Model GST Audit Manual, Gujarat, 2022

1. INTRODUCTION:

1.1. Purpose of this Manual:

This model GST Audit Manual is intended to be developed as a comprehensive document which would be helpful for the audit officers of the Gujarat State throughout the entire process of selection of taxpayers for audit till the completion of audit in an efficient and effective manner.

Audit selection is a dynamic process where the experience of audit in each year plays a vital role in modifying the selection criteria. However, in GST, ascertaining a risk profile of the Auditees based on a scientific approach is vital for selection of audit. The aspects of such risk profile assessment are also discussed in this manual.

This manual discusses the (i) methods of looking into the aspects that demand meticulous attention, (ii) methods of preparation for an effective desk review before Audit actually commences and (iii) methods for conducting a quality audit under GST that would not only reflect the efficiency of an audit officer but would also successfully achieve the goal of monitoring compliance management and revenue augmentation. The manual has also focused in developing a structure for the vertical hierarchy so that audit officers can place their findings before the appropriate higher authority. This would definitely help the audit officer to prepare a proper audit plan.

Audit in GST would intend to evaluate the credibility of self-assessed tax liability of a taxpayer based on the twin test of accuracy of taxpayer’s declarations and the accounts maintained by the taxpayer. Thus, Audit in GST would have the following twin effects:

- Deterrent effect:

Discovering the areas of deviation is expected to prevent a taxpayer in continuing with such deviations that result in erroneous declaration of self-assessed liability.

- Preventive effect:

Establishment of adverse observations in audit is expected to prevent a taxpayer to repeat any offence.

Audit in GST would intend to verify the correctness of the facts and figures declared in the returns vis-a-vis the books of accounts. It may happen that self-assessed declarations would contain hidden deviations. These deviations may be of the nature of omission, error or deliberate deceptions by a taxpayer. This Audit Manual in GST would surely play a vital role in detection of non-compliances, if any, in the self-assessed declarations.

However, such deviations may also be mere technical in nature without having any real revenue impact. The approach to be adopted in such cases would also be dealt with in this manual.

Finally, audit in GST is desired to be a Audit officer’s work, he/she would conduct the audit and prepare the audit report with the assistance of sub-ordinates. This entire work process would involve a series of activities including preparing desk review to identify the high-risk areas, preparation of a sound audit plan, to accord sanction to the audit plan and conducting of audit within the prescribed time limit.

So, for conducting an effective audit of a selected taxpayer, the audit officer has to be ready with:

| 1 | Ready with a well- drafted pre-plan for Identifying the areas of concern. | What to examine?

How to examine? |

| 2 | Well aware of the procedural aspects. |

|

| 3 | Legal provisions, Law changes, notifications, circulars, rates. |

|

| 4 | Final computation to calculate dues. |

|

Attempt has been made to address the aforesaid issues in this Manual.

However, it is needless to say that there cannot be a uniform approach of audit of every taxpayer. Occasion may arise that a fact or figure apparent on the documents may need an examination with reference to some other sets of documents or even other sources.

Therefore, in a nutshell, audit in GST would have a much-widened perspective.

These issues have all been discussed in detail in this document.

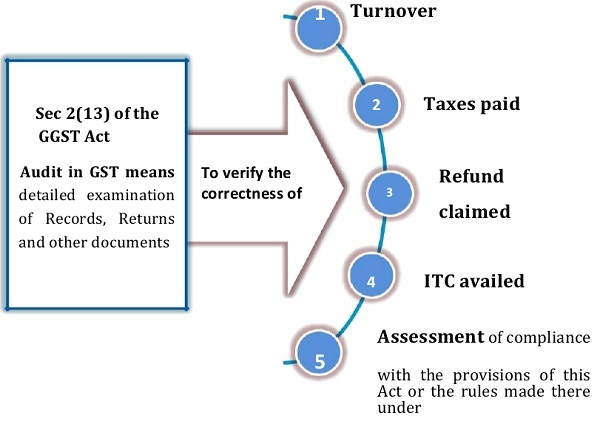

1.2. Definition of audit under GGST Act, 2017:

Audit is defined in sub-sec 13 of sec 2 of the GGST Act, 2017 as –

“detailed examination of records, returns and other documents maintained or furnished by the taxable person under this Act or Rules made thereunder or under any other law for the time being in force to verify, inter alia, the correctness of turnover declared, taxes paid, refund claimed and input tax credit availed, and to assess his compliance with the provisions of this Act or rules made thereunder”.

Hence, GST audit is not restricted to the reconciliation of the tax liability & payment of tax by a taxable person only, but its scope is also extended to assess the compliances with the provisions of the GST laws. Question may arise in the mind of the Audit Officer as to how much scope is there to assess the compliances with the provisions of the GST laws? What are the provisions where compliance checking is required? There are some illustrative examples as follows:

- The approach towards a particular Auditee may vary depending upon the study on that Auditee. The main objective here is to identify the areas where noncompliance or wrong interpretation of the law may have occurred resulting less payment or non-payment of taxes, interest, late fees, etc. Identification of such areas will prevent the Auditee in continuing with such deviations which result in erroneous declaration of self-assessed liability.

