ICAI Suggestions on Form GSTR 9C- Reconciliation statement & Certification

Suggestions on GST GSTR- 9C

Indirect Taxes Committee

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

NEW DELHI

INTRODUCTION

1. The Institute of Chartered Accountants of India considers it a privilege to submit its suggestions on Reconciliation Statement and Certificate in Form GSTR 9C. We shall be pleased to discuss these suggestions provided in this communication during a meeting in person, to illustrate the points made by us.

We look forward to contribute in the drafting of simple, transparent and fair GST laws in India.

| S. No. | Topic(s) | Suggestion (s) |

| 1. | Calculation of Turnover of Rs. 2 Crore for the applicability of GST Audit | Limit of Turnover of Rs. 2 Crore would be calculated from July onwards for the FY 2017-18 or the Financial year 2017-18 would be considered for the same. Therefore, It is suggested to provide suitable clarification in this regard. |

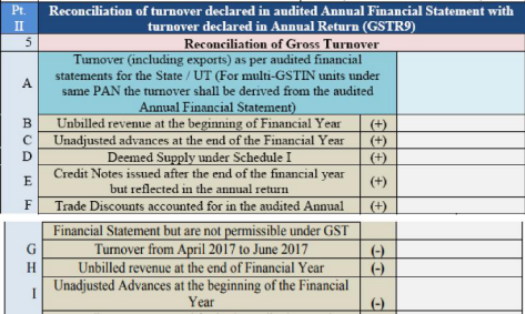

| 2. | Turnover of multi GSTN units under same PAN | Requirements “at the beginning of the financial year” in part 5B and 5Iseems to lead to some confusion. Therefore it is suggested to substitute it with words “as on 30th June, 2017” |

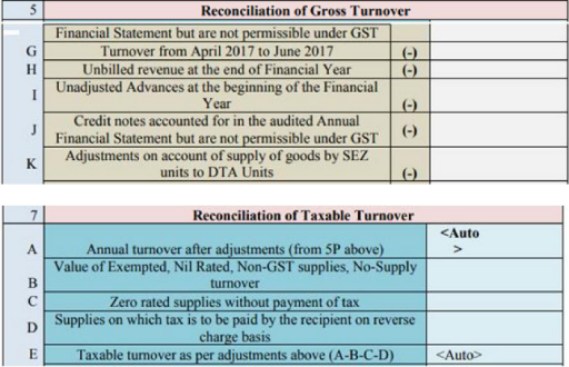

| 3. | Credit notes issued after the end of financial year | Credit notes accounted for in the audited annual financial statement must not be reduced from turnover as per Financial Statements but they should be added back so as to reconcile the amount with Annual Return. |

| 4. | Adjustment on account of supply of goods by SEZ to DTA units | It is suggested that this requirement to separately report the supplies of SEZ to DTA units in 5K be clarified that the turnovers to be reported in this clause would only be situations where the SEZ units do not file bill of entry in their name and IGST is paid by DTA buyer on reverse charge basis. |

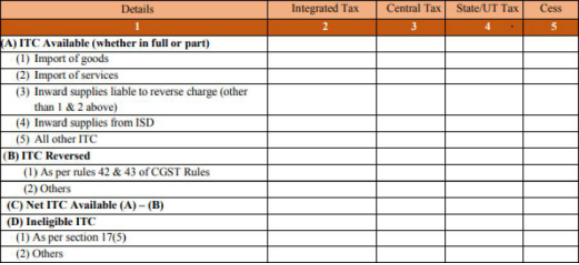

| 5. | Expense wise reconciliation | Table 14 of GSTR-9C requires expense-wise reporting of ITC available and availed whereas it is not feasible for auditors to verify expense wise ITC. Therefore, It is suggested to give relaxation in furnishing such breakup, to the extent maintained. |

| 6. | Classification of turnover between Nil, exempted, non-GST and no-supply turnover. | There is no clarity between non-GST supply and no-supply turnover due which it is difficult to bifurcate for e.g. whether high seas supply taken place out of country will be classifiable as no supply turnover or exempted turnover is not clear. Therefore, it is suggested to specifically define no-GST supplies or Non-GST turnover for classification of the same. |

| 7. | Cash flow statement requirement | There is a requirement to attach cash flow statement with form GSTR-9C. However, for small scale businesses it is difficult to comply with as they are not required to prepare the same. Therefore, It is suggested to make the attachment of cash flow statement optional for small scale businesses. |

| 8. | Certification by Auditor | The certification wordings places the entire responsibility of reporting on the Auditor whereas the information is provided by the Auditee (Registered Person) and the Auditor can only verify information to the extent provided and certify the same. Therefore, It is suggested that the verification wordings be suitable modified as :

“I hereby solemnly affirm and declare that the information given herein above is true and correct as per the information provided to us by the Registered Person and to the best of my knowledge and belief and nothing has been concealed there from. |

| 9. | Pt. V- Auditor’s recommendation on additional Liability due to non-econciliation |

It is suggested that:-

i. Nature of recommendation by Auditor (binding or non-binding) to be clarified ii. Recommendations to ‘pay’ or ‘not pay’ tax be permitted in this Part. iii. Payment of tax be allowed through ITC as well as cash. |

| 10. | Requirement of Audit in | Where a taxpayer has obtained registration |

DETAILED SUGGESTIONS

1. Calculation of Turnover of Rs. 2 Crore for the applicability of GST Audit In terms of Rule 80(3) of the CGST Rules “every registered person whose aggregate turnover during a financial year exceeds two crore rupees shall get his accounts audited.

