Earlier, the author believed that we do not need a direct tax code and appropriate amendments to the Income Tax Act, 1961 will do the needful.

But after looking at changes made especially from the Taxation Laws (Amendment) Act, 2019 to the CBDT instruction dated 11-May-2022 on implementation of Supreme Court decision in the case of Ashish Agarwal, the author feels that it will be better if one harmonious and complete code is introduced to replace the Income Tax Act, 1961 and some more legislations.

Also Read: . Why we need a Direct Tax Code – Part – II

The total article is divided into 2 parts whereby:

1) first part deals with individual instances of various reasons of a complex law and the

2) second part deals with overall framework of principles as to why the laws are complex or become complex and probable solution to the same.

A DTC is not a magic box that will solve all problems, but it will definitely reduce the level of complexity to which the Income Tax Law has reached.

Replacement of Income Tax law in United Kingdom

The Income Tax Act 2007 (c 3) is an Act of the Parliament of the United Kingdom. It is the primary Act of Parliament concerning income tax paid by individual earners subject to the law of United Kingdom, and mostly replaced the Income and Corporation Taxes Act 1988.

The main purpose of the Income Tax Act 2007 is to rewrite the income tax legislation that has not so far been rewritten so as to make it clearer and easier to use.

The Act does not generally change the meaning of the law when rewriting it. The minor changes which it does make are within the remit of the Tax Law Rewrite project and the Parliamentary process for the Act. In the main, such minor changes are intended to clarify existing provisions, make them consistent or bring the law into line with established practice.

Rest of the details are given at the end of the article in Note -3

Index

I Purpose of law A Creating faith of people B Revenue collection C Punishing the law brakers D Honoring the honest |

II Manner of drafting

A Need for usage of plain language principles B Desirability of single code for all direct taxes C Need for Flexibility to adopt forth-coming changes D Consolidation of law with proper arrangement E Elimination of regulatory functions – F Elimination / reduction of Litigation G Stability H Avoid Repetition I Use of Tables J Shift some portion from Delegated legislation to main DTC III Implementation A Increasing the tax base B Expanding role of Income Tax Appellate Tribunal (ITAT) C Common data pool for TRC D One nation one data |

How one can bring in the DTC

|

1) Target – To be tabled in the budget session in 2023 i.e. on 1-Feb-2023. 2) Amend the draft of August 2019 and publish it my 31-May-2022 3) The due date for First set of suggestions be 31st July 2022. |

4) The Government will publish second version of DTC on 1st November 2022.

5) The due date for second set of suggestions will be 31st December 2022. 6) The Government will table the revised version on 1st February 2023. |

Background-:

Prime Minister Narendra Modi, during the annual conference of tax officers in September 2017, had observed that the Income-Tax Act, 1961, which was drafted more than 50 years ago and needs to be redrafted. It is relevant to observe that the Goods and services tax Act, 2017 has come into force from 1-July-2017 which has in effect brought same goods / services same tax rate and eligibility for input tax credit across the country.

Task force was formed November 2017 and eventually submitted its report in August 2019. One can say that the task force took around 2 years and conducted more than 80 meetings.

Today we are in May 2022 whereby people are settling down from the impact of Covid-19 pandemic.

The latest draft direct tax code is of August 2019 which is not in public domain and the one in public domain was published in 2013-14.

There is more than one reason as to why we need a Direct tax code.

It is rather a perception of respective members of audience who have different expectations from the Income Tax Law.

Empirical study

There is a need to accumulate the wisdom earned at least from Income Tax Act of 1926 and the one currently in force i.e. of 1964.

You might have heard of various agencies reporting various case laws and development in the Act. Let’s take ITR (Income Tax Reporter) as a reference.

An exercise be conducted which will make analysis of every legislative enactment and / or judicial pronouncement from 1 ITR 1 which is being published since 1933.

It will state the status of respective legislative enactment and / or judicial pronouncement in the context of new DTC

It may be categorized as

1. Issue addressed by section — / rule —

2. Not relevant any more

It is advisable to put other remarks which will enable a student of law to study the same.

The above-mentioned data also be put into public domain for comments and corrective actions be taken based on comments received.

Just like DTC, there is an urgent need for consolidation of various rules and schemes notified to give effect to the purpose and provisions of the Income Tax Act, 1961.

