The Central Board of Direct Taxes (CBDT) has issued the final rules pertaining to Master File (MF) and Country by Country reporting (CbCR) on 31st October 2017. This is an outcome of the OECD/G20 BEPS Action Plan 13. India has been an active participant of the OECD BEPS (Base Erosion and Profit Shifting) project. The Finance Act, 2016 introduced Section 286 in the Income-tax Act, 1961 (the Act) providing for furnishing of Country by Country Report (CbCR) in respect of an International Group (IG). Further, Section 92D of the Act has also been amended to provide for filing of the Master File.

In the present article I have discussed these provisions in detail. The modus operandi of the article is to brief you about the basic provisions and the queries which I encountered during my practical exposure.

MASTER FILE Related Forms in India[1]

The MF should provide an overview of the MNE business, and the nature of its global operations, overall TP policies, allocation of income and economic activity. MF is not intended to provide exhaustive details. It will basically contain the group structure, description of the business, intangibles, intercompany financial activity between members of the group, and MNE financial and tax positions.

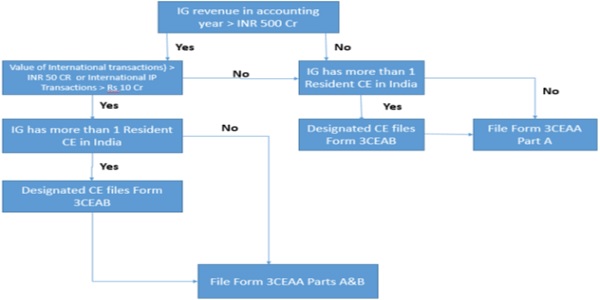

A. Provisions: Form 3CEAA applicability in India–

- Part A to be filled by Every constituent entity*

(*Constituent Entity of the International Group in India means any entity of the International Group in India whose accounts is included in Consolidated Financial Statement.)

- Part B is applicable to the Group entities where:

1. Revenue threshold: Consolidated Group revenue > than INR 500 Crores; and

2. Transaction threshold:

a. International transactions> INR 50 Crores OR

b. Intangibles related transactions > INR 10 Crores

♦ Due Date – On or before the due date for furnishing the return of income as specified under sub-section (1) of section 139.

Actual Due Date for FY 2020-21: On or before 15.03.2022

Detailed description with regard to the Due date for Filling Form 3CEAA

Section 92D of the Income-tax Act, 1961 requires a constituent entity of an international group to keep and maintain the information and document in respect of an international group. The same is prescribed in Rule 10DA of the Income Tax Rules, 1962.

- Rule 10DA (1) prescribes which constituent entity is required to maintain what information and documents of the international group.

- Rule 10DA(2) requires furnishing of the information in Form 3CEAA to the Joint Commissioner on or before the due date for furnishing the return of income as specified under sub-section (1) of section 139.

- Rule 10DA(4) provides that, if more than one constituent entities resident in India of an international group required to file the information and document under Rule 10DA(2), the Form 3CEAA may be furnished by anyone constituent entity under the following circumstances:

- The international group has designated such entity for this purpose

- The information has been conveyed in Form No. 3CEAB to the Joint Commissioner on this behalf thirty days before the due date of furnishing Form No. 3CEAA.

♦ How to recognize whether Accounting Year should be written or Calendar Year in Form 3CEAA?

As per Section 92D Maintenance and furnishing of information and document by certain person under section 92D.]

10DA.

As per sub-section (2) of section 92D of the Income-tax Act, 1961 in compliance with Rule 10DA, the information and document in Form No. 3CEAA – Master File shall be furnished on or before the due date for furnishing the return of income as specified under section 139(1).

The due date of furnishing of Return of Income for the Assessment Year 2021-22, which is 30th November, 2021 under sub-section (1) of section 139 of the Act, as extended to 31st December, 2021 vide Circular No.9/2021 dated 20.05.2021, is hereby further extended to 28th February, 2022;

the terms ‘accounting year’ shall have the same meaning as assigned in sub-section (9) of section 286.

(9) For the purposes of this section, —

(a) “accounting year” means, —

(i) a previous year, in a case where the parent entity or alternate reporting entity is resident in India; or

(ii) an annual accounting period, with respect to which the parent entity of the international group prepares its financial statements under any law for the time being in force or the applicable accounting standards of the country or territory of which such entity is resident, in any other case;

Therefore, the due date for furnishing Master File, is 15 March, 2022.

Example: The Return of Income filed by Hero Holding GMBH is for the Accounting Year Jan 2020 to Dec 2020 and accordingly the Master File would be filed for the accounting year Jan 2020 to Dec 2020 in accordance with section 286(9) (aii).