Issue: Limit of Turnover of Rs. 2 Crore would be calculated from July onwards for the FY 2017-18 or the Financial year 2017-18 would be considered for the same.

Suggestion: It is suggested to provide suitable clarification in this regard.

2. Turnover of multi GSTN units under same PAN

Issue:

1. Part 5B “Unbilled revenue at the beginning of Financial year” seems to lead to some confusion.

2. Part 5I “Unadjusted advances at the beginning of the financial year” seems to lead to some confusion.

3. This confusion is on account of the fact that the GST regime was effective from July 1, 2017. The question that arises is, when the form states ‘beginning of financial year’, whether information as at April 1, 2017 should be considered or as at July 1, 2017. It is clear that in respect of GST reconciliation, information must be reckoned from its inception and not earlier. For this reason, it is advisable to clear this confusion by suitably stating with reference to the date of inception of GST, that is, “as at July 1, 2017”.

Suggestion:

It is suggested to substitute the words “at the beginning of the financial year” in part 5B and 5I with words “as on 30th June, 2017”

3. Credit notes issued after the end of financial year

Issue: Part 5E require reporting of credit notes issued after the end of financial year but reflected in the annual return as addition to turnover whereas part 5J requires credit notes accounted for in the audited annual financial statement but not permissible under GST as deduction.

Since the reconciliation is derived from turnover as per financial statements towards annual return, the amount of credit notes not reduced from turnover in FS till March-18 but reduced from turnover Annual Return cannot be ‘added’ but be ‘reduced’ from turnover in FS so as to reconcile the amount with turnover Annual Return. The symbol ‘+’ is creating the confusion. Therefore, the symbol ‘-‘would clear any confusion.

Also, credit notes accounted for in the audited annual financial statement but are contrary to section 34 (stated as, not permissible under GST) must not be reduced from turnover as per Financial Statements Annual Return but they should be added back so as to reconcile the amount with Annual Return.

Suggestion: It is suggested to make following modifications in the form GSTR-9C.

| E | Credit notes accounted for in the audited annual financial statement but are not permissible under GST | (+) |

…..

| J | Credit notes issued after the end of the financial year but reflected in the annual return | (-) |

4. Adjustment on account of supply of goods by SEZ to DTA units

Issue: There are certain SEZ units who remove goods to DTA on their own account by filing ‘self-bill of entry’, pay corresponding IGST and move the goods under an Invoice with IGST on forward charge basis. Clause 5K, does not appear to clearly state this situation causing confusion.

Suggestion: It is suggested that this requirement to separately report the supplies of SEZ to DTA units in 5K be clarified that the turnovers to be reported in this clause would only be situations where the SEZ units do not file bill of entry in their name and IGST is paid by DTA buyer on reverse charge basis.

5. Expense wise reconciliation

Table 14 of GSTR 9C

| 14 | Reconciliation of ITC declared in Annual Return (GSTR9) with ITC availed on expenses as per audited Annual Financial Statement or books of account | |||

| Description | Value | Amount of Total ITC | Amount of eligible ITC availed | |

| 1 | 2 | 3 | 4 | |

| A | Purchases | |||

| B | Freight / Carriage | |||

| C | Power and Fuel | |||

| D | Imported goods (Including received from SEZs) | |||

| E | Rent and Insurance | |||

| F | Goods lost, stolen, destroyed, written off or disposed of by way of gift or free samples | |||

| G | Royalties | |||

Table 4 of GSTR 3B

4. Eligible ITC

Issue:

1. Table 14 of GSTR-9C requires expense-wise reporting of ITC available and availed whereas it is not feasible for auditors to verify expense wise ITC.

2. Table 14 of GSTR 9C require reporting of total ITC and eligible ITC separately which is also the requirement in form GSTR 3B but some assesses have reported only the net amount of ITC eligible while filing GSTR 3B. In such cases, it will become difficult to identify these figures separately as assessees would have expensed such ineligible ITC in the respective head of expense at the time of booking.

One must appreciate the fact that the relevant Form GSTR 9C was notified after the end of the financial year. Units have not maintained this data to be able to furnish the same accurately.

Suggestion:

It is suggested to give relaxation in furnishing such breakup, to the extent maintained.

6. Classification of turnover between Nil, exempted, non-GST and no-supply turnover.

| 7 | Reconciliation of Taxable Turnover | |

| 7A | Annual turnover after adjustments (from 5P above) | <Auto> |

| 7B | Value of Exempted, Nil Rated, Non-GST supplies, No-Supply Turnover | |

Issue: There is no clarity between non-GST supply and no-supply turnover due which it is difficult to bifurcate for e.g. whether high seas supply taken place out of country will be classifiable as no supply turnover or exempted turnover is not clear.

Suggestion: It is suggested to specifically define no-GST supplies or Non-GST turnover for classification of the same.

7. Cash flow statement requirement

Issue: There is a requirement to attach cash flow statement with form GSTR-9C. However, for small scale businesses it is difficult to comply with as they are not required to prepare the same.