Permanent Body for R&D

Law commission of India which has tag line as “”Reforming the Law for maximising Justice in Society and Promoting Good Governance under the Rule of Law”.

Department of Revenue already a committee as “foreign tax and tax research”. It may be relevant to expand the scope and strengthen them further to achieve objective.

Department of Revenue should have an active body on the lines of Law commission of India which will continuously keep on doing research and development and the same is translated on a pro-active basis into the statute book. This should cover both, direct and indirect taxes

Reasons for having a direct tax code

The reasons are divided into two categories namely

- Elementary Reason

- Advanced Reasons

Elementary Reasons

To remove irrelevant portion and to simplify the relevant portion.

|

Income Tax Act, 1961 |

Income Tax Rules, 1962 |

| Though the first section is No. 1 and the last section is 298, the Income Tax Act, 1961 as amended by the Finance Act, 2021 comprises of around 900 sections.

We have section 80JJAA. Deduction in respect of employment of new workmen. 115BBDA. Tax on certain dividends received from domestic companies. |

Though the first rule is No. 1 and the last rule is 133, the Income Tax Rules as amended by the February 2021 comprises of around 191 sections.

We have rule 18AAAAA – Guidelines for specifying an association or institution for the purposes of notification under section 80G(2)(c ). |

Advanced Reasons

It is about changing the structure of the Act or making innovative changes to make it resilient enough to keep up with time and achieve other purposes. Refer Note 1

What to consolidate

The direct tax code should consist of provisions of;

a) the Estate Duty Act, 1953; inheritance (Abolished)

b) the Expenditure-tax Act, 1987 (Abolished)

c) the Wealth-tax Act, 1957; (abolished)

d) the Income-tax Act, 1961;

e) the Super Profits Tax Act, 1963

f) the Prohibition of Benami Property Transactions Act, 1988;

g) Chapter VII of the Finance (No. 2) Act, 2004; (securities transaction tax)

h) Chapter VII of the Finance Act, 2005 (banking cash transaction tax) – Abolished

i) Chapter VII of the Finance Act, 2013; (commodity transaction tax)

j) the Black Money (Undisclosed foreign Income and Assets) and Imposition of Tax Act, 2015;

k) Chapter VIII of the Finance Act, 2016; or (Equalisation levy)

l) Gift Tax Act, 1958 (abolished in 1998 and brought under Income Tax Act in 2004)

This does not mean that Government should introduce each levy as mentioned above. It means that, Government should inculcate necessary portion of each of the above laws and keep space to levy tax on above basis.

If you observe, the concept of assets, expenditure, income and liabilities are interlinked.

Income is a floating concept whereas asset is a static concept.

Consolidation and codification of Income Tax Rules

The Commission’s function is to research and advise the Government of India on legal reform, and is composed of legal experts, and headed by a retired judge.

It may be called as the Direct Tax rules and Schemes, 2023

You will be surprised to know the list of various rules and regulations notified for giving effect to the Income Tax Act, 1961

