Q.1 Who is eligible to file ITR-2 for AY 2021-22?

Ans. ITR-2 can be filed by individuals or HUFs who:

-Are not eligible to file ITR-1 (Sahaj)

-Do not have income from profit and gains of business or profession and also do not have income from profits and gains of business or profession in the nature of:

- interest

- salary

- bonus

- commission or remuneration, by whatever name called, due to, or received by him from a partnership firm

-Have the income of another person like spouse, minor child, etc., to be clubbed with their income – if income to be clubbed falls in any of the above categories.

Q.2 Who is not eligible to file ITR-2 for AY 2021-22?

Ans. ITR-2 cannot be filed by any individual or HUF, whose total income for the year includes income from profit and gains from business or profession, and also who has income in the nature of:

- interest

- salary

- bonus

- commission or remuneration, by whatever name called, due to, or received by him from a partnership firm.

Q.3 What are the changes in ITR-2 as compared to previous years?

Ans. In ITR-2 of AY 2021-22, you can choose to opt for the new tax regime under section 115BAC. Please note that option for selecting new tax regime u/s 115BAC will be available only till the due date of filing of return u/s 139(1).

Q.4 What documents do I need to file ITR-2?

Ans.

- If you have salary income, you need Form 16 issued by your employer.

- If you have earned interest on fixed deposits or saving bank account and TDS has been deducted on the same, you need TDS certificates i.e., Form 16A issued by Deductors.

- You will need Form 26AS to verify TDS on salary as well as TDS other than salary. Form 26AS could be downloaded from the e-Filing portal.

- If you are living in rented premises, you need rent paid receipts for calculation of HRA (in case you have not submitted the same to your employer).

- If you have any capital gains transactions in shares, you will need a summary or profit / loss statement of capital gain transactions of shares or securities during a year, if any, for computation of capital gain.

- You will need your bank passbook, Fixed Deposit Receipts (FDRs) to calculate amount of interest income.

- If you have received rent from your rented house property, then you will need your tenant / local tax payment / interest on borrowed capital details (if any) to calculate income from house property.

- In case you want to claim any loss incurred during the current year, then you will need the relevant documents exhibiting the loss.

- In case you wish to claim previous year’s loss, you will need a copy of ITR-V pertaining to the previous year, disclosing the said loss.

- You will also need documents or proofs for claiming tax saving deductions u/s 80C, 80D, 80G, 80GG such as life and health insurance receipts, donation receipts, rent receipts, receipts for tuition fees etc., if the same were not considered in your Form 16.

Q.5 What precautions should I take to avoid issues while filing my ITR?

Ans. To avoid issues in filing your return and getting your refund, you must ensure you have done the following:

- Linked Aadhaar and PAN.

- Pre-validated your bank account where you want to receive your refund.

- Choose the correct ITR before filing it; else filed return will be treated as defective and you will need to file a revised ITR using the correct form.

- File the return within the specified timelines.

- Verify your return – you can opt for e-Verification (recommended option – e-Verify Now) is the easiest way to verify your ITR.

Q.6 Can an HUF / Firm claim rebate u/s 87A?

Ans. No. Rebate under section 87A is available only to an individual, hence, any person other than an individual cannot claim rebate under section 87A.

Q.7 I am a non-resident. Can I claim rebate u/s 87A?

Ans. No. Rebate under section 87A is available only to an individual who is resident in India, hence, non-residents cannot claim rebate under section 87A.

Q.8 I own two houses. One is a farmhouse that I visit every week, and the other is my residence. Can both these residences be treated as self-occupied?

Ans. Up to AY 2019-20, you can claim only one property as self-occupied property and other property will be deemed to be let-out. From AY 2020-21 onwards only, both the houses can be treated as self-occupied properties for residential purpose subject to fulfilment of specified conditions.

Q.9 How to compute income from a property that is self-occupied for part of the year and let out for part of the year?

Ans. In this case, for the purpose of computation of income chargeable to tax under the head Income from House Property, such a property will be treated as let-out throughout the year and income will be computed accordingly. However, while computing the taxable income in case of such a property, actual rent will be considered only for the let-out period.

Q.10 What incomes are charged to tax under the head Capital Gains?

Ans. Any profit or gain arising from transfer of a capital asset during the year is charged to tax under the head Capital Gains.

Q.11 What is the meaning of Capital Asset?

Ans. Capital Asset is defined under Section 2(14) of the Income Tax Act, 1961 to include:

- Any kind of property held by an assessee, whether or not connected with business or profession of the assessee.

- Any securities held by a FII which has invested in such securities in accordance with the Regulations made under the SEBI Act, 1992 (subject to certain exclusions).

Q.12 What is the meaning of the term Long-Term Capital Asset?

Ans.

- Any capital asset held for a period of more than 36 months immediately preceding the date of its transfer will be treated as Long-Term Capital Asset. However, in respect of certain assets like shares (equity or preference) which are listed in a recognized stock exchange in India, units of equity-oriented mutual funds, listed securities like Debentures and Government Securities, Units of UTI and Zero Coupon Bonds, the period of holding to be considered is 12 months instead of 36 months.

- In case of unlisted shares in a company, the period of holding to be considered is 24 months instead of 36 months.

- With effect from AY 2018-19, the period of holding of immovable property (being land or building or both) shall be considered as 24 months instead of 36 months.

Q.13 As per the Income Tax Law, gain arising on transfer of Capital Asset is charged to tax under the head Capital Gains. What constitutes transfer as per Income Tax Law?

Ans. Generally, transfer means sale, however, as per Section 2(47) of the Income Tax Act, 1961 transfer, in relation to a Capital Asset, includes:

- Sale, exchange or relinquishment of the asset;

- Extinguishment of any rights in relation to a Capital Asset;

- Compulsory acquisition of an asset;

- Conversion of Capital Asset into Stock-in-Trade;

- Maturity or redemption of a Zero Coupon Bond;

- Allowing possession of immovable properties to the buyer in part performance of the contract of the nature referred to in section 53A of the Transfer of Property Act, 1882;

- Any transaction which has the effect of transferring an (or enabling the enjoyment of) immovable property; or

- Disposing of or parting with an asset or any interest therein or creating any interest in any asset in any manner whatsoever.

Q.14 What are the provisions framed under the Income Tax Law in relation to carry forward and set-off of Capital Loss?

Ans.

- If loss under the head Capital Gains incurred during a year cannot be adjusted in the same year, then unadjusted Capital Loss can be carried forward to next year.

- In the subsequent year(s), such loss can be adjusted only against income chargeable to tax under the head Capital Gains, however, Long-Term Capital Loss can be adjusted only against Long-Term Capital Gains. Short-Term Capital Loss can be adjusted against Long-Term Capital Gains as well as Short-Term Capital Gains.

- Such loss can be carried forward for eight years immediately succeeding the year in which the loss is incurred.

- Such loss can be can carried forward only if the return of income / loss of the year in which loss is incurred is furnished on or before the due date of furnishing the return, as prescribed u/s 139(1).

Manual

1. Overview

The pre-filling and filing of ITR-2 service is available to registered users on the e-Filing portal. This service enables individual taxpayers to file ITR-2 online through the e-Filing portal. This user manual covers filing of ITR-2 through online mode.