Suggestion: It is suggested to make the attachment of cash flow statement optional for small scale businesses.

8. Certification by Auditor

Verification:

“I hereby solemnly affirm and declare that the information given herein above is true and correct to the best of my knowledge and belief and nothing has been concealed there from.”

Issue: The certification wordings places the entire responsibility of reporting on the Auditor whereas the information is provided by the Auditee (Registered Person) and the Auditor can only verify information to the extent provided and certify the same.

Suggestion: It is suggested that the verification wordings be suitable modified as “I hereby solemnly affirm and declare that the information given herein above is true and correct as per the information provided to us by the Registered Person and to the best of my knowledge and belief and nothing has been concealed there from.

9. Pt. V- Auditor’s recommendation on additional Liability due to non-reconciliation

Issue:

i. The recommendations by the Auditor in Pt. V are understood to be a ‘note or disclosure’. While it is a statement of fact, it need not be an opinion. There can also be situations which could be an opinion of the Auditor whereas the Registered Person may differ. Such situations need not necessarily result in payment of tax. Auditor’s recommendations may be clarified to be ‘binding or non-binding’ recommendation that the Registered Person will engage with the revenue authorities for its final determination. Clarity in this regard is much needed.

ii. As Auditor’s recommendation may not necessarily be in favour of revenue. Such comments in the recommendations will most certainly not lead to payment of tax immediately. In fact, in this Part, the Auditor may be permitted to disclose such situations also. However, it appears that only where taxes are found payable only are being dealt with in this Part. Clarity in this regard is also required.

iii. Payment of tax under auditor’s recommendation through cash. There may be instances where Registered Persons who have surplus ITC but a genuine error resulting in payment of tax was identified at the time of GST audit. In such situations, the form must provide to enable payment of such dues, to adjust the available credit and pay the dues. Whether the system permits this understanding is to be clarified.

Suggestion: It is suggested that:-

iv. Nature of recommendation by Auditor (binding or non-binding) to be clarified

v. Recommendations to ‘pay’ or ‘not pay’ tax be permitted in this Part.

vi. Payment of tax be allowed through ITC as well as cash.

Part B – Certificate

Financial Statements comprise of Balance Sheet, Profit and Loss account and Cash flow Statement. These are not prepared for each Registered Person. It may be clarified whether the Financial Statements of the Entity alone is to be annexed or not.

Comments by the Auditor regarding the books of accounts already subject to audit under any other statute may appear to contradict with the findings by that auditor. Such situations are to be avoided. GST Auditor may limit his findings to GST and not travel beyond into the Financial Statements.

Suggestion – Revised Part B Provided below :

PART – B- CERTIFICATION

I. Certification in cases where the reconciliation statement (FORM GSTR-9C) is drawn up by the person who had conducted the audit:

* I/we have conducted audit of the books of accounts of M/s ……………. (Name and address of incorporation of the Person) having GSTIN ……………… and registration in the State at ……………. (Name and Principal Place of Business of Registered Person) comprising of—

(a) balance sheet as at ………….

(b) the *profit and loss account/income and expenditure account for the period beginning from …….to ending on …………….. ,

(c) the *cash flow statement for the period beginning from ……….to ending on …………. , —are attached herewith, and

(d) documents declared by the said Act to be part of, or annexed to, the *profit and loss account/income and expenditure account and balance sheet.

2. Based on our audit I/we report that the said Person—

*has maintained the books of accounts, records and documents in respect of transactions of the Registered Person as required by the IGST/CGST/<<>>GST Act, 2017 and the rules/notifications made/issued thereunder subject to the following observations / limitations:

1.

2.

3.

3. *I/we further report, in respect of the transactions of the Registered Person, that, –

(A) *I/we have obtained all the information and explanations which, to the best of *my/our knowledge and belief, were necessary *were / were not provided/partially provided to us.

(B) In *my/our opinion, proper books of accounts pertaining to the Registered Person *have/have not been kept by the Person so far as appears from*my/ our examination of the said books of accounts maintained at the principal place of business at ……… and …….. additional place of business within the State..

4. I/we certify that the transactions pertaining to the Registered Person recorded in the said books of accounts *are / are not in agreement with the audited financial statements, that is, balance sheet, the *profit and loss / income and expenditure account and the cash flow statement issued in respect of the Person The documents required to be furnished under section 35 (5) of the CGST Act and Reconciliation Statement required to be furnished under section 44(2) of the CGST Act is annexed herewith in Form No. GSTR-9C.

5. In *my/our opinion and to the best of *my/our information and according to examination of books of accounts pertaining to the Registered Person including other relevant documents and explanations given to *me/us, the particulars given in the said Form No.9C are true and correct subject to the following observations / qualifications, if any:

(a) ……………………………………………………………………………………………………

(b) ……………………………………………………………………………………………………

(c) …………………………………………………………………………………………………….

………………………………….

………………………………….

** (Signature and stamp/Seal of the Auditor)

Place: ……………

Name of the signatory ………………

Membership No ……………………

Date: …………………

Full address …………………….