| 1) Income-Tax Rules, 1962

2) Black Money (Undisclosed foreign Income and Assets) and Imposition of Tax Rules, 2015 3) Prohibition of Benami Property Transactions Rules, 2016 4) Wealth-Tax Rules, 1957 5) Securities Transaction Tax Rules, 2004 6) Accounting Standards Notified Under Section 145(2) 7) Authority for Advance Rulings (Procedure) Rules, 1996 8) Bank Term Deposit Scheme, 2006 9) Banking Cash Transaction Tax Rules, 2005 10) Capital Gains Accounts Scheme, 1988 11) Centralised Processing of Returns Scheme, 2011 12) Deposit Scheme for Retiring Employees of Public Sector Companies, 1991 13) Deposit Scheme for Retiring Government Employees, 1989 14) Direct Tax Dispute Resolution Scheme Rules, 2016 15) Direct Tax Vivad Se Vishwas Rules, 2020 16) Electronic Filing of Returns of Tax Collected at Source Scheme, 2005 17) Electronic Filing of Returns of Tax Deducted at Source Scheme, 2003 18) Electronic Furnishing of Return of Income Scheme, 2004 19) Electronic Furnishing of Return of Income Scheme, 2007 20) Electronic Hardware Technology Park (EHTP) Scheme 21) Employees Stock Option Plan or Scheme 22) Equalization Levy Rules, 2016 23) Equity Linked Savings Scheme, 2005 24) European Economic Community International Institutional Partners Scheme, 1993 25) Expenditure-Tax Rules, 1987 26) Faceless Appeal Scheme, 2020 27) Faceless Assessment Scheme, 2019 28) Faceless Penalty Scheme, 2021 29) Furnishing of Return of Income On Internet Scheme, 2004 30) Guidelines for Providing Training By Shipping Companies for Tonnage-Tax Scheme Under Chapter XII-G of Income-Tax Act 31) Hospitalisation and Domiciliary Hospitalisation Benefit Policy 32) Income Declaration Scheme Rules, 2016 33) Income-Tax (Appellate Tribunal) Rules, 1963 34) Income-Tax (Certificate Proceedings) Rules, 1962 35) Income-Tax (Dispute Resolution Panel) Rules, 2009 36) Income-Tax Ombudsman Guidelines, 2010 37) Income-Tax Settlement Commission (Procedure) Rules, 1997 38) Income-Tax Welfare Fund Rules, 2007 |

39) Industrial Park Scheme, 2002

40) Industrial Park Scheme, 2008 41) Instructions To Subordinate Authorities – Authorisation Regarding Condonation of Delay In Filing Refund Claim 42) Investment Deposit Account Scheme, 1986 43) Issue of foreign Currency Convertible Bonds and ordinary Shares (Through Depositary Receipt Mechanism) Scheme, 1993 44) Issue of foreign Currency Exchangeable Bonds Scheme, 2008 45) National Pension Scheme Tier II – Tax Saver Scheme, 2020 46) National Savings Certificates (IX-Issue) Rules, 2011 47) National Savings Certificates (VI Issue) Rules, 1981 48) National Savings Certificates (VII Issue) Rules, 1981 49) National Savings Certificates (VIII Issue) Rules, 1989 50) National Savings Certificates (VIII Issue) Scheme, 2019 51) National Savings Scheme Rules, 1987 52) National Savings Scheme Rules, 1992 53) Public Provident Fund Scheme, 1968 54) Public Provident Fund Scheme, 2019 55) Reverse Mortgage Scheme, 2008 56) Scheme for Bulk Filing of Returns By Salaried Employees, 2002 57) Scheme for Filing of Returns By Salaried Employees Through Employer, 2004 58) Scheme for Furnishing of Paper Returns of Tax Collected at Source, 2005 59) Scheme for Furnishing of Paper Returns of Tax Deducted at Source, 2005 60) Scheme To Develop, Operate & Maintain Special Economic Zones Under Section 80-Ia of The Income-Tax Act Read With Rule 18C(2) of Income-Tax Rules 61) Senior Citizens’ Savings Scheme, 2019 62) Site Restoration Fund Scheme, 1999 63) Social Security Certificates Rules, 1982 64) Software Technology Parks Scheme 65) Tax Return Preparer Scheme, 2006 66) Waiver or Reduction of Interest 67) Wealth-Tax Settlement Commission (Procedure) Rules, 1997 68) Faceless Appeal Scheme, 2021 69) E-Verification Scheme, 2021 70) Faceless Inquiry or Valuation Scheme, 2022 71) E-Advance Rulings Scheme, 2022 72) E-Dispute Resolution Scheme, 2022 73) E-Assessment of Income Escaping Assessment Scheme, 2022 74) Faceless Jurisdiction of Income-Tax Authorities Scheme, 2022 75) E-Settlement Scheme, 2021 76) Faceless Appeal Scheme, 2020 77) Faceless Penalty Scheme, 2021 78) E-Assessment Scheme, 2019 79) Startup India Seed Fund Scheme (Sisfs) |

Consolidation and codification of Notifications, Circulars, Instructions, Press release

It may be called as Direct tax (Delegated Law) Code, 2023

Exactly on the above lines, it will have all the notifications, circulars, instructions, press releases

It will be mirror image of the manner of classification of the Direct Tax Code

Artificial intelligence

Today with the use of Informaton and communication technology various private vendors are rendering the service of analysis of the law fulfilling various requirements of the counsels and / or judges.

