Budget Analysis:

The Finance Budget 2016 has been passed in Lok Sabha on 05 May 2016 with few amendments. The president assented the finance bill on 14 May 2016. The following are the major highlights of Finance Act, 2016:-

Amendment in Direct Tax

1. Rate of surcharge has been increased from 12% to 15% if total income of an individual/HUF/AOP/BOI/trust exceeds Rs. 1 crore.

2. An additional tax at 10% shall be paid by a resident individual, HUF or a firm on gross amount of dividend, if such dividend received by them from a domestic company exceeds Rs. 10 lakhs per annum.

3. The Finance Bill, 2016 as passed by the Lok Sabha inserted a new clause to provide that the period of 36 months would be substituted with period of 24 months in case of unlisted shares. In other words, unlisted shares of company would be treated as short-term capital asset if it is held for a period of 24 months or less immediately preceding the date of its transfer.

4. Relief under Section 87A has been raised from 2,000 to Rs. 5,000 in order to provide for relief to small taxpayers. This relief is available to a resident individual if his/her total income is not more than Rs. 5,00,000.

5. Incase of domestic company, the rate of Income-tax shall be 29% of the total income if the total turnover or gross receipts of the company in the previous year 2015-16 does not exceed Rs. 5 crore and in all other cases the rate of Income-tax shall be 30% of the total income.

6. For the purpose of advance tax, to bring at par the non-corporate tax payers with corporate taxpayers, non-corporate tax payers shall be required to pay advance tax in four installments’, viz; 15%, 45%, 75% and 100% of tax on or before 15th June, 15th September, 15th December and 15th March respectively.

7. Advance tax provisions shall apply to assessees’ opting for presumptive taxation u/s 44AD and consequently interest on default and deferment of advance tax under section 234B and 234C respectively shall be levied.

8. TCS is to be levied at 1% in case of sale in cash of goods or services, if value there of exceeds Rs.2lakhs. Further, levy of TCS at 1% on sale of motor vehicle, if the value exceeds Rs. 10 Lakhs.

9. A new section 44ADA is introduced for computing professional income on presumptive basis at 50% of gross receipts if the receipts do not exceeds Rs. 50 Lakhs.

10. The limit of section 44AD is increased to 2 Crores.

11. Increase in the limit from Rs. 25 Lakhs to Rs. 50 Lakhs under section 44AB for requirement of audit for specified professionals.

12.In order to provide relief to newly setup domestic companies, the rate of tax shall be 25% if the following conditions are met:

a. the company has been setup and registered on or after 01-03-2016;

b. the company is engaged in the business of manufacture or production of any article or thing and is not engaged in any other business;

c. the company has not claimed any benefit under section 10AA, benefit of accelerated

d. depreciation, benefit of additional depreciation, investment allowance, expenditure on scientific research and any deduction in respect of certain income under Part-C of Chapter-VI-A other than the provisions of section 80JJAA; and

e. the option is furnished in the prescribed manner before the due date of furnishing of income.

13. Tax incentives for New startups is defined as below:

a. a deduction of 100% of the profits and gains derived by an eligible start-up from a business involving innovation development, deployment or commercialization of new products, processes or services driven by technology or intellectual property.

b. The benefit is available to all startups which is setup by 01-04-2019.

c. Section 54EE is introduced to provide exemption from capital gains tax if the Long term capital gains proceeds are invested by an assessee in units of such specified funds, as may be notified by the Central Government in this behalf and such amount remains invested for 3 years. The Investment in the units of the fund shall be allowed maximum up to Rs. 50 Lakhs.

14. In order to encourage indigenous research & development activities and to make India a global R & D hub, the government has decided that where income of the eligible assessee, who is the true and first inventor of the invention and whose name is entered on the patent register as the patentee in accordance with Patents Act, 1970, includes royalty in respect of such patent, the same shall be taxable at 10%(excluding SC, EC & SHEC) under section 115BBF.

15. With a large objective of ‘Housing for All’, the government has come up with amendment to provide 100% deduction of the profits of an assessee developing and building affordable housing projects if the housing project is approved by the competent authority before the 31-03-2019 subject to certain conditions which are as follows:

a. The project is completed within a period of 3 years from the date of approval,

b. The project is on a plot of land measuring not less than 1000 sq.metres where the project is within 25 km from the municipal limits of four metros namely Delhi, Mumbai, Chennai & Kolkata and in any other area, it is measuring not less than 2000 sq. metres where the size of the residential unit in the said areas is not more than thirty sq. metres and sixty sq. metres, respectively,

c. where residential unit is allotted to an individual, no such unit shall be allotted to him or any member of his family, etc

16. In furtherance to the goal of the Government of providing ‘housing for all’, the government has also incentivized first-home buyers availing home loans, by providing additional deduction in respect of interest on loan taken for residential house property from any financial institution up to Rs. 50,000 if the value of the house is less than Rs. 50 Lakhs and loan amount not exceeding Rs. 35 Lakhs has been sanctioned by the bank during 01-04-2016 to 31-03-2017. The benefit shall last till repayment of loan. This deduction will be over and above the limit of Rs. 2,00,000 as mentioned in Section 24(b).

