A person is required to pay income tax on the income earned in any financial year. However, what happens, if the person incurs a loss? Notably, the Income Tax Act, 1961 contain specific provisions to address this situation. These provisions allow for the set off of losses incurred in any assessment year. Losses can first be set-off against income earned in the same financial year in which loss is incurred. Any remaining loss, after set off, can be carried forward and set off against the income earned in the subsequent assessment year.

The loss can first be set-off against the income from another source under the same head in the year in which it is incurred. Any remaining loss, after this set-off, can be set-off against income from other heads of the same year.

Losses remaining after inter source and inter head set off can be carried forward for set-off against the income earned in the subsequent financial years. The person does not have the option to forgo set-off of losses or to choose whether to utilize the set-off in the financial year.

Only losses determined in pursuance of a furnished loss return are eligible to be carried forward. To ensure eligibility, loss returns must be filed on or before the prescribed due date. Any delay in filing the loss return will render the loss permanently ineligible for carry forward and set-off.

However, losses incurred in a specified business under section 35AD can be carried forward and set-off against the income of the specified business, even if the loss return is not filed on or before prescribed due date as per section 73A, read with section 80 and section 139(3) of the Income Tax Act, 1961.

Losses are eligible for set off in the year in which it is incurred, even if the return of loss is not filed on or before the prescribed due date.

Speculative business refers to transactions in which contracts for sale or purchase of commodities, shares, or scrips are ultimately and periodically settled otherwise than by actual delivery, with certain exception. Intraday transactions are speculative business. Loss incurred in such transactions are classified as speculative business loss. An Intraday trader can carry forward and set off such losses in the forthcoming years against profit from intraday trade in those years. It would be advantageous for traders to file their income tax return on or before due date.

A company shall be deemed to be carrying on speculative business for the purpose of carry forward and set-off of losses when it derives its income primarily under the head Profits and Gains of business or profession (PGBP), and any part of its business consist of sale or purchase of shares.

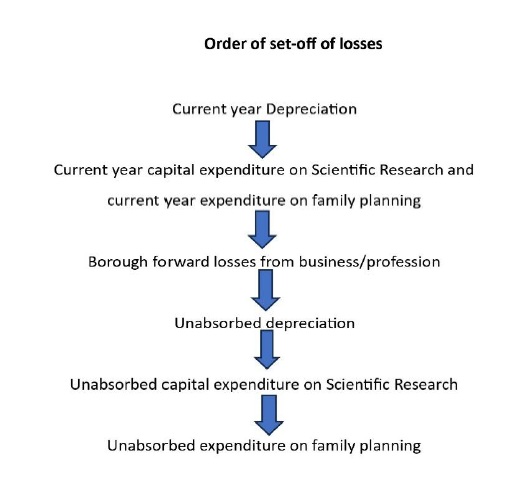

Depreciation and business losses will be separately identified, as the unabsorbed depreciation can be carried forward and set-off for indefinite period of time, whereas business losses can be carried forward for a maximum eight assessment years.

Order of Set -Off of Losses:

Inter-source set off: Income under each head is computed by grouping together the net result of the activities of all the sources covered by that particular head.

(i) Loss under the head Income from house property: Loss from house property can be set-off from income from another house property.

(ii) Loss under the Profits & Gains of Business or Profession (PGBP): Loss from one source under the head PGBP can be set-off against profit from any other source under this head. However, loss from speculation business, loss from specified business u/s 35AD and loss from the activity of owning and maintain race horses cannot be set of against profits and gains from any other source under the head PGBP. It can be interpreted that the loss from other business can be set-off from the profit, if any, from speculation business, specified business u/s 35AD, and the activity of owning and maintain race horses.

(iii) Loss under the head capital gain: Losses under this head are classified into short-term-capital-loss and long-term-capital-loss. Short-Term-Capital-Loss is eligible to be set-off from both Short-Term-Capital-Gain and Long-Term-Capital-Gain. Long-Term-Capital-Loss cannot be set-off against Short-Term-Capital-Gain.

(iv) Loss under the head Income from other sources: Loss from one source under this head can be set-off from income from other source under the same head.

Inter-head set-off: The net result for an Assessment year, after grouping together result of all activities under a particular head, can be a loss. This loss can be set off against income from another head during the same assessment year in which losses is incurred, subject to certain exceptions.