Form 3CEAB is the Intimation by HTIPL of Hero Group that it will file the Master File on behalf of other Indian Constituent entities. Therefore, the accounting year of master file will be the accounting year for Form 3CEAB i.e. Jan 2020 to Dec 2020.

|

Section |

Penalty | Quantum of penalty |

| 271AA(2) | Penalty for failure to keep and maintain Master File | INR 500,000 |

B. Provisions: Form 3CEAB applicability in India–

|

Out of all the Constituent Indian Entities in India, International Group shall designate one Indian Entity that will file form 3CEAA and such designation will be given in Form 3CEAB. |

Where there are more than one constitute entities resident in India of an international group then in such a case, this form shall decide that which entity shall file form 3CEAA.

Due Date – The intimation shall be made at least 30 Days before the due date of filling the report 3CEAA.

Actual Due Date for FY 2020-21: On or Before 15.02.2022

Flow Chart illustrating Master File filing requirements.

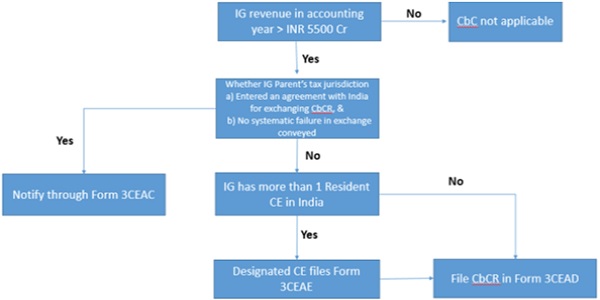

CBCR related Forms in India[2]

CBCR related Forms in India[2]

Rule 10DB provides the guidance for the information to be furnished as part of CbCR, threshold and the procedure of furnishing the information. The CbCR reporting requirements apply to an IG for an accounting year, if total consolidated group revenue, as per its consolidated financial statements for the preceding accounting year exceeds INR 5,500 Cr (Approx. Eur 720 million), it is marginally lower than the threshold as per OECD guidelines of Eur 750 million.

A. Provisions: Form 3CEAD applicability in India–

Form 3CEAD has been prescribed for reporting CbCr information and needs to be filed on or before the date of filing of the return of income.

|

Section |

Penalty | Quantum of penalty |

| 271GB | For failure to furnish CBCR u/s286(2) | a. INR 5,000 per day up to one month; or

b. INR 15,000 per day beyond one month Failure continues after penalty order INR 50,000 per day |

B. Provisions: Form 3CEAE applicability in India–

Form 3CEAE: In case the IG has presence through more than one CEs resident in India, the group may designate one of the CE to furnish CbC report in India and notify DGIT (Risk Assessment) in Form 3CEAE.

C. Provisions: Form 3CEAC applicability in India– (This form needs to be filed in case of more than 2 constituent entities in India)

|

Every Indian constituent entity of a group headquartered outside India is required to file the CbC report notification in this form. Form 3CEAC is to be filed by all the Constituent Indian Entities of International Group whose Parent Entity is not resident in India. Thus this form is to be filled by all the Indian Entities whose books of accounts are consolidated into Consolidated FS of International Group. |

Intimation by a constituent entity, resident in India, of an international group, the parent entity of which is not resident in India.

Due Date – The intimation shall be made at least 2 Months prior to the due date of filling of CIT return under section 139(1). This is required to be filed at least two months prior to the due date for filing the CbC report.

Actual Due Date for FY 2020-21: On or Before 15.01.2022

Flowchart illustrating CbCR filing requirements

The rules provide a great level of clarity on the information expected by the authorities and the

process of furnishing MF and CbCR information where needed. The information requirement being largely in line with OECD guidelines, however certain additional information that has been requested may present challenges. The thresholds either for MF or CbCR are also comparable to other jurisdictions though marginally lower, and not set very low so as to cause inconvenience to the assesses, which is another positive step for a fair administration. It will only help if CBDT doesn’t add further information requirements over a period of time or reduce thresholds so as to make reporting more cumbersome and overwhelm organisations with additional compliance burden.

[1] https://www.incometaxindia.gov.in/forms/income-tax%20rules/103520000000055972.pdf and https://www.incometaxindia.gov.in/forms/income-tax%20rules/103520000000055973.pdf

[2] https://www.incometaxindia.gov.in/forms/income-tax%20rules/103520000000055975.pdf and https://www.incometaxindia.gov.in/forms/income-tax%20rules/103520000000055976.pdf

****

Author: Jyoti Jaiswal | Qualification: Pursuing Chartered Accountancy | Mail Address: jyotijaiswal223@gmail.com

Author Bio

Well done. Very helpful, Good Luck, Keep continue……..

Thank you so much!!