Decoding the “unsaid” by our Hon’ble FM Nirmala Sitharaman as she presented the Union Budget 2022-23 amid slogans, applauses in the Lok Sabha during her 90-minute budget speech in exultant attention. Instead of a briefcase which has been a custom for years, she read out her speech from a ‘Made in India’ tablet which was in a red cover with the National Emblem embossed on it.

Like last year, this year too our Hon’ble FM did’nt speak much on the Tax proposals, infact they are being muted and left for the analysts and experts to decipher from the budget memorandum. It begs a question whether the common man who always expects some tax relief on the budget day, will get any!!

Further, it looks like we still had to deal with the retroactive effect of tax laws this time it is in relation to already settled positions of the Hon’ble High Court. To simply put, if you can’t win your cases on merits in the Courts, then simply amend the Law!

In the Budget, she made sure the iconic Maharajah returns home as the government allocated an additional 52k crore towards the settlement of outstanding guaranteed liabilities of Air India thus putting an end to the most high-profile disinvestment process of Air India so far. Air India had been making losses since 2007 when it was merged with the state-owned domestic operator Indian Airlines. It remained operational due to taxpayer-funded bailouts.

Further, she proposed that a Digital Rupee would be introduced in the year 2023, and also impose a tax of 30 percent on virtual assets, (without setting off or carry forward, Mind you! ) and thus getting the most sought-after assets in its ambit. Crypto!!

Our Hon’ble FM stated while beginning the direct-taxes part of her Budget speech. “I take this opportunity to thank all the taxpayers of our country who have contributed immensely and strengthened the hands of the government in helping their fellow citizens in this hour of need,” Beyond the token, there isn’t much in the Union Budget 2022-23 for the common man to be thankful for.

There were many new announcements like an introduction to the cryptocurrency, chip-embedded passports, 400 Vande Bharat trains, focus on boosting infrastructure, railways, roads, employment, health, housing, however, tax slabs remained unchanged in terms of relief or increasing the burden on the common man. I have tried to summarise in short in the budget attached herewith.

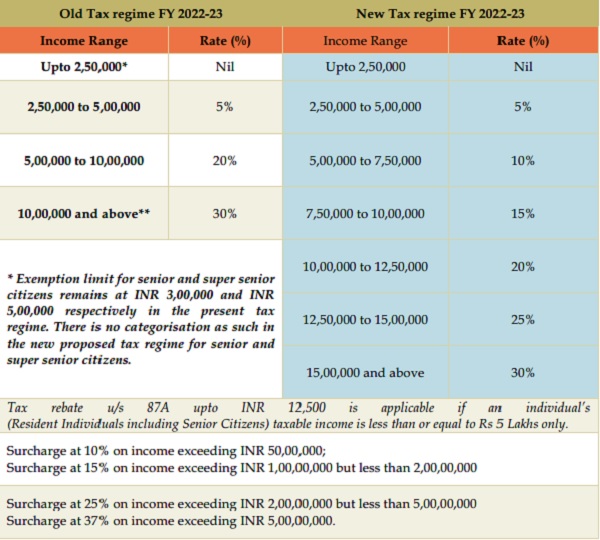

Personal Income Tax

There is no change in the personal income tax rates of the individuals and HUF for Financial Year (‘FY’) 2022-23 in reference to Assessment year (‘AY’) 2023-24

Individuals and HUF have an option same as last year to choose between the Old tax regime and the New Tax regime as introduced in in Budget 2020. The option shall be exercised for every previous year where the individual or the HUF has no business income, and in other cases where there is Business income, the option once exercised for a previous year shall be valid for that previous year and all subsequent years. In nutshell, Business Income taxpayers can only switch between old and new tax regime once in a lifetime.

Amendments proposed in the Direct Taxation Regime

- Surcharge on Long term Capital Gains (‘LTCG’): Surcharge on LTCG on any type of assets transferred are liable to maximum surcharge of 15 per cent irrespective of the higher surcharge being levied on other income excluding LTCG.

