Introduction: Insight, the robust platform for tax investigation, unveils its functionality for verifying high-risk refund cases. As per Directive No. 78 from the Directorate of Income Tax, the investigation wing now has a comprehensive tool at its disposal to scrutinize suspicious refund claims effectively.

Detailed Analysis:

1. Identification of High-Risk Clusters:

- Clusters of high-risk refund cases are identified based on specific rules, primarily targeting instances of wrong refunds due to various fraudulent means like false TDS claims, income under-reporting, and inflated deductions.

2. Allocation and Investigation Process:

- Upon receiving the clusters, designated officers allocate cases to investigation officers for comprehensive scrutiny.

- A standard operating procedure (SOP) outlines the steps to be followed during verification, ensuring thorough examination before uploading the verification report.

3. Sample Selection and Investigation Techniques:

- The methodology for determining the sample size within a cluster is detailed, emphasizing a systematic approach based on the size of the cluster.

- Investigation officers are guided on various aspects, including identifying the key persons behind common email IDs, gathering relevant information, and conducting inquiries to verify claims.

4. Feedback and Reporting:

- Officers are instructed on providing timely feedback on the verification process, ensuring transparent communication and efficient resolution of cases.

- The submission of verification reports, including details of genuine and non-genuine claims, is a crucial step towards closing the investigations.

Conclusion: Insight’s functionality for verifying high-risk refund cases equips investigation wing users with a structured approach to tackle fraudulent refund claims effectively. By adhering to the guidelines outlined in Directive No. 78, officers can conduct thorough investigations, identify fraudulent practices, and ensure compliance with tax regulations. With a focus on transparency and efficiency, Insight empowers tax authorities in safeguarding revenue and maintaining the integrity of the taxation system.

*****

Insight Instruction No. 78

DIRECTORATE OF INCOME TAX (SYSTEMS)

ARA Centre, Ground Floor, E-2, Jhandewalan Extension,

New Delhi-110055

F. No. DGIT(S)-ADG(S)-2/HRR/2023-241 Dated:02.04.2024

To,

All DGsIT (Inv.)

Sir / Madam,

Sub.:- Functionality for Verification of High Risk Refund Cases for Investigation wing users at Insight – reg.

Kindly refer to the above.

2. Email based clusters of High-Risk Refund ITRs, identified based upon certain rules have been disseminated to the PDITs (Investigation) for the purpose of verification.

3. Upon receiving the cluster, the concerned CRU Nodal Officer may preferably allocate one or more cluster to a particular DDIT(Inv.)/ADIT(Inv.) for comprehensive investigation.

4. In this regard, SOP for verification of High-Risk Refund (HRR) cases by Investigation wing officers is attached as Annexure-A. All the aspects mentioned in the SOP have to be examined in detail before uploading verification report. Further, kindly refer to Annexure-B for Step-by-Step guidance on case view, verification and feedback on Insight portal.

5. In case of any technical difficulty being observed, users may contact OR write to Insight help desk. (Helpdesk number- 1800-103-4216, Email id: helpdesk@insight.gov.in).

Yours faithfully,

(Abhishek Kumar)

ADG(Systems)-2, New Delhi.

Copy to:

1. PPS to the Chairman, Member (S&FS), Member (TPS), Member(L), Member (A&J), Member (Adm.) & Member (IT & Rev.), CBDT and DGIT(Systems), New Delhi for information.

2. Nodal officer of ITBA, Insight i-Library, httos://irsofficersonline.00v.in

ADG(ems)-2, New Delhi.

Annexure A

414/36/2023-IT (Inv. I)

Government of Indi

Ministry of Finance

Department of Revenue

Central Board of Direct Taxes

*****

Room no. 269, North Block,

New Delhi Dated: 13th March, 2024

OFFICE MEMORANDUM

Subject: – Detailed Guidelines for Directorate of Investigation for verification of High-Risk Refund (HRR) e-mail level clusters — regarding

Several instances have been reported wherein wrong refunds had been claimed through various means such as wrong claim of TDS credit, under reporting of income. over stating of deductions, claim of bogus expenses etc. Accordingly, some cases have been identified based upon certain rules.

2. Suspicious clusters, comprising of ITRs in which common email ID has been reported, have been identified based on certain rules. Details of such high-risk clusters are being disseminated to the respective CRU [Central Registry Unit] Nodal officers for the purpose of verification of suspicion that false claims of refunds have been made in an organised manner or through a single key person. Such cases should be dealt with as per the procedure prescribed below.

