Salient Features on Deduction us 80M with other ancillary aspects of the Income Tax Act, 1961

Amidst high expectations the Finance Bill, 2020 was presented by Hon’ble Finance Minister before The House of Parliament on 1st February 2020. The Finance Bill, 2020 proposes 104 amendments including Re-Taxation of Dividend Income in the hands of Recipient shareholder instead of taxing it at the distribution point by collecting Corporate Dividend Tax from the Domestic Company distributing it as per erstwhile law. In order to remove the cascading effect of dividend income i.e. avoiding the double taxation section 80M was also proposed to “Re Inserted”.

The opening words of Proposed Section 80M was as under:

Where the gross total income of a domestic company in any previous year includes any income by way of dividends from any other domestic company, there shall, in accordance with and subject to the provisions of this section, be allowed in computing the total income of such domestic company, a deduction of an amount equal to …………………………….

However, in the Finance Act, 2020 the opening words are as under;

Where the gross total income of a domestic company in any previous year includes any income by way of dividends from any other domestic company or a foreign company or a business trust, there shall, in accordance with and subject to the provisions of this section, be allowed in computing the total income of such domestic company, a deduction of an amount equal to …………………………………………………….

As per Section 80M re-inserted by Finance Act, 2020 Dividend received by indian Domestic company from Foreign Companies & Business Trust is also covered which was not a part of the proposed Finance Bill, 2020 as stated above. Except mentioned above all other aspects of section 80M was in line with proposed Finance Bill, 2020.

This article is prepared to highlight the possible reason of difference between proposed provisions & the provision which actually became the part of the Income Tax Act, 1961 vide Finance Act,2020. Read on……

A) Position of Law upto Finance Act, 2019

- As per Section 115O-(1) Any amount Declared/Distributed/Paid by Domestic Company by way of Dividend whether interim/Final Such Dividend shall be chargeable to tax Known as Additional Income Tax (i.e. CDT/DDT) @ 15% grossly or with an effective Rate of 20.56%.

- The Dividend which was subject to Section 115-O were exempted in the hand of Recipient Shareholders u/s 10(34) with an exception that was given u/s 115BBDA.

- The Provision of Section 10(34) were applicable only when the Dividend was subject to Section 115-O. Section 115-O was only applicable in case of dividend paid by domestic company. We can conclude that every dividend received from indian company was exempted in the hands of shareholder (Except Dividend referred to in Section 115BBDA)

- The provision of CDT was not applicable to Foreign Company, Business Trusts etc. Hence such dividend is taxable in the hands of shareholders. If Domestic Company Received dividend from Foreign Company then such dividend shall be taxable @ 30%. (There are some amendments inserted in the chapter of Business Trust vide Finance Act, 2020 which will cover in the later part of the article)

- However as per Section 115BBD, Dividend received from Specified Foreign Company (i.e. Foreign Company in which Domestic Company holds 26% or more of nominal Capital) such dividend shall be taxable in the hands of domestic company @ gross rate of 15%.

- As per Section 115-O(1A) in order to reduce the cascading effect on dividend there shall be allowed a reduction in the amount of dividend on which CDT is required to be paid by such amount of Dividend received from other subsidiary company provided that following condition were satisfied:

* Where such Subsidiary company is Domestic Company, the subsidiary had paid the CDT u/s 115-O which is required to pay under that Section

* Where such Subsidiary company is Foreign Company then recipient indian Holding Company had paid the Tax on Such dividend us 115BBD.

(subsidiary company means a company in which more than half of the nominal value of equity share capital had been acquired by domestic company)

- If an indian company holds nominal value of share capital in Foreign Company equal to or more than 26% but up to 50% then such dividend is taxable in the hands of domestic company us 115BBD @ 15% but such dividend were not taken into account while reducing the amount on which CDT is required to paid as per Section 115-O.

Since as per section 115-O(1A) Dividend received from Foreign Company which is subsidiary of indian company was only covered.