- Alternate minimum tax (‘AMT’) on Cooperative Societies: AMT on cooperative societies is reduced to 15% from the present 18.5%. Also the surcharge on cooperative societies is reduced to 7% from the present 12 per cent for those having total income of more than 1 crore and up to 10 crores. This amendment will take effect from 1st April, 2023 and will accordingly apply in relation to the assessment year 2023-24 and subsequent assessment years.

- Introducing new Section 139(8A) ‘Updated return’: In case the assesse has committed omissions or mistakes in correctly estimating their income for tax payment, they can file the updated return within 2 years from the end of the relevant AY. However, the updated return cannot be filed in the following cases:

a. Loss making return

b. Effect of decreasing the tax payable, or increasing the refund amount as filed in the Original/Revised/ Belated Return

c. Search/ Survey/ Seizure or notice u/s 132 or 132A has been issued for seizure of Books of accounts or money/ Jewellery/ Valuable article etc.

d. Updated return once filed cannot be revised.

e. any proceeding for assessment or reassessment or recompilation or revision of income under the Act is pending or has been completed for the relevant assessment year in his case

f. Assessing Officer has information in respect of such person for the relevant assessment year in his possession under the Prevention of Money Laundering Act 2002 or the Black Money Act.

Rates of Additional tax payable while filing updated return:

| Rate of tax | Time period within which the Updated return is filed |

| 25% of the Total tax payable* | 12 months from the end of the relevant Assessment year of filing the original return |

| 50% of the Total tax payable* | 24 months from the end of the relevant Assessment year of filing the original return |

*Total tax payable means tax payable including education cess and Surcharge, (if applicable) and after deduction of all the prepaid taxes.

- Disallowance under section 14A: New Explanation to section 14A has been inserted for disallowance of the expenditure incurred to earn exempt income. Disallowance u/s 14A will be made even if the tax payer in a particular year has not earned any exempt income.

- Conversion of the outstanding interest liability into debentures will not be considered as an actual payment and will not be available for deduction as a business expenditure. This amendment will take effect from 1st April, 2023 and will accordingly apply in relation to the assessment year 2023-24 and subsequent assessment years.

- Computation of interest on delay on payment of TDS: Section 201 is being amended to provide that the interest shall be paid by the person in accordance with the order which is made/ issued by the Assessing Officer for the default under sub-section (1) of 201.

- Section 115BAB – Tax rate @ 15% for new manufacturing domestic companies can be availed if they commence the manufacturing unit or production up till 31st March 2024. (Earlier is was allowed till 31st March 2023)

- Section 80-IAC of the Income tax Act provides for a deduction of an amount equal to 100% of the profits and gains derived from an eligible business by an eligible start-up for three consecutive assessment years out of ten years. The time limits for incorporation for eligible start-up for tax exemption has been increased by one year i.e. up to 31st March 2023.

- Incentives to National Pension System (NPS) subscribers for state government employees: The limit of deduction in respect of contribution made by the State Government to its employees under section 80CCD has been increased from 10% to 14%. This amendment will take effect retrospectively from 1st April, 2020 and will accordingly apply in relation to the assessment year 2020-21 and subsequent assessment years so as to ensure no additional tax liability arises on any contribution made in excess of 10% during such time.

- Tax free annuity to a disabled person: The amount of annuity received by the dependant (who is a senior citizen) before his death shall be tax free. Earlier, the annuity received during the lifetime of a dependant was taxable in the hands of the dependant for whom the policy was taken. This amendment will take effect from 1st April, 2023 and will accordingly apply in relation to the assessment year 2023-24 and subsequent assessment years

- Section 206AB which was inserted last year in the Act providing for higher rate for TDS for the non-filers of income-tax return for last two years is being reduced to one year. Also this section will not apply on Individual and HUF who are covered under section 194IA, 194IB and 194M. TDS rate in this section is higher of the followings rates: –

a. twice the rate specified in the relevant provision of the Act

b. twice the rate or rates in force

c. the rate of five per cent.

