Form 16 and Form 16A are important TDS certificates issued under the Income-tax Act, 1961 to certify tax deducted at source and assist taxpayers in accurate return filing. Form 16 is issued by employers or specified banks for TDS deducted under Sections 192 and 194P and comprises Part A, containing TDS details, and Part B, containing salary, pension, allowances, deductions, rebates, and perquisite information. It must generally be issued by 15 June following the relevant financial year. Form 16A, on the other hand, is issued quarterly for TDS deducted under provisions other than specified exclusions and includes details such as PAN/Aadhaar, TAN, challan particulars, and TDS return receipt numbers. Both certificates are generated through the TRACES portal and may be authenticated digitally or manually. Failure by the deductor to issue these certificates attracts a penalty of Rs. 500 per day under Section 272A.

Form 16 and Form 16A

A TDS (Tax Deducted at Source) certificate is a document issued to a person who has deducted tax on payments made to another person. The TDS certificate is issued under the provisions of the Income-tax Act, which requires certain persons to deduct tax at source before making payment to the recipient. In this tutorial, we will understand the TDS certificate issued in Form 16 and Form 16A.

Form 16

Where the employer has deducted tax under Section 192 from the employee’s salary or tax has been deducted by the specified bank under Section 194P from the total income of the senior citizen, then the employer/specified bank is required to issue TDS certificate in Form 16.

The TDS certificate is divided into two parts – Part A and Part B. Part A provides information on the tax that has been deducted, while Part B includes details related to the employee’s salary, such as allowances, deductions, rebates, etc. For tax deducted under Section 194P, Part B also includes details on the senior citizen’s pension, interest income, as well as any deductions, rebates, etc. that may have been allowed.

The deductor is required to verify the contents of Part A and Part B of the TDS certificate before issuing them to the deductee. This authentication can be done either manually or digitally using a signature. The deductor shall ensure that once the certificate is digitally signed, the contents of the certificates are not amenable to change, the certificates have a control number, and he maintains a log of such certificates.

Further, the employer shall provide information relating to the nature and value of perquisites separately in Form No. 12BA if the salary paid or payable is above Rs. 1,50,000. In other cases, the information would have to be provided by the employer in Form No. 16 itself.

In case of more than one employer

In case an employee has worked or is currently working with multiple employers in a financial year, each employer is obligated to provide Part A of Form 16 for the duration the employee was employed under them. The employee can choose to receive Part B from either each employer or the last employer.

Due date for issue of certificate

Form 16 is required to be issued by the employer up to 15th June of the financial year immediately following the financial year in which the amount was paid and tax has been deducted.

Steps to download Form 16

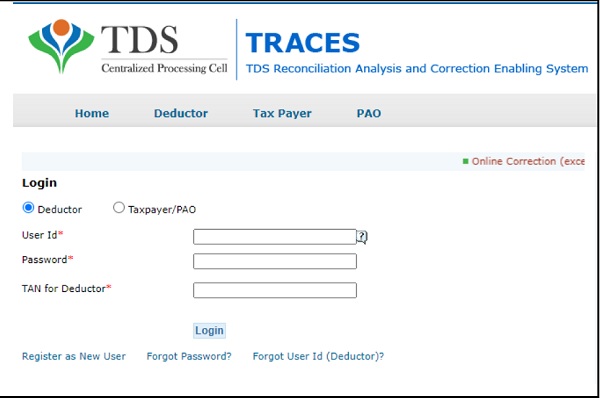

Step 1: Visit TRACES (www.tdscpc.gov.in)

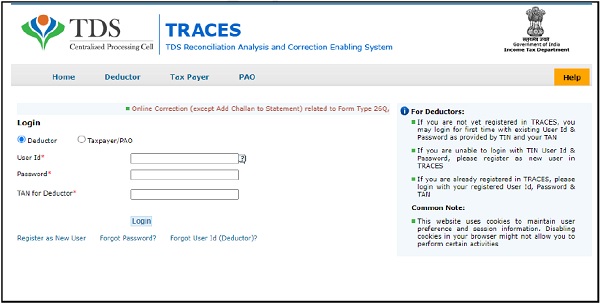

Step 2: Login using the User ID, Password and TAN.