3. Guidelines for handling high risk refund cases disseminated by Pr. DGIT / DGIT (Systems) [e-mail-level Cluster] —

A. Upon receiving the cluster. the CRU Nodal officer concerned, with the prior approval of DGIT(Inv.)/PDIT(Inv.) as the case may be, may preferably allocate one or more cluster to a particular DDIT(Inv.)/ADIT(Inv.) [hereinafter referred to as the 10] for comprehensive investigation within a period of 7 days from receipt of information. The IO shall complete the investigation within a period of 3 months from the date on which the case is allocated by CRU Nodal Officers to the 10.

B. Such case will be pushed to the JO in the Verification Module of the Insight Portal with a new case type- “High Risk Refund Cases-Inv.-2. The 10 shall proceed for open enquiry only after administrative approval of the JDIT(Inv.)/Addl. DIT(Inv.).

C. BASIS FOR DETERMINATION OF SAMPLE — The Sample while investigating the HRR cases would be top 10% of the refund claimants in the cluster or Top 10 refund claimants of the cluster, whichever is higher. For clusters containing less than 10 ITRs, all the ITRs present in the cluster are to be treated as Sample. The FIRST SAMPLE will contain the first top 10% of the refund claimants in the cluster or Top 10 refund claimants of the cluster, the SECOND SAMPLE will contain the next 10% of the refund claimants in the cluster or next top 10 refund claimants of the cluster. The same is illustrated with a few examples. Example 1 — If the cluster size is 85, then the FIRST SAMPLE will contain top 10 refund claimants as 10% of 85 is 8.5 which is less than 10, and the SECOND SAMPLE will contain next top 10 refund claimants. Example 2 — If the cluster size is 125, FIRST SAMPLE will contain Top 13 refund claimants and the SECOND SAMPLE will contain next 13 top refund claimants. Example 3 — If the cluster size is 9, the FIRST SAMPLE will contain all 9 refund claimants.

D. While investigating, the I0 will take care of following aspects:

I. (i) The I0 concerned, who has been assigned the case, should first attempt to ascertain the identity of the natural person (hereinafter referred to as the KEY PERSON] associated with the common e-mail ID identified, by making use of internal database available with the Department like Insight / ITBA / e-filing portals etc. If such KEY PERSON could not be identified from the internal database, the I0 may call for information under section 131 (1A) of the Act or by issuance of letter, requesting the FIRST SAMPLE (preferably within their jurisdiction) to furnish: –

(a)the details and identity of the KEY PERSON whose e-mail id has been furnished in their respective ITRs (including contact details and address of the person), and

(b)Submit supporting documents to substantiate the genuineness of claim made on account of exemption, deduction, expenses etc.

(ii) The information called for under section 131(1A) of the Act or through letter issued should mandatorily be delivered through registered post along with service of the same on all the registered e-mail ids (these details should initially be called for without requiring personal appearance of the taxpayers in office.).

(iii) If from the FIRST SAMPLE no compliance is observed and no reply is received, their personal attendance may be ensured, and identity of the KEY PERSON associated with the common e-mail ID may be identified along with proofs to substantiate claim on account of expenses, exemptions, deductions etc. However, if from the reply received from the FIRST SAMPLE, the KEY PERSON can be identified, personal attendance of FIRST SAMPLE is not to be ensured at this stage.

(iv) If JO cannot identify the KEY PERSON associated with the common email ID, then SECOND SAMPLE may be asked to provide the relevant details in the same manner as for the FIRST SAMPLE.

(v) However, if still I0 is not able to ascertain the identity of the KEY PERSON associated with the common e-mail ID, the FIRST SAMPLE along with as many other ITRs from the cluster as deemed fit, may be examined in detail and requisite enquiries may be made & if required, statements of taxpayers may be recorded, to verify either the genuineness of claims made in the ITR or to strengthen the enquiry in terms of corroborative evidences for the false claim.

II. Once the KEY PERSON behind common e-mail Id is identified, the JO, under section 131 (1A) of the Act, may call for information / the documents from the KEY PERSON in support of the claim made on account of deduction, exemption, expenses etc. in the 20-30% of the Cluster size which shall include FIRST SAMPLE. (These details should initially be called for without requiring personal appearance of the KEY PERSON in the office)

III. If, as a result of the enquiry made with the KEY PERSON behind common e-mail Id, the claim of expenses, deductions, exemptions etc, in the enquiry undertaken as per 3.D.II is found to be genuine, then the 10 may close the enquiries and submit the feedback in the feedback functionality present in “High Risk Refund Cases- Inv” case type with the prior approval of PDIT(Inv.).