- It might be possible that after allowing the reduction us 115-O(1A), no CDT Liability arises. Still the Dividend Income was exempted in the hands of shareholders us 10(34). Since Section 10(34) Contemplates that Dividend referred to in Section 115-O was exempted in the hands of shareholders. It’s nowhere mentioned that dividend is exempted only to the extent of CDT Paid by domestic company.

- In order to increase the revenue base of Income Tax Department, Section 115BBDA was introduced to target the High Net Worth Resident Individual having in receipt of Dividend referred to in section 115-O.

- As per section 115BBDA Where the total income of a specified assessee resident in India includes income in aggregate exceeding Rs 10 Lacs by way of dividends in a financial year declared/ distributed/ paid by a Domestic Company, then such dividend in excess of Rs 10 Lacs shall be taxable @ 10%.

- Specified assessee means any person other than domestic company, Trust us 12AA/10(23C) or a Fund. Section 115BBDA apply only on Resident assessee it means dividend received by foreign Company including non -resident Individual from Domestic Company were exempted fully.

- Even the dividend is taxable us 115BBDA, Still Domestic company is required to paid CDT us 115-O on the same amount. Hence, there was double taxation.

- Dividend Income earned by/from Business Trust up to Ay 2020-21

i) Dividend received by Business Trust from indian company in which it holds controlling interest which is known as Special Purpose Vehicle were exempted in the hands of Business Trust us 10(23FC) provided that Dividend referred in section 115O-(7).

ii) As per Section 115-O(7) Dividend paid by indian company in which 100% nominal capital is acquired by Business Trust (Except statutory holdings) then such indian company i.e. SPV were not required to pay CDT on Distribution of Dividend to Business Trust if such dividend was paid out of current profits earned after the date of acquisition of 100% holding. Means in such a situation there were no CDT, neither such dividend was taxable in the hands of Business trust by virtue of section 10(23FC).

iii) Even if the case is not covered by section 115O-(7) it means SPV is required to pay CDT then this dividend was exempted in the hands of Business Trust by virtue of Section 10(34) & not us 10(23FC).

iv) Business Trust enjoy passed through status of income. The income passed by it to its unit holders shall be taxable in the hands of its unit holders vide section 115UA. Exception was there in Section 10(23FD)

v) As per Section 10(23FD) dividend received by unitholders of business trust which is in the nature of 10(23FC) read with Section 115O-(7) is exempted in their hands.

vi) Dividend which is in the nature of other than Section 115O-(7) were subjected to CDT & hence such dividend is exempted by virtue of Section 10(34) since tax on such dividend were already collected from SPV @ distribution point.

vii) Dividend which were directly distributed by Business Trust to its unit holder were not being subject to CDT/DDT u/s 115-O & hence such dividend was taxable in the hands of unit holders & exemption by virtue of Section 10(34) were not available to unitholders.

It is important to note that if such dividend were received by specified assessee in excess of Rs 10 Lacs in a financial Year then also Section 115BBDA were not comes into play. Since Section 115BBDA covers dividend which were covered by section 115-O only.

B) Position of Law as per Finance Act, 2020 i.e. From AY 21-22

- Section which became operationally ineffective after the enactment of Finance Act, 2020;

* Section 115-O – Sub-section 1 cast an obligation to Domestic Company to pay CDT while making the payment. There was certain exception to that i.e. Section 115O-(7).

* But the main section it shall became inoperative on any dividend declared/ distributed/paid on or after 1st April 2020 whether interim or final dividend by domestic Company (amended by Finance Act, 2020). It means Section 115O-(7) it automatically became operationally redundant.

* The larger impact is that now every dividend paid/distributed/declared by domestic company be it Special Purposes Vehicles or otherwise will not be subjected to dividend distribution tax.

- Section 10(34) – From Finance Act, 2020 dividend income will be taxable in the hands of shareholders even it receives single rupees as income. Exemption us 10(34) shall not be available from AY 2021-22.

