Sec 17(2) of the CGST Act, 2017 provides that where the goods or services are used partly for effecting taxable supplies (including zero rated) and partly for exempt/ non-business use then the amount of credit as attributable to exempt supplies or non- business use shall be reversed as per Rule 42/43 of the CGST Rules, 2017.

Rule 42: Manner of determination of input tax credit in respect of inputs or input services and reversal thereof

As per Rule 42, reversal is required for that portion of common credit which is attributable to exempt supplies or for non-business use. (common credit means that part of ITC which cannot be identified specifically to taxable supplies including zero rated or exempt supplies or non- business rather commonly used for taxable supplies, exempt supplies or/and for non-business use.)

A formula has been prescribed to determine the eligible ITC to be taken removing the ITC attributable to exempt supplies or used for non-business use.

For using that formula, we need to first work out 3 things i.e. common credit (C2), common credit attributable to exempt supplies (D1), common credit attributable to non-business use (D2).

Remainder ITC to be taken removing a part of common credit attributable to exempt supplies etc. denoted by “C3”is- C3= C2- (D1+D2)

Working of C2, D1 and D2

1. Working of Common credit:

| Particulars | Amount | Remarks | |

| Gross amount on tax charged on inputs/input services | xxxxx | Gross tax amount in respect of inputs/input services procured | |

| Less: | Ineligible credit as per Sec 17(5) rent a cab, works contract etc. | xxx | |

| Less: | Tax component on goods and services exclusively used for effecting exempt suplies | xxx | Can be identified separately |

| Less: | Tax component on goods and services exclusively used for non-business use | xxx | Can be identified separately |

| Common credit | xxxxx |

2. Working of common credit attributable to exempt supplies (D1):

Where, Aggregate value of exempt supplies to be arrived at as per the below table :

| Particulars | Amount | Remarks | |

| Value of exempt supplies | xxxx | Exempt supplies defined in Sec 2(47) | |

| Add: | Value of outward supplies on which recipient is liable to pay tax under reverse charge mechanism | xxx | This is for GTA, Legal consultants etc. who has to include this value while arriving at exempt supplies value |

| Add: | Sale of land | xx | |

| Add: | Sale of Building | xx | If the same is not subject to GST as per Para 5(b) to Schedule II to CGST Act. Sale of building subject to GST only when any amount received by builder before issuance of completion certificate |

| Aggregate value of exempt supplies | xxxx |

Where, Total turnover the state means exempt plus taxable value of GST supplies including zero rated and non- GST supplies( of that state only) excluding tax amounts.

3. Working of common credit attributable to supplies used in non –business use (D2):

D2= 5% of common credit. As simple as that!!

Now, when we are able to calculate C2, D1 and D2, we can use the above formula i.e. C2- (D1+D2) to calculate the C3 – Final ITC to be taken removing the ITC attributable to exempt/non business use supplies.

Point to be noted:

1. This C3 has to be calculated separately for CGST, SGST, IGST and UTGST.

This is only to be done for complying with Rule 42.

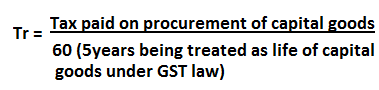

Rule 43: Manner of determination of input tax credit in respect of capital goods and reversal thereof in certain cases.

ITC attributable on capital goods partly used for taxable supplies and partly used for effecting exempt supplies or for non-business use shall be calculated as under:

[In short, the above formula will give us the ITC on common capital goods to be reversed as attributable to use for exempt supplies or/and for non-business use)

Where, Aggregate value of exempted supplies and Total turnover shall be calculated in the similar way as calculated for Rule 42(above)

Such Tr to be calculated for every capital good having common use (i.e. for taxable as well as non –taxable) every month till its life expires or disposed off. upto five years from the date of the invoice for such goods

it is clarified vide Notification No. 16/2020- Central Tax dated March 23, 2020 that w.e.f 01 April 2020 , the useful life of any capital goods shall be considered as five years from the date of invoice and the said formula shall be applicable during the useful life of the said capital goods.”;

Tr to be calculated separately for CGST, SGST, IGST and UTGST.

Formula of reversal as above, also need to be applied separately for CGST, SGST, IGST and UTGST every month.

(Republished with Amendments. Amendments been made by CA Anita Bhadra)

Author Bio

I am trading in seeds-fertilizers and pesticides dealer and seed is exempted and pesticides and fertilizers are taxable so itc reverse in rule 42 in exempted goods thanks

girish patel ob 91-9427370799

we purchase AC and it used in the Office, we manufacture taxable and non-taxble both goods, is it required to revers of ( AC) ITC on prorata base or can take all.

Dealer has identified Purchase against Exempt goods and ITC on purchase is cost of Assessee so not shown in 3B Return as ITC , is to be required to show in 3B as 2A mismatch is very heavy , If we shown this ITC in 3B where in 3B this amount is to be reversed whether under Rule 42 and 43

In rule 42 exempted supply does it include both rcm and no supply please help

Sir, I have purchased hosting from Net4 India. I have paid Rs. 7787 (Value=6599 + 1187 IGST) and I have the tax invoice having my GST number. They have not submitted the GST amount from June 2019. Can you please let me know, how can I claim ITC in 3B?

Very useful article.

Dear Plz Help

I purchase assets in 29-11-2017 and Reversal u/s 43 not made during the year.

My question is

1. Which Total turnover is taken up to November-2017 or March – 2018

2. Supposed I filed GSTR-9 and Reversal shown in GSTR-9 against Total Turnover as on 31/03/2018, So Formula Used:

(Capital Input/60)*Exempt Supply/Total Turnover

Question Arise: Reversal Start from November – 2017 or March -2018

above calculation or section 42 is totally wrong……….who will deduct T4 component for exclusively taxable supples from TOTAL credit……..plz. dont mis guide the public……thanks

WE PURCHASE ONE AIR CONDITIONER FOR OFFICE USE. SHALL WE CLAIM ITC.

One of My client has claimed excess ITC in Nov 2017 GSTR 3B .

Please advise how to rectify this error?