Will threshold limit of 5 crore as mentioned in 44AB applicable for AY 2020-21?

Yes, it will be applicable.

NOTE: The discussion in article is only w.r.t Tax Audit for person carrying on Business.

FACTS:

1) Before amendment, applicable limit u/s 44AB for getting Tax Audit done is 1 crore.

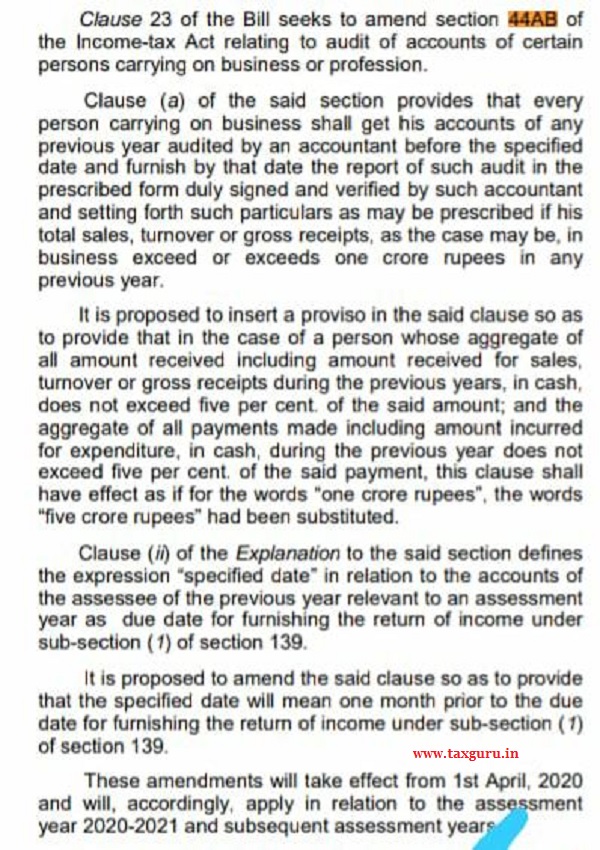

44AB clause a in FA 2019

(a) carrying on business shall, if his total sales, turnover or gross receipts, as the case may be, in business exceed or exceeds one crore rupees in any previous year

2) ‘Clause a’ of section 44AB was amended by Finance Act No. 12 of 2020 with an insertion of proviso . Such amendment is effective from 01-04-2020.

Extract of section 44AB was amended by Finance Act No. 12 of 2020 is as follows:-

Income Tax Department

Section – 44AB, Income-tax Act, 1961-2020

Audit of accounts of certain persons carrying on business or profession.

44AB. Every person,—

(a) carrying on business shall, if his total sales, turnover or gross receipts, as the case may be, in business exceed or exceeds one crore rupees in any previous year:

[Provided that in the case of a person whose—

(a) aggregate of all amounts received including amount received for sales, turnover or gross receipts during the previous year, in cash, does not exceed five per cent of the said amount; and

(b) aggregate of all payments made including amount incurred for expenditure, in cash, during the previous year does not exceed five per cent of the said payment,

this clause shall have effect as if for the words “one crore rupees”, the words “five crore rupees” had been substituted; or]

(b) carrying on profession shall, if his gross receipts in profession exceed fifty lakh rupees in any previous year; or

(c) carrying on the business shall, if the profits and gains from the business are deemed to be the profits and gains of such person under section 44AE or section 44BB or section 44BBB, as the case may be, and he has claimed his income to be lower than the profits or gains so deemed to be the profits and gains of his business, as the case may be, in any previous year; or

(d) carrying on the profession shall, if the profits and gains from the profession are deemed to be the profits and gains of such person under section 44ADA and he has claimed such income to be lower than the profits and gains so deemed to be the profits and gains of his profession and his income exceeds the maximum amount which is not chargeable to income-tax in any previous year; or