- On the similar note Section 115BBDA will became ineffective since the entire dividend income is taxable. This will largely benefit the high net worth Individual, since they will now not require to Pay tax on dividend exceeding Rs 10 Lacs. Hence double taxation will now avoid.

- Since the Provisions of corporate dividend tax will no longer relevant from assessment year 21-22 hence there is no question arises of any reduction in amount on which CDT was required to pay. It means No CDT, No Reduction. That’s why section 115-O(1A) were also became irrelevant.

- Section 115BBD will be there as it is & Dividend income received from Foreign Subsidiary in which domestic company holds nominal capital not less than 26% shall be taxable grossly @ 15%.

- To avoid the cascading effect i.e. double taxation of dividend Section 80M were re inserted by Finance Act, 2020.

- As per Section 80M domestic company who distributes any income by way of dividend, shall allow a deduction as lower of the following –

* Dividend amount distributed by such domestic company on or before the month prior to due date mentioned us 139(1)

* amount of dividend received from other domestic company or Foreign Company or Business Trust.

- Deduction u/s 115-O(1A) were available only to the domestic company when dividend received by it from subsidiary company be it is domestic or Foreign. This was result in double taxation specifically under those circumstances where holding- subsidiary relation were not exist.

- Further as per erstwhile law deduction was available in case of Foreign subsidiary only when the recipient domestic company paid the taxes us 115BBD.

- However according to section 80M there is no requirement of such. Every Foreign /Domestic Company or Business Trusts are covered.

- Dividend Income earned by/from Business Trust from AY 2021-22

i) Now entire income received as dividend shall be exempted in the hands of Business Trust us 10(23FC) & when such dividend is passed to unit holders then such income shall be taxable in their hands us 115UA on which TDS us 194LBA will be deducted by the trust.

ii) Dividend income earned directly by unitholders shall continue to be taxed in the hands of unitholders as per erstwhile law discussed earlier.

iii) if indian company who is the unit holder of trust received dividend from Business Trust then it will be taxable in the hands of the company. When such dividend is pass to the shareholders of Recipient indian company it will again became taxable in the hands of the shareholder. To avoid double taxation section 80M includes such dividend & allow the deduction to indian company.

iv) Dividend income received by non-resident assessee including Foreign Company shall be taxable @ 20% as per Section 115A

C) The Provisions of Section 80M which was proposed as per Finance Bill, 2020 were exactly same as passed by Finance Act,2020 except discussed in the introduction paragraph of the article.