17. In order to increase the employment opportunities, the government has come up with expansion of section 80JJAA to provide that the deduction under the said provisions shall be available in respect of cost incurred on any employee whose total emolument does not exceed Rs. 25,000 per month. No deduction, however, shall be allowed in respect of cost incurred on those employees, for whom the entire contribution under Employees’ Pension Scheme notified in accordance with Employees’ Provident Fund and Miscellaneous Provisions Act, 1952, is paid by the Government.

18. In order to provide relief to the individual tax payers, section 80GG (deduction for rent paid) has been amended so as to increase the maximum limit of deduction from existing Rs. 2,000 per month to Rs. 5,000 per month.

19. There is an amendment that any shares received by an individual or HUF as a consequence of demerger or amalgamation of a company shall not attract the provisions of clause (vii) of sub-section (2) of section 56.

20. In view of the fact that housing projects often take longer time for completion, therefore section 24(b) has been amended to provide that deduction on account of interest paid on housing loan shall be available if the acquisition or construction is completed within 5 years(as against current 3 years) from the end of the financial year in which loan was borrowed.

21. In order to reduce compliance burden, section 206AA has been amended so as to provide that the provisions of this section shall not apply to a non-resident, not being a company, or to a foreign company, in respect of any other payment, other than interest on bonds, subject to such conditions as may be prescribed. The government has not yet provided an condition to avail such benefit.

22. Now, the Non-compete fees and exclusivity rights shall also be taxed under “profits and gains from business and profession”.

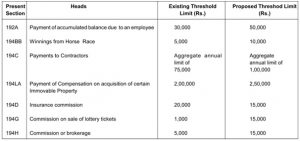

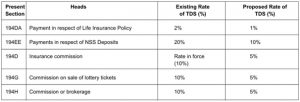

23. Amendment in TDS chapter are discussed below:

a. Change in threshold

b. Change in rates

b. Change in rates

24. Section 50C has been amended to provide that if the sale agreement is entered much before the actual date of transfer of the immovable property in which actual sale consideration is mentioned, then the stamp duty value as on the date of sale agreement shall be deemed to be full value of consideration.

25. In finance bill 2016, it was proposed that the contributions made on or after 01-04-2016 by an employee participating in recognized provident fund (RPF) or superannuation fund (SAF) up to 40% of accumulated balance on withdrawal shall be exempt. That means balance 60% shall be taxable on withdrawal except if the amount is annuitized. If annuitized, the regular pension received will be taxed and the tax liability will be deferred to next years. However, the government has rolled back such proposal in Finance Act 2016 passed in Lok sabha.

26. Any payment by NPS trust to an employee on account of closure of pension scheme, to the extent of 40% of accumulated balance, shall be exempt from tax. However, the whole amount received by nominee, on death of the assessee shall be exempt from tax.

27. If a person having income which is exempt u/s 10(38) and income of such person without giving effect to the said clause of section 10 exceeds the maximum amount which is not chargeable to tax, shall also be liable to file income tax return before the due date.

28. Time limit for filing belated return has also been reduced. In this regard, it has been provided that, any person who has not furnished a return within the time allowed to him under sub-section (1), may furnish the return for any previous year at any time before the end of the relevant assessment year or before the completion of the assessment, whichever is earlier.

29. Belated return can also be revised within such time as mentioned in section 139(5) of the Act.

30. Section 139(9) has also been amended so as to provide that a return shall not be regarded as defective merely because self-assessment tax and interest payable in accordance with the provisions of section 140A has not been paid on or before the due date of filing of return,

31. A return shall be processed u/s 143(1) prior to completion of assessment u/s 143(3), However, the finance bill as passed by the Lok Sabha provides that the processing of return is not necessary before the expiry of one year from the end of the financial year in which return is furnished, where a notice is issued for scrutiny assessment under Section 143(2).

32. Currently, the time limit for completion of assessment is two years from the end of assessment year in which the income was first assessable. Since the government is desirable that proceedings under the Act are finalized more expeditiously as digitization of processes within the Department will enhance its efficiency in handling workload. In order to simplify the provisions, the time limit has been rationalized to complete the assessments. It has been reduced by 3 months in each case. Eg. for completion of assessment under section 143 or section 144 be changed from existing 24 months(2 years) to 21 months from the end of the assessment year in which the income was first assessable,

33. Section 244A has also been amended so as to provide that in cases where the return is filed after the due date, the period for grant of interest on refund may begin from the date of filing of return. An additional interest on such refund amount, which arises out of appeal being delayed beyond the prescribed time, shall be calculated at the rate of 3% p.a., for the period beginning from the date following the date of expiry of the time allowed under sub-section (5) of section 153 to the date on which the refund is granted.

34. Section 271 shall not apply to and in relation to any assessment for the assessment year commencing on or after the 01-04-2017. Penalty shall be levied under the newly inserted section 270A w.e.f. 01-04-2017. The new section 270A provides for levy of penalty in cases of under reporting and misreporting of income.