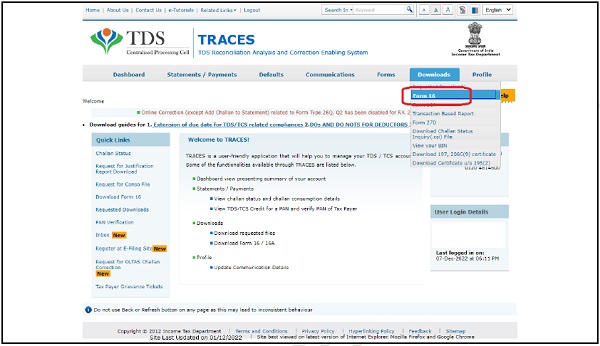

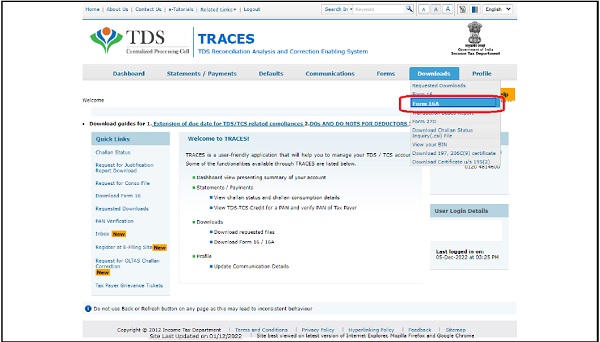

Step 3: Go to Downloads Form 16.

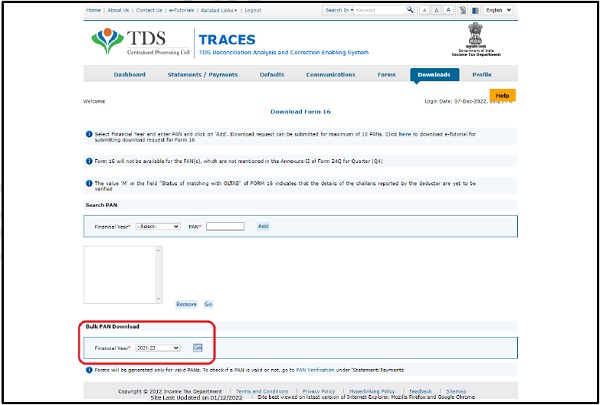

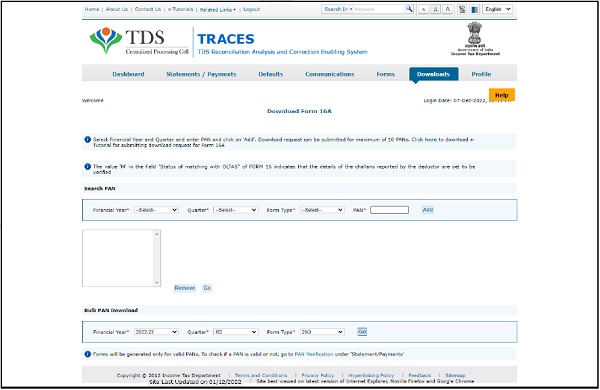

Step 4: Select the Financial Year, enter PAN and click ‘Add‘. After the PANs are reflected in the window, click ‘Go’. A maximum of 10 PANs can be added to this screen. To generate TDS Certificate in bulk, in the lower section of ‘Bulk PAN Download’, select Financial Year, and click ‘Go’.

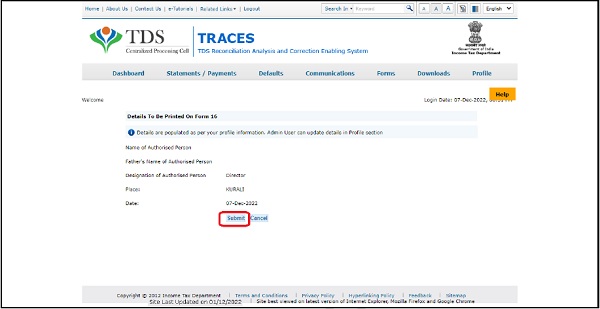

Step 5: On the next screen, the details to be printed on Form 16 will be displayed. Verify the details and click ‘Submit’.