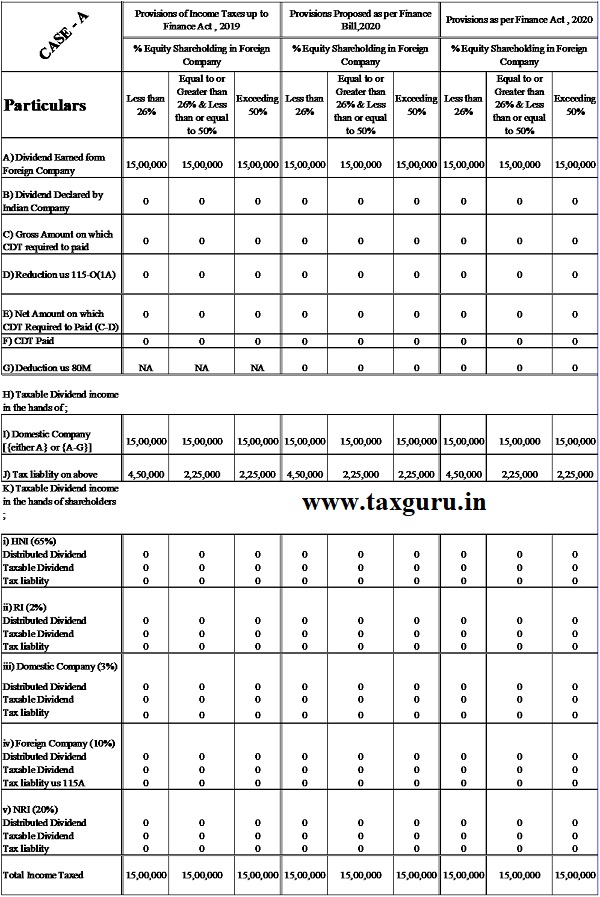

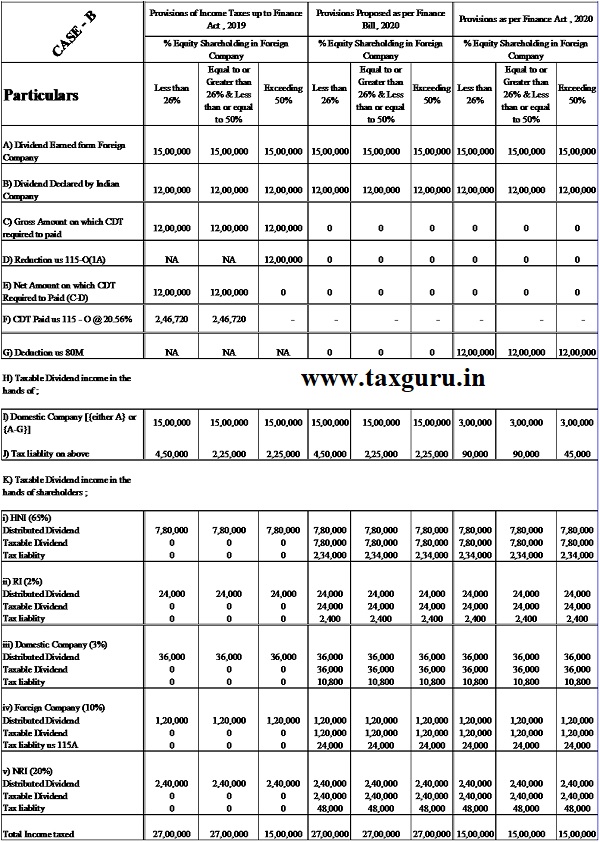

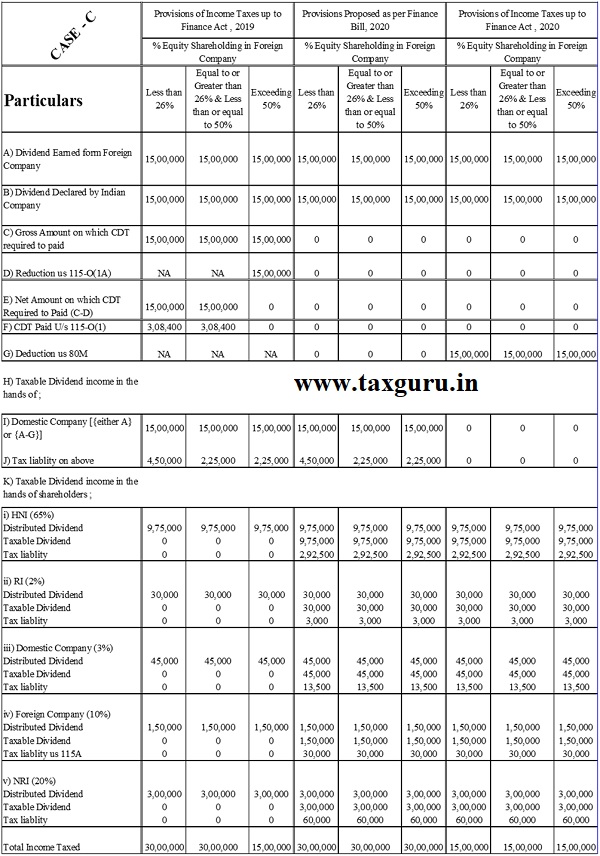

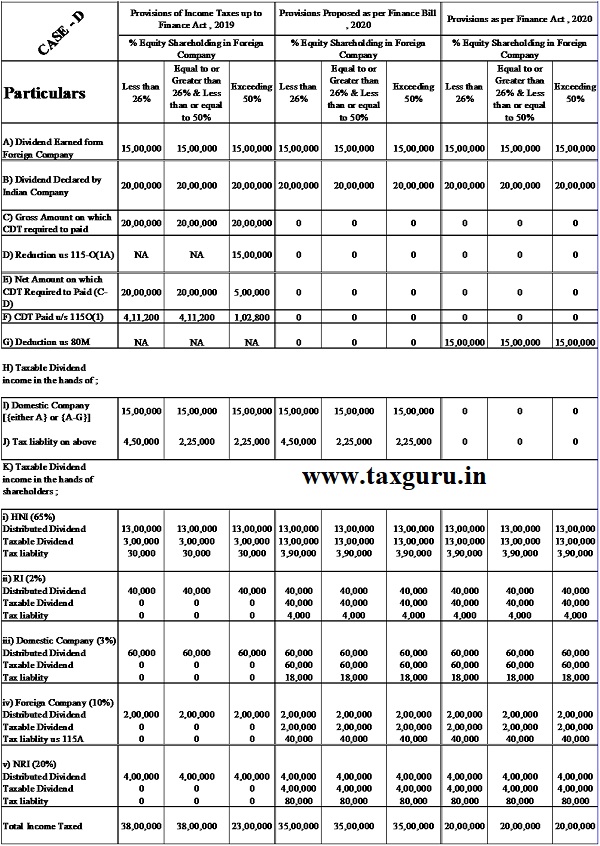

To summarise the above provisions & their impact I am presenting illustrations having 4 various scenario/cases.

In the illustration there is a domestic company whose shareholding is as follows;

- HNI stands for High Net worth Resident Individual – 65%

- Foreign Company – 10%

- Non-Resident Individual – 20%

- Other Indian Company – 3%

- RI stands for (other) Resident Individual – 2%

In each case Dividend received from Foreign company by domestic company is Rs 15,00,000 & Dividend distributed by Domestic Company shall be as follows;

- Case A – Rs Nil

- Case B – Rs 12,00,000/-

- Case C – Rs 15,00,000/-

- Case D – Rs 20,00,000/-

Analysis of the below illustrations:

A) General Points to be note;

i) In Income Tax Act, 1961 the concept of double taxation on a particular source of income is rarely exists. Even if any income is incidentally taxed twice then assessee will allow the tax credit of the same. For example, Tax Credit us 90/91 allowed to the assessee as per DTAA/TIEA.

ii) It is the shareholder who invest their money in the company & Company is only custodian of their money. Hence Dividend income which is earned by the company by investing the funds received from shareholders & which is passed on to the shareholders should be taxable in the hands of shareholders.

iii) However, if after earning dividend income from other corporates & no dividend is passed to the shareholders then entire dividend income shall be taxable in the hands of the company, since income is accrued. In no case dividend income should allowed to be doubly taxed.

iv) Upto AY 2020-21 there was a reduction available u/s 115-O(1A) but it covers dividends which were received from subsidiary company only. Hence there was a scope of double taxation. When these dividend on which CDT was paid reached at the hands of HNI they also required to be paid tax on dividend in excess of Rs 10 Lacs @10% u/s 115BBDA it was also termed as double taxation.

v) To remove all these hardships Finance Act, 2020 takeaway the provisions of CDT First & taxed the entire income of dividend in the hands of shareholders itself & to remove the cascading effect Section 80M was also reinserted in the Act.

B) Common Observation in all cases as per Finance Act, 2020

i) In all the cases the total dividend income taxed is equal.

* If dividend is not distributed it will be taxable in the hands of the company itself (Case A).

