Executive summary

The committee on taxation of E-commerce (constituted by the Central Board of Direct Taxes) took heed of the Report on Action Plan 1 of the Base Erosion & Profit Shifting (BEPS) Project, which reveals the need for modifying the existing international taxation rule. G20 countries, including India and OECD members, have accepted and acknowledged this report.

The BEPS report on Action Plan 1 outlines three choices, it is about establishing a new nexus based on significant economic presence (‘SEP’), imposition of a withholding tax on digital transactions (WHT), and the imposition of an Equalisation Levy (‘EQL’). The report provides detailed information on the features of these alternatives and their potential tax structures. However, the report refrains from endorsing any specific option at this point, considering the need for further examination regarding profit attribution. Nonetheless, it acknowledges the sovereignty of any country that wishes to adopt these options, whether through its domestic legislation or in bilateral tax agreements.

Upon reviewing the three options outlined in the reports, the committee analysed the first two alternatives and concluded that the SEP and WHT would necessitate modifications to several tax treaties. In contrast, the third option, the EQL, offers a more straightforward solution that can be implemented through domestic laws without requiring extensive amendments to numerous tax treaties.

Subsequently, the EQL was introduced in June 2016 as a distinct chapter within the Indian Finance Act, 2016(‘Finance Act’) (Section 163 to 180). Furthermore, in 2020, the scope of the EQL was expanded to encompass Section 165A.

The EQL is a tax imposed on specific types of digital transactions conducted by non-resident companies in relation to the Indian operation. Except for the state of Jammu and Kashmir, it is applicable across India.

Equalisation Levy Structure

1. Section-165

A non-resident person shall pay EQL at the rate of Six percent of the consideration for specified service received or receivable by such person-

i. Indian resident carrying on profession or business; or

ii. Non-resident having a permanent establishment (‘PE’) in India.

Applicability of EQL as per section 165: –

i. Where service provider is a Non-Resident.

ii. Service Recipient is an Indian resident who is involved in business or profession

iii. Amount of Consideration exceeding INR 1 Lakhs in a Previous Year (P.Y).

iv. Services used in India for carrying out profession or business.

Key Definition

Specified services mean term “online advertisement” encompass provisions for digital advertising space as well as any other services specifically intended for online advertising purposes. This encompass any other service that has been notified by the Central Government as necessary in relation to online advertising.

2. Section-165A

An EQL shall be charge at the rate of Two percent of the consideration received or receivable by non-resident E-commerce operator (ECO) not having PE in India from e-commerce supply or services (ECS) made or facilitated or provided by it—

(i) to Indian resident person; or

(ii) to a non-resident person in the specified circumstances -:

a) Sale of an advertisement, that targets customers residing in India or customers who access the advertisement through an Indian IP address; and

b) Sale of data, collected from an Indian resident or from someone who uses an Indian IP address.

(iii) to a person who buys such goods or services or both using Indian IP address.

Exclusion

a) Consideration, turnover or gross receipts of the ECO received throughout the year is less than Rs. 2 crores during FY;

b) If an ECO engage in making, or providing or facilitating ECS and has a PE in India and such ECS is in fact related to that PE or;

c) EQL is leviable under section 165 of the Finance Act.

Analysis of certain definitions

i. E-commerce Operator

A person who is non-resident person owns, manages or operates digital or platform or electronic facility for selling online goods or services or both.

[Only non-resident can qualify as an ECO. The term “Non-resident” is not used in this context is not specifically defined under chapter VIII of the finance act. However, the definition under Income Tax Act, 1961(‘Income Tax’) would be applicable]

ii. E-commerce supply or services

a) Online sell of ECO’s own goods; or

b) Online supply of ECO’s own services; or

c) Online selling goods or services or both, facilitated by the ECO; or

d) Combination of the above.

iii. Online sale of goods and Online provision of services

One or more of the following online activities:

a) Agreeing to a sales offer; or

b) Placing of purchase order; or

c) Assent of the purchase order; or

d) Fulfilment of payment; or

e) Supply of goods or services, partly or wholly

iv. Own, operate or manage

Non-resident who owns, operates or manage a digital or electronic platform is considered as an ECO. This provision implies that individuals or entities fulfilling any of these roles can be classified as ECO. In theory, according to section 165(ca), all three non-residents mentioned, who own, operate or manage the platform can qualify as ECO.

According to section 165A, the person who “receives” the consideration is subject to the EQL.

v. Consideration from e-commerce supply or service

In a typical e-commerce transaction, the entire consideration is initially received by the ECO. The operator may be entitled to a small commission based on the agreement between the operator and the vendor of goods or services. The question at hand is determining the amount on which EQL should be charged.

a) Where the operator facilitates sells of vendor’s goods

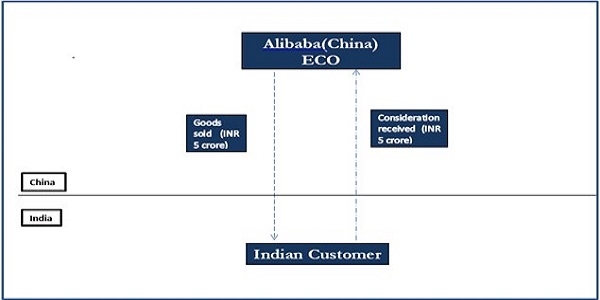

According to Figure 1.1, Alibaba (China) owns and operates a website where vendors can sell their goods. Under an agreement with Levi’s, Alibaba is entitled to a commission of 1% on the consideration for Levi’s (China) goods sold through its website. In an online transaction, Alibaba receive consideration of INR 5 crore from the Indian customers. Alibaba is entitled to retain his commission INR 5 lac from the transaction.

