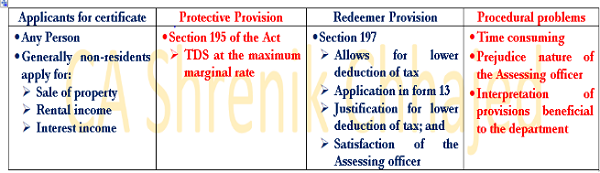

The provisions of the Income-tax Act, 1961 (Act) was written in a very progressive manner by the law makers. While they adopted the best tax practices present globally at the time, they ensured to duly mould them to suit Indian economic scenario. Though many of the provisions of the Act are progressive in nature, there are certain provisions which are protective in nature. One such protective provision is section 195 of the Act.

Section 195 of the Act states that income-tax should be deducted at source on any income earned by a non-resident which is chargeable to income-tax. Needless to say that the provision will be applicable on the payment or credit whichever is earlier and income tax shall be deducted at the rates in force (i.e. at maximum rate of tax). Also if such income is credited to any ‘Suspense Account’, such credit shall be deemed to be income of the non-resident and the provision of section 195 will accordingly apply. As said above, the provision of the Act were written in a progressive manner which allows the non-residents to take away the rightfully earned money without any tax deduction provided that they make an application to the Assessing Officer u/s 197 of the Act in the prescribed form (i.e. Form 13).

The application of tax deduction at lower rate shall be applied to the Assessing officer who, if satisfied, that the deduction of tax should be given at lower rate or Nil rate shall grant a certificate for deduction of tax at such lower rate to the applicant.

The certificate for deduction of tax at lower rate is normally required by Indian citizens (who are non-residents for Income-tax purpose) staying abroad and selling off their residential properties located in India. As per the provision of the Act the said property becomes a capital asset and therefore the necessary taxes for short term capital asset (i.e. income-tax is chargeable as per slab rates) and long term capital asset (income-tax is charged at the rate of 20%) plus applicable surcharge and education cess needs to be deducted from the sale proceeds. The tax burden is too high as it does not take the cost of acquisition and the period of holding of such property. In such a scenario the lower deduction certificate comes as redeemer for the non-residents as it allows them to take the sales proceeds at a lower deduction of tax (i.e. after taking into consideration the cost of acquisition and the period of holding such property).

The procedure for obtaining the certificate is not a straightforward one as convincing the Assessing officer is not an easy task. The Assessing officer is prejudiced towards deducting tax at a higher rate. The provisions are interpreted which are beneficial to the Income-tax department i.e. not accepting the claim of the non-resident. No appeal can be filed before the Commissioner of Income-tax (Appeals) against order u/s 197 as held by the Bombay High Court in the case of CIT v. Garware Nylons Ltd. (1995) 212 ITR 242 (Bom.). In other words, the order given by the Assessing Officer is a final one and not appealable. It is hardly seen that such certificate are given at NIL rate of income-tax.

CBDT notification dated 27.10.2018 has introduced the online filing of application for lower deduction of tax (i.e. form 13) and let’s hope obtaining the certificate becomes seamless and time bound with such introduction.

receive a LDC by a party of income tax rule period on 01/07/2015 to 31.03.2016. Now i receive a bill and dated 10.04.2015 , how deduct tds lower or normal ?