Advance tax, as the name suggests, is nothing but taxes paid in advance on the estimated annual income. Advance tax, along with tax deducted at source (TDS) and self-assessment tax, constitute the three means by which income taxes are collected by the government. Since the government machinery needs constant flow of funds, it cannot wait till the year end for tax payers to compute their income and then pay taxes, hence the provisions for advance tax forms part of the Income Tax Act.

Advance tax needs to be paid by all individuals, irrespective of whether they are consultants, businessmen or salaried. However, the liability to pay advance tax arises only if the tax payable (after taking the benefit of TDS and other prescribed credits) is Rs 10,000 or more.

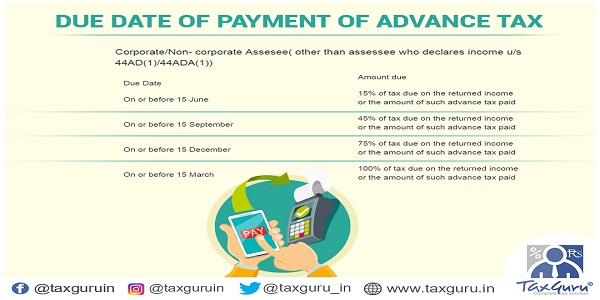

Due Date Of Payment Of Advance Tax

| Corporate/Non- corporate Assesee( other than assessee who declares income u/s 44AD(1)/44ADA(1)) | |

| Due Date | Amount due |

| On or before 15 June | 15% of tax due on the returned income or the amount of such advance tax paid |

| On or before 15 September | 45% of tax due on the returned income or the amount of such advance tax paid |

| On or before 15 December | 75% of tax due on the returned income or the amount of such advance tax paid |

| On or before 15 March | 100% of tax due on the returned income or the amount of such advance tax paid |

Wef A.y 2017-18: The assessee who declares income under Section 44AD(1)/44ADA(1) should pay pay the entire tax (100%) as advance tax on or before 15th march.If there is any shortfall, interest shall be levied simple interest@1% per month or part of the month on the short amount.

However if the advance tax paid by the assessee on the current income, on or before the 15th day of June or the 15th day of September is not less than twelve per cent or, thirty-six per cent respectively of the tax due on the returned income, then, the assessee shall not be liable to pay any interest on the amount of the shortfall on those dates. Also any amount paid by way of Advance Tax on or before the 31st March of that year, is treated as Advance Tax Paid during that Financial Year.

Moreover, no interest is leviable if the short fall in payment of advance-tax is on account of under estimation or failure to estimate the amount of capital gains or any income from winnings from lotteries, crossword puzzles, races, and other games including an entertainment program on television or electronic mode, in which people compete to win prizes etc., and the assessee has paid the tax on such income as part of the remaining instalments of advance tax which are due or if no instalment is due, by 31st March, of the Financial Year.

Further as per section 207, a resident senior citizen (i.e., an individual of the age of 60 years or above) not having any income from business or profession is not liable to pay advance tax.Senior Citizens not having Business Income exempt From Advance tax

To illustrate, if the tax on total estimated income for the year is Rs 1,00,000 and taxes estimated to be deducted at source from this income is Rs 60,000, the amount payable as advance tax would be Rs 40,000.

Failure to pay or any delay in payment of advance tax as above attracts mandatory interest of 1% per month or part thereof.

In case of a salaried individual having no other sources of income, there is normally no need to worry on advance tax because his employer is obliged to deduct tax (payable on salary income after considering the deductions on account of investments) at source on his full salary.

The individual also has the option to declare any other income, for example rental income or capital gains, to his employer if he wants that income to be considered for deducting tax from his salary.

This saves the individual from the hassle of keeping track of the advance tax deadlines.

However, in case of an individual, having worked with two or more employers during the year, either parallel or sequentially, there may arise a situation that even in absence of any other income, the individual may be required to pay advance tax on his salary income.

This happens when, in absence of the details of salary earned from the other employer, the benefit of slab (Rs 2,50,000 for Individuals, and Rs 300000 for senior citizen and Rs. 500000 for Very Senior Citizens) is allowed by each employer separately.

At the time of final income and tax computation, where the benefit of slab is taken only once, some tax may become payable which will need to be paid as self-assessment tax before filing the return.

To conclude, salaried people who have switched jobs during the year should furnish the required income details to their subsequent employers so that correct taxes are deducted and there are no shortfalls at the year end.

Also Read:

- https://taxguru.in/income-tax/calculate-interest-234a-234b-234c-return-due-date-consequences-late-filing.html

- https://taxguru.in/income-tax/interest-payable-section-234a-234b-234c-income-tax-act1961.html

(Republished With Amendments)

Advance Tax NOT payable by Senior/Suoer Senior citizens

Advance Tax is not payable by Seior/Super Senior Citizens