This section is applicable to those parties on whom the TDS deduction is greater than fifty thousand in the last preceding year.

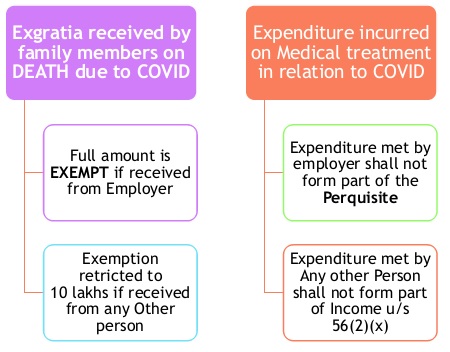

- Exemption of amount received for medical treatment and on account of death due to COVID-19:

- TDS on sale of immovable property: TDS is to be deducted at the rate of 1% of sum paid to the resident or the stamp duty value of such property, whichever is higher.

Consideration paid for the transfer of immovable property and the stamp duty value of such property are both less than fifty lakh rupees, then no tax is to be deducted under section 194-IA.

- New Section of TDS 194R: New section 194R is being introduced to provide that the person responsible for providing to a resident, any benefit or perquisite of a value more than INR 20,000, whether convertible into money or not, arising from carrying out of a business or exercising of a profession, by such resident, shall, deduct TDS @ 10% on such benefit or perquisite. Applicability: the provisions of the said section shall not apply to an individual or a HUF, whose total sales, gross receipts or turnover does not exceed one crore rupees in case of business or fifty lakh rupees in case of profession. This amendment will take effect from 1st July, 2022

- Provisions pertaining to bonus stripping and dividend stripping are made applicable to securities and units. Now the said Bonus/ Dividend stripping will also be applicable to the units of business trusts such as InvIT, REIT and AIF. This amendment will take effect from 1st April, 2023 and will accordingly apply in relation to the assessment year 2023-24.

- Taxation of Digital Assets/ Cryptocurrency (Section 115BBH): Tax shall be paid @ 30% on Transfer of any virtual digital asset. Further, no set off of any loss arising from transfer of virtual digital asset shall be allowed against any income

and no carry forward of loss will be allowed to future AY’s. Section 56(2)(x) also amended to include the taxing of the gifting of virtual digital assets. This amendment will take effect from 1st April, 2023 and will accordingly apply in relation to the assessment year 2023-24 and subsequent assessment years - New Section 194 S: TDS will be deducted at the rate of 10% for payments made on transfer of virtual digital asset. Further, no tax is to be deducted in case the payer is the specified person and the value or the aggregate of such value of consideration to a resident is less than INR 50,000 during the financial year. In any other case, the said limit is proposed to be INR 10,000 during the financial year.

- Withdrawal of concessional rate of taxation on dividend income under section 115BBD: Normal tax rate will be charged to the Indian domestic company, in case of dividends received by such Indian companies from specified foreign companies. This amendment will take effect from 1st April, 2023 and will accordingly apply in relation to the assessment year 2023-24 and subsequent assessment years

- Withdrawal of Exemptions under section 10: The exemption that have been provided under section 10 clause (8), (8A), (8B) and (9) for the remuneration received by the individual from the foreign state for such duties and any other income accruing or arising outside India, in respect of which the individual is required to pay any income or social security tax to the Government of the foreign state, stands withdrawn.

- Amendment in the provisions of section 248 of Income-tax Act and insertion of new section 239A: person who has deducted the TDS of a Non-resident on the transaction on which TDS was not deductible, can now file an application for refund before the Assessing officer. Earlier, an appeal was to be filed with the Commissioner (Appeals).

- Additional Onus of proof for Cash credits under section 68 of the Act: Nature and source of any sum, whether in form of loan or borrowing, or any other liability credited in the books of an assesse shall be treated as explained only if the source of funds is also explained in the hands of the creditor or entry provider. However, this additional onus of proof of explaining the source in the hands of the creditor, would not apply if the creditor is a well regulated entity, i.e., it is a Venture Capital Fund, Venture Capital Company registered with SEBI:

- This amendment will take effect from 1st April, 2023 and will accordingly apply in relation to the assessment year 2023-24 and subsequent assessment years

- Faceless Schemes under the Act: Section 92CA/144C relating to Transfer Pricing functions and international taxation have been brought under the faceless assessment scheme of the Act. Also, the time limit for issue of directions under the aforesaid sections have been extended to 31st March 2024.