IV. However, if after verification carried out as per 3.D.II, it is found that the claims made on account of expenses, deductions, exemptions etc. are not genuine or that the KEY PERSON has failed to furnish sufficient evidence to support the claim of refund, the I0 may record the statement of KEY PERSON. The 10 should verify the veracity of the suspicion that false claims of refunds have been made in an organized manner or through a KEY PERSON. Also, the FIRST SAMPLE along with as many other ITRs from the cluster as deemed fit, may be examined in detail and requisite enquiries may be made & if required, statements of taxpayers may be recorded, to verify either the genuineness of claims made in the ITR or to strengthen the enquiry in terms of corroborative evidences for the false claim. Intrusive actions may be planned to unearth any systematic fraudulent claims depending upon the facts and circumstances of such enquiry.

Accordingly, the methodology adopted by the KEY PERSON while filing ITRs may be ascertained. It may include inquiring about the details of documents obtained by him from his clients before filing the ITRs. Moreover, if any patterns in claim of deductions like bulk of the clients claiming similar deductions are observed, the same may be confronted with the KEY PERSON and the circumstances under which such individuals came in contact with him / her should be recorded clearly in the statement. Care must be taken not to disclose the source of intelligence in possession of the Investigation Directorate.

VI. If the investigation reveals that the KEY PERSON has NOT indulged in fraudulent practices and the claims of expenses, deductions, expenses made in the ITR are genuine, No negative inference may be drawn against the KEY PERSON and the ITRs of the Cluster and the IO may close the enquiries and submit the feedback in the feedback functionality present in “High Risk Refund Cases- Inv” case type with the prior approval of PDIT(Inv.).

- However, if it is revealed that the KEY PERSON has indulged in fraudulent practices, the investigation reports as prepared by the IO, in the case of KEY PERSON and tax payers examined in 3.D.IV, be submitted in the feedback functionality present in “High Risk Refund Cases- Inv– case type with the prior approval of PDIT(Inv.) with the comments verification completed. For the remaining ITRs of the cluster, i.e., the ITRs/Assessees of the Cluster which have not been examined in 3.D.IV, based on findings of the enquiry and such other observations which might have material effect on the claim of deduction, exemption, expenses etc., the enquiry report is to be submitted with the comments `Further Verification Required’ quantifying the expenses, deduction, exemption claimed based on which the case was flagged in the Cluster.

For Example — In a Cluster of 85 ITRs, 19 ITRs have been examined in 3.D.IV and 66 have not been examined. Out of the 19 ITRs examined, it is revealed that 9 assessees have all the documents to substantiate the claim and 10 assessees do not have such documents. The enquiry report may be prepared as under: –

a) GENUINE CLAIM & NO ADVERSE VIEW: -for the 9 assessees, report shall mention NIL Income escapement in these cases and no adverse inference maybe drawn.

b) NON-GENUINE CLAIM & INCOME ESCAPEMENT QUANTIFIED: For the 10 assessees, where the assessee could not substantiate the claim, report shall mention the quantum of Income escapement based on the risk rules as quantified by the 10.

c) Unexamined ITRs & further verification required: – For the remaining 66 ITRs of the cluster where no enquiry has been conducted but based on enquiry undertaken of the KEY PERSON and such other observations which might have material effect on the claims made, the 10 will submit the report quantifying the expenses, deductions, exemption, etc. claimed based on the risk rules on which the case was flagged in the Cluster with the comments ‘Further Verification Required’.

E. The JO must submit timely feedback within an overall period of 4 months from the date on which the case had been disseminated to the concerned CRU Nodal Officer in Insight Portal after thorough investigation.

F. During the enquiry, 10 might come across cases where unsubstantiated claims of deductions. expenses, exemptions, etc. have been made in the previous years as well, i.e., for the year for which data has not been flagged in the Cluster. In such instances, 10 shall upload the findings on the VRU for each PAN year-wise separately.

5. These guidelines shall be circulated to bring in the knowledge of the field formations of Investigation Directorate for the investigation of High-Risk Refund (HRR) e-mail level clusters.

6. This issues with the approval of Chairman, CBDT.

Enclosed: – Flow Chart of the process

Vedant Kanwar

Under Secretary (Inv. I),

CBDT Usinvl -cbdt@nic.in/Dcit-invl@gov.in

To,

All DGsIT(Inv.)