2. Prerequisites for availing this service

| General |

|

| Others |

|

ITR-2 has the following sections that you need to fill before submitting the form, a summary section where you review your tax computation and pay tax and finally submit the return for verification:

3.1 Part A General

3.2 Schedule Salary

3.3 Schedule House Property

3.4 Schedule Capital Gains

3.5 Schedule 112A and Schedule-115AD(1)(iii) proviso

3.6 Schedule Other Sources

3.7 Schedule CYLA

3.8 Schedule BFLA

3.9 Schedule CFL

3.10 Schedule VI-A

3.11 Schedule 80G and Schedule 80GGA

3.12 Schedule AMT

3.13 Schedule AMTC

3.14 Schedule SPI

3.15 Schedule SI

3.16 Schedule EI

3.17 Schedule PTI

3.18 Schedule FSI

3.19 Schedule TR

3.20 Schedule FA

3.21 Schedule 5A

3.22 Schedule AL

3.23 Part B – Total Income (TI)

3.24 Tax Paid

3.25 Part B-TTI

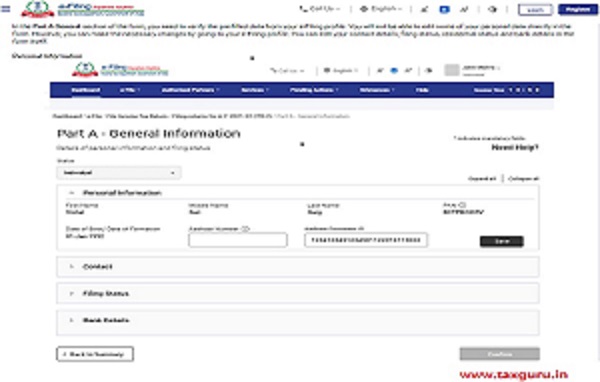

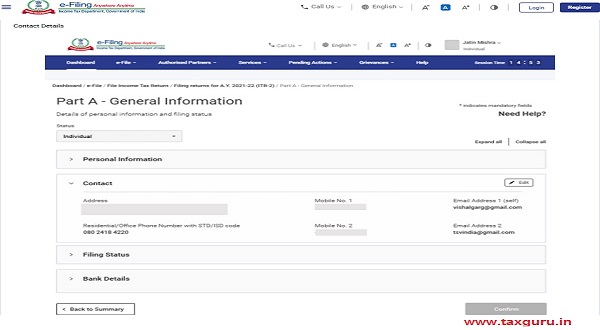

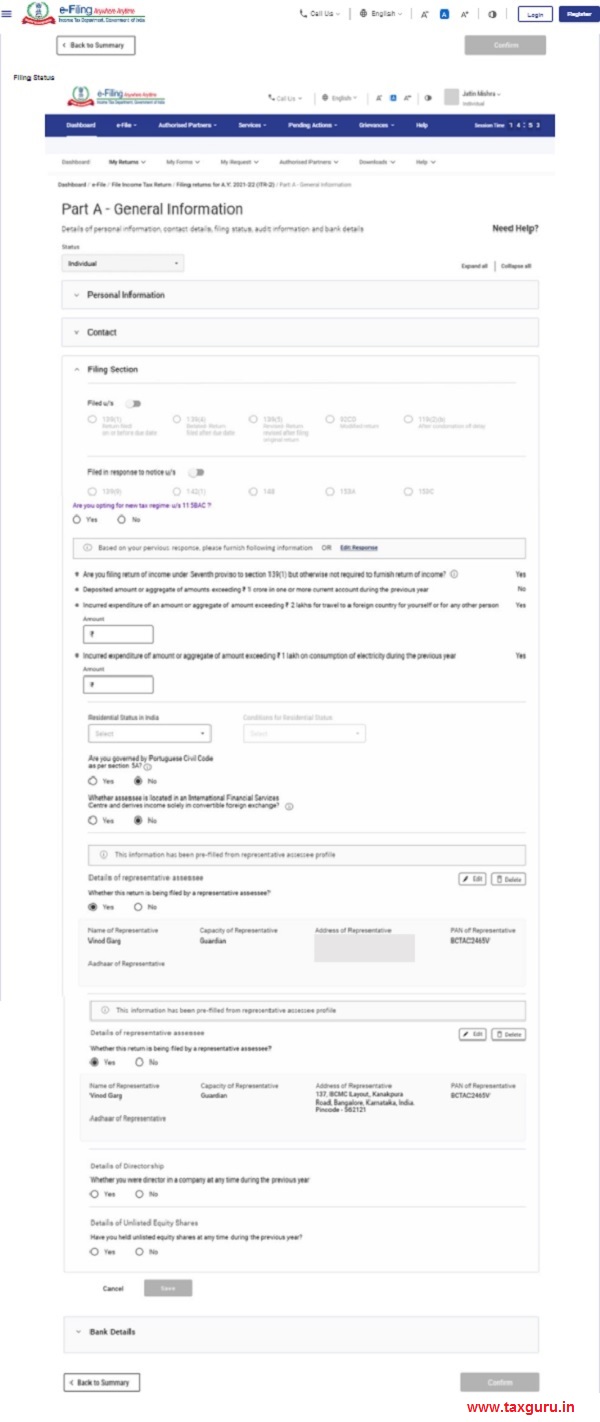

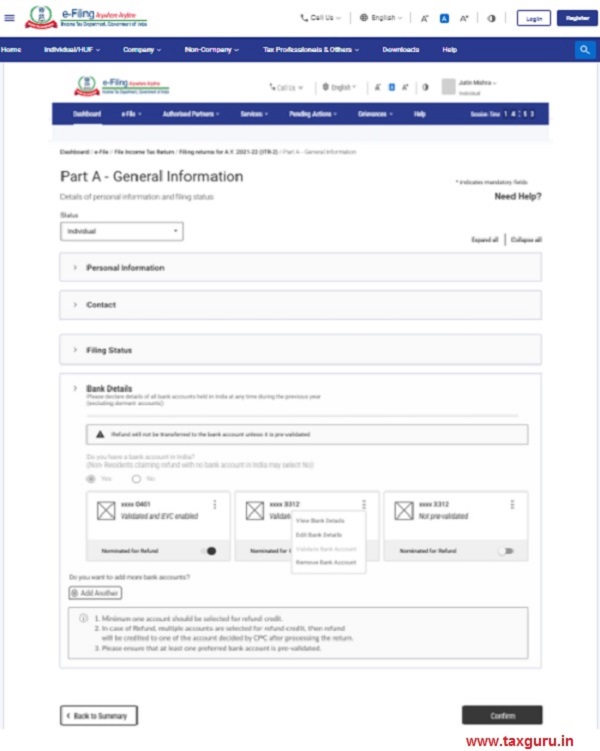

3.1 Part A General

In the Part A General section of the form, you need to verify the pre-filled data from your e-Filing profile. You will not be able to edit some of your personal data directly in the form. However, you can make the necessary changes by going to your e-Filing profile. You can edit your contact details, filing status, residential status and bank details in the form itself.

Personal Information

Contact Details

Filing Status

Bank Details

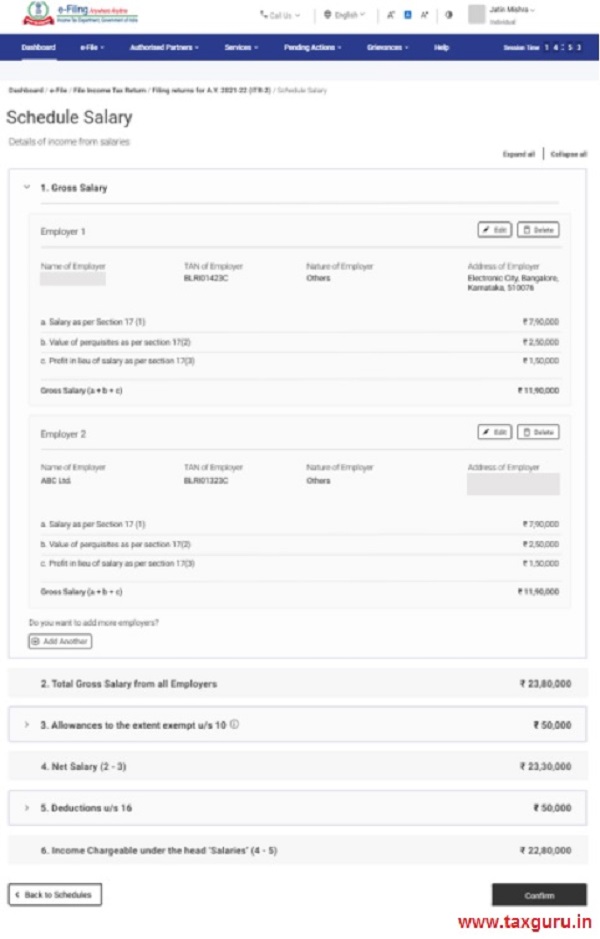

3.2 Schedule Salary

In Schedule Salary, you need to review / enter / edit details of your income from salary / pension, exempt allowances and deductions u/s 16.