- Set off of loss in search cases – Amendment in the provisions of section 79A of the Act: No set off of losses or unabsorbed deprecation shall be made against the undisclosed income unearthed during the search or survey conducted.

- Rationalization of the provisions of sections 149(1)(b): A notice under section 148 shall be issued only for the relevant assessment year after three years but prior to ten years where the Assessing Officer has in his possession books of account or other documents or evidence which reveal that the income chargeable to tax has escaped assessment amounting to or likely to amount to INR 50 lakhs rupees or more.,

- (a) in the form of an asset; or

- (b) expenditure in respect of a transaction or in relation to an event or occasion; or

- (c) an entry or entries in the books of account,

- Amendment in the provisions of section 272A of the Act: Penalty under section 272A for failure to answer questions, sign statements, furnish information, returns or statements, allow inspections has been increased to INR 500 per day from the present INR 100.

- Several IT-based systems have been established for accelerated registration of new companies. Now the Centre for Processing Accelerated Corporate Exit (C-PACE) with process re-engineering, will be established to facilitate and speed up the voluntary winding-up of these companies from the currently required 2 years to less than 6 months.

- Rationalisation of the provision of Charitable Trust and Institutions: New section 271AAE is inserted to provide for penalty on trusts or institution which is equal to amount of income applied by such trust or institution for the benefit of specified person where the violation is noticed for the first time during any previous year and twice the amount of such income where the violation is notice again in any subsequent year. These amendments will take effect from 1st April, 2023 and will accordingly apply in relation to the assessment year 2023-24 and subsequent assessment years

- Principal Commissioner/ Commissioner have been empowered to cancel the registration of the trusts if they are satisfied that one or more specific violation has taken place. Specified violation has been defined by insertion of explanation to sub section 4 of Section 12AB of the act. The term “specified violation” is defined to mean the following:

a. where any income of the trust has been applied other than for the objects for which it is established; or

b. the trust has income from profits and gains of business which is not incidental to the attainment of its objectives or separate books of account are not maintained by it in respect of the business which is incidental to the attainment of its objectives; or

c. the trust has applied any part of its income from the property held under a trust for private religious purposes which does not ensure for the benefit of the public; or

d. the trust established for charitable purpose, after the commencement of this Act, has applied any part of its income for the benefit of any particular religious community or caste; or

e. any activity being carried out by the trust:

(i) is not genuine; or

(ii) is not being carried out in accordance with all or any of the conditions subject to which it was registered;

f. the trust or the institution has not complied with the requirement of any other law, as referred to in item (B) of sub-clause (i) of clause (b) of sub-section (1) of section 12AB, and the order, direction or decree, by whatever name called, holding that such non-compliance has occurred, has either not been disputed or has attained finality.

- Reduction of years for accumulation: The time limit for expenditure after the accumulation of five years under section 11 of the Act and taxation thereof in the sixth year has been reduced to 5 years itself. If the accumulation is not utilised for the purpose for which it is so accumulated or set apart shall be deemed to be the income of the trust of the previous year being the last previous year of the period, for which the income is accumulated or set apart. This amendment will take effect from 1st April, 2023 and will accordingly apply in relation to the assessment year 2023-24 and subsequent assessment years

- Exit tax for Charitable trust being converted to Non charitable trust: Exit tax is to be levied at maximum marginal rate if the Trust is converted into a non-charitable organisation or gets merged with a non-charitable organisation or a charitable organisation with dissimilar objects or does not transfer the assets to another charitable organisation. These amendments will take effect from 1st April, 2023 and will accordingly apply in relation to the assessment year 2023-24 and subsequent assessment years.