B Annexure B- Step by Step Guide

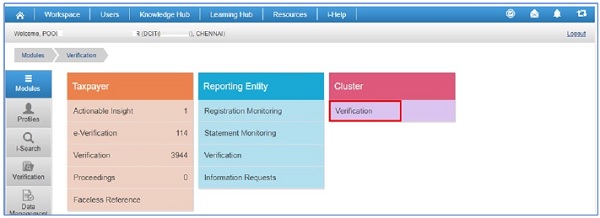

Navigation to Group Verification

1. After successfully login to Insight, user needs to navigate to Verification and Select “Verification” displayed under Cluster Tab to navigate to High-Risk Refund- Investigation Cases.

Figure 1Navigation to Cluster Verification cases

Navigate to High Risk Refund cases- Inv

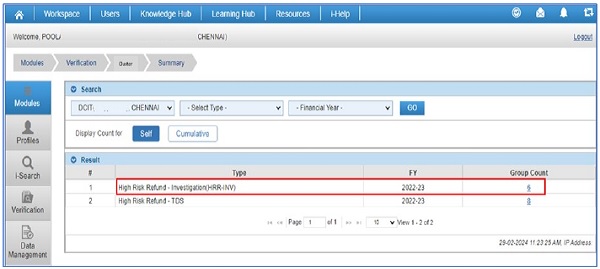

2. User will be navigated to Cluster Case summary view to select High Risk Refund Cases- Inv.

User needs to click on Groupcount as displayed below to navigate to Group Case List View.

Figure 2Navigation to High-Risk Refund Investigation Cases

Navigate to Group Case List View

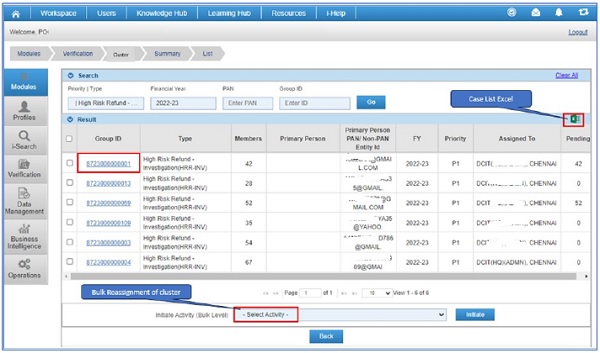

3. In Group Case List view, user will be able to view Group cases created on Mail ID of single key person.

4. User will be able to download Group Case List excel having additional details like count of PANs in group cases, PAN Case ID and PANs in group cases.

5. User will be able to reassign group in bulk from this view.

6. By clicking “Group ID” hyperlink user will be navigated to Group Case Detail View.

Figure 3Navigation to Group Cases List

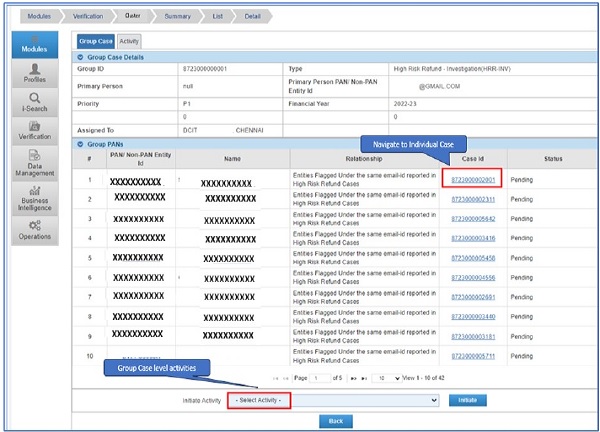

Group Case Detail View and Group Case level activities.

7. At Group Case Detail View, user will be able to view Details of PANs available in group i.e. PANs Name, PAN, and Case id of Individual PAN.

a. User will be able to click on Case ID Hyperlink to navigate to Case Detail view of single PAN.

8. Following Group Case level activities will be available to the user at Group Case Detail Page (Refer Figure 4 Below).

a. Reassign Case

b. Submit Verification Report Bulk

c. Enter Comments

d. View Upload Case attachments.

Figure 4Group Cases Detail View

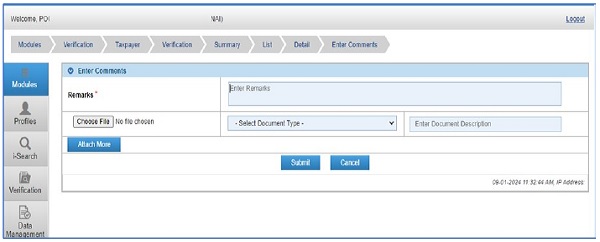

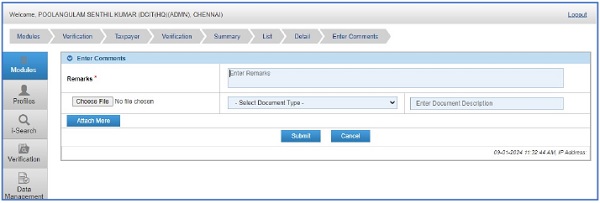

Enter Comments

9. The following screen will be visible to user on clicking activity “Enter Comments”. User will be able to update comments in the Remarks section which will be visible to the user and all supervisor in hierarchy (In cumulative View). User will be able to add documents relevant to the case by clicking “choose file”, providing “document type” and entering “document description”. User can also add multiple documents by clicking “attach more”.