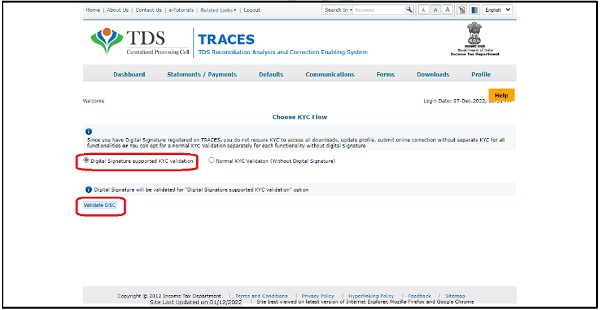

Step 6: Select the option for DSC-based validation or Normal Validation.

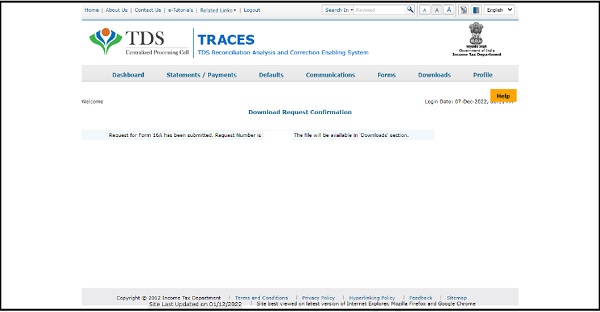

Step 7: After submission of the request, a successful message with a reference number will appear on the screen.

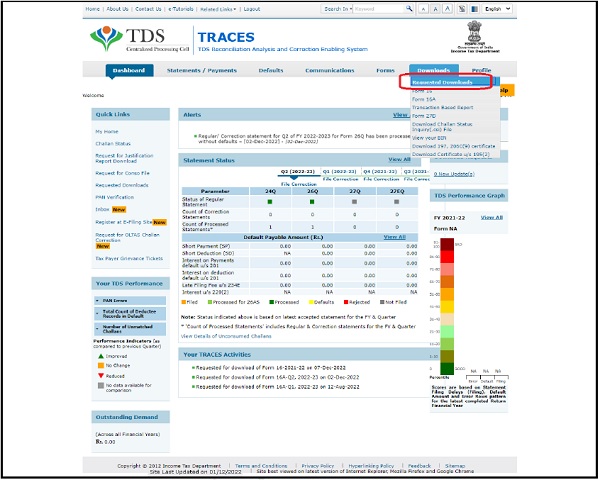

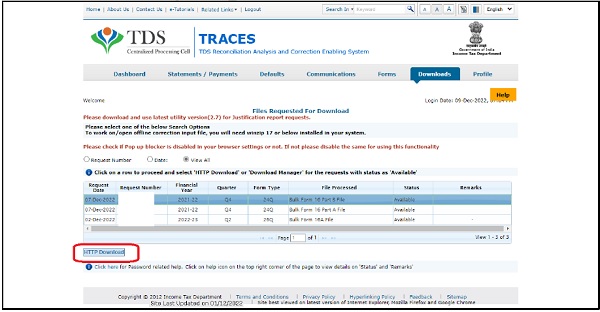

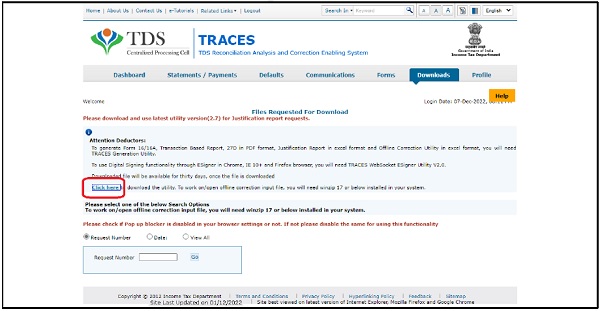

Step 8: Go to Downloads>Requested Downloads.

Step 9: Enter the request number generated on submission of the request (Step 7) and click ‘Go’. The filing status of Form 16 will be displayed. Select the row and click on ‘HTTP download’.

