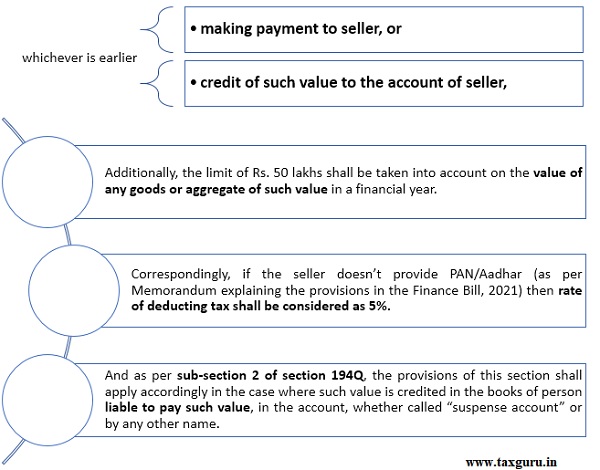

As per Section 194Q the buyer, whose turnover or gross receipts or total sales is exceeding Rs. 10 crores in a financial year immediately preceding the relevant financial year, shall be liable to deduct tax at rate of 0.1% on the value exceeding Rs. 50 lakhs at the time of: –

Section 194Q was introduced in the Budget of 2021-22 and has come into effect from 1st July, 2021. However, the CBDT has said that this provision would not be applicable on share or commodity transaction done through recognised stock exchange or cleared & settled by the recognised clearing corporation.

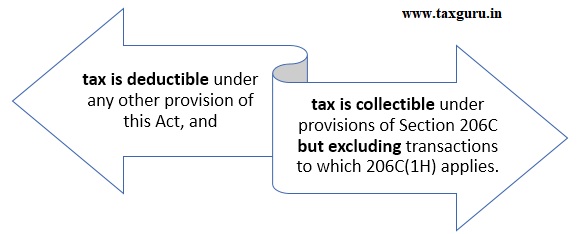

Likewise, as per sub-section 5 of section 194Q, the provisions of this section shall not apply to transactions on which: –

Therefore, provisions of Section 194Q shall apply on the transactions in the case of potential overlap between Section 194Q and Section 206C(1H).

Further clarifications

| 1. | Whether threshold limit be inclusive or exclusive of GST? | ♦ Threshold limit of Rs. 10 crores shall be exclusive of GST and Rs. 50 lakhs shall be inclusive of GST. |

| 2. | Which section will prevail for deducting/collecting tax in case of potential overlap between sections?

|

♦ No requirement of TDS u/s 194Q on a transaction where tax is deductible under any other provision or TCS is collectible under section 206C but excluding 206C(1H).

♦ TDS u/s 194Q shall prevail in case of potential overlap between TDS u/s 194Q and TCS u/s 206C(1H). Therefore, both TDS u/s 194Q and TCS u/s 206C(1H) will not apply on the same transaction. |

| 3. | Are capital goods also covered under this provision?

|

♦ Yes, any good whose value or aggregate of such value is exceeding Rs. 50 lakhs in a financial year.

♦ The Income Tax Act,1961 does not define the term “goods” so one may have to draw reference from the definition under the Sale of Goods Act, 1930 wherein stock and shares are inclusive while defining the term “goods”. ♦ Nevertheless, the CBDT has said that this provision would not be applicable on share or commodity transaction done through recognised stock exchange. |

| 4. | From when this section is applicable and what about the transactions prior to its applicability?

|

♦ This Section shall be applicable with effect from 1st July, 2021.

♦ Since the threshold of Rs. 50 lakh is with respect to a financial year where calculation of sum for checking applicability of this section shall be computed from 1st April, 2021. ♦ Hence, if a person being buyer has already credited or paid Rs. 50 lakhs or more up to 30th June, 2021 to a seller, then provisions of Section 194Q shall apply on all credit or payment during the financial year, on or after 1st July, 2021. |

| 5. | What is time limit for deduction of TDS under section 194Q?

|

♦ Tax to be deducted at the earliest of the following dates:

♦ time of credit of such value to the account of the seller, or ♦ time of payment. |

******

About the Author

Author is Ruchika Bhagat, FCA helping foreign companies in setting up and closure of business in India and complying with various tax laws applicable to foreign companies while establishing a business in India. Neeraj Bhagat & Co. Chartered Accountants, is a well-established Chartered Accountancy firm founded in the year 1997 with its head office at New Delhi.