* delete whichever is not applicable

II. Certification in cases where the reconciliation statement (FORM GSTR-9C) is drawn up by a person other than the person who had conducted the audit of the accounts:

*I/we report that the audit of the books of accounts M/s……………. (Name and address of incorporation of the Person) having GSTIN …………… and registration in the State at ……………….. (Name and Principal Place of Business of Registered Person) was conducted by M/s. …………………. (full name and address of auditor along with status), bearing membership number in pursuance of the provisions of the ………………. Act, and *I/we annex hereto a copy of their audit report along with the audited financial statements of the Person dated ………………… comprising of :-

(a) balance sheet as at …………..

(b) the *profit and loss account/income and expenditure account for the period beginning from …………. to …………. ending on ,

(c) the *cash flow statement for the period beginning from ………………. to ending on ……………, and

(d) documents declared by the said Act to be part of, or annexed to, the *profit and loss account/income and expenditure account and balance sheet.

2. I/we report that the said Person—

*has maintained the books of accounts, records and documents in respect of transactions of the Registered Person as required by the IGST/CGST/<<>>GST Act, 2017 and the rules/notifications made/issued thereunder subject to the following observations / limitations:

1.

2.

3.

3. The documents required to be furnished under section 35 (5) of the CGST Act and Reconciliation Statement required to be furnished under section 44(2) of the CGST Act is annexed herewith in Form No.GSTR-9C.

4. In *my/our opinion and to the best of *my/our information and according to examination of books of accounts pertaining to the Registered Person including other relevant documents and explanations given to *me/us, the particulars given in the said Form No.9C are true and correct subject to the following observations / qualifications, if any:

(a) ……………………………………………………………………………………………………

(b) ……………………………………………………………………………………………………

(c) …………………………………………………………………………………………………….

………………………………….

** (Signature and stamp/Seal of the Auditor)

Place: ……………

Name of the signatory ………………

Membership No ……………………

Date: …………………

Full address …………………….II.

* delete whichever is not applicable

10. Requirement of Audit in case of exempted outward supplies only

In terms of Rule 80(3) of the CGST Rules “every registered person whose aggregate turnover during a financial year exceeds two crore rupees shall get his accounts audited as specified under sub-section (5) of Section 35 of the Act.

Issue : A taxpayer has obtained registration due to application of provision of Section 24 of CGST Act, 2017 read with Section 9(3), however dealing in exclusively exempted supply only.

Suggestion : We understand that in the aforesaid scenario, Audit would be required as aggregate turnover includes exempt supply, However clarificatory circular may be issued in this regard.

In case any further clarifications or data is considered necessary, we shall be pleased to furnish the same. The contact details are:

| Name and Designation | Contact Details | |

| Ph. No. | Email Id | |

| CA. Madhukar N Hiregange Chairman, Indirect Taxes Committee | 9845011210 | madhukar@hiregange.com |

| CA. Sharad Singhal, Secretary, Indirect Taxes Committee | 09310542608 0120- 3045954 |

idtc@icai.in ; s.singhal@icai.in |

For any further information, please visit the website of Indirect Taxes Committee: www.idtc.icai.org.

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

(Set up by an Act of Parliament)

CA. Naveen N. D. Gupta

President

ICAI/IDTC/2018-19/Letted/19

24th September, 2018

Shri Arun Jaitley

Hon’ble Union Minister of Finance, and

Chairman, Goods & Services Tax Council

Ministry of Finance,

Government of India, North Block

New Delhi — 110001

Respected Sir,

Sub: Suggestions on GST Annual Return form

At the outset, we are thankful to the Government for considering most of the suggestions on issues related to GST submitted by the ICAI from time to time.

We refer to the Annual Return form as released by the Government vide Notification No. 39/2018- Central Tax dated 4th September, 2018. In this regard, we consider it a privilege to submit herewith ICAI’s suggestions thereon. The suggestions have been finalized based on the inputs received from members across India who are involved in GST implementation. We hope that these suggestions would also be considered favorably.

We shall be glad to provide any further input as may be required and your office may reach us at idtc@icai.in or 0120-3045954.

Thanking you and with warm regards,

Yours sincerely,

CA. Naveen N. D. Gupta

Suggestions on GST Annual return form

Indirect Taxes Committee

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

NEW DELHI

INTRODUCTION

1. The Institute of Chartered Accountants of India considers it a privilege to submit its suggestions on Annual return form. We shall be pleased to discuss suggestion in meeting to illustrate the points made by us.

2. We look forward to contributing in the drafting of simple, transparent, & fair GST laws in India

Suggestions on Annual Return

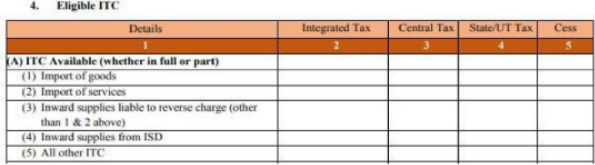

1. Total amount of ITC availed through Form GSTR 3B

Table 4 of GSTR 3B

Table 6 of GSTR 9

Issue: Part E of Table 7 of Annual return require reporting of ineligible ITC under section 17(5) to find out net eligible ITC by deducting the ineligible ITC from the total ITC calculated in Table 6. However, Table 6 (A) figures are auto populated from only Table 4A of GSTR 3B which collates the information of total ITC available.

Suggestion: It is suggested that Table 6 (A) figures be auto populated from table 4A and 4D as applicable instead of only from 4A.