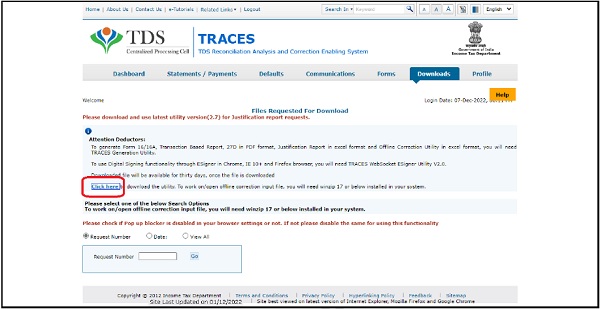

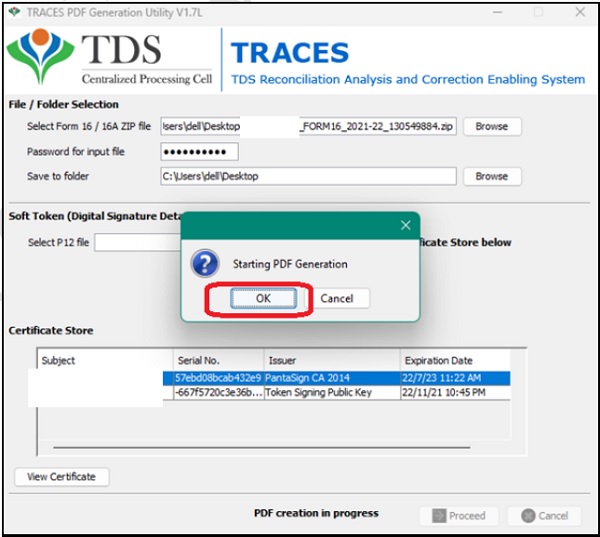

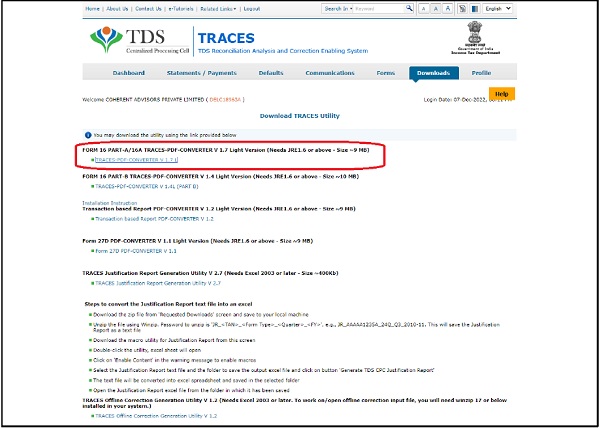

Step 10: Download the TRACES PDF Generation Utility. To view the PDF version of the downloaded Form 16, TRACES PDF Generation Utility can be used to extract the same. Different utilities must be downloaded for Form 16-PART A and Form 16-PART B.