2. Types of Audit in GST:

Three types of Audit are prescribed in GST:

1. Audit by Tax Authorities: As per provision of section 65 of the GGST Act, 2017 and as prescribed in rule 101 of the GGST Rules, 2017. This audit is to be conducted by an authorized officer; the power being delegated by the chief commissioner.

2. Special Audit: Special Audit by a chartered / cost accountant, on the order of an officer (not below the rank of Assistant Commissioner), upon prior approval of the Commissioner and appointed by the Commissioner, under section 66 of the GGST Act, 2017 read with rule 102 of the CGST Rules, 2017.

3. Turnover based Audit: Turnover based Audit u/s 35(5) of the GGST Act, 2017 read with rule 80(3) of the GGST Rules, 2017, by a chartered / cost accountant appointed by the RTP, when Aggregate Turnover exceeds prescribed quantum.

Note: This GST Audit Manual is focused towards audit by Tax Authorities only. The audited books of accounts and audit report submitted by the taxpayer in prescribed Form(s) are also subject to audit u/s 65.

3. Legal Provisions of Audit by Tax Authorities

(Legal Provisions under Section 65 of the GGST Acts, 2017 read with the Rules made there-under)

3.1. Provisions under Section 65:

|

Sub- |

Provisions of the Act |

| (1) | The Commissioner or any officer authorized by him/her, by way of a general or a specific order, may undertake audit of any registered person for such period, at such frequency and in such manner as may be prescribed. |

| (2) | The officers referred to in sub-section (1) may conduct audit at the place of business of the registered person or in their office. |

| (3) | The registered person shall be informed by way of a notice not less than fifteen working days prior to the conduct of audit in such manner as may be prescribed. |

| The audit under sub-section (1) shall be completed within a period of three months from the date of commencement of the audit:

Provided that where the Commissioner is satisfied that audit in respect of such registered person cannot be completed within three months, he may, for the reasons to be recorded in writing, extend the period by a further |

|

| (4) | period not exceeding six months.

Explanation. – For the purposes of this sub-section, the expression ‘commencement of audit’ shall mean the date on which the records and other documents, called for by the tax authorities, are made available by the registered person or the actual institution of audit at the place of business, whichever is later. |

| (5) | During the course of audit, the authorized officer may require the registered person,— (i) to afford him/her the necessary facility to verify the books of account or other documents as he/she may require; (ii) to furnish such information as he/she may require and render assistance for timely completion of the audit. |

| (6) | On conclusion of audit, the proper officer shall, within thirty days, inform the registered person, whose records are audited, about the findings, his/her rights and obligations and the reasons for such findings. |

| (7) | Where the audit conducted under sub-section (1) results in detection of tax not paid or short paid or erroneously refunded, or input tax credit wrongly availed or utilized, the proper officer may initiate action under section 73 or section 74. |

3. 2. Provisions under rule 101:

|

Sub- |

Provisions of the Act |

| (1) | The period of audit to be conducted under sub-section (1) of section 65 shall be a financial year or part thereof or multiples thereof. |

| (2) | Where it is decided to undertake the audit of a registered person in accordance with the provisions of section 65, the proper officer shall issue a notice in FORM GST ADT-01in accordance with the provisions of subsection (3) of the said section. |

| (3) | The proper officer authorized to conduct audit of the records and books of account of the registered person shall, with the assistance of the team of officers and officials accompanying him/her, verify the documents on the basis of which the books of account are maintained and the returns and statements furnished under the provisions of the Act and the rules made thereunder, the correctness of the turnover, exemptions and deductions claimed, the rate of tax applied in respect of supply of goods or services or both, the input tax credit availed and utilized, refund claimed, and other relevant issues and record the observations in his audit notes. |

| (4) | The proper officer may inform the registered person of the discrepancies noticed, if any, as observed in the audit and the said person may file his/her reply and the proper officer shall finalize the findings of the audit after due consideration of the reply furnished. |

| (5) | On conclusion of the audit, the proper officer shall inform the findings of audit to the registered person in accordance with the provisions of sub- section (6) of section 65 in FORM GST ADT-02 |