2. Part I and J of table 8 require same information

| 8 |

Other ITC related information |

||||

| A | ITC as per GSTR-2A (Table 3 & 5 thereof) | <Auto> | <Auto> | <Auto> | <Auto> |

| B | ITC as per sum total of 6(B) and 6(H) above | <Auto> | |||

| C | ITC on inward supplies (other than imports and inward supplies liable to reverse charge but includes services received from SEZs) received during 2017-18 but availed during April to September, 2018 | ||||

| D | Difference [A-(B+C)] | ||||

| E | ITC available but not availed (out of D) | ||||

| F | ITC available but ineligible (out of D) | ||||

| G | IGST paid on import of goods (including supplies from SEZ) | ||||

| H | IGST credit availed on import of goods (as per 6(E) above) | <Auto> | |||

| I | Difference (G-H) | ||||

| J | ITC available but not availed on import of goods (Equal to I) | ||||

Issue: Part J of table 8 of Annual return requires data equal to Part I. Two separate rows requiring same information is duplication of data.

Suggestion: It is suggested that intention for putting separate rows for same information be clarified.

3. Segregated details of ITC availed as I /IS/CG

| 6 | Details of ITC availed as declared in returns filed during the financial year | |||||

| A | Total amount of input tax credit availed through FORM GSTR-3B (sum total of Table 4A of FORM GSTR-3B) |

<Auto> | <Auto> | <Auto> | <Auto> | |

| B | Inward supplies (other than imports and inward supplies liable to reverse charge but includes services received from SEZs) | Inputs | ||||

| Capital Goods | ||||||

| Input Services | ||||||

| C | Inward supplies received from unregistered persons liable to reverse charge (other than B above) on which tax is paid & ITC availed | Inputs | ||||

| Capital Goods | ||||||

| Input Services | ||||||

| D | Inward supplies received from registered persons liable to reverse charge (other than B above) on which tax is paid and ITC availed | Inputs | ||||

| Capital Goods | ||||||

| Input Services | ||||||

| E | Import of goods (including supplies from SEZs) | Inputs | ||||

| Capital Goods | ||||||

Issue: Table 6 ( B to E ) of GSTR-9 requires the taxable person to bifurcate the total ITC availed as ITC on input, capital goods and input services. This is a new / additional detail that a taxable person would be required to prepare & it is important to note that such classification was not required in GSTR-3B.

Suggestion: It is suggested that since there is no difference in treatment of ITC on Goods & services and such details were not asked in earlier period returns therefore the bifurcation of the same in the Annual return leads to recapturing of accounting entries as assessee has not recorded the same in the notified formats, therefore such requirement be omitted.

4. Details of outward and inward supplies declared during the financial year

Issue: The heading of Part II of GSTR 9 requiring “Details of outward and inward supplies declared during the financial year” creating confusion as to what details can be filed in annual Return i.e. only the details submitted in GSTR 3B and/or GSTR 1 earlier can be reported in GSTR 9 or details furnished after the end of the financial year in the returns can also be incorporated in the annual return.

Suggestion: It is suggested that suitable clarification be issued in this regard. Also, clarify whether an assessee can furnish information beyond submitted returns.

5. Table 8A : Other ITC related information

| A | ITC as per GSTR-2A (Table 3 & 5 thereof) | <Auto> | <Auto> | <Auto> | <Auto> |

Issue:

i. Table 8A contains Auto populated figure, till which date will it be auto populated? GSTR-1 by its counter supplier can be filled belatedly after submission of annual return by recipient

ii. Whether Table 8A auto populated figures will contain effects of amendments made during the FY 17-18, and made in FY18-19 for effect of FY 17-18?

Suggestion: It is suggested to clarify the above issues.

6. Table 8D : Other ITC related information

| 8 | Other ITC related information | ||||

| A | ITC as per GSTR-2A (Table 3 & 5 thereof) | <Auto> | <Auto> | <Auto> | <Auto> |

| B | ITC as per sum total of 6(B) and 6(H) above | <Auto> | |||

| C | ITC on inward supplies (other than imports and inward supplies liable to reverse charge but includes services received from SEZs) received during 2017-18 but availed during April to September, 2018 | ||||

| D | Difference [A-(B+C)] | ||||

Issue: In Point 8D, provision is made only where ITC as per GSTR 2A exceeds ITC reported in Table 8B & 8C of GSTR-9. No provision is made when ITC taken in GSTR-3B exceeds ITC as per GSTR 2A. Point 8D shall reflect negative figure in certain situations viz. supplier has not uploaded the invoices in GSTR-1.

Suggestion: Impact of negative figure may be clarified including issue arising out of counter party late submission etc. raised at point 8A.

7. Table 8E & 8F : Other ITC related information

| E | ITC available but not availed (out of D) | ||||

| F | ITC available but ineligible (out of D) |

Issue :

(1) Reference is drawn from 8D which may be incorrect in some cases?

(2) In few cases, 8E & F can be positive even if 8D is negative.

It may be the case that Supplier has not filled GSTR-1, therefore credit appearing in 2A is less than what have been availed and may include ineligible credit.

Eg. Rs. 1000 appearing in 2A which includes Rs. 200 ineligible credit and Rs. 50 not availed and taxpayer has claimed Rs. 1200 as credit in 8B, resulting 8D is negative. Rs. 200 and Rs. 50 cannot be written in 8 E and 8 F which is negative Rs.200.