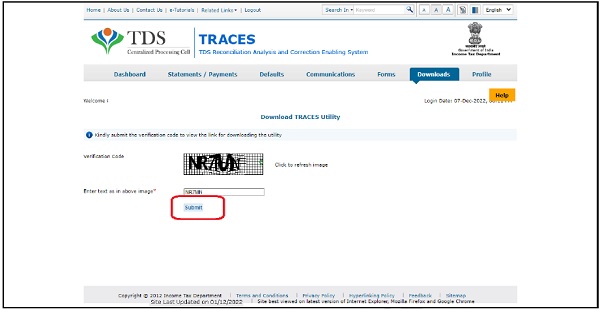

Step 11: Enter the captcha and click on ‘Submit’ to download the utility

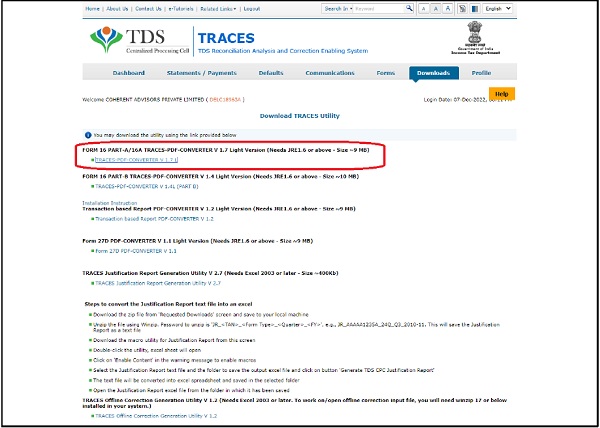

Step 12: Click on the link to start the download

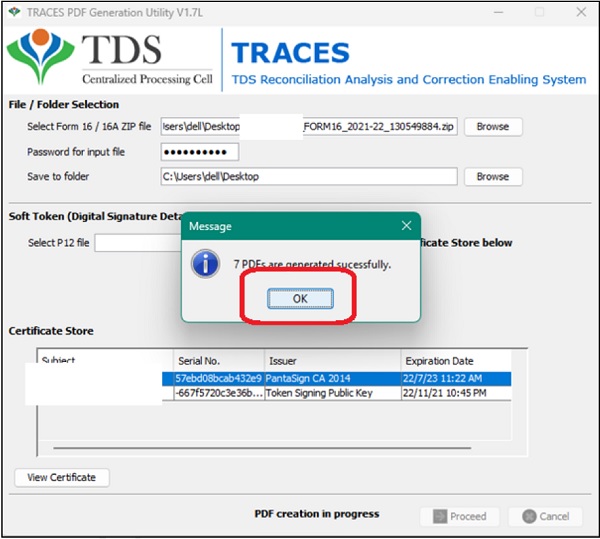

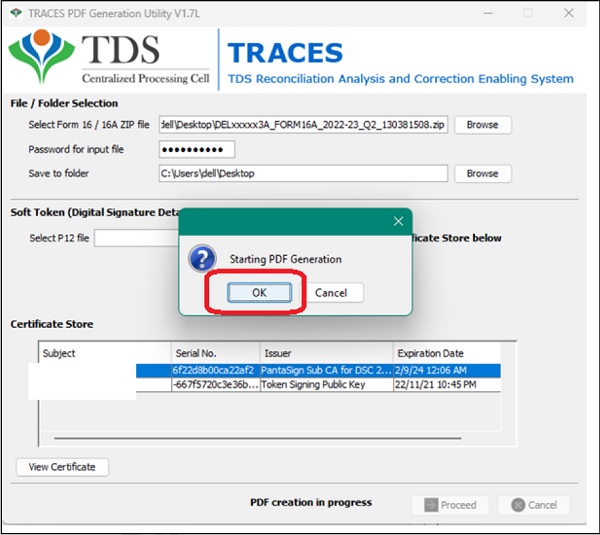

Step 13: Extract the PART-A utility, browse the form 16-PARTA Zip file and affix the DSC to sign the certificates digitally.

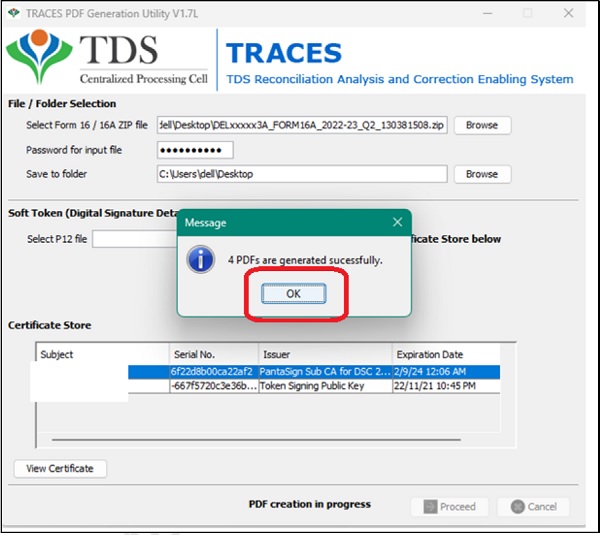

Step 14: Form 16-PART A shall be generated.