Refer the article to understand level of Artificial intelligence – https://economictimes.indiatimes.com/prime/technology-and-startups/tracing-the-journey-of-ai-its-turning-points-and-what-the-future-looks-like/primearticleshow/91652271.cms

Impact

Legislature

Drafting or codifying an idea by taking into consideration all possible permutations and combinations that probably may happen or pose situation is a very difficult job.

It will be great if the Dept. of Revenue itself creates and maintains such a database i.e. consolidated Rules, Consolidated notifications, circulars, instructions, press release alongwith heavy indexation

Refer a note on UK Income Tax Act, 2007 at the end of this article where a screen shot is there where time slot wise changes are tracked on official website of Government.

When such a complete, relevant, accurate data is available on a web portal of Government itself, it will give a great sense of completeness, transparency and Government being responsible. It will have significant positive impact on foreign investors as well.

While drafting the Act, it can help the law drafters to take into consideration all the permutations and combinations and use mathematical formula to extrapolate the potential situations.

Consider following example for Equalisation levy

|

Sr. No. |

Customer / buyer | Seller | Banker | E-commerce operators # | Nature of goods purchased or services obtained or both |

| 1 | R | R | R | Does not have facility to render service | Space provided by microsoft – onedrive. |

| 2 | NR within sub-sec (3) | NR | NR | Has facility render service | Architectural |

| 3 | NR outside sub-sec (3) | E-commerce-operator -owning the goods | Owns the goods | Data hosting charges

|

|

| 4 | ISP address in India | E-commerce-operator -NOT owning the goods | Owns the services | Website hosting

|

|

| 5 | ISP address outside India | Has PE in India | Using an application online | ||

| 6 | Does not have PE in India | Amount charged back by foreign company to Indian Company for Above transactions | |||

| 7 | Sale of advertisement or sale of data |

Through mathematical modelling of permutation and combination, a table of all possible permutations can be prepared to bring completeness to the potential cases and it can be ensured that answers to call the cases are there in the law.

Judiciary-:

Just like drafting, judging also is a difficult task. While adjudicating in a particular manner, one must be alive of its ramifications.

A simulation on above lines is equally relevant for judiciary, especially for the higher judiciary.

A typical judicial order is as follows;

|

Particulars |

Question / grounds of appeal | Role of (AI) (AI) Artificial Intelligence | |||||

| 1 | 2 | 3 | 4 | 5 | 6 | ||

| Basics – | Can add high value with completeness, Accuracy and relevance whereby the judicial officer(s) may heavily depend upon it.

Once used consistently across the country, it itself will create an empirical data of adjudication. |

||||||

| Facts – undisputed | |||||||

| Facts – disputed | |||||||

| Governing legal framework | |||||||

| judicial precedence | |||||||

| contention of applicant | |||||||

| contention of respondent | |||||||

| Analysis of Court | Human wisdom be given upper hand | ||||||

| Conclusion of Court | |||||||

The observations under the heading “Artificial intelligence “ are equally applicable to other streams of law as well.

Attributes of DTC

Any tax law essentially has following three attributes. If any of them is missing at any point in time or is ambiguous or vague, the taxing mechanism fails.

|

Attribute |

Description which should be explicitly clear |

| Charging mechanism | It explicitly and in no uncertain terms defines the base on which the charge of the tax is created or levied. for example, Income Tax is a tax on “Total Income” |

| Measurement mechanism | Measurement Mechanism prescribes the mechanism of computing the total quantum of base i.e. total income and thereafter applying the tax rate to compute the tax to be paid |

| Collection mechanism | It prescribes as to how the tax is should be dis-charged. for example, advance tax, self-assessment tax, with-holding tax i.e. TDS, TCS |

It is expected that under DTC, the co-relation between these three compartments should be clear. Refer Note – 4 to read the example.

I Purpose of law

A Creating faith of people

|

1) The main hesitation for payment of taxes is its ultimate utilization which is hampered by two main causes, firstly inefficiency and secondly corruption. 2) If possible, some part of income tax liability should be in the nature of CSR which will include high net-worth assessees’. |

Reality indicates that relation of faith between an assessee and taxman are strangers to each other.