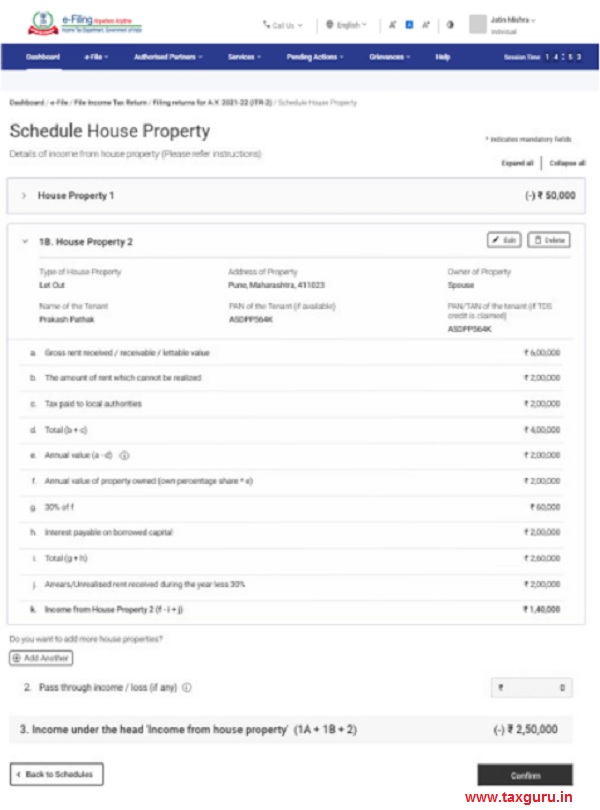

3.3 Schedule House Property

In Schedule House Property, you need to review / enter / edit details relating to house property (self-occupied, let out, or deemed let out). The details include co-owner details, tenant details, rent, interest, pass through income etc.

3.4 Schedule CG – Capital Gains

Capital Gains arising from sale / transfer of different types of capital assets have been segregated. In a case where capital gains arises from sale or transfer of more than one capital asset, which are of same type, please make a consolidated computation of capital gains in respect of all such capital assets of same type. But in case of transfer of land / building, it is mandatory to enter the computation towards each land / building. In Schedule Capital Gains, you need to enter details of your Short-Term and Long-Term Capital Gains / Losses for all types of Capital Assets owned.

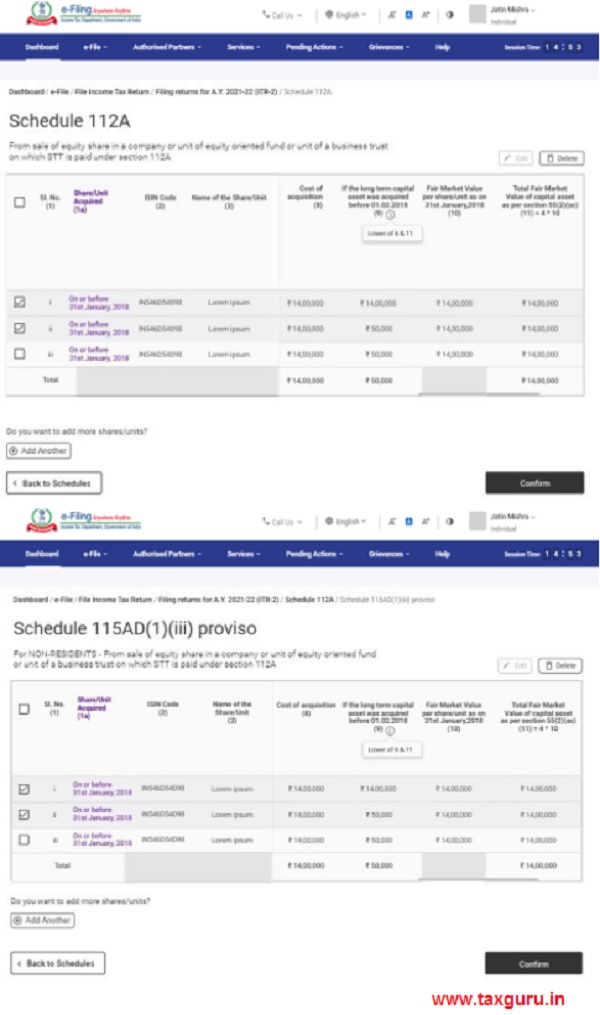

3.5 Schedule 112A and Schedule-115AD(1)(iii) proviso

- In Schedule 112A, you need to review / enter / edit details about sale of equity shares of a company, an equity-oriented fund, or a unit of a business trust on which STT is paid.

- Schedule 115AD (1)(iii) proviso involves entering the same details as for Schedule 112A but is applicable to non-residents.

Note: If Shares are bought on or before 31st Janurary.2018, it is mandatory to enter Scrip-wise details of each transfer under Schedule 112A and Schedule-115AD(1)(iii) proviso.

3.6 Schedule Other Sources

In Schedule Other Sources section, you need to review / enter / edit details of all your income from other sources, including (but not limited to) income charged at special rates, deductions u/s 57 and income involving race horses.

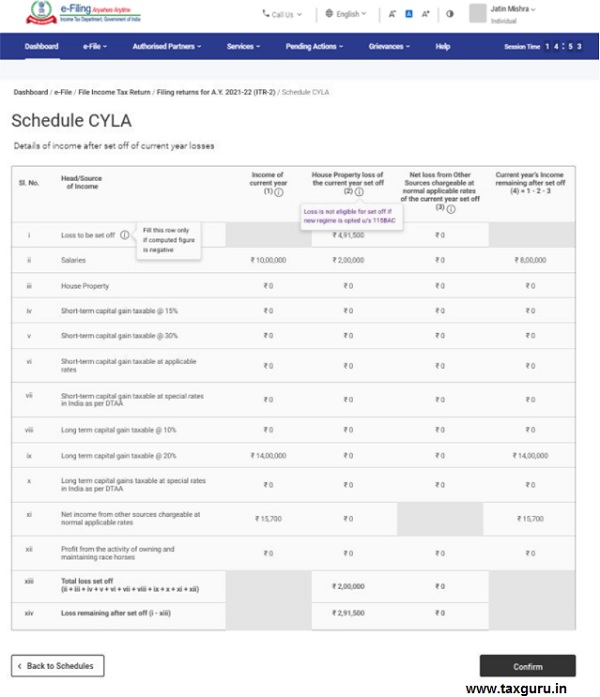

3.7 Schedule Schedule Current Year’s Loss Adjustment (CYLA)

In Schedule Current Year’s Loss Aidjustment (CYLA), you will be able to view details of income after set-off of current year losses. The unabsorbed losses allowed to be carried forward out of ths are taken to Schedule CFL for carry forward to future years.