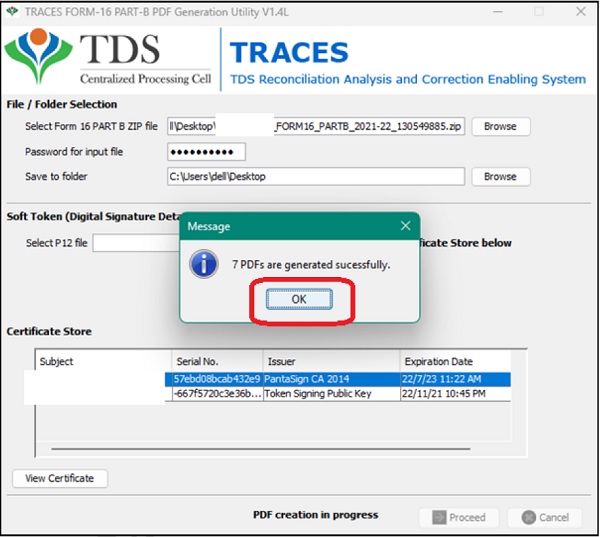

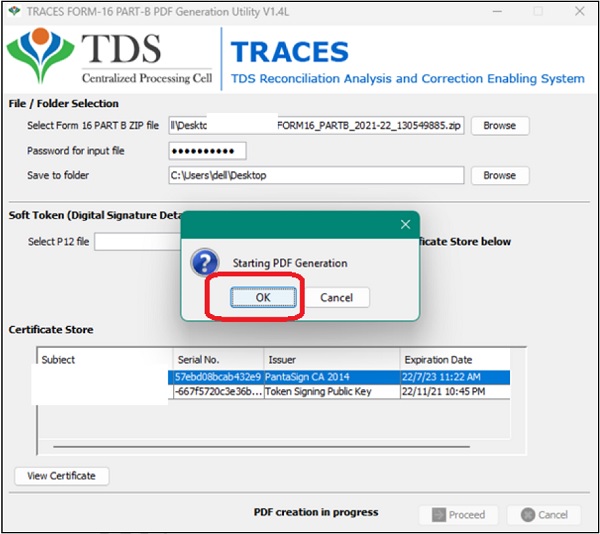

Step 15: Extract the PART-B utility, browse the Form 16-PARTB Zip file and affix the DSC to sign the certificates digitally.

Step 16: Form 16-PART B shall be generated.

Form 16A

If tax has been deducted under any provision other than Section 192, Section 194-IA, Section 194-IB, Section 194M, Section 194P, and Section 194S (for specified persons), then the deductor is required to issue a TDS certificate in Form 16A . This TDS certificate shall be downloaded from the website of TRACES. Deductors shall authenticate these certificates using either a digital or manual signature.

Form 16A generally contains the following information:

(a) Permanent Account Number (PAN) or Aadhaar of deductee

(b) Tax Deduction and Collection Account Number (TAN) of the deductor

(c) Book Identification Number if tax is deposited by the Govt. Office without production of challan

(d) Challan Identification Number in case of payment through bank

(e) Receipt Number of the TDS Statement furnished in Form 26Q or Form 27Q or Form 26QF

Due date for issue of certificate

Form 16A is required to be issued by the deductor on a quarterly basis within 15 days from the due date of furnishing the statement of tax deducted at source in Form 26Q or Form 27Q. For Quarters 1, 2, 3, and 4 the due date for issue of the TDS certificate shall be August 15, November 15, February 15, and June 15 (of the next financial year), respectively.

Steps to download Form 16A

Step 1: Visit TRACES (www.tdscpc.gov.in)

Step 2: Login using the User ID, Password and TAN.

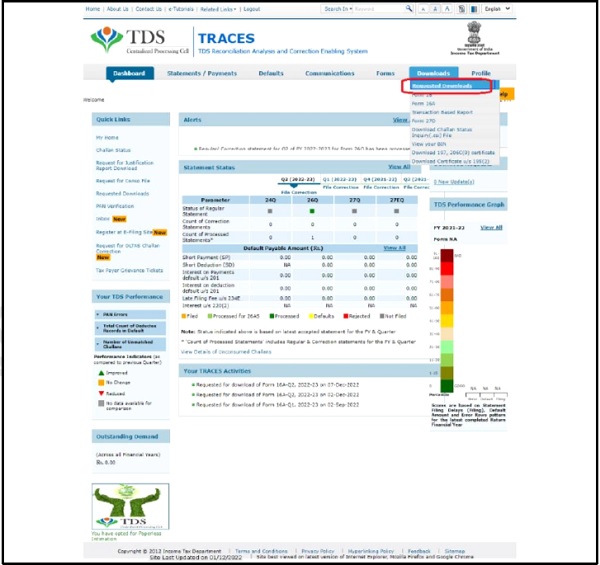

Step 3: Go to Downloads> Form 16A .

Step 4: Select the Financial Year, Quarter, Form Type, enter PAN and click ‘Add‘. After the PANs are reflected in the window, click ‘Go’. A maximum of 10 PANs can be added to this screen. To generate TDS Certificate in bulk, in the lower section of ‘Bulk PAN Download’, select Financial Year, Quarter, Form Type and click ‘Go’.