(e) carrying on the business shall, if the provisions of sub-section (4) of section 44AD are applicable in his case and his income exceeds the maximum amount which is not chargeable to income-tax in any previous year,

get his accounts of such previous year audited by an accountant before the specified date and furnish by that date the report of such audit in the prescribed form duly signed and verified by such accountant and setting forth such particulars as may be prescribed :

Provided that this section shall not apply to the person, who declares profits and gains for the previous year in accordance with the provisions of sub-section (1) of section 44AD and his total sales, turnover or gross receipts, as the case may be, in business does not exceed two crore rupees in such previous year:

Provided further that this section shall not apply to the person, who derives income of the nature referred to in section 44B or section 44BBA, on and from the 1st day of April, 1985 or, as the case may be, the date on which the relevant section came into force, whichever is later :

Provided also that in a case where such person is required by or under any other law to get his accounts audited, it shall be sufficient compliance with the provisions of this section if such person gets the accounts of such business or profession audited under such law before the specified date and furnishes by that date the report of the audit as required under such other law and a further report by an accountant in the form prescribed under this section.

Explanation.—For the purposes of this section,—

(i) “accountant” shall have the same meaning as in the Explanation below sub-section (2) of section 288;

(ii) “specified date”, in relation to the accounts of the assessee of the previous year relevant to an assessment year, means date one month prior to the due date for furnishing the return of income under sub-section (1) of section 139.

3) For AY 20-21 applicable Finance Act is FA,2019.

ANALYSIS:

1. Now the question is above proviso came into effect from 01-04-2020. Will this proviso applicable to AY 20-21?

2. Before deciding on applicability of proviso let us understand when should we check the threshold limit. The “words in clause a” and “proviso to clause a” clearly says that threshold limit should be checked during previous year.

3. Now we may interpret that proviso to clause a coming into effect from 01-04-2020 is applicable for PY 20-21 i.e AY 21-22, thereby 5 crore threshold limit is not applicable to AY 20-21 BUT

4. In explanation to Finance Bill No. 26 of 2020, it is clearly said that 5 crore threshold limit is applicable from AY 20-21 onwards and for all subsequent Assessment Years.

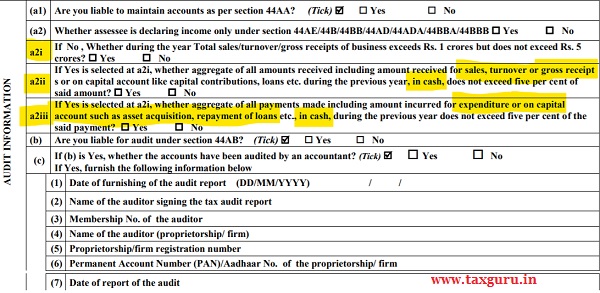

5. Even in ITR – 3 for AY 20-21, assessee should tick if his cash receipts and cash payments exceeds 5 percent or not.

CONCLUSION:

1. 5 crore threshold limit is applicable to AY 20-21 subject to satisfaction of conditions specified in proviso to clause a of 44AB.

Read 44AB clause a proviso

Read analysis of this article

My sole intention of writing this article is to bring to the notice of students that reading finance act should be read along with latest finace Bill . Because bill contains intention person who drafted law which is invisible in act. To understand this read only 44ab in finace act and then read finance Bill 2020

My dear friends in this article please do focus on applicability of proviso added via finance act 2020. It is an example of a retrospective ammendment without any such wordings. Source FinanceBill no 26 of 2020.

This is foul play as nobody is expected to show income @ 6% or 8% as the case may be. Since it would create a mammoth tax liability & hence everyone would go for tax audit under 44AD or in other sec declaring income less than 6%/8%. Actually this is just sugar coated section in reality everything remains same.

That if my turnover is less than Rs. 2 cr and I am showing less than 6%/8%, then tax audit is not is required?

Ans. Tax Audit is required. However if aggregate total income is less than maximum amount which is not chargeable to tax, in such case it is not required.

Please reply to this query

That if my turnover is less than Rs. 2 cr and I am showing less than 6%/8%, then tax audit is not is required?