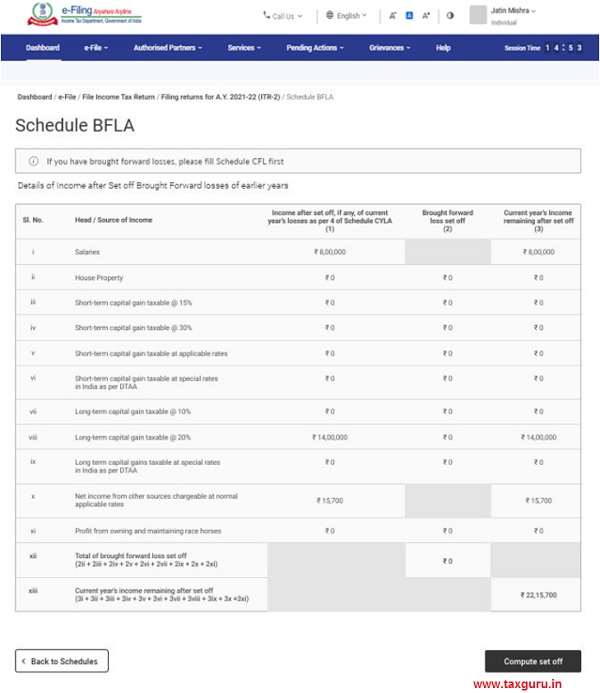

3.8 Schedule Schedule Brought Forward Loss Adjustment (BFLA)

In Schedule Brought Forward Loss Adjustment (BFLA), you can view the details of income after set-off of brought forward losses of earlier years.

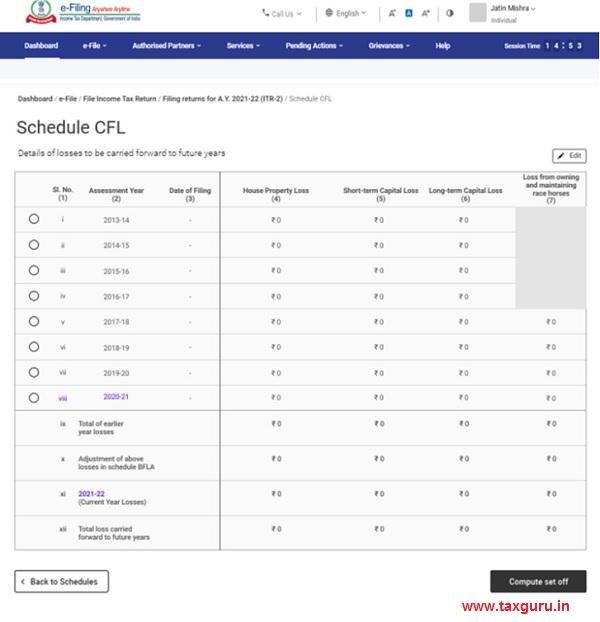

3.9 Schedule Schedule Carry Forward Losses (CFL)

In Schedule Carry Forward Losses (CFL), you can view the details of losses to be carried forward to future years.

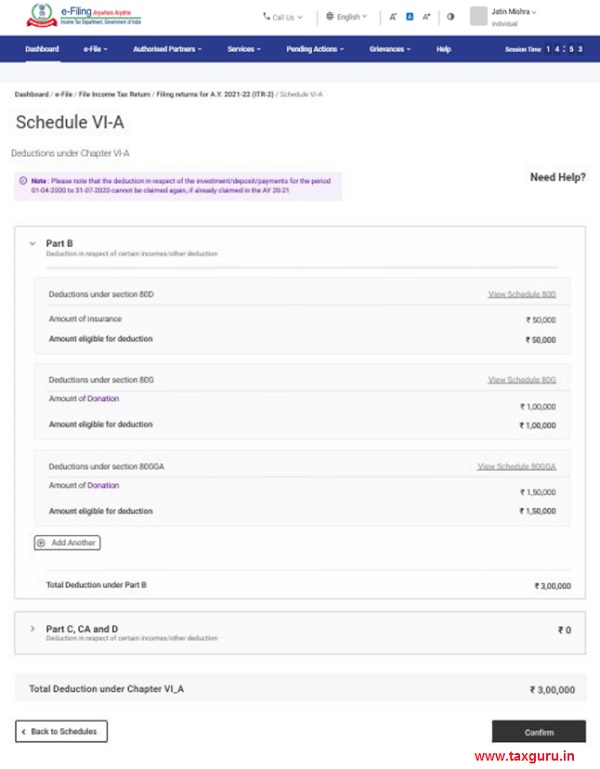

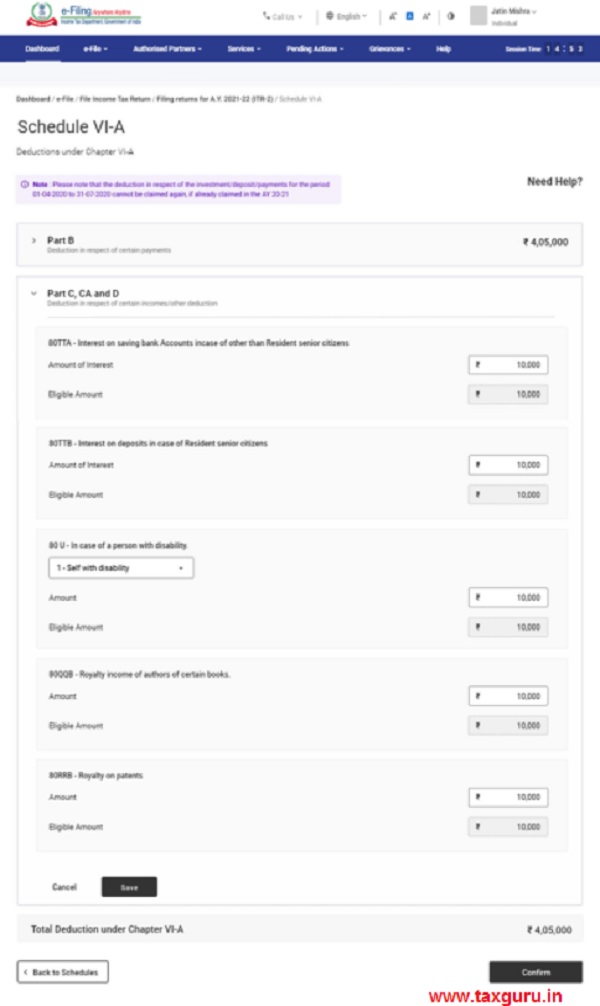

3.10 Schedule VI-A

In the Schedule VI-A, you need to add and verify any deductions you need to claim under Section 80 – Parts B, C, CA, and D (subsections as specified below) of the Income Tax Act.

Note: Please note that the deduction in respect of the investment/ deposit/ payments for the period 1st April 2020 to 31st July 2020 cannot be claimed again, if already claimed in the AY 20-21.