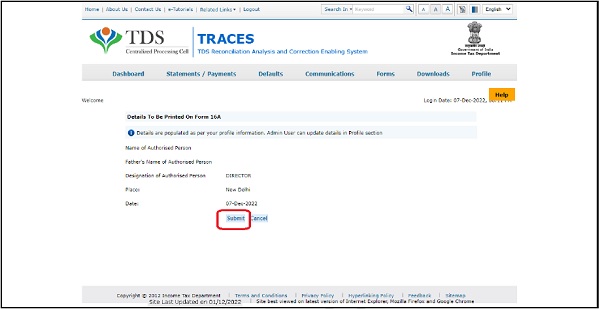

Step 5: On the next screen, the details to be printed on Form 16A will be displayed. Verify the details and click ‘Submit’.

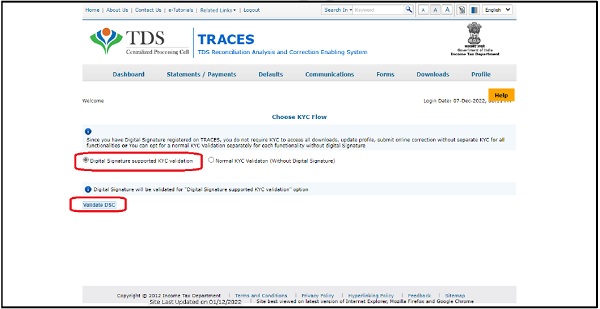

Step 6: Sign using the digital signature certificate.

Step 7: After submission of the request, a successful message with a reference number will appear on the screen.

Step 8: Go to Downloads>Requested Downloads.

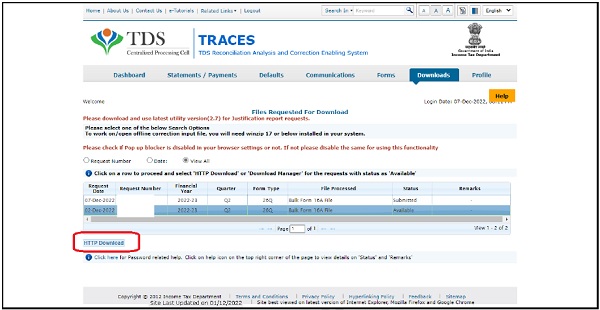

Step 9: Enter the request number generated on submission of the request (Step 7) and click ‘Go’. The filing status of Form 16A will be displayed. Select the row and click on ‘HTTP download’. The file for Form 16A will be downloaded.

Step 10: Download the TRACES PDF Generation Utility. To view the PDF version of the downloaded Form 16A , TRACES PDF Generation Utility can be used to extract the same.

Step 11: Enter the captcha and click on ‘Submit’ to download the utility

Step 12: Click on the link to start the download.

Step 13: Extract the utility, browse the Form 16A Zip file and affix the DSC to sign the certificates digitally.

Step 14: Form 16A shall be generated.

Duplicate Certificate

The deductor may issue a duplicate certificate if the deductee has lost the original certificate and makes a request for the issue of a duplicate certificate. This certificate should be certified as ‘Duplicate’ by the deductor.

Penalty for non-issuance of TDS Certificate

Where a person, who has deducted tax at source, fails to issue a TDS Certificate, he shall be liable for payment of a penalty of Rs. 500 per day under Section 272A.

MCQs on Form 16 and Form 16A

Q1. Form 16 can be downloaded from the website of TRACES __________.

a) After filing TDS Statement

b) After processing of the TDS Statement

c) Before processing of TDS Statement

d) Either (b) or (c)

Correct Answer: (b)

Justification of the correct answer: The TDS certificate shall be downloaded from the website of TRACES (https://www.tdscpc.gov.in) after processing of the TDS Statement.

Q2. The employer is required to issue __________ with respect to the tax deducted from the employee’s salary.

(a) Form 16

(b) Form 16A

(c) Form 16B

(d) Form 16C

Correct Answer: (a)

Justification of the correct answer: Where the employer has deducted tax under Section 192 from the employee’s salary, then the employer shall issue a TDS certificate to the employee in Form 16.

Q3. Form 16 contains ________.

