going forward, while supporting growth.

14. All members of the MPC – Dr. Shashanka Bhide, Dr. Ashima Goyal, Prof. Jayanth R. Varma, Dr. Mridul K. Saggar, Dr. Michael Debabrata Patra and Shri Shaktikanta Das – unanimously voted to keep the policy repo rate at 4.0 per cent.

15. All members, namely, Dr. Shashanka Bhide, Dr. Ashima Goyal, Prof. Jayanth R. Varma, Dr. Mridul K. Saggar, Dr. Michael Debabrata Patra and Shri Shaktikanta Das unanimously voted to remain accommodative while focusing on withdrawal of accommodation to ensure that inflation remains within the target going forward, while supporting growth.

16. The minutes of the MPC’s meeting will be published on April 22, 2022.

17. The next meeting of the MPC is scheduled during June 6-8, 2022.

(Yogesh Dayal)

Chief General Manager

Press Release: 2022-2023/38