Once such area is charitable / religious organisations. Income Tax Department believes that nobody does the charity…

Charitable work … not so much chairtable

There is a lot of litigation in this area. Though the Finance Act, 2020 has sought to reduce litigation regarding registration, the changes made from the Finance Act, 2020 to the Finance Act, 2022 are cumbersome.

Consider following examples

TATA group trusts – rejecting tax benefits

You may be aware that, various charitable trusts of tata group have chosen to not to have any income tax benefits and have de-registered themselves from Income tax. For further reading, refer Note 5.

Higher Income – charitable benefit highly litigated

Refer the decision in the case of Board of Control for Cricket in India v PCIT-Exemption – 3

Income Tax Dept. dis-allowed the charitable benefit to BCCI. Income Tax Appellate tribunal held as follows;

…

…

29. As for the basic issue raised by the revenue authorities, which has witnessed vehement arguments from both sides, i.e. whether the IPL matches can indeed be said to be commercial in nature in the sense that the entire orientation of these matches is aimed at making money in the garb of promotion of cricket, strictly speaking, it is not necessary for us to go into this aspect of the matter at this stage, as the impugned order is held to be vitiated in law on account of factors discussed hereinabove. We may, however, add that on the face of it merely because a sports tournament is structured in such a manner so as to make it more popular, resulting in more paying sponsorships and greater mobilization of resources, the basic character of the activity of popularizing cricket is not lost. It is indeed possible that the predominant object remains the promotion of cricket but that activity is done in a more effective and financially optimal manner, and that there is no conflict in the cricket becoming more popular and the cricket becoming more entertaining. It results in providing significant economic opportunities to those associated with the holding of the IPL tournament and, in the process, enriching the resources of the assessee trust. As long as the object of promoting cricket remains intact, and that continues to be the predominant object, the assessee cannot be said to be not following the object of promoting cricket, just because the operational model of a cricket tournament, whether IPL or any other tournament, is more entertaining, more economically viable, provides greater economic opportunities to all those associated with that tournament, and mobilizes greater financial resources for popularising cricket. The purpose for which all the funds at the disposal of the assessee trust, including the additional funds generated by holding the IPL tournament, are employed is certainly for promoting cricket, and that is what really matters. Improvising the rules of the game, adding entertainment value to it and making it economically attractive, may be a purist’s nightmare but the same factors can also be viewed as radical and innovative ideas to popularise a game- the very raison d’être of an institution like this assessee, and that is how we view it.

30. In view of the above discussions, as also bearing in mind the entirety of the case, we hold that the assessee was entitled to the continuance of its registration under section 12A dated 12th February, 1996 and that, accordingly, the impugned order passed by the learned Principal Commissioner stands quashed. The assessee gets the relief accordingly.

The phenomena of tata group trusts rejecting income tax benefits, income tax dept. treating any entity with high income being not as charitable is not at all a good picture.

|

B Revenue collection Perhaps the most important purpose from Government’s viewpoint. Unless a particular amount of taxes is collected, the infrastructure created will not be able to function. 90,000 (as referred to in judgement of Supreme court dated 4-May-2022 in the case of Ashish Agrawal) re-assessment notices issued just before they are becoming time-barred shows the eagerness of the Revenue to collect taxes to meet the budget. With ICT, modulations are possible and as the data is available on figure-tips, planned and organized steps can be taken without disturbing genuine taxpayers |

C Punishing the law brakers

Typically, an area more talked about than done anything. It essentially needs a political willingness. Refer comments relating to agricultural income above.

D Honoring the honest

Something needs to be done beyond lip-service or generating electronic certificates.

A scheme may be introduced which is more like an insurance scheme that, in case of an assessee who is otherwise honest, meets with a disaster, income tax paid by him for immediately 6 preceding years will be refunded to him

II Manner of drafting

A Need for usage of plain language principles

1) Any common man should come to understand the exact tax liability just by reading portion relevant for him. One may usefully refer https://vidhilegalpolicy.in/research/manual-on-plain-language-drafting/. Only one point that I would like to high-light is to draft small sentences.

2) Simultaneously, with the draft code, its authentic translation in the languages as per eighth Schedule of Constitution currently having 22 languages be published. The exercise of translation itself will also reveal the gaps in drafting and make it easier to put a nip in the bud.