Part A – Deduction in respect of certain payments

Part C, CA and D – Deduction in respect of other income / deductions

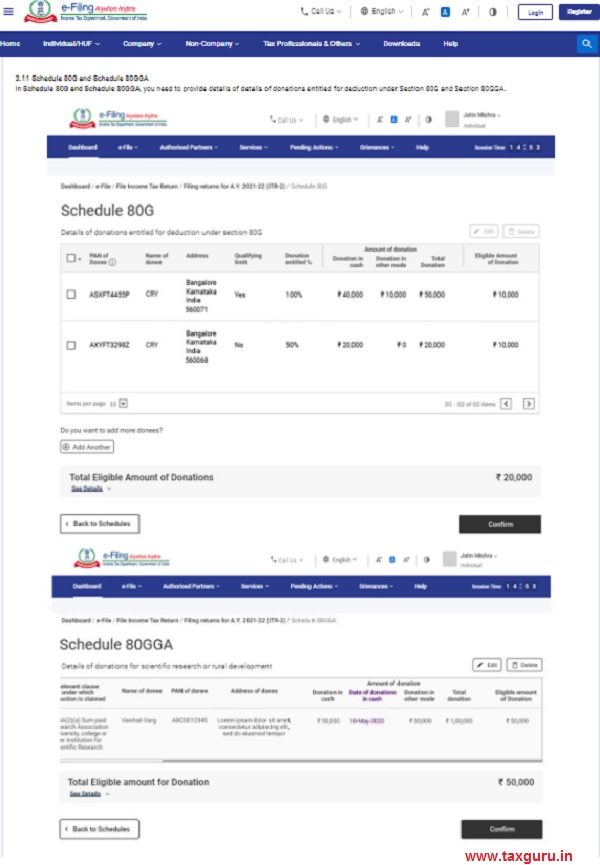

3.11 Schedule 80G and Schedule 80GGA

In Schedule 80G and Schedule 80GGA, you need to provide details of details of donations entitled for deduction under Section 80G and Section 80GGA.

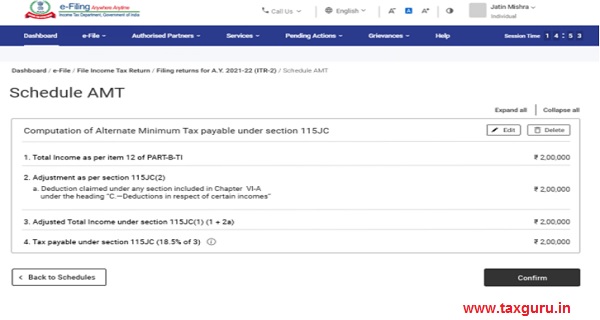

3.12 Schedule AMT

In Schedule AMT, you need to confirm the computation of Alternate Minimum Tax payable u/s 115JC.

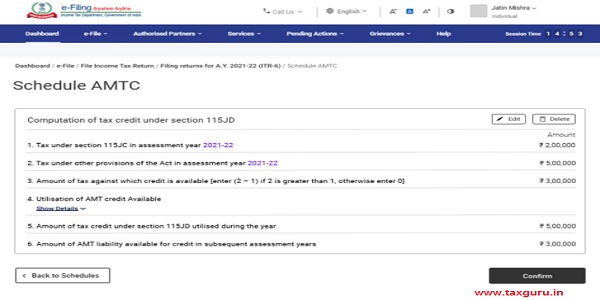

3.13 Schedule AMTC

In Schedule AMTC, you need to add details of tax credits u/s 115JD.

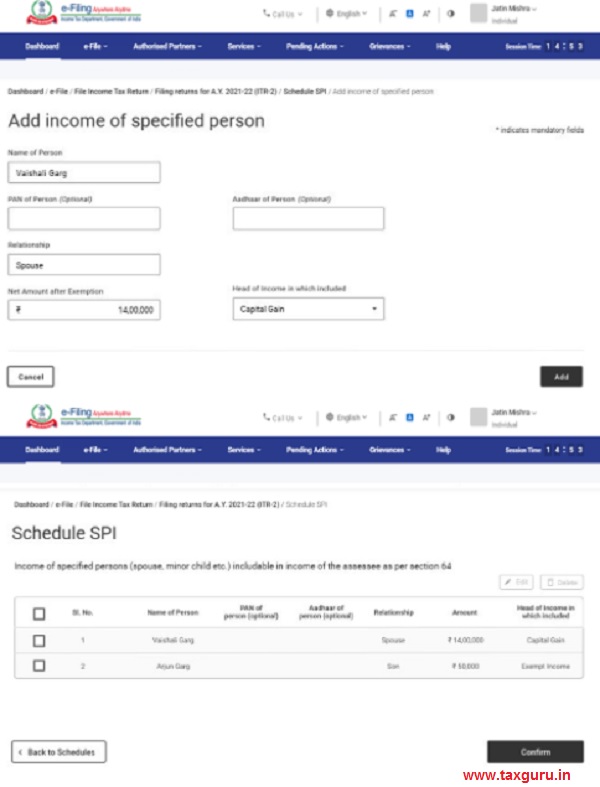

3.14 Schedule SPI

In Schedule SPI, you need to add the income of specified persons (e.g. spouse, minor child) that is includable or required to be clubbed with your income as per Section 64.

3.15 Schedule SI

In Schedule SI, you will be able to view the income that is chargeable to tax at special rates. The amount under various income types are taken from the amounts provided in the relevant Schedules i.e., Schedule OS, Schedule BFLA.

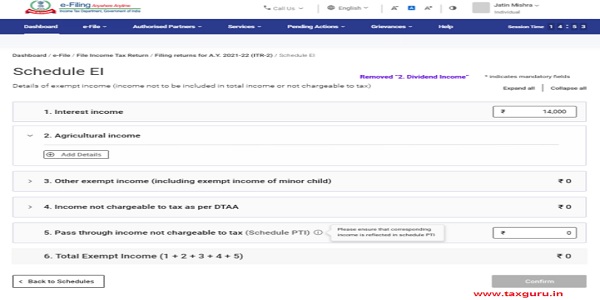

3.16 Schedule Exempt Income (EI)

In Schedule Exempt Income (EI), you need to provide your details of exempt income i.e., income not to be included in total income or not chargeable to tax. The income types included in this schedule include interest, dividend, agricultural income, any other exempt income, income not chargeable to tax through DTAA and pass through income which is not chargeable to tax.

3.17 Schedule Pass Through Income (PTI)

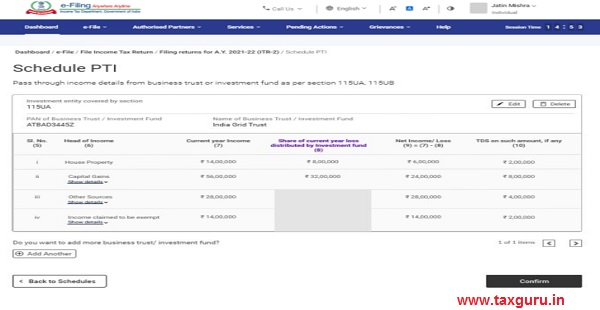

In Schedule Pass Through Income (PTI), you need to provide details of pass through income received from business trust or investment fund as referred to in section 115UA or 115UB.

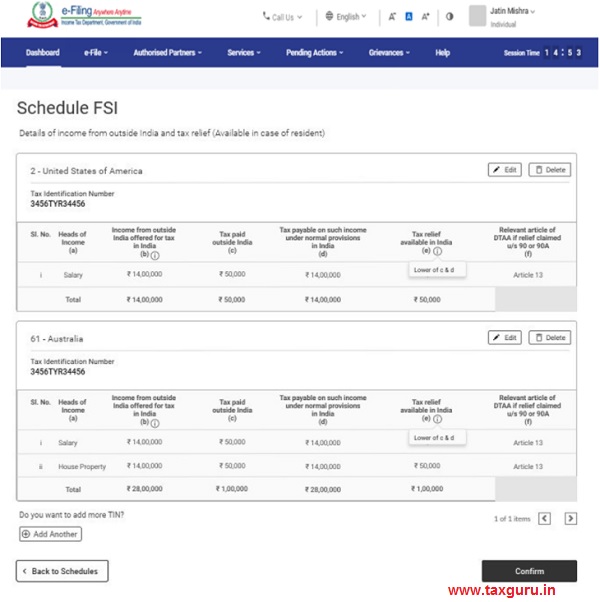

3.18 Schedule Foreign Source Income (FSI)

In Schedule Foreign Source Income (FSI), you need to report the details of income, which is accruing or arising from any source outside India. This schedule is available for residents only.