Suggestion: Appropriate amendments may be made in Table 8 to handle all ineligible and non-availed credits.

8. Table 8G : Other ITC related information

| G | IGST paid on import of goods (including supplies from SEZ) |

Issue:

(a) No row similar to 8C is provided for taking of credit on import of goods received during 2017-18 but ITC taken from April 2018 to September 2018.

(b) No provision is made for calculation of ITC to lapse on reverse charge including import of service. Provision for ITC to lapse is made only for items in Table 3 & 5 of GSTR 2A and import of goods.

Suggestion: (a) Row be inserted in Table 8 to provide for taking of ITC on import of goods and supplies from SEZ from April 2018 to September 2018

(b) The relevant rows be inserted in Table 8 to provide for ITC to lapse in respect of import of service and ITC on reverse charge on domestic inward supplies.

9. Part V of GSTR 9 disclosure or reporting

| Pt. V | Particulars of the transactions for the previous FY declared in returns of April to September of current FY or upto date of filing of annual return of previous FY whichever is earlier | |||||

| Description | Taxable Value |

Central Tax | State Tax/ UT Tax |

Integrate

d Tax |

Cess | |

| 1 | 2 | 3 | 4 | 5 | 6 | |

| 10 | Supplies / tax declared through Amendments (+) (net of debit notes) | |||||

| 11 | Supplies / tax reduced through Amendments (-) (net of credit notes) | |||||

| 12 | Reversal of ITC availed during previous financial year | |||||

| 13 | ITC availed for the previous financial year | |||||

Issue: Part V of GSTR 9 requires particulars of transactions declared in returns upto date of filing of annual return of previous year. However it is not clear that this is just a reporting requirement or a tax calculation mechanism

Suggestion: It is suggested that a suitable clarification be issued in this regard.

10. Requirement to report Debit note / credit note issued this year

Issue: Debit/ credit note issued in 2018-19 for 2017-18, should that be reported in this Form. In those cases where debit/ credit note issued but tax liability has not been reduced and ITC not reversed, because they are not in the format of Section 34.

Suggestion: It is suggested that suitable explanation with proper examples be given to clarify the issue.

11. Segregated details of outward supplies on which tax is not payable

| 5 | Details of Outward supplies on which tax is not payable as declared in returns filed during the financial year | |||||

| A | Zero rated supply (Export) without payment of tax | |||||

| B | Supply to SEZs without payment of tax | |||||

| C | Supplies on which tax is to be paid by the recipient on reverse charge basis | |||||

| D | Exempted | |||||

| E | Nil Rated | |||||

| F | Non-GST supply | |||||

| G | Sub-total (A to F above) | |||||

Issue: In Annual return there is a column for furnishing details of outward supplies on which tax is not payable where nil rated and non-GST supplies are required to furnish separately without any purpose of seeking the same.

Also, nil and exempted supplies also need to be furnished separately whereas there is no clarity between nil and exempted supply leading to difficulty in compilation.

Suggestion: It is suggested to merge the requirement of supplies on which tax is not payable despite separate reporting of nil, exempted and non-taxable supply as it is not serving any purpose but causing difficulty in compilation as these segregations have not been captured by assessee.

12. Clarification on Taxes Payable

Part II of Annual Return provides for the details of outward and inward supplies declared during the financial year and Part IV provides for the details of tax paid as declared in returns filed during the financial year.

Issue: There is no explanation provided for the tax Payable reporting in Part II and Part IV. There arises a question that whether this be auto populated or manually reported and how would this be reconciled with returns. Should these values be based on the returns or computed based on the respect above reporting table?

Suggestion: It is suggested that suitable explanation with proper examples be given to clarify the issue.

13. Reporting of Amendments

Issue: Amendments to the Turnover has been reported in both Part II and Part V. Is Part V merely a subset of Part II to be used as reconciling item for the subsequent year? If so, whether heading of Table 4 should be be altered? If not where should the missing turnover of FY 2017-18 reported in Table 4, 5, 6 of FY 2018-19 be reported. How would one come to conclusion of Total Turnover Figure as per the Annual returns?

Suggestion: It is suggested that suitable explanation with proper examples be given to clarify the issue.

14. Requirement for filing details of ineligible ITC be done away

| 8 | Other ITC related information | ||||

| A | ITC as per GSTR-2A (Table 3 & 5 thereof) | <Auto> | <Auto> | <Auto> | <Auto> |

| B | ITC as per sum total of 6(B) and 6(H) above | <Auto> | |||

| C | ITC on inward supplies (other than imports and inward supplies liable to reverse charge but includes services received from SEZs) received during 2017-18 but availed during April to September, 2018 | ||||

| D | Difference [A-(B+C)] | ||||

Issue: Table 8 part F of Annual return requires information related to ITC available but ineligible whereas ineligible credits are taken as expense therefore reporting of this data for the annual return would be a challenge for the assessee.

Suggestion: It is suggested that this requirement of reporting information related to ITC available but ineligible be done away with as this credit is not eligible and reporting of same is not serving any purpose.

15. Option of Period selection should be there in

GSTR 9

Issue: For instance a taxpayer has been shifted to Composition scheme from normal scheme in the mid of the year in 2017-18. There are separate forms of Annual return for normal and composition taxpayer however there is no option to select the period for which taxpayer is filing Annual Return.