Figure 5Activity Enter Comments

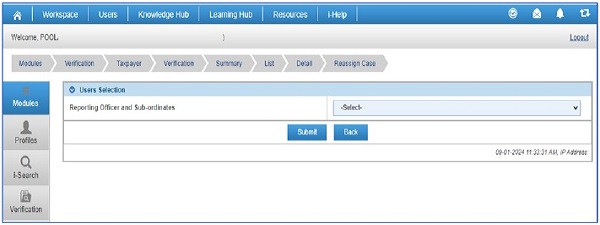

Reassign Case

10. User will be able to Reassign Group case to the Reporting Officer and Subordinates in hierarchy.

Figure 6Activity Reassign Case

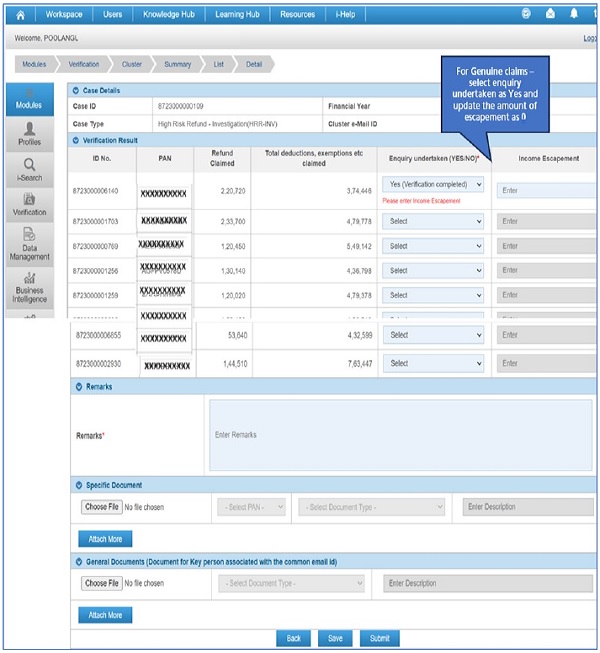

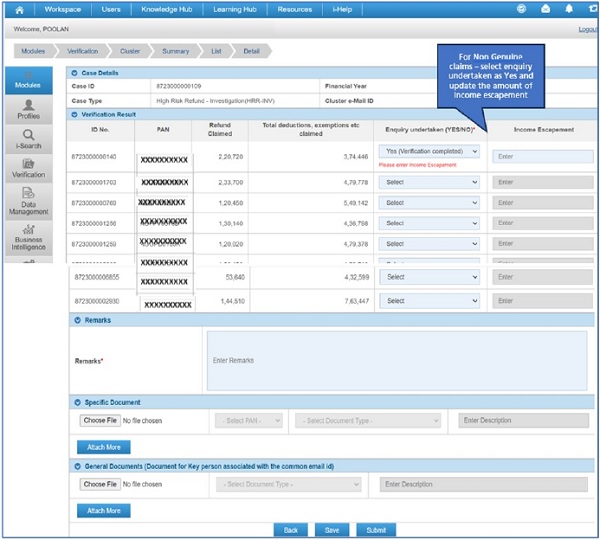

Submit Verification Report (Bulk)

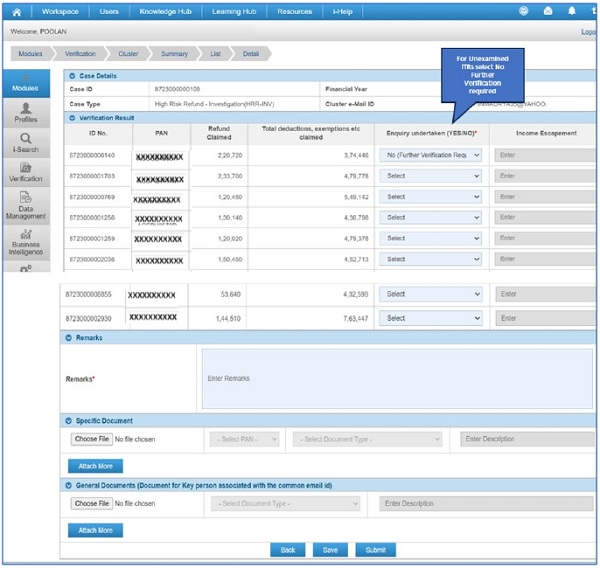

11. This activity will be performed by ITD User to submit the Verification Report on the Group Case.

a. User will be able to provide feedback on enquiry undertaken (Yes/No) and amount of Income escapement with respect to each PAN.