Whether, EQL is to be charged on INR 5 crore or INR 5 lac or INR 4.95 crore? How much consideration has the ECO received from the e-commerce supply it facilitated?

Since, total receipts which are chargeable to EQL exceed INR 2 crore, EQL @ 2% is attracted on the sum of INR 5 crore, which would amount to INR 10 lac.

Figure 1.1

b) Where the operator sells his own goods

According to Figure 1.2, Alibaba owns and operates an online platform through which it sells its own goods or services. The company generates INR 5 crores in revenue from customers. In this scenario, the entire amount of INR 5 crores is considered as Alibaba’s Income. Section 165A explicitly states that 2% levy is to be applied on the complete consideration amount of INR 5 crores.

Since, total receipts which are chargeable to EQL exceed INR 2 crores, EQL @ 2% is attracted on the sum of INR 5 crores, which would amount to INR 10 lac.

Figure 1.2

Interplay between the Section 194-O of the Income Tax Act, 1961 and the Section 165A of the Finance act, 2016

| Particular | 194O | EQL |

| Applicability: | This clause pertains to ECOs who are obligated to withhold tax on the gross amount of sale of goods or services facilitated through their platform at a rate of 1% at the source (TDS). | This tax is applicable to non-resident e-commerce companies providing certain services to Indian customers. The rate of levy is 2% or 6% on the gross amount of payment made to the non-resident company. |

| Threshold limit: | The TDS provisions under 194-O apply if the sum of sale of goods, services, or both of the ECO exceeds INR 50 lakhs. | The levy is applicable if the non-resident company’s total sales, turnover, or gross receipts from digital services provided in India exceed INR 2 crores. |

| Types of transactions covered: | This provision covers the supply of goods or services made through an ECO’s platform. | This tax applies to certain specified digital services like online advertising, digital platform services, and e-commerce transactions provided by non-resident companies. |

| Person responsible for payment | The ECO is responsible for deducting TDS and making the payment to the government. | The Indian customer is responsible for making the payment of EQL to the government. |

| Exemptions: | Certain types of transactions are exempted from the TDS provisions under 194-O, such as goods or services for personal use, charitable organizations, etc. | The levy does not apply to specified digital services provided by residents or non-residents having a PE in India. |

Figure 2.1 (Section 194-O)

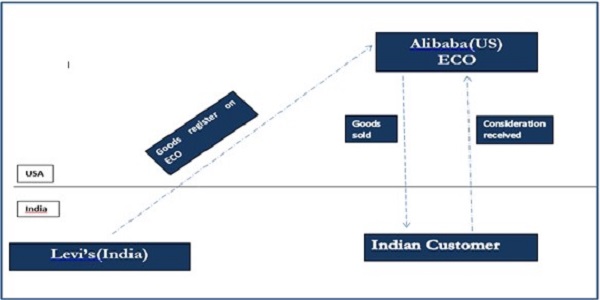

According to Figure 2.1, Alibaba (USA) owns and operates a website where vendors can their goods. Alibaba (ECO) received an amount of INR 6 lac as consideration from the Indian customers (e-commerce participant). After deducting TDS @ 1% on the sum of sales of goods or services facilitated through their platform, Alibaba remits the sum of INR 5,94,000 (TDS INR 6,000) to the Indian customers.

Figure 2.1 highlight that the primary focus of Section 194-O of the Income tax act, 1961 is on two parties: the ECO and the e-commerce participant.

[E-commerce participant will always be resident and ECO can be resident or non-resident]

Figure 1.1& 1.2 highlight that the primary focus of the Section 165A of the finance act is on two parties: the ECO and the buyer.

Levi’s (China) will be considered solely in one scenario to determine the applicability of EQL, which is when goods or services are facilitated by the ECO.

Other points for consideration

i. Is expense deductible?

Section 165A or Chapter VIII of the Finance Act does not provide any deduction for expenses from the consideration and hence levy is to be charged on the gross amount of consideration.

ii. Overlap with Section 10(50)?

Income derived from “specified services” that are chargeable to EQL under Chapter VIII of the Finance Act are exempt from income tax in accordance with section 10(50).

iii. In relation with Section 40(a)(ib)?

Disallowing business expense on account of non-deduction of Section 165 of the Finance Act.

iv. Is the TDS required to be deducted if the amount is collected directly from the e-commerce participants?

Irrespective of the mode of payment to E-commerce participant, it is mandatory for all the ECO to deduct TDS for all the transaction facilitated by them.

Criticisms of EQL

i) Small – medium size businesses will adversely affect by the EQL because the foreign company will not incur a loss and will increase the price of its products by grossing up this tax amount. Ultimately, the burden of the loss is likely to be borne by the Indian Businessperson. This outcome can result in higher cost and diminished competitiveness for them.

ii) EQL has the potential to result in double taxation in certain cases. To illustrate this point, let’s consider an example: if a non-resident company is already paying taxes in its home country, the imposition of the EQL can create a situation of double taxation. This can serve as a disincentive for companies to conduct business in India and may even lead to a reduction in foreign investment.

Conclusion

i) EQL is an important tax measure introduced by the Indian government to tax digital transactions.

ii) It helps to ensure that foreign companies providing digital services in India are taxed appropriately and contributes to the Indian tax base.

iii) While there have been some criticisms, the levy has been largely successful in achieving its objectives.