* If dividend is distributed to the extent of Rs 12,00,000 i.e. lower than what is received by indian company then Rs 12,00,000 is taxable in the hands of shareholders & balance Rs 3,00,000/- is taxable in the hands of company since it was not distributed. (Case B)

* if Dividend is distributed to the extent of Rs 15,00,000/- then entire Rs 15,00,000/- is taxable in the hands of the shareholders & nothing shall be taxable in the hands of company (Case C)

* if Dividend is distributed to the extent of Rs 20,00,000/- then entire Rs 20,00,000/- is taxable in the hands of the shareholders & nothing shall be taxable in the hands of company (Case D)

C) Special Observation if proposed Finance Bill, 2020 with respect to Section 80M will accepted as it is;

From the table given below in all the scenarios, where the dividend is distributed by an indian company then there is clearly double taxation since 80M deduction was not proposed for Foreign Company.

Initially the dividend received is taxable in the hands of the domestic company & when dividend is passed to the shareholders it will also get taxable in the hands of the shareholders.

This may be the possible reason of difference between provisions of section 80M as proposed by Finance Bill, 2020 as against the Provisions as per Finance Act, 2020. On the similar line Business Trust is also inserted in section 80M Vide Finance Act, 2020. Since neither Deduction us 80M was available nor Reduction us 115-O(1A) was present.

D) Special Observation up to Assessment Year 2020-21

* in all the cases where the reduction us 115-O(1A) was available & Section 115BBDA didn’t attract the net outcome will be same as Finance Act, 2020. It means in those Cases No double taxation was there.

* in all the cases where the reduction us 115-O(1A) was available & Section 115BBDA also attract then Rs 3,00,000/- as per Section 115BBDA were doubly taxed while compare to Finance Act, 2020 (Case D)

* in all the cases where the reduction us 115-O(1A) weren’t available & Section 115BBDA also not attracted then the situation upto Finance Act, 2019 were as it is as per Proposed Finance Bill, 2020 (Case A, B & C)

* in all the cases where the reduction us 115-O(1A) weren’t available & Section 115BBDA also attract then there was double taxation to the extent of Rs 3,00,000/- due to Section 115BBDA while comparing to Proposed Finance Bill, 2020.

Assumptions with respect to Tax Rates of shareholders of Domestic Company

| Class of Shareholder | Applicable rate of Taxes on Divided Income |

| High Net worth Individual | 30% |

| Other Resident Individual | 10% |

| Domestic Company | 30% |

| Foreign Company | 20% u/s 115A |

| Non Resident Individual | 20% U/S 115A |

–

–

–

Concluding Remarks;

After amending the section 80M of the act & includes Dividend earned from Foreign Company & Business Trust in it as against it was proposed by Finance Bill, 2020 following advantages accrue;

- Double taxation will avoid to the greater extent but not completely. Suppose Indian Company A Limited Received dividend during the FY 2020-21 of Rs 25 Lacs from Y Inc a Foreign Company. A Limited Paid the dividend to its shareholders after “Due Date’’ mentioned us 80M say on 31st December 2021. Now A limited will not be eligible for deduction us 80M since the dividend was paid after the “Due Date’’ & it have to pay taxes on entire Rs 25 Lacs whether us 115BBD or normally during AY 2021-22. Now when this dividend reached in the hands of shareholders on 31st December 2021, it will again taxable in their hands in AY 2022-23. Hence in such a manner there will be double Taxation. To avoid it either Such dividend should exempt in the hands of shareholders in AY 2022-23 or Indian Company should allow deduction us 80M while distributing such dividend.

- Dividend income will taxable in the hands of shareholder & company will required to deduct the TDS us 194 on such dividend. Earlier the credit of CDT was not allowed at all. Now this TDS will reflect in Form 26AS which he can utilised against the payment of Its tax Liabilities us 140A or otherwise.

- Non -Resident can claim the benefits of Double Taxation avoidance agreement since now this income is taxable in their hands & they can claim the credit of TDS.

- High net worth individual now shall be dealt in parallel of other shareholders & they are now no more subject to double taxation.

- The Scope of litigation with respect to Expenditure to be disallowed us 14A i.e. expenses made in order to earn the income which is otherwise exempted as per the Income Tax Act, 1961.