i. Amount to be entered will be mandatory in case Yes has been selected by user under option “enquiry undertaken”.

ii. For Genuine Claim user will provide feedback as “Yes Verification completed” and update the amount as 0 in Income Escapement Column.

iii. For Non-Genuine Claim user will provide feedback as “Yes Verification completed” and update the amount of Income escaping assessment.

iv. For Unexamined ITRs user needs to provide feedback as “No further Verification Required”.

Figure 7 Activity Submit Verification Report (Bulk)

12. User will be able to make the Verification Result of the case.

a. Columns PANs (as available in Group Case), Refund claimed (in ITR), Total expenses, deductions claimed will be pre-filled.

b. User will be able to provide feedback on enquiry undertaken (Yes/No) and amount of Income escapement with respect to each PAN.

i. Amount to be entered will be mandatory in case Yes has been selected by user under option “enquiry undertaken”.

ii. For Genuine Claim user will provide feedback as “Yes Verification completed” and update the amount as 0 in Income Escapement Column.

iii. For Non–Genuine Claim user will provide feedback as “Yes Verification completed” and update the amount of Income escaping assessment.

iv. For Unexamined ITRs user needs to provide feedback as “Nofurther Verification Required”. User needs to attach relevant document for each PAN quantifying tentative escapement on basis of risk parameters on which the ITR was flagged.

v. Where user is able to identify Key person of the cluster he may provide General document relevant to identification of the key person.

13. Remarks will be mandatory.

14. User will be able to add documents specific to the PAN Case under section “Specific Documents”.

15. General documents relevant for Key person associated with the common mail ID can be added in the “General Documents” section.

16. On clicking submit button, Verification Report will be submitted and the status of the case will be updated from “Under Verification” to “Verified”.

17.

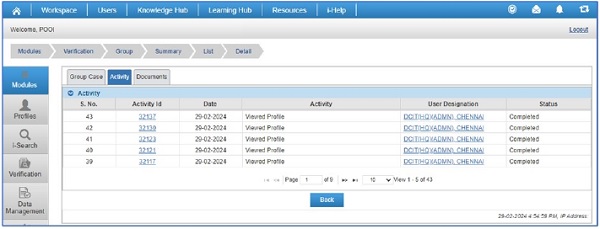

History of activities performed at Group Case Level

18. History of Activities performed at Group Case Level will be visible to ITD user at Activity Tab available at Group Case Detail view.

19. The page will display Activity ID wise activities with complete details of remarks and documents uploaded by user while performing the activity.

Figure 8Group Activities History view

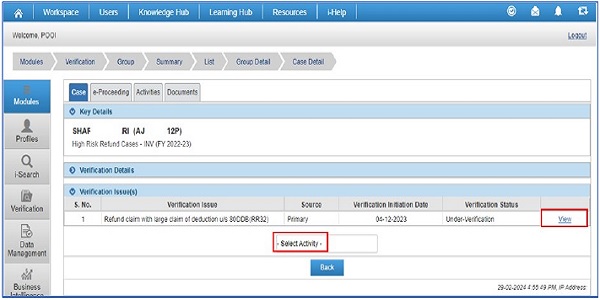

Case Detail View

Figure 9Case Detail View

20. The Case Detail page will display details of case available on individual PAN in the group and provide detail of Verification Issue on the PAN