(i) Loss under the head house property: There is a cap of ₹2 lakh on the set-off of losses from this head against income from other heads. However, if a person opts for the new tax regime, losses under the head “Income from House Property” are not eligible for set-off against income from other heads.

(ii) Loss under the head PGBP: Losses under the PGBP can be set off against income from other heads, except for income under the head “Salary.”

(iii) Speculation business loss: Losses from speculative business cannot be set off against income under any other heads of income.

(iv) Losses from specified business u/s 35AD: Specified business losses cannot be set off against income from other heads. However, such losses can be set off against profits of another specified business. Losses from other business, on the other hand, can be set off against profits from a specified business.

(v) Loss under the head Capital Gains: Loss under this head cannot be set off against income under any other heads. However, losses from other heads of income can be set-off against income under the head ‘capital Gains’.

(vi) Loss from the activity of owning and maintain race horses: It is not eligible for set-off against the income from other heads.

Carry forward and set-off

There can be loss, after giving effect of inter head adjustments, under a particular head of income in a given assessment year. This loss can be carried forward for set off in subsequent assessment years. The primary condition for carrying forward of such a loss is that it must be determined in pursuance of return of loss filed under section 139(3). However, the loss, after set-off as mentioned above, under the head income from house property can be eligible for carry-forward even if the return of loss is not filed under section 139(3).

(i) Loss from house property – Carry forward dealt as given below;

(a) Old Tax regime – A net loss under the head ‘Income from house property’ can be carried forward and can be set-off against the income under the same head. This loss can be carried forward for a maximum eight forthcoming Assessment years from the end of the Assessment year in which loss is incurred.

(b) New Tax Regime – Where the person opts to pay tax at concessional rate, the loss under the head ‘Income from House Property’ is not eligible for carry forward.

(ii) PGBP’S Loss: When there is net loss under the head PGBP after inter head set off in an assessment year, such a Loss can be carried forward and set-off against the profit of any business carried on by the person who has originally incurred the loss, and not necessarily from the profit of the business in which loss was initially incurred. Such loss can be carried forward for a maximum of eight assessment years from the end of the assessment years in which the loss was initially incurred.

(iii) Loss of specified business u/s 35AD: The loss incurred in the specified business can be carried forward for succeeding assessment year until the such loss is set-off only against the profit of the specified business. It can be carried forward indefinitely for set-off against profit of specified business.

(iv) Loss in Speculative business- Loss can be carried forward and set-off against the profit of speculative business. Such loss can be carried forward for a maximum period of four assessment years from the end of the assessment years in which loss was incurred.

(v) Losses under the head Capital gains- Loss under this head is carried forward and set-off as follow;

(a) Short-Term-Capital-Loss: It can be carried forward and set-off against the gain from Short-Term or Long-term arising in the following year.

(b) Long-Term-Capital-Loss: This loss can be carried forward and set-off against the gain from Long-Term arising in the following year.

Loss under this head can be carried forward for maximum eight assessment years.

(vi) Losses from the activity of owning and maintain race horses: Such losses can be carried forward and set-off against the income from this activity alone. They can be carried forward for a maximum four assessment years from the end of relevant assessment year.

Other aspects are covered

Loss of Partnership Firm: In the event of a change in the constitution of a firm on account of retirement or death, the proportionate share of the loss of the retired or deceased partner that remains unabsorbed shall not be allowed to be carried forward by the firm.

Loss of a closely held company: Where a change in the shareholding of a closely held company has occurred in a financial year, no loss incurred in any year prior to the year of change shall be carried forward and set-off against the income of the subsequent year. However, this will only apply if, on the last day of both the financial year of change and the financial year in which the loss was incurred, the share of the such company carrying at least 50% of the voting power are not beneficially held by the same person. This restriction will not apply where change in the shareholding occurred by reason of death of the shareholder, resolution plan approved under the Insolvency and Bankruptcy Code, 2016, demerger or amalgamation of an Indian subsidiary of a foreign company or other specified changes in shareholding.

*****

Disclaimer: The information provided in this article is for general informational purposes only and should not be regarded as professional advice. No actions should be taken solely based on the content of this article. For advice tailored to your specific circumstances, it is strongly recommended to consult a qualified professional.

Author Bio

Can you please confirm if the AY 18-19 business loss admitted in tribunal in AY 26-27, can we set off 8 years from ay 26-27?