B Desirability of single code for all direct taxes

3) It will eliminate litigation regarding jurisdiction or authority of parliament to enact tax on a particular aspect of the subject.

4) It will bring predictability and will eliminate over-lapping and avoid multiple taxation by way of over lapping.

E.g. Equalisation levy and income tax

C Need for Flexibility to adopt forth-coming changes

Any law is expected to be future looking. The structure should be flexible enough to adopt different changes in policies and its reflection in the Direct tax code without getting complicated.

In the draft Code 2013, many things blocking the space in the Act which are assessee specific have been transferred to schedule e.g. list of entities eligible for 100% / 50% Donations

D Consolidation of law with proper arrangement

It will automatically trim down the size of the Act because many policies that now have become redundant will not find a place in the DTC like

Chapter XX-C Purchase of property by Central Government in certain cases of transfer,

Series of section 80HH, section 10A and 10B,

In order to enable a better understanding of tax legislation, provisions relating to definitions, incentives, procedure and rates of taxes have been consolidated. Further, the various provisions have also been rearranged to make it consistent with the general scheme of the Act.

There is no harm in having some vacant numbers for each category

E Elimination of regulatory functions –

Traditionally, the taxing statute has also been used as a regulatory tool. However, with regulatory authorities being established in various sectors of the economy, the regulatory function of the taxing statute has been withdrawn. This has significantly contributed to the simplification exercise.

F Stability

At present, the rates of taxes are stipulated in the Finance Act of the relevant year. Therefore, there is a certain degree of uncertainty and instability in the prevailing rates of taxes. Under the Code, all rates of taxes are proposed to be prescribed in the First to the Fourth Schedule to the Code itself thereby obviating the need for an annual Finance Bill. The changes in the rates, if any, will be done through appropriate amendments to the Schedule brought before Parliament in the form of an Amendment Bill.

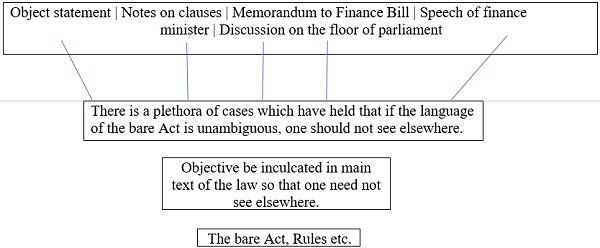

G Elimination / reduction of Litigation

Legislative Enactments

Currently, the objective of a particular set of provisions of law are spread over as follows;

H Avoid Repetition

Refer chapter VI-A. In case of giving benefits, one of the condition that the new entity should be a bonafide one. In general following conditions are prescribed and one can find the same multiple times in chapter VI-A, rather multiple times within the same section like 80-I.

(2) This section applies to any industrial undertaking which fulfils all the following conditions, namely :—

|

(i) |

it is not formed by the splitting up, or the reconstruction, of a business already in existence; |

| (ii) | it is not formed by the transfer to a new business of machinery or plant previously used for any purpose; |

| (iii) | it manufactures or produces any article or thing, not being any article or thing specified in the list in the Eleventh Schedule, or operates one or more cold storage plant or plants, in any part of India, and begins to manufacture or produce articles or things or to operate such plant or plants, at any time within the period of ten years next following the 31st day of March, 1981, or such further period as the Central Government may, by notification in the official Gazette, specify with reference to any particular industrial under-taking; |

| (iv) | in a case where the industrial undertaking manufactures or produces articles or things, the undertaking employs ten or more workers in a manufacturing process carried on with the aid of power, or employs twenty or more workers in a manufacturing process carried on without the aid of power : |

Provided that the condition in clause (i) shall not apply in respect of any industrial undertaking which is formed as a result of the re-establishment, reconstruction or revival by the assessee of the business of any such industrial undertaking as is referred to in section 33B, in the circumstances and within the period specified in that section :

Provided further that the condition in clause (iii) shall, in relation to a small-scale industrial undertaking, apply as if the words “not being any article or thing specified in the list in the Eleventh Schedule” had been omitted.

The above-mentioned portion be carved out and kept only at one place. At all remaining places, only cross-reference be drawn to this text.