- Application of Income for the trusts will only be considered as Application when it is actually paid. Thus, expenses shall be considered as application of income in the previous year in which such sum is actually paid by it irrespective of the previous year in which the liability to pay such sum was incurred by such trust.

- New sub-section (10) in section 13 is being inserted to provide that where the provisions of sub-section (8) are applicable to any trust or institution violates the conditions prescribed under section 12A, its income chargeable to tax shall be computed after allowing deduction for the expenditure (other than capital expenditure) incurred in India, for the objects of the trust subject to fulfilment of the following conditions, namely:-

(i) such expenditure is not from the corpus standing to the credit of such trust as on the last day of the financial year immediately preceding the previous year relevant to the assessment year for which the income is being computed;

(ii) such expenditure is not from any loan or borrowing;

(iii) claim of depreciation is not in respect of an asset, acquisition of which has been claimed as application of income in the same or any other previous year; and

(iv) such expenditure is not in the form of any contribution or donation to any person.

Amendments proposed in the Indirect Taxation Regime

Goods and Services Tax

- Time-limit to avail Input Tax Credit (‘ITC’) u/s 16(4) extended till 30th November of next year from 30th September.

- Section 10 Composition Tax Payer’s Registration can be cancelled suo-moto if they have not filed their GSTR-4 return beyond 3 months from the due date.

- Additional Conditions for availment of Input Tax Credit (‘ITC’) u/s 16(2)- ITC can be availed only if the same is not restricted under Section 38 – as per the details communicated to the purchaser in GSTR-2B.

- Registration of a person, other than those paying tax under section 10, can be cancelled if has not furnished returns for such continuous tax period as may be prescribed.

- Credit Notes in respect of supply made in a financial year can be issued by 30th November of next financial year (currently allowed till 30th September).

- Any rectification of error in GSTR-1/ GSTR-3B is now permitted till 30th November of next financial year (currently allowed till 30th September).

- ITC availment on self-assessment basis:

a. Section 49 of the CGST Act is being amended so as to provide for prescribing restrictions for utilizing the amount available in the electronic credit ledger.

b. It will allow transfer of amount available in electronic cash ledger under the CGST Act of a registered person to the electronic cash ledger under the said Act or the IGST Act of a distinct person.

c. Section 49 of the CGST Act is being amended so as to provide for prescribing the maximum proportion of output tax liability which may be discharged through the electronic credit ledger.

- Explicit refund claim process is being introduced of any balance lying in Electronic Cash ledger under Section 54.

- Time limit of 2 years provided for claiming tax refund on inward supplies of both goods or services u/s 55, from last day of the quarter in which said supply was received.

- GST portal www.gst.gov.in notified Retrospectively as the common portal for all the functions provided under CGST Rules 2017 except for E way bill generation and for generation of invoices under Rule 48(4) of CGST Rules.

- Rate of Interest u/s 50(3) for availing of ITC or wrong availment of ITC is prescribed as 18% in all cases.

Customs/ Other Indirect Tax

Here’s what has become expensive:

- Duty on umbrellas is being raised to 20 per cent. Exemption to parts of umbrellas is being withdrawn.

- Headphones and Earphones.

Here’s what has become cheaper:

- Domestic electronic wearable devices, hearable devices and electronic smart meters.

- Mobile phone parts: Duty concessions are being given to parts of transformer of mobile phone chargers and camera lens of mobile camera module and certain other items.

- Gems and jewelry: Customs duty on cut and polished diamonds and gemstones are being reduced to 5%. Simply sawn diamond would attract nil customs duty to facilitate the export of jewelry through e-commerce.

- Chemicals: Customs duty on certain critical chemicals namely methanol, acetic acid and heavy feed stocks for petroleum refining are being reduced.

- Sweet biscuits

Compiled by: CA Himanshu Taneja, Chartered Accountant | himanshu@aknair.com | ht.taneja@gmail.com

Author Bio

EXCELLENT WEBSITE, ALL INFORMATION IN DETAILS WITH UNDERSTANDING EASY..