Suggestion: It is suggested that option for selection of period for which taxpayer is filing Annual return be provided in the return.

16. Cross charge be taken in Annual return

Issue: Recently AAR has ruled that employees employed in corporate office are providing services to the corporate office only and hence they have no employer-employee relationship with other offices.

In this regard there is no clarity whether such cross charge need to be considered in furnishing of information for Annual return though not considered in returns filed earlier.

Suggestion: It is suggested to clarify the reporting of cross charge in Annual return.

17. Reporting requirements

Issues:

1. Whether pre-GST supplies affected post- GST require reporting under GSTR 9?

2. Whether non-GST supplies like Duty- drawback, creditors written off etc. require reporting under GSTR 9?

Suggestion: It is suggested that the above reporting requirement be clarified.

18. Some Sort of Notes to Annual Return

Suggestion: Word file to insert some description / Explanation should be provided at the end so that transactions which are reported by mistake or left out or incorrectly reported & which are very difficult to correct via subsequent GSTR 3B or 1 even as per circular 26 for any reason, can be explained by the taxable person & hence it can act as a disclosure tool in connection with the concealment part specified in the Verification at the end.

19. To capture difference between GSTR 2A and GSTR 3B

| 8 | Other ITC related information | ||||

| A | ITC as per GSTR-2A (Table 3 & 5 thereof) | <Auto> | <Auto> | <Auto> | <Auto> |

| B | ITC as per sum total of 6(B) and 6(H) above | <Auto> | |||

| C | ITC on inward supplies (other than imports and inward supplies liable to reverse charge but includes services received from SEZs) received during 2017-18 but availed during April to September, 2018 | ||||

| D | Difference [A-(B+C)] | ||||

| E | ITC available but not availed (out of D) | ||||

| F | ITC available but ineligible (out of D) | ||||

| G | IGST paid on import of goods (including supplies from SEZ) | ||||

| H | IGST credit availed on import of goods (as per 6(E) above) | <Auto> | |||

| I | Difference (G-H) | ||||

| J | ITC available but not availed on import of goods (Equal to I) | ||||

Issue: Table 8 is designed to accumulate difference in ITC reflecting in GSTR 2A and furnished in GSTR 3 B. However, the table covers few difference areas only.

Suggestion: It is suggested to incorporate other reasons of difference in the table.

20. Difference in tax due to some reasons

Issue: Difference of opinion between any additional taxes (HSN difference or POS difference / valuation difference etc.) How to report such transactions.

Suggestion: It is suggested to clarify in this regard.

21. Other Suggestions

Issues:

1. Whether the formats of Annexures are standardized (to be provided if standardized) or can be customized in terms of presentation?

2. Whether the information to be provided on Input Tax Credit restrictions as per sections 17(5), 42 and 43 of CGST Act, 2017 should be detailed or consolidated value?

3. In Table 15, there is no clarity on how to provide details on various types of refunds in relation to exports, inverted duty structure, wrong payments and double tax payments. Whether the annexures will be standardized or can be customized for each type of refund?

4. As per the Annual return there is 2 years reconciliation statement required, whether the annexures in relation to this are standardized or can be customized? And whether reconciliation is be made available for outward supplies?

Suggestion: It is suggested to issue suitable clarifications in this regard.

22. Permit availment of ITC pertaining to FY 2017-18 till filing of Annual return.

Sec. 16(4) of the CGST Act, 2017 provides that a registered person shall not be entitled to take input tax credit in respect of any invoice or debit note for supply of goods or services or both after the due date of furnishing of the return under section 39 for the month of September following the end of financial year to which such invoice or invoice relating to such debit note pertains or furnishing of the relevant annual return, whichever is earlier.

As of today there is no due date for filing return (GSTR-3) u/s 39 and amended Rule 61(5) of the CGST Rules, 2017 provides that GSTR-3B is not a return in lieu of GSTR-3 and hence input tax credit pertaining to FY 2017-18 can be claimed till the date of filing of the annual return.

| C | ITC on inward supplies (other than imports and inward supplies liable to reverse charge but includes services received from SEZs) received during 2017-18 but availed during April to September, 2018 | ||||

| D | Difference [A-(B+C)] | ||||

| E | ITC available but not availed (out of D) | ||||

| F | ITC available but ineligible (out of D) | ||||

| G | IGST paid on import of goods (including supplies from SEZ) | ||||

| H | IGST credit availed on import of goods (as per 6(E) above) | <Auto> | |||

| I | Difference (G-H) | ||||

| J | ITC available but not availed on import of goods (Equal to I) |

Issue: Part 8C & 8E read with 8K of Table 8 of GSTR 9 provides for lapse of ITC eligible but not availed till September.

Suggestion: It is suggested to make suitable modification in Form GSTR 9 to allow input tax credit for invoices pertaining to FY 2017-18 till 31st December, 2018.

23. General Issue :

Issue A : The information in GSTR-9 , Table 4, 10 & 11 instruction indicate data “May be” taken from GSTR-1, however, table headings uses the word as declared in the returns which could be Form GSTR- 3B.

a. How to address differences between 1 & 3 B

b. How to address turnover reported in books of accounts, but not considered in GSTR-9

Suggestion: It is suggested that suitable clarification be provided in the instructions or additional field for capturing missing information. Suitable clarification is also required for cases not covered under GSTR-9C as to where they should rectify the errors or report additional liability as GSTR-9 is only compilation of information filed earlier.