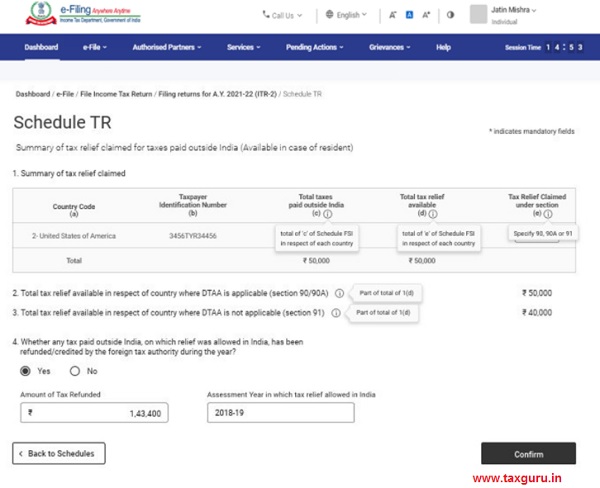

3.19 Schedule TR

In Schedule TR, you need to provide a summary of tax relief which is being claimed in India for taxes paid outside India in respect of each country. This schedule captures a summary of detailed information furnished in Schedule FSI.

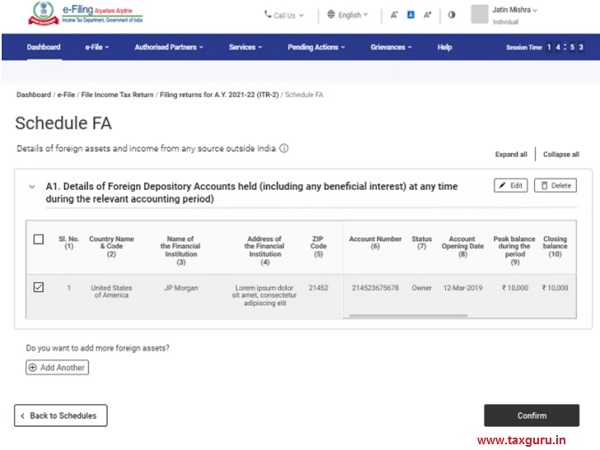

3.20 Schedule FA

In Schedule FA, you need to provide details of foreign asset or income from any source outside India. This schedule need not be filled up if you are Not Ordinarily Resident or a Non-Resident.

3.21 Schedule 5A

In Schedule 5A, you need to provide the information necessary for apportionment of income between husband and wife if you are governed by the system of community of property under the Portuguese Civil Code 1860.

3.22 Schedule AL

If your total income exceeds ₹50 lakh, it is mandatory to disclose the details of movable and immovable assets in Schedule AL along with liabilities incurred in relation to such assets. If you are a non-resident or resident but not ordinarily resident, only the details of assets located in India are to be mentioned.

3.23 Part B – Total Income (TI)

In the Part B –Total Income (TI) section, you will be able to view your computation of total income auto-populated from all the schedules you filled in the form.

3.24 Tax Paid

In the Tax Paid section, you need to verify your tax details as paid by you in the previous financial year. Tax details include TDS from Salary / TDS from Income Other than Salary, TCS, Advance Tax and Self-Assessment Tax.

3.25 Part B-TTI

In the Part B-TTI section, you will be able to view the overall computation of total income tax liability on total income.

Note: For more details, refer to the instructions to file ITR issued by CBDT for AY 2021-22.

4. How to Access and Submit ITR-2

You can file and submit your ITR through the following methods:

- Online Mode – through e-Filing portal

- Offline Mode – through Offline Utility

You can refer to the Offline Utility for ITRs user manual to learn more.

Follow the steps below to file and submit the ITR through online mode:

Step 1: Log in to the e-Filing portal using your user ID and password.

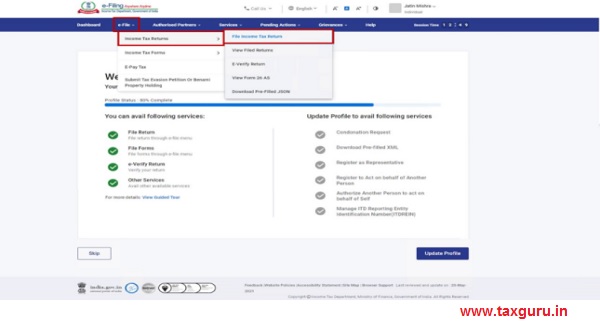

Step 2: On your Dashboard, click e-File > Income Tax Returns > File Income Tax Return.

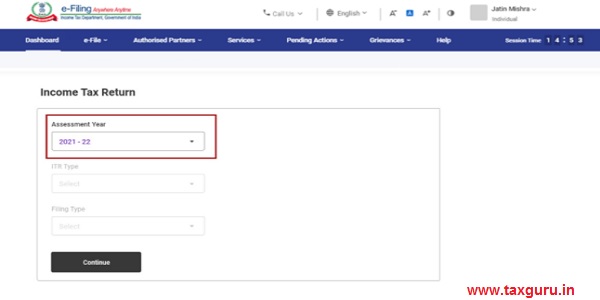

Step 3: Select Assessment Year as 2021 – 22 and click Continue.

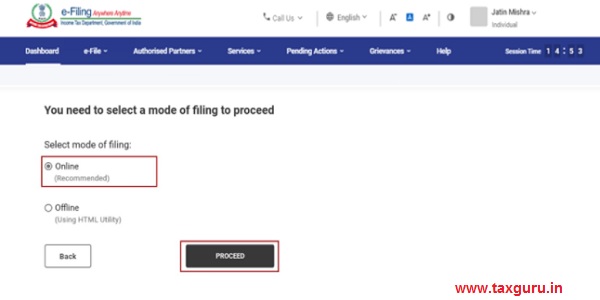

Step 4: Select Mode of Filing as Online and click Proceed.

Note: In case you have already filled the Income Tax Return and it is pending for submission, click Resume Filing. In case you wish to discard the saved return and start preparing the return afresh click Start New Filing.

Step 5: Select Status as applicable to you and click Continue to proceed further.

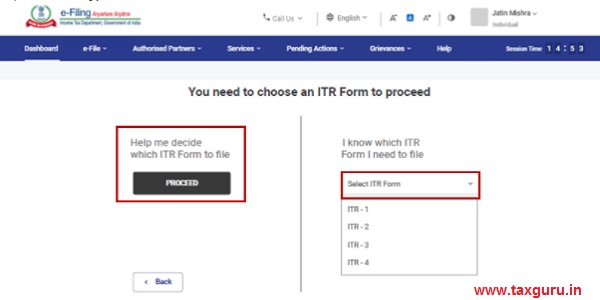

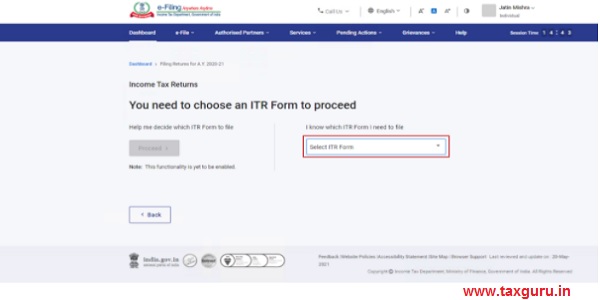

Step 6: You have two options to select the type of Income Tax Return:

- If you are not sure which ITR to file, you may select Help me decide which ITR Form to file and click Proceed. Once the system helps you determine the correct ITR, you can proceed with filing your ITR.

