Section 115BAA was introduced by way of a mid year budget in FY 2019-20 and is applicable to certain domestic companies from 1st April 2020. The new section gives a one-time option to Domestic Companies to pay tax on their taxable income at 22% (instead of 25%/30%) and additional surcharge of 10% irrespective of taxable income subject to certain conditions:

1. Deductions for SEZ Units u/s 10AA are not claimed

2. Additional depreciation for new Plant & Machinery u/s 32(1)(iia) is not claimed

3. Deduction on account of deposit into Tea Development Account and Site Restoration Fund under Sections 33AB and Section 33ABA are not claimed respectively

4. Weighted deductions for contribution/expenditure on scientific research u/s 35 are not claimed

5. Deduction in respect of expenditure on specified business u/s 35AD, investment in backward areas u/s 32AD, expenditure on agricultural extension projects u/s 35CCC and expenditure on certain skill development projects U/s 35CCD are not claimed

6. Chapter VIA C Deductions wrt certain incomes are not claimed

Additionally, any carry forward and set off of brought forward loss or depreciation allowances in respect of above provision are shall be not claimed as well. Also, a domestic company exercising this option should continue under same provision for all subsequent years.

This provision is also in line with the plan of phasing out of tax incentives and deductions by the Government. Minimum Alternative Tax provisions u/s 115JB is also not applicable upon opting for the taxation under Sec. 115BAA.

Section 115BAA restricts claiming of brought forward loss and unabsorbed depreciation on account of specific sections of the Act only (whether intentional or not). Hence, it can be inferred that normal business loss and unabsorbed depreciation can still be claimed by a company and there is no need to forego the same. Interestingly, situations can arise whereby a company neither pays tax under MAT (on account of non-applicability of 115JB) nor any normal tax on account of carry forward and set off of normal business loss/unabsorbed depreciation.

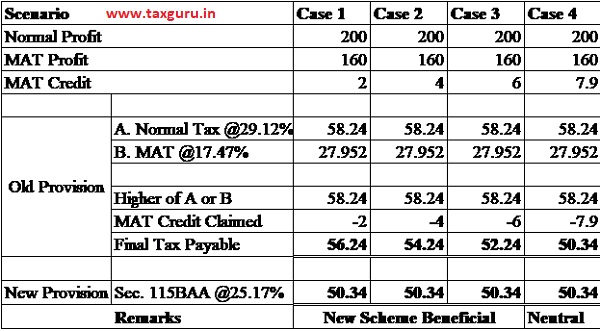

Since, MAT is not applicable for Companies opting for new regime, claiming MAT credit entitlement shall also be not available and they’d have to forego the same. Companies which already have MAT Credit entitlement in their Balancesheet will be posed with a question of whether to go for reduced tax (22%) under new provisions or to go with old tax regime (25%) and claiming the MAT credit. The effective tax rate after considering surcharge and cess will be 25.17% under Sec.115BAA and 26%/27.82%/29.12% under normal provisions. It is advisable to first see whether the old tax regime or the new one is beneficial and results in lower tax outflow. As a rule of thumb, if the MAT credit entitlement is lower than tax differential (0.83% [26%-25.17%]/2.65%[27.82%-25.17%]/ 3.92%[29.12%-25.17%]) on normal taxable income, it would be beneficial to go with new tax regime and vice versa.

A sample sensitivity analysis is below considering highest surcharge case under 25% tax rate (you may observe that as long as MAT credit entitlement is less than 200*3.92%, ie. 7.9, new regime will be more beneficial)

Hence, there is nothing wrong in going with the old scheme to use fully/exhaust to maximum extent the MAT credit available and then opt in for the new taxation regime. This being an irreversible decision, an assessee shall also look into the commercial impact of choosing the new regime – whether it plan for any SEZ unit in near future, or to start investing in new plant and machinery or backward area projects etc.