I Shift some portion from Delegated legislation to main DTC

The portion related to measurement mechanism of income which is included in delegated legislation i.e. in Rules or regulations or notification etc., be shifted in the main body of DTC. IT is so because the valuation aspects occupy a large spectrum of litigation area.

There are probabilities ad consequences to this proposal. It will make the system less flexible, and it is more of an idealistic viewpoint.

A via-media may be that, in respect of valuation of asset, liabilities, net-worth, income and / or expenditure, the broad principles be inculcated into the main Code and CBDT be empowered to draft rules within the said framework.

Though now there are not many of this type of cases, consider example of section 14A r.w.r. 8D.

Following principles may be included in the text of section 14A itself

1) For dis-allowance of expenditure, it is not necessary that the matching income should have been earned or offered for taxation in that year itself

2) Expenditure means any expenditure and not necessarily directly related with earning of exempt income. It will also include the proportion of overheads.

3) The computation of allocation of expenditure will be in accordance with the cost accounting standards as may be notified by the Institute of Cost (and Works) Accountants of India, a body formed under an Act of Parliament.

4) The quantum of expenditure to be dis-allowed can-not exceed the amount of exempt income for the year.

For another example on this topic, please refer Note 2

III Implementation

The starting point is acceptance and more importantly, reliance on Information and communication technology (ICT).

The system of target be abolished. Alternate system of quarterly review or performance on the basis of vibrant use of information technology be inculcated.

A Increasing the tax base

The agricultural income criteria be introduced and obtaining PAN and maintaining proper books of account followed by audit be made mandatory for those having turnover above say 2 crores.

B Expanding role of Income Tax Appellate Tribunal (ITAT)

ITAT has over a period of time has done fantastic job. It is more than desirable that its responsibilities be increased. With ICT, it will be possible to have even distribution of the work load on PAN-India basis.

ITAT should have a permanent larger bench i.e. Special bench at least one in each of the metro cities ideally consisting of five members whereby the President ITAT will be able to distribute questions involving differing opinions being taken by different benches or a vexed issue which is likely to create different opinions being pronounced by the different benches.

ITAT should be allowed to act as an Authority on advance Ruling AAR and the same be allowed to admit a mixed question of fact and law by the assessee before the transaction is actually undertaken. It will reduce the uncertainty for the investor.

C Common data pool for TRC

Most of the countries including China has agreed for automatic exchange of information. It is desired that OECD / UN creates a database on the lines of utility made available by Income Tax Department for section 206AB AND 206CCA relating to whether the assessee has filed return of income and whether at least the tax as mentioned in the return of income is paid or not.

It will eliminate the requirement for the client to obtain TRC from the foreign vendor, for the Chartered Accountant to rely on certificate that what is produced before him is true copy etc.

In the opinion of the author, declaring tax residency is not a violation of his right to privacy when sufficient checks and balances are implemented and the principle of “need to do and need to know” is followed.

D One Nation One Data

Background-:

Currently, each government agency or respective Ministry or Department drafts its own requirement for collecting data from any business entity.

It has also been recognized that the entities are undertaking more and more transactions through banking or electronic channels rather than in cash or other means i.e. virtual digital assets.

Poser

The only question is, can’t there be one portal where ALL the information, as required by any Government agency is uploaded and consequentially each of the Government agency(ies) / ministry(ies) / department(s) get the data relevant to them?

The Government is free to apply intellectual differentia in drafting requirements of return / statement to be filed having regard to

| 1) Format of statement | 2) nature of business / profession / employment |

| 3) Extent of pre-filled data | 4) types of transactions / events |

| 5) Periodicity | 6) Language(s) employed |

Also refer judgement of ustice K.S. Puttaswamy; v Union of India. It will act as a guiding factor to protect privacy https://www.scobserver.in/cases/puttaswamy-v-union-of-india-fundamental-right-to-privacy-case-background/

Also Watch: Direct Tax Code 2025: Simplified Taxation, Key Updates & Impact on Taxpayers

thank you. I agree. Perhaps with this first reply, the inertia has started in that direction

Very good thoughtful views but a demand should be from all stake holders and industry. Government participators are working there on since long but no results. So there should be unitedly voice from all stake holders and professional bodies not only in the interest of taxpayers but also to Government and professionals.