(a) Details of tax deducted from salary

(b) Details of the salary and various allowances, deductions, rebate, etc. claimed by employee

(c) Details of the salary and various allowances, deductions, rebate, etc. allowed to employee

(d) All of the above

Correct Answer: (d)

Justification of the correct answer: The TDS Certificate in Form 16 has two parts – Part A and Part B. Part A of the certificate contains the details of tax deducted from salary. Whereas Part B contains the details of the salary and various allowances, deductions, rebate, etc. claimed or allowed to the employee.

Q4. The certificate can be verified by __________.

(a) Manual Signature

(b) Digital Signature

(c) Either (a) or (b)

(d) Both (a) and (b)

Correct Answer: (c)

Justification of the correct answer: The certificate can be verified either by using a manual signature or a digital signature.

Q5. The employer shall provide information relating to the nature and value of perquisites in ________ if the salary paid or payable is above ________.

(a) Form No. 12B, Rs. 3,00,000

(b) Form No. 12BA, Rs. 1,50,000

(c) Form No. 16, Rs. 3,00,000

(d) Form No. 16, Rs. 1,50,000

Correct Answer: (b)

Justification of the correct answer: The employer shall provide information relating to the nature and value of perquisites in Form No. 12BA if the salary paid or payable is above Rs. 1,50,000. In other cases, the information would have to be provided by the employer in Form No. 16 itself.

Q6: Form 16 is required to be issued by the employer up to _________ immediately following the financial year in which the amount was paid and tax has been deducted.

(a) 15th March of the financial year

(b) 15th June of the financial year

(c) 15th July of the financial year

(d) 15th May of the financial year

Correct Answer: (b)

Justification of the correct answer: Form 16 is required to be issued by the employer up to 15th June of the financial year immediately following the financial year in which the amount was paid and tax has been deducted.

Q7. Form 16A is required to be issued by the deductor on ____________.

(a) Quarterly basis

(b) Half-yearly basis

(c) Yearly basis

(d) None of the above

Correct Answer: (a)

Justification of the correct answer: Form 16A is required to be issued by the deductor on a quarterly basis within 15 days from the due date of furnishing the statement of tax deducted at source in Form 26Q or Form 27Q. For Quarters 1, 2, 3, and 4 the due date for issue of the TDS certificate shall be August 15, November 15, February 15, and June 15 (of the next financial year), respectively.

Q8. Where a person, who has deducted tax at source, fails to issue a TDS Certificate, he shall be liable for payment of a penalty of____________.

(a) Rs. 500 per day under Section 272A

(b) Rs. 1,000 per day under Section 272A

(c) Rs. 50,000

(d) Rs. 1,00,000

Correct Answer: (a)

Justification of the correct answer: Where a person, who has deducted tax at source, fails to issue a TDS Certificate, he shall be liable for payment of a penalty of Rs. 500 per day under Section 272A.

Q9. Form 16A is issued if the tax has beed deducted under __________.

(a) Section 194-I

(b) Section 194-IA

(c) Section 194-IB

(d) All of the above

Correct Answer: (a)

Justification of the correct answer: Where tax has been deducted under any provision, not being Section 192, Section 194-IA, Section 194-IB, Section 194M, Section 194P, and Section 194S (in case of a specified person), the deductor shall issue a TDS Certificate in Form 16A .

Q10. Form 16A contains __________.

(a) Permanent Account Number (PAN) or Aadhaar of deductee

(b) Challan Identification Number in case of payment through bank

(c) Receipt Number of the TDS Statement furnished in Form 26Q or Form 27Q or Form 26QF

(d) All of the above

Correct Answer: (d)

Justification of the correct answer: Form 16A generally contains the following information:

a) Permanent Account Number (PAN) or Aadhaar of deductee

b) Tax Deduction and Collection Account Number (TAN) of the deductor

c) Book Identification Number if tax is deposited by the Govt. Office without production of challan

d) Challan Identification Number in case of payment through bank

e) Receipt Number of the TDS Statement furnished in Form 26Q or Form 27Q or Form 26QF

Above document contains the provisions of the Income-tax Act, 1961, as amended by the Finance Act, 2026.

******

Disclaimer: The contents of this document are for information purposes only. This aims to enable public to have a quick and an easy access to information and do not purport to be legal documents. Viewers are advised to verify the content from Government Acts/Rules/Notifications etc.

(Republished with amendments)

Can an individual download form 16 or 16A for himself/herself?