Introduction:

Filing Income Tax Returns (ITRs) is a crucial responsibility for taxpayers to fulfill their obligations and contribute to the nation’s growth. Once taxpayers have completed the process of filing their ITRs, their interaction with the Income Tax Authority does not end there. Instead, this marks the beginning of a series of important steps taken by the Income Tax Authority to verify and assess the accuracy and compliance of the filed returns.

An “Intimation under Section 143(1)” refers to a communication issued by the Income Tax Department in India after processing a taxpayer’s income tax return. This intimation outlines the computation of the taxpayer’s total income, deductions claimed, taxes payable, and the refund (if any) due. It also highlights any discrepancies between the return filed by the taxpayer and the department’s records, along with any interest or penalties levied. The taxpayer is encouraged to carefully review the intimation and respond if there are disagreements or corrections needed. It is a crucial step in the income tax filing process, ensuring accuracy and transparency in tax assessments.

In this article, we will delve into the steps taken by the Income Tax Authority after the filing of ITRs to ensure a fair and transparent tax system.

- Acknowledgment and Initial Processing: Upon receiving the ITR, the Income Tax Authority acknowledges the receipt through an acknowledgment form known as the ITR-V (Income Tax Return-Verification). In case the taxpayer has filed the ITR electronically using a digital signature, the process is considered complete. However, if the return is filed without a digital signature, the taxpayer must submit the ITR-V to the Centralized Processing Center (CPC) within 120 days from the date of e-filing.

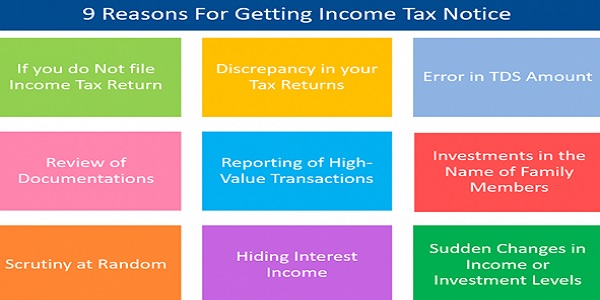

- Data Validation and Matching: The Income Tax Authority crosschecks the data provided in the ITR with the information available in its database. This process includes verifying details such as income, deductions, TDS (Tax Deducted at Source) credits, and other financial transactions against the taxpayer’s PAN (Permanent Account Number) and Form 26AS. Any discrepancies or mismatches may trigger a notice seeking clarification or additional documentation from the taxpayer.

- Scrutiny and Assessment: Based on the data validation and matching, the Income Tax Authority may select certain ITRs for scrutiny or assessment. These cases undergo a more comprehensive review to ensure the accuracy and authenticity of the information provided by the taxpayer. The taxpayer may be required to provide supporting documents and attend hearings, if necessary, during this process.

- Issuance of Notices: If the Income Tax Authority identifies discrepancies or inconsistencies in the filed ITR, they may issue notices to the taxpayer seeking explanations or rectification of errors. These notices can be sent under various sections of the Income Tax Act, such as Section 139(9) for defective returns, Section 143(1) for preliminary assessment, or Section 148 for reassessment.

- Refunds and Demand Adjustments: If the Income Tax Authority determines that a taxpayer is eligible for a refund, the refund amount is processed and issued to the taxpayer. On the other hand, if there are outstanding tax dues, penalties, or interest applicable, the Income Tax Authority may adjust the refund amount against these dues.

- Penal Action for Non-Compliance: In cases of deliberate tax evasion or non-compliance, the Income Tax Authority has the power to take penal action. This may include levying penalties and charging interest on unpaid taxes. In severe cases of tax evasion, prosecution proceedings may be initiated against the taxpayer.

- Dispute Resolution: If a taxpayer disagrees with the assessment made by the Income Tax Authority, they can raise an appeal with the appropriate appellate authorities. The taxpayer can present their case and provide additional evidence to support their claim during the appeal process.

One of the essential steps taken by the Income Tax Authority after the filing of Income Tax Returns (ITRs) is data validation and matching. This process involves cross-verifying the information provided by the taxpayer in the ITR with the data available in the Income Tax Department’s database.

During data validation, the Income Tax Authority ensures that the key details mentioned in the ITR, such as income from various sources, deductions claimed, and tax payments made, align with the records available to the department. They also verify the taxpayer’s PAN (Permanent Account Number) against their personal and financial details to confirm the authenticity of the return.

Additionally, the Income Tax Authority matches the details provided by the taxpayer in the ITR with the information available in Form 26AS. Form 26AS is a consolidated statement that reflects all the tax-related information available with the Income Tax Department, including TDS (Tax Deducted at Source) credits, advance tax payments and self-assessment tax payments. Any discrepancies or differences between the data in the ITR and Form 26AS may raise a red flag for further scrutiny.

The objective of data validation and matching is to ensure the accuracy and integrity of the tax return filed by the taxpayer. It helps the Income Tax Authority to identify any discrepancies, underreporting of income, or incorrect claims of deductions and take necessary actions to rectify them.

If any discrepancies or mismatches are found during this process, the Income Tax Authority may issue a notice to the taxpayer, seeking clarification or supporting documents to resolve the inconsistencies. It is essential for taxpayers to respond to such notices promptly and with accurate information to avoid any potential penalties or further scrutiny.

Overall, data validation and matching play a crucial role in maintaining the transparency and fairness of the tax system, while also encouraging taxpayers to comply with tax laws and fulfill their obligations to the nation.

Conclusion:

Filing Income Tax Returns is an essential part of every taxpayer’s responsibility toward the nation’s development. The steps taken by the Income Tax Authority after the filing of ITRs are crucial to ensuring the accuracy, transparency, and fairness of the tax system. By conducting data validation, scrutiny, and assessment, the authority aims to identify any discrepancies and encourage taxpayers to comply with the tax laws effectively. Timely cooperation and compliance with the Income Tax Authority can make the entire process smoother for taxpayers and contribute to a more efficient tax administration system.

******

About the Author

The author is Ruchika Bhagat, FCA helping foreign companies in setting up and closing businesses in India and complying with various tax laws applicable to foreign companies while establishing a business in India. Neeraj Bhagat & Co. Chartered Accountants is a well-established Chartered Accountancy firm founded in the year 1997 with its head office in New Delhi.