Chaos due to Clause 16(d) of Form No. 3CD and Possible Solutions both for the aggrieved people and for the CPC

In form no. 3CD (audit report form), clause 16(d) asks about the amount of any other item of income not credited to the profit and loss account.

In most of the cases, people don’t credit income from sources other than the source of business / profession to the profit and loss account and credit the same to the capital account. So, auditor reports those incomes at this clause no. 16(d). It doesn’t mean that those incomes have not been offered to tax under any of the remaining 4 heads of income also. Till A.Y. 2019-20, queries were not being raised in this matter by the CPC.

But, suddenly from A.Y. 2020-21, queries were started being raised by the CPC as under (Scenario 1 and 2) in the form of adjustment notices under section 143(1)(a) of the Income Tax Act, 1961.

Scenario – 1: If the auditor has reported some figure at clause no. 16(d) of Form no. 3CD, but nothing has been mentioned at point no. 5(d) of Schedule Part A : OI Other Information.

Queries are being raised by the CPC as under.

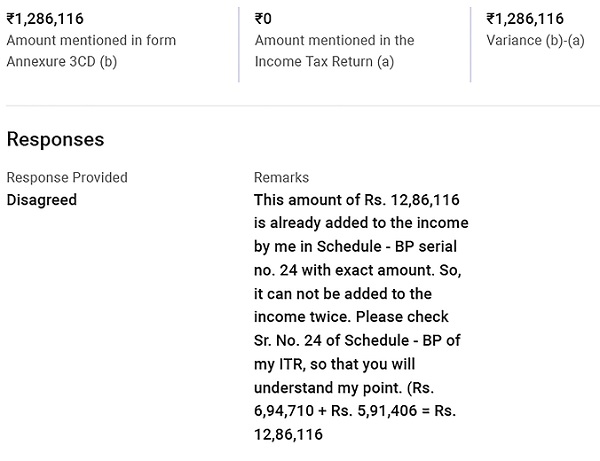

Suppose someone gives answer of this to CPC as under.

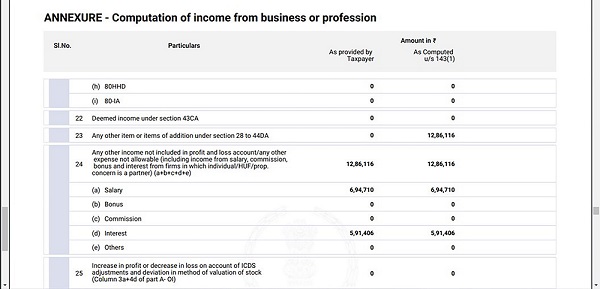

But even such well convincing answers are getting ignored and additions are being made to the income of those amounts which are already the part of income as under. (See row number 23 and 24, the same amount is counted twice as income in schedule – BP by CPC.

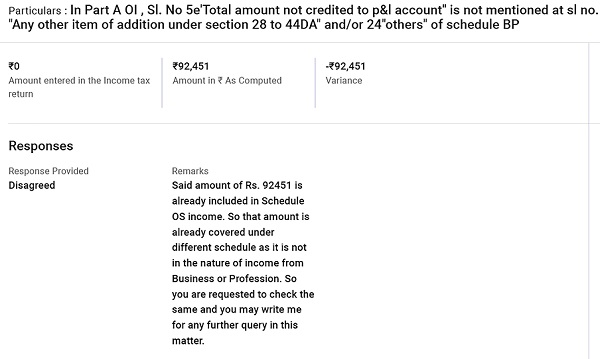

Scenario – 2: If the auditor has reported some figure at clause no. 16(d) of Form no. 3CD, and the same amount has been mentioned at point no. 5(d) of Schedule Part A : OI Other Information also. In this case, queries in the following manner are being raised by the CPC.

In short, form the behaviour of CPC as shown in scenario 1 and 2 above, it can be inferred by any prudent human being that CPC seems to be of the opinion that the amount which is not credited to the profit and loss account and reported at clause no. 16(d) of Form no. 3CD are forming part of income from the business or profession. In other words, one can interpret from this as – “there is no requirement to report any income at clause no. 16(d) of Form No. 3CD other than the income under the head of business profession!!!”. This seems incorrect when we read clause no. 16(d) of Form No. 3CD, but proves to be hundred percent correct when see the behaviour of CPC in above mentioned two scenarios.