Issue B: Table of GSTR9 states “Financial year”. Instruction no. 2 also provides for details for the period from July, 2017 to March, 2018. If taxpayer is shifting from Composition scheme to normal scheme during FY 2017-18.

a. Is he required to file FORM – 9 as well as FORM – 9A?

b. Whether system will allow filing two annual returns for the same tax period?

Suggestion: It is suggested that appropriate clarification be issued in this regard.

24. Taxable Value (Table 4k-4l)

| K | Supplies/tax declared through Amendments (+) | |

| L | Supplies / tax reduced through Amendments (-) |

Issue: This table expects gross reporting in 4A to 4H and corrections to the gross reporting in 4K to 4L. This might be misleading to the taxpayer unless suitable instructions are given. Also whether addition of invoice in a subsequent tax period (within FY 2017-18) relating to previous tax period should be reported in 4B or 4K ?

For example, July 2017 B2B turnover reported as Rs. 500 and corrected to 450 in the month of Jan, 2018 by way of amendment in Table 9 of GSTR-1, while correcting the same procedure to amend is not an upward or downward adjustment rather it is modification of the original value itself, therefore the reporting in GSTR-9 could be as follows :

(a) 4B = Rs. 450 and 4L = 0

(b) 4B= Rs. 500 and 4L= -50

It may be noted that in case (b), the adjusted value of Rs. -50 is apparently not available in any of the return value.

If the same is corrected in GSTR-3B in the month of April 2018, it is not clear whether this adjustment to be reported in Table 4 or Table 11.i

Suggestion: It is suggested that

(a) The same information can be auto populated

(b) Suitable instructions to be given with examples to fill the form

(c) Option to report at net basis to be made available

25. Table 9 : Details of tax paid as declared in returns

| Pt. IV | Details of tax paid as declared in returns filed during the financial year | ||||||

| 9 | Description | Tax Payable | Paid through cash | Paid through ITC | |||

| Central Tax | State Tax / UT Tax |

Integrated Tax | Cess | ||||

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | |

Issue: Whether Tax payable col. 2 would be from Part II of GSTR-9 or GSTR-3B.

Suggestion: Suitable clarification be provided.

26. Taxable Value (Table 4 F)

| F | Advances on which tax has been paid but invoice has not been issued (not covered under (A) to (E) above) |

|

|

|

|

|

Issue : This table expects reporting of unadjusted advances of the previous financial year. Considering GSTR 1 this value would be GSTR 1 Table 11A – Table 11B. This cannot be extracted from 3B.

Suggestion: It is suggested that

(a) The same information can be auto populated from GSTR-1

(b) Suitable instructions to be given with examples to fill the form.

27. Table 6 J : Details of ITC availed in returns

| I | Sub-total (B to H above) | |||||

| J | Difference (I – A above) |

Issue (A): 6A is auto populated from GSTR3B and 6B to 6H is segregation of various types of Input Tax Credit. If 6A is greater than I, then 6J would be negative. what would be the impact of such negative figure?

For Eg. Taxpayer claimed Rs. 1000 during the Fy 2017-18 Rs. 1000, however, on actual verification of books it was Rs. 900, then Negative -100 would be arrived in 6J.

(B) If 6A is less than 6I indicates taxpayer has not taken tax credit in GSTR-3B, additional Input Tax credit has now availed in GSTR-9, would this credit be added to electronic credit ledger ?

For E.g Taxpayer claimed Rs. 1000 till Sep, 2018 , however while filing return, it has been noticed that Rs. 200 credit was not availed which he added in GSTR-9

Suggestion: Suitable clarification be issued for the above issues.

28. Table 18 HSN inward is required whereas no such requirement in GSTR 3B

Issue: Table 18 of GSTR-9 requires the taxable person to report HSN wise summary of inward supplies – UQC, Total Qty, Taxable Value, Rate of Tax, CGST, SGST, and IGST. Such HSN wise details for inward supplies were not required to be reported in GSTR-3B. This again is a cumbersome requirement as HSN codes were given only for output supplies and not for inward. Also it may be noted that HSN is not mandatory to the suppliers with turnover less than Rs. 1.5 Crore.

Further Categorisation of HSN reporting for inward supply would be more cumbersome over outward supplies when a taxpayer is dealing in few goods only and for manufacturing such goods he procured more than 200 inward supplies which have different HSN including supplies received from taxpayer having less than Rs. 1.5cr turnover, due to which invoice does not capture HSN codes.

Suggestion: It is suggested that this requirement of reporting of HSN wise inward

supplies be done away with.

Alternatively, reporting of Top five inward supplies may be sought.

In case any further clarifications or data is considered necessary, we shall be pleased to furnish the same. The contact details are:

| Name and Designation | Contact Details | |

| Ph. No. | Email Id | |

| CA. Madhukar N Hiregange Chairman, Indirect Taxes Committee | 9845011210 | madhukar@hiregange.com |

| CA. Sharad Singhal, Secretary, Indirect Committee | 09310542608

0120- 3045954 |

idtc@icai.in ;

s.singhal@icai.in |

For any further information, please visit the website of Indirect Taxes Committee: www.idtc.icai.org.