Case Law Details

Gloria Eugenia Rynjah Banerji Vs ITO (ITAT Delhi)

Introduction: The Income Tax Appellate Tribunal (ITAT) Delhi’s decision in the case Gloria Eugenia Rynjah Banerji Vs ITO has ignited considerable debate in the tax law domain. The verdict essentially establishes that a technical ground alone cannot nullify income tax additions made by the Assessing Officer (AO). This article delves into the case’s details, focusing on its key aspects and implications.

The Crux of the Case: The main issue concerned an addition of Rs.2002801 made by the AO under section 68 of the Income Tax Act, which the assessee, Gloria Eugenia Rynjah Banerji, appealed. This appeal was against the order of the CIT(A)-34, New Delhi, which had confirmed the AO’s addition.

Previous Litigation History: This was not the first round of litigation between the parties. Initially, the CIT(A) had deleted the addition, prompting an appeal from the revenue side. The ITAT then sent the case back to the AO for reassessment in accordance with the law.

New Evidence and Contentions: In the new round of assessment, the assessee provided a will that differed from the one presented in the first round. The AO questioned the genuineness of the will, and the assessee responded with various explanations including the logic behind making deposits in amounts less than Rs. 50,000. All these contentions failed to convince the AO.

Legal and Factual Complexity: The counsel for the assessee argued that section 68 was not applicable as the assessee did not maintain any books of account. The money was deposited into a bank account from the sale of land in Meghalaya, which the AO found difficult to trace and verify. The factual matrix presented by the assessee was not consistent with ‘human probability,’ according to the ITAT.

The Final Verdict: The ITAT upheld the CIT(A)’s findings, stating that the income tax addition could not be deleted merely based on the technicality that the AO mentioned section 68 instead of section 69. The case’s peculiar facts did not warrant any relief to the assessee.

Conclusion: The ITAT Delhi’s decision in Gloria Eugenia Rynjah Banerji Vs ITO serves as a crucial reminder that technicalities should not overshadow substantial matters in income tax assessments. The ruling emphasizes the importance of presenting a factual matrix consistent with ‘human probability,’ failing which, tax additions are likely to be upheld, irrespective of the section under which they are made.

FULL TEXT OF THE ORDER OF ITAT DELHI

This appeal by the assessee is preferred against the order of the CIT(A)-34, New Delhi dated 26.03.2019 pertaining to A.Y.2007-08.

2. The solitary grievance of the assessee is that the CIT(A) erred in confirming the addition made by the AO u/s. 68 of the Act amounting to Rs.2002801/-.

3. This is not the first round of litigation as in first round when the addition was made the CIT(A) deleted the addition and the revenue preferred an appeal before this Tribunal and this Tribunal in ITA No.316/Del/2012 restored the issue back to the files of the AO to decide the same in accordance with law.

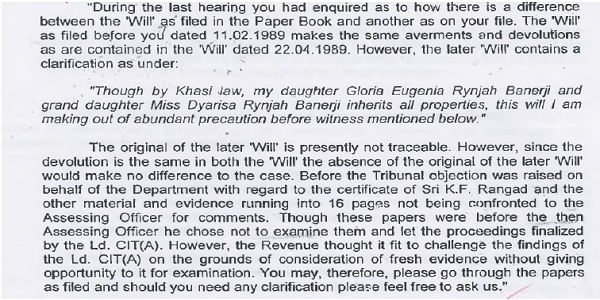

4. In the fresh assessment proceedings the AR of the assessee furnished a copy of will which was different from what was filed in the first round of litigation. The AO questioned the genuineness of the will, the assessee replied as under : –

5. The assessee was further asked to explain the delay in sending the money to Delhi and why there were deposits in amounts less than Rs. 50,000/-. In so far as the first querry is concerned the assessee replied as under :-

5. In respect of the second querry it was replied that the bank charges, handling charges of cash deposit exceeding Rs.50,000/-, therefore, to avoid bank charges cash was deposited in amounts less than Rs.50,000/-. The explanation of the assessee did not find any favour with the AO who completed the assessment by making the addition of Rs.2002801/- u/s. 68 of the Act.

6. Assessee carried the matter before the CIT(A) but without any success.

7. Before us the Counsel for the assessee vehemently stated that the addition cannot be made u/s. 68 of the Act in as much as assessee does not maintain any books of account and the cash was found to be deposited in the bank account, therefore, provisions of section 68 of the Act do not apply.

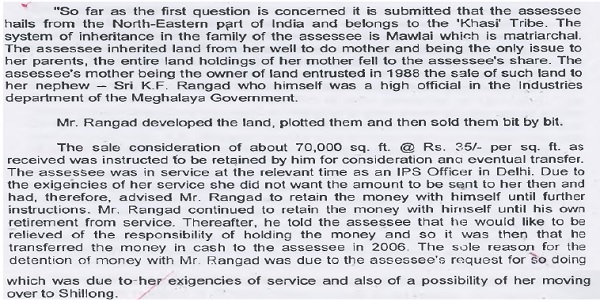

8. The Counsel reiterated that the amount of Rs.2002801/-emerged out of the sale proceeds of land at Meghalaya. It is the say of the Counsel that since the sources has been duly explained there is no reason for making the impugned addition.

9. The DR strongly supported the findings of the AO and read operative part of the assessment order.

10. We have given a thoughtful consideration to the orders of the authorities below. There is no dispute that some land was sold at Meghalaya in 1989 for a consideration of Rs.24.50 lacs. It is also not in dispute that the sale consideration was kept by the cousin brother of the assessee at Meghalaya. What is not understandable and is beyond the human probability that the brother of the assessee kept such a huge amount at Meghalaya since 1989 till 2006. It is also not understandable nor it has been proved before any authority including us as to how such a huge amount travelled in cash from Meghalaya to Delhi. The logic behind deposit of cash of Rs. 49,000/- each time in the bank account is also not justified. To sum up the factual matrix is not commensurate with the human probability. On such unbelievable facts the additions cannot be deleted merely on technical ground that the AO mentioned section 68 instead of section 69 of the Act.

The peculiar facts of the case discussed here in above do not justify any relief on this count.

11. We find no reason to interfere with the findings of the CIT(A). The appeal of the assessee is dismissed.

Order pronounced in the open court on 16.08.2023.

This is not an ordinary mistake . The purpose of a particular section is defeated . . Section 68 applies where books of accounts are maintained by the assessee and 69A is where cash or bank deposits are found and no explanation is given by the assessee . Every section has a specific character as enshrined in law . The order can be challenged in High Court . Just my opinion .