- If you are sure which ITR to file, select I know which ITR Form I need to file. Select the applicable Income Tax Return from the dropdown and click Proceed with ITR.

Note:

- In case you are not aware which ITR or schedules are applicable to you or income and deductions details, your answers in response to a set of questions will guide in determining the same and help you in correct / error free filing of ITR.

- In case you are aware of the ITR or schedules applicable to you or income and deduction details, you can skip these questions.

- Refer to the Identification and Generation of ITR for AY 21-22 user manual to learn more.

Step 7: Once you have selected the ITR applicable to you, note the list of documents needed and click Let’s Get Started.

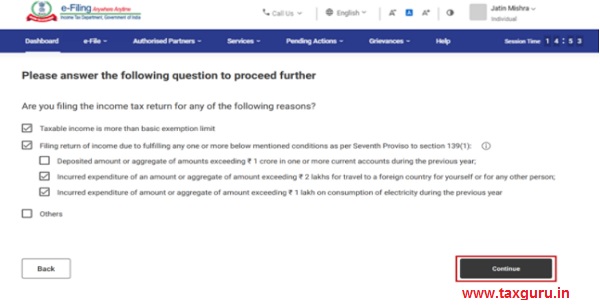

Step 8: Select the checkboxes applicable to you and click Continue.

Step 9: Review your pre-filled data and edit it if necessary. Enter the remaining / additional data (if required). Click Confirm at the end of each section.

Step 10: Enter your income and deduction details in the different section. After completing and confirming all the sections of the form, click Proceed.

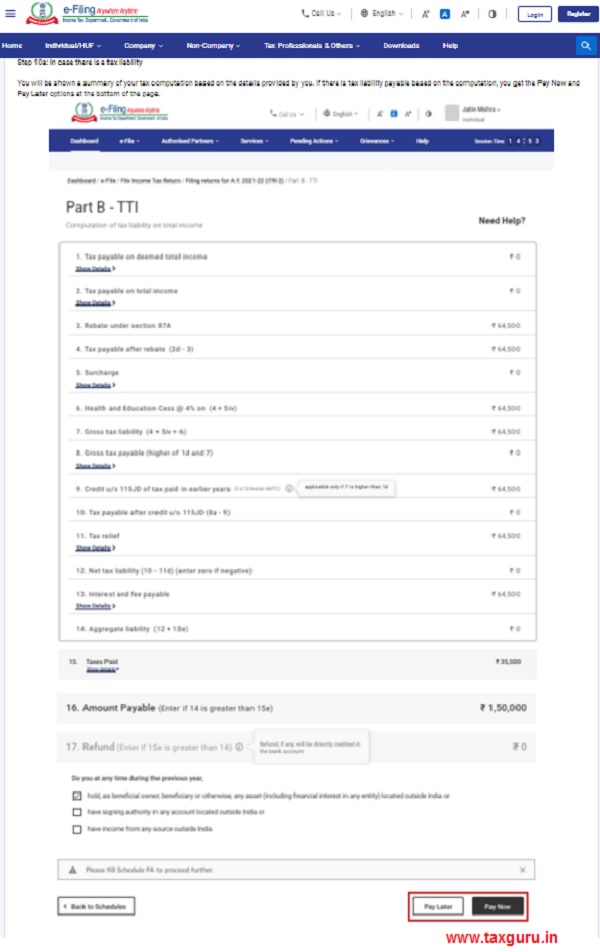

Step 10a: In case there is a tax liability

You will be shown a summary of your tax computation based on the details provided by you. If there is tax liability payable based on the computation, you get the Pay Now and Pay Later options at the bottom of the page.

Note:

- It is recommended to use the Pay Now option. Carefully note the BSR Code and Challan Serial Number and enter them in the details of payment.

- If you opt to Pay Later, you can make the payment after filing your Income Tax Return, but there is a risk of being considered as an assessee in default, and liability to pay interest on tax payable may arise.

Step 10b: In case there is no tax liability (No Demand / No Refund) or if you are eligible for a Refund

After paying tax, click Preview Return. If there is no tax liability payable, or if there is a refund based on tax computation, you will be taken to the Preview and Submit Your Return page.

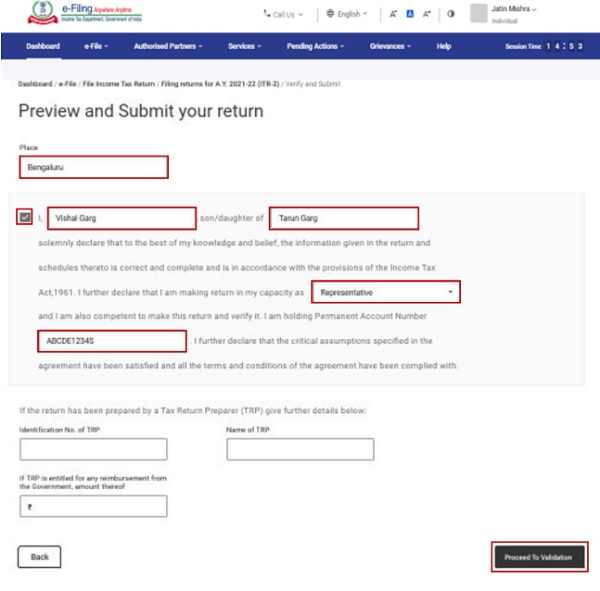

Step 11: On the Preview and Submit Your Return page, enter Place, select the declaration checkbox and click Proceed to Validation.

Note: If you have not involved a tax return preparer or TRP in preparing your return, you can leave the textboxes related to TRP blank.

Step 12: Once validated, on your Preview and Submit your Return page, click Proceed to Verification.

Note: If you are shown a list of errors in your return, you need to go back to the form to correct the errors. If there are no errors, you can proceed to e-Verify your return by clicking Proceed to Verification.

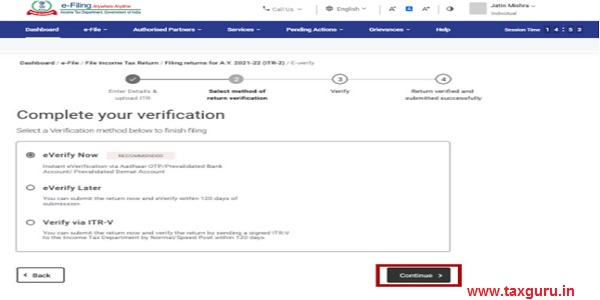

Step 13: On the Complete your Verification page, select your preferred option and click Continue.

It is mandatory to verify your return, and e-Verification (recommended option – e-Verify Now) is the easiest way to verify your ITR – it is quick, paperless, and safer than sending a signed physical ITR-V to CPC by post.

Note: In case you select e-Verify Later, you can submit your return, however, you will be required to verify your return within 120 days of filing of your ITR.

Step 14: On the e-Verify page, select the option through which you want to e-Verify the return and click Continue.

Note:

- Refer to How to e-Verifyuser manual to learn more.

- If you select Verify via ITR-V, you need to send a signed physical copy of your ITR-V to Centralized Processing Center, Income Tax Department, Bengaluru 560500 by normal / speed post within 120 days.

- Please make sure you have pre-validated your bank account so that any refunds due maybe credited to your bank account.

- Refer to My Bank Account user manual to learn more.