35. It is also provided that an assessee may make an application to the Assessing Officer for grant of immunity from imposition of penalty under section 270A and initiation of proceedings under section 276C (prosecution), provided he pays the tax and interest payable as per the order of assessment or reassessment within the period specified in such notice of demand and does not prefer an appeal against such assessment order. The assessee can make such application within one month from the end of the month in which the order of assessment or reassessment is received in the form and manner, as may be prescribed.

36. The application of POEM has been deferred for one year more.

37. GAAR will apply from 01 April 2017.

38. Disallowance under section 14A will be limited to 1% of the average monthly value of the investments yielding exempt income, but not exceeding the actual expenditure under rule 8D.

Amendment in Service Tax& Excise

1. The facility for revision of return available to service tax assessees only, has been extended to manufacturers also.

2. Enabling provision is being made to levy Krishi Kalyan Cess (KKC) on all taxable services w.e.f. 01-06-2016, to finance and promote initiatives to improve agriculture @ 0.50%. The notification is still awaited.

3. The exemption on following services has been withdrawn–

a. Services by senior advocate(an advocate designated as Senior advocate by High Court of any state or Supreme court of India) to an advocate or firm of advocates providing legal services shall not be taxable @ 14%,

b. Service of construction, erection, commissioning or installation of original works pertaining to monorail or metro, in respect of contracts entered into on or after 01-03-2016 shall be taxable @ 5.60%,

c. Services of transport of passengers, with or without accompanied belongings, by ropeway, cable car or aerial tramway shall be taxable @ 14%,

d. Service Tax is being levied on transportation of passengers by air conditioned stage carriage with effect from 01-06-2016, at the same level of abatement as applicable to the transportation of passengers by a contract carriage, that is, 60% without credit of inputs, input services and capital goods.

4. The following are few services shall be new entry for exemption:

a. The services of general insurance business provided under ‘Niramaya’ Health Insurance scheme launched by National Trust for the Welfare of Persons with Autism, Cerebral Palsy, Mental Retardation and Multiple Disability in collaboration with private/public insurance companies are being exempted from Service Tax with effect from 1st April, 2016.

b. Services by way of construction etc. in respect of-

(i) housing projects under Housing For All (HFA) (Urban) Mission/Pradhan Mantri Awas Yojana (PMAY);

(ii) low cost houses upto a carpet area of 60square metres in a housing project under“ Affordable housing in Partnership” component of PMAY,

(iii) low cost houses upto a carpet area of 60 squaremetres in a housing project under any housing scheme of the State Government,

5. Services of construction provided to the government, a local authority in respect of construction of govt. schools, hospitals, etc. or construction of ports or airports,

6. The benefit of quarterly payment of Service Tax is being extended to ‘One Person Company’ (OPC) and HUF with effect from 01-04-2016.

7. Services provided by mutual fund agents to asset management company are being made taxable under forward charge with effect from 01-04-2016,

8. Interest rates on delayed payment of duty/tax across all indirect taxes are being rationalized and made uniform at 15% except where service tax collected but not deposited by exchequer interest rate will be 24% from the date service tax payment became due. Where value of taxable services in the preceding year/years covered by the notice is less than Rs. 60 Lakh, the rate of interest shall be 12%.

9. The rate of abatement in respect of services by way of construction of residential complex, building, civil structure, or part thereof, shall be 70% as against current(70%/75%) therefore new rate of tax shall be 4.20%,

10. The new rate of service tax in case of GTA services used for shifting of household goods shall be 5.60%. The existing rate of tax of 4.20% on transport of other goods by GTA continues unchanged.

11. Service tax on the services of Information Technology Software on media bearing RSP is being exempted from Service Tax with effect from 01-03-2016 provided Central Excise duty is paid on RSP,

12. Section 73 of the Finance Act, 1994 is being amended so as to increase the limitation period from 18 months to 30 months for short levy/non levy/short payment/non-payment/erroneous refund of Service Tax.

13. The power to arrest in Service Tax is being restricted only to situations where the tax payer has collected the tax but not deposited it to the exchequer, and that too above a threshold of Rs 2 crores. The monetary limit for launching prosecution is being increased from Rs.1 crore to Rs.2crores of Service tax evasion.

14. The finance act 2016 has also introduces annual returns for service tax and Cenvat credit which will be submitted to the department by 30th November of the following year.

15. Rate of interest on late deposit of service tax has been rationalized in the following manner:

| S.No | Particulars | Rate of interest(p.a.) |

| 1 | Collected any amount as service tax but failing to pay the amount so collected to the government on or before the due date | 24% |

| 2 | Other than above situation (In case of Reverse charges) | 15% |

The rate of interest shall be reduced by 3% if the gross receipts are less than Rs. 60 Lakhs.

(Author can be reached at csdiveshgoyal@gmail.com )

Author Bio

why point 5 should not be given the same treatment as point No 6 . i.e. to bring at par the non-corporate tax payers with corporate taxpayers