Actually, CPC wants to assure itself whether any income mentioned in clause no. 16(d) of Form no. 3CD has escaped from tax. But the way it has chosen to assure this is totally unjustifiable as to the addition of each and everything under the head of business / profession as unreported income. This behaviour of CPC has become the curse for the genuine tax payers and the income tax consultants who have just reported the figure in good faith at clause no. 16(d) of Form no. 3CD and even covered those income at some or other head of income in ITR.

Now the question is what is the solution to this issue which can create a win-win situation both for the CPC and assessees.

Possible Solution for the CPC: Director General of Income Tax (Systems) must provide a drop-down menu in clause no. 16(d) of Form No. 3CD which contain the options of all heads of income. So that the auditor can report it with proper selection that the income is of the nature of this head and CPC’s system can compare the same with the amounts mentioned under those heads in ITR and get assured itself whether the income has escaped from the tax or not. This can be done from the A.Y. 2022-23, but what to do of such queries for earlier year like A.Y. 2021-22? Then again, the answer is The Director General of Income Tax (Systems) must provide a drop-down menu in response screen (response to adjustment notices under section 143(1)(a)), with which an assessee can explain to the system that the said amount is already covered under those heads of income in ITR. In rectification screen of portal also, box must be given to explain the stand of assessee to the department while submitting the rectification application with option “ Reprocess the return”.

Possible Solution for the assessee and the auditor: Until such drop-down menu is provided in form no. 3CD clause 16(d), only the income taxable under the head of business / profession and not credited to the profit and loss account should be reported in said clause and nothing else (as can be well interpreted from the behaviour of the CPC in above mentioned 2 scenarios). One can give even a note of such an understanding in form no. “3CB” as separate comment for clarification. But still there will remain a problem for the assessee to the extent the income from partnership firm to the partner which is credited to capital account and thus reportable at clause no. 16(d) of Form no. 3CD, as the CPC is adding such income at row no. 23 of Schedule – BP of ITR without checking the fact that the same has been already reported at row no. 24 of Schedule – BP of ITR (as has been shown in scenario -1 above). So, in such cases, rectification application can be filed with option “Reprocess the return”, as there is not any mistake on the part of assessee in the ITR. And not to forget to file Grievance as under.

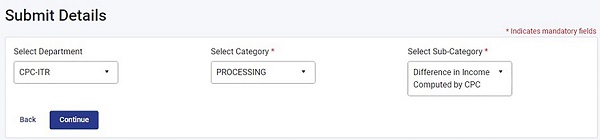

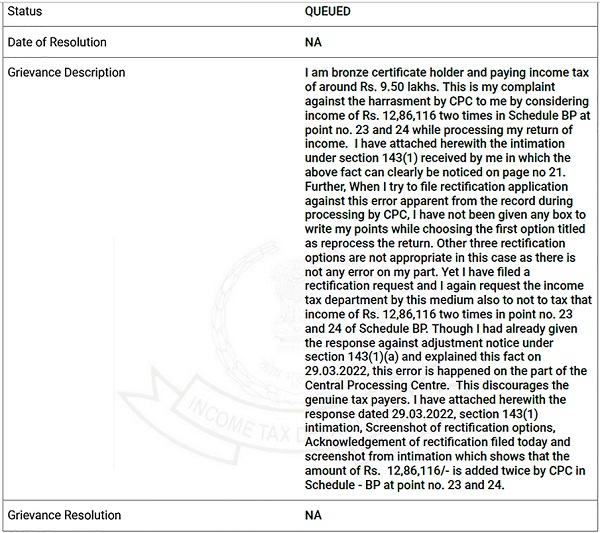

Specimen Grievance in this situation is as under.

Even it’s a duty of trade associations to report such matters to Finance Ministry and if the solution is not provided in time, then even reporting the matter to the PMO.

Disclaimer: This is not an opinion to anyone and author is / will not be responsible to anyone for any matter whatsoever regarding any reliance placed on this article and / or any action taken by anyone based on any matter written in this article. This is merely a genuine attempt to resolve this confusion which is of the great importance at present and wasting precious time of assessees and consultants in this hectic schedule of statutory deadlines.

Author Bio