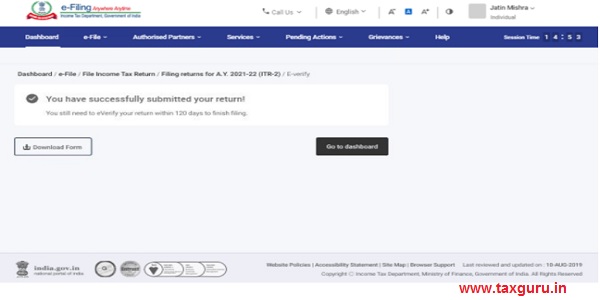

Once you e-Verify your return, a success message is displayed along with the Transaction ID and Acknowledgment Number. You will also receive a confirmation message on your mobile number and email ID registered on the e-Filing portal.

In ITR-2 form select schedule – inside other schedules below schedules are already selected and it is not required for me but I am not able to unselect/delete these schedule. So is it mandatory to fill? If yes then how can we fill or we just submit and confirm it without any value. Please advise.

In Other tab below are schedules-

Schedule CYLA

Schedule CFL

Schedule BFLA

Schedule AMT

Schedule AMTC

After struggling for hours to fill up the schedules, all my data were showing zeroes after I clicked on “compute” in Schedule BFLA.

Even the TDS and self assessment taxes which were picked up correctly earlier showing zero.

Very frustrating.

The new Income Tax offline utility for ITR2 is not considering 1 Lac exemption against LTCG against sale of Equity MF units. More so, Tax rate as per slab is being applied instead. Same with online. Is this a common issue ?

I am facing same problem as yours LTCG on equities are taxed @10% but as per 112A LTCG less than 1 lakh should not be taxed

Sir, my LTCG for previous year 2020-21 is less than 15000 which is add in 112A in the new utility but he tax is charged @30 slab which is at actual rate. LTCG below 1 lakh is exempted but any idea why the new utility is not considering.

Very same problem I am also facing in ITR-2.

LTCG is less than 1 lakh, it is being calculated correctly by IT portal , it but Utility not allowing for this exemption and computing tax on the amount

I am not finding Schedule EI in ITR-2 downloaded thru Utility software

Don’t you feel FM should give 10K as bonus to all IT filling individual for struggling to solve return filing puzzle? Every year the story is same. When can this issues be fixed for once and all.

You pay tax and also buy headache for solving filing issues every year?

I also feel the same, there should be special tax reduction for struggling multiple times with multiple ongoing problems with the new Portal . Don’t know if Infosys had experienced Tax CA on team to correctly reflect the new changed IT rules, or is using tapayers to do the job

Getting error report after validation saying CG Table F sr.no.3 break up for all quarters not not equal to value from item 3v of schedule BFLA.

On Checking BLFA values found to be correct.

Please suggest

I am having the same problem with the FA Schedule which is not applicable for Non Residents.. but it does not permit one to go forward. If you click on the schedule it says ‘Not applicable for you’. Need someone to attend to calls.. so that we can solve our problems.

I am facing two problems while filling up ITR2

1. In Schedule TTI last row, despite checking the box with ‘NO’ with regard to foreign assets, foreign income etc. at the time of previewing the return, it automatically populates as ‘YES’ in the check box and asking me to fill up Schedule FA. I took up the matter with CPC who confirmed that there is a technical glitch and will be rectified. But the issue remains even though more than 10 days have passed

2. Today, I noticed in the Desk top Utility that in Schedule TTI, an amount of Rs.5000 has been charged towards penalty under section 234F. Unable to understand why this has been charged despite the Govt. extending the date of filing the return to 30th Sept 2021. Also, there are no taxes due from me for AY 2021-22. There appears to be a technical glitch in this also.

Can anyone clarify on this ? Thank you.

Sir, ITR2 for AY 2021-22 link is not activated. Pl inform me the date.

we need help in resolving validation errors in various schedules. In my case in ITR2 it says enter figure in CYLA schedule at Sl 2xiii equal to summation of 2 ii to xii. but the cyla is only for viewing. not able to correct.

Am a senior citizen. can anyone help ?

i am a central govt employees and hence my salary being credited in banks and i have income from savings bank account and fixed deposit besides salary. i owned single house on which home loan taken. please suggest which is the correct form for itr filling. regards

The TDS fileds populated from pre0-filled data does not contain TAN details and i am asked to fill that manually. previous year this details were automatically filled in previous years .

is this a bug?

i tax department expects some phone numbers in my bank account and in my income tax records

if this is different the validation fails.

is there a remedy for this?

the amount of TDS as per tds is , say, 12000.

the prefilled TDS shows only 1000 rs

i tried to edit the values but the form shows 200 will be carried forward to next year.

is this a bug?

How to save the half (partly filled) ITR2 to continue after one or two days.?

In itr 2 , when entering the pension amount, the message props up to show the break up, which was not the case in the previous year. The problem is we get the pension after the

commuted deduction is deducted from the actual pension. And there is no provision to show this deduction. As a result the pension shown in the system is more than the actual pension received

Dear Sir, While submitting ITR 2, I am getting an Error message : In Schedule OS, Sl. No. 10 the quartely break up of Dividend Income (i ii iii iv v) is not equal to [1a – DTAA Dividend -System calculated value at 3aii] of Schedule OS” Also another problem I am facing is that in Schedule TTI, clause 19 : Do you at any time during the prev year….! I am selecting checkbox ‘No’ but in summary the checkbox get automatically change to “Yes”. Can you please help me what could be the problem. The online utility indicates no error on validation. However, this error pops up while verification.

Yes Sir, after validation successful and proceeding to verification, this verifications error message pops up. It would be a great help you can suggest the solutions. Thanks

I have the same two issues and I do not know how to fix them. I have struggled for 2 days to find a solution but could not do so. Can someone help?

While filing return while entering the tax deducted TDS for fin year it is not reflecting in proper column and instead it is reflecting in column no 13 which is for carried forward. It is also not taking automatic from 26 As not allowing manual filling pl guide

I am facing a similar problem

yes same problem for everyone, infosys has to solve the problem on priority

I am unable to e-verify ITR 2. I am filling it as KARTA of HUF but at e-verification error says that PAN of representative assessee and PAN of person uploading the return are different.. For ay 20200–21 I submitted itr 2 as KARTA of HUF.

While submitting ITR 2, I am getting an Error message : In Schedule OS, Sl. No. 10 the quartely break up of Dividend Income (i ii iii iv v) is not equal to [1a – DTAA Dividend -System calculated value at 3aii] of Schedule OS”

Also another problem I am facing is that in Schedule TTI, clause 19 : Do you at any time during the prev year….! I am selecting checkbox ‘No’ but in summary the checkbox get automatically change to “Yes”. Can anybody help me what could be the problem

I too have a similar problem. The ironical part is that the online utility indicates no error on validation. However, this error pops up while verification.

Dear Sir,

LTCG under sec 112A for FY 2020-2021 is less than 1 lakh is not taxable income. Can this amount be deducted from Total Income (Example Total income inclusive of LTCG sec 112A RS 530000 – LTCG sec112A Rs 30000 = Rs 500000)in order to get eligibility of sec 87A

Dividend income is now taxable in the hands of recipient

The so called new IT system implemented for filing Income Tax needs to be made user friendly.Thete are empteen number of glitches.Certsinly made more difficult for e filing by general public May require expertise unless made simple and user friendly.

sorry to say ITR 2 filing online is not applicable ..the website is not showing itr 2 online..the reply from ITR section also mentioned it is not available online

There is no mention by you of Agricultural Income exceeding ₹5000/- p.a. Earlier, it used to be reflected in Schedule AI. Is it required to be shown in Schedule OS? Pl. clarify and also throw some light as to how to use offline utility for filing ITR-2.

Very detailed and neatly explained all the steps.

I need jobs

Sir, ITR for the AY 2021-22 link was not activated pl inform me to the date of activation.

Very exhaustive and good information.will help in preparing off line itr2 utility