21. View hyperlink will navigate the user to Information Detail view.

22. Refer section “case level activities available on PAN Case” for detail of activities available at Case level.

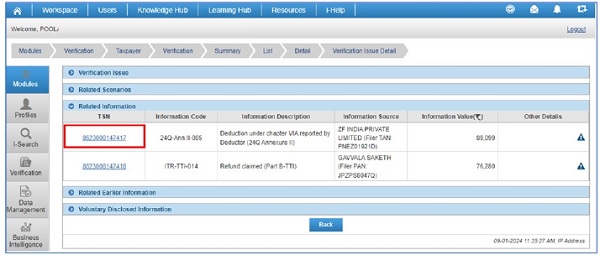

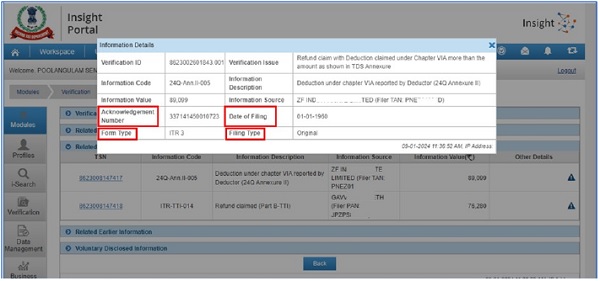

Information Detail View

23. Information Detail view will provide detail of Information underlying the Verification Issue. TSN will be hyperlink which will provide detail of Information like Acknowledgement Number, Date of Filing, Form Type and Filing Type.

Figure 10 Information Detail View

TSN Pop up view

Figure 11 Pop up View

Case Level activities available on Individual PAN Case

24. User will be able to below mention activities at Individual PAN Case level.

a. Enter Comments- This activity will allow ITD user to enter case level comments. The history of activity performed by ITD User will be visible to all supervisors in hierarchy (in cumulative view).

Figure 12 Enter Comments

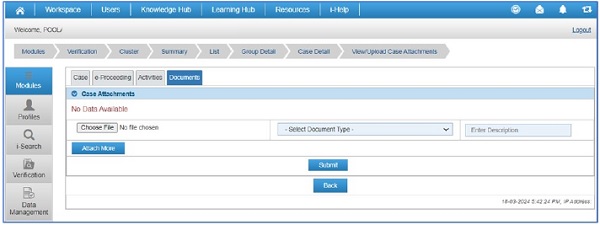

b. View upload Case attachments – This activity will allow ITD User to upload documents relevant to the case. The history of activity performed along with the documents uploaded by the ITD User will be visible to all supervisors in hierarchy (in cumulative view).

Figure 13 View Upload Case Attachments

Figure 14

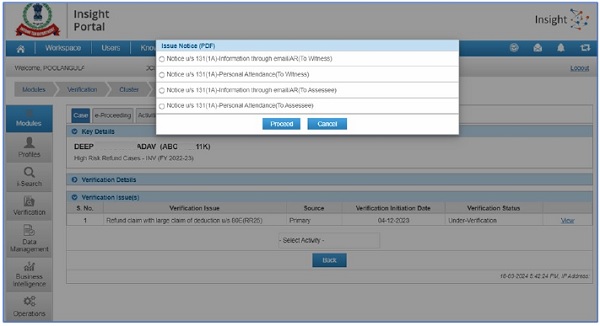

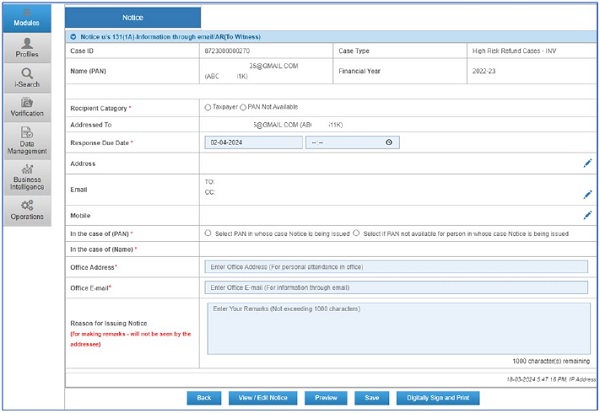

c. Issue Notice (PDF) –These Notices can be issued to Taxpayer (Assessee/Witness) for calling of information. Taxpayer will be required to submit the response through email (email address will be mentioned in notice) OR through Authorized Representative (AR) or Personal attendance in office (office address and attendance time will be mentioned in notice). Response against Notice can be submitted by Taxpayer will be required to submit the response through email (email address will be mentioned in notice) OR through Authorized Representative (AR) in office (office address and attendance time will be mentioned in notice).

Figure 15 Issue Notice PDF

Issue Notice (PDF)

25. Following types of Notices has been enabled at Individual PAN Case level. These notices can be issued to

d. Notice u/s 131(1A)-Information through email/ AR (To Witness)

e. Notice u/s 131(1A)-Information through email/ AR (To Assessee)

f. Notice u/s 131(1A)-Personal Attendance (To Witness)

g. Notice u/s 131(1A)-Personal Attendance (To Assessee)

Figure 16 Notice Generation screen

26. User needs to select the relevant Notice and click on proceed.

27. After selection of the notice template, user will be navigated to notice generation screen.

(Note – On notice generation screen, fields will be populated as per selected notice template)

28. On Notice Generation screen, follow below mentioned steps:

h. Select the radio button ‘Taxpayer’ against ‘Recipient Category’ field.

i. On the displayed pop-up screen, enter the PAN of the person/ entity to whom notice will be issued.

j. Click on Search button and click against a PAN from the Results. Click Select.

k. Upon selecting the recipient from ‘Recipient Category’ field, below fields will be auto populated:

i. Addressed To – Name and PAN of the recipient

ii. Address – Address of the recipient

iii. Email – Email of the recipient

iv. Mobile – Mobile of the recipient

l. Select Response Due Date (Time also for attendance in office)

m. Select PAN in whose case Notice is being Issued radio button from ‘In the case of (PAN)’ field (applicable if notice is being issued to Witness)

i. On the displayed pop-up screen, enter the PAN of the person/ entity in whose case notice is being Issued.

ii. Click on Search button and click against a PAN from the Results. Click Select.

n. Upon selecting the PAN, below field will be auto populated:

i. In the case of (Name) – Name and PAN of the person/ entity in whose case notice is being Issued.

o. Provide Office Address (applicable for attendance in office)

p. Provide Office E-mail (applicable for response through E-mail)

q. Provide ‘Reason for Issuing Notice’ – Reason for issuing notice for internal purpose.

r. Provide additional text in Rich Text Format box – Click on ‘View/ Edit Notice’ button to enter the additional text. The addition text will be appended to notice.

s. Preview the notice to verify the content. – On click of ‘Preview’ button, draft notice will be downloaded in PDF format.

t. Click on Print and Digitally Sign Now button to digitally sign and generate the notice.

Viewing the Generated Notice at Insight Portal

The Notice issued u/s 131(1A) can be viewed under ‘e-Proceeding’ tab available at Case Detail Page.

29. Issued notice details can be viewed under e-Proceeding case tab.

u. On clicking DIN, generated notice will be downloaded.

30. Initiated activity details can be viewed from Activities tab.

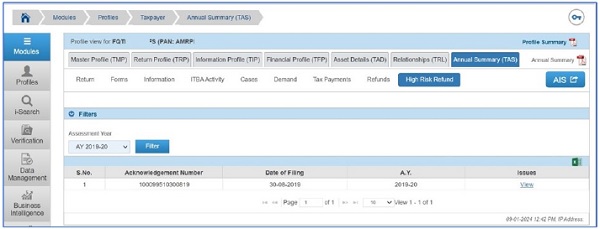

View Previous Years HRR Issue in Taxpayer Profile views

31. The user will be able to view the Details of the High-Risk Refund issues flagged on PAN of the Taxpayer in Previous years, if any, in Taxpayer Profile Views under Taxpayer Annual Summary (TAS).

32. User needs to select the relevant Assessment Year filter.

33. User will be able to click on view hyperlink and view the Verification issues of previous year acknowledgement Number wise.

Figure 17 View previous year HRR Issues

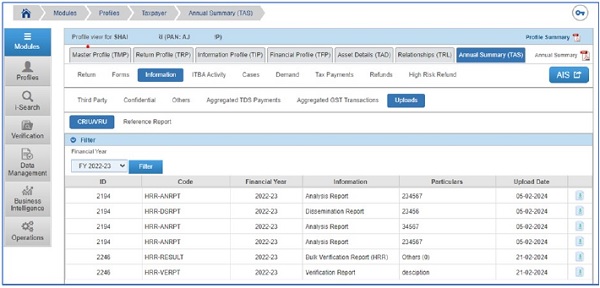

Viewing the Verification Report in Respective PAN in Profile views

34. The Verification Report submitted in bulk in the case by investigation user will be visible in Taxpayer Profile views of Respective PANs.

35. Any ITD User having level 2 access over PAN will be able to view the Verification Report submitted by Investigation user in HRR Investigation case under Taxpayer Annual Summary (TAS)>>Information>.Uploads

36. User will be able to view complete details of the Verification Report submitted alongwith documents uploaded.

Notes

1CRU Nodal officer referred in the SOP shall be the same CRU Nodal Office as referred in the OM Dated 08/06/2022 Sub: – Revised guidelines for management of Suspicious Transaction Reports and exchange of information with Financial Intelligence Unit — India (FIU-IND)

2The 10 needs to refer to the relevant Insight Instruction for accessing the case type and related details in Insight Portal.

—–End of Document—-