4. Some relevant provisions of GGST Act, 2017 directly or indirectly linked with Audit:

| Sec | Section Heading | Rule /

Notification |

Heading |

| 12 | Time of Supply of Goods | N.N. 66/17 -CT dt,15.11.17 |

Delinking advance payment from time of supply in case of goods. |

| 13 | Time of Supply of Service | ||

| 14 | Time in case of change in rate of tax. | ||

| 15 | Value of Taxable Supply | 27 to 35 | Determination of Value of Supply |

| 16,17,18, 19&20 | Input Tax Credit | 36 to 45 | Rules related to ITC and ISD |

| 31 | Tax Invoice | 46 to 55A | Tax Invoice, Credit and Debit Notes |

| 34 | Credit & Debit Notes | ||

| 35 | Accounts and other records | 56 to 58 | Accounts and Records |

| 44 | Annual Return | 80 | Annual return and Reconciliation Statement (GSTR 9, 9A, 9B, 9C) |

| 49 | Payment of tax, interest, penalty and other amounts. | 85 to 88A | Payment of Tax |

| 50 | Interest | ||

| 54 | Refund of tax | 89 to 97A & updated Circulars(125&1 29 of 2019) |

Refund |

| 71 | Access to business premises | ||

| 73&74 | Determination of tax not paid or short paid | Rule 142 | Demand & Recovery |

| 76 | Tax collected but not paid to the Government | ||

| 77 | Tax wrongly collected and paid to the Central /State Government | ||

| 125 | General Penalty |

4.1. Access to business premises: Section 71 –

“(1) Any officer under this Act, authorized by the proper officer not below the rank of Joint Commissioner, shall have access to any place of business of a registered person to inspect books of account, documents, computers, computer programmes, computer software whether installed in a computer or otherwise and such other things as he may require and which may be

available at such place, for the purposes of carrying out any audit, scrutiny, verification and checks as may be necessary to safeguard the interest of revenue.

(2) Every person in charge of place referred to in sub-section (1) shall, on demand, make available to the officer authorized under sub-section (1) or the audit party deputed by the proper officer or a cost accountant or chartered accountant nominated under section 66––

(i) such records as prepared or maintained by the registered person and declared to the proper officer in such manner as may be prescribed;

(ii) trial balance or its equivalent;

(iii) statements of annual financial accounts, duly audited, wherever required;

(iv) cost audit report, if any, under section 148 of the Companies Act, 2013;

(v) the income-tax audit report, if any, under section 44AB of the Income Tax Act, 1961; and

(vi) any other relevant record,

for the scrutiny by the officer or audit party or the chartered accountant or cost accountant within a period not exceeding fifteen working days from the day when such demand is made, or such further period as may be allowed by the said officer or the audit party or the chartered accountant or cost accountant.”

> Such access includes online access of books of accounts.

4.2. Officers to assist proper officers:

Section 72 –

“(1) All officers of Police, Railways, Customs, and those officers engaged in the collection of land revenue, including village officers, officers of central tax and officers of the Union territory tax shall assist the proper officers in the implementation of this Act.

(2) The Government may, by notification, empower and require any other class of officers to assist the proper officers in the implementation of this Act when called upon to do so by the Commissioner.

4.3. Determination of tax not paid or short paid or erroneously refunded or input tax credit wrongly availed or utilized for any reason other than fraud or any willful misstatement or suppression of facts:

Section 73 –

Sec 73 is applicable when there are no reasons of fraud or any willful misstatement or suppression of facts to evade tax

“(1) Where it appears to the proper officer that any tax has not been paid or short paid or erroneously refunded, or where input tax credit has been wrongly availed or utilized for any reason, other than the reason of fraud or any willful misstatement or suppression of facts to evade tax, he shall serve notice on the person chargeable with tax which has not been so paid or which has been so short paid or to whom the refund has erroneously been made, or who has wrongly availed or utilized input tax credit, requiring him/her to show cause as to why he/she should not pay the amount specified in the notice along with interest payable thereon under section 50 and a penalty leviable under the provisions of this Act or the rules made thereunder.

(2) The proper officer shall issue the notice under sub-section (1) at least three months prior to the time limit specified in sub-section (10) for issuance of order.

(3) Where a notice has been issued for any period under sub-section (1), the proper officer may serve a statement, containing the details of tax not paid or short paid or erroneously refunded or input tax credit wrongly availed or utilized for such periods other than those covered under sub-section (1), on the person chargeable with tax.

(4) The service of such statement shall be deemed to be service of notice on such person under sub-section (1), subject to the condition that the grounds relied upon for such tax periods other than those covered under sub-section (1) are the same as are mentioned in the earlier notice.

(5) The person chargeable with tax may, before service of notice under subsection (1) or, as the case may be, the statement under sub-section (3), pay the amount of tax along with interest payable thereon under section 50 on the basis of his own ascertainment of such tax or the tax as ascertained by the proper officer and inform the proper officer in writing of such payment.

(6) The proper officer, on receipt of such information, shall not serve any notice under sub-section (1) or, as the case may be, the statement under sub-section (3), in respect of the tax so paid or any penalty payable under the provisions of this Act or the rules made thereunder.

(7) Where the proper officer is of the opinion that the amount paid under subsection (5) falls short of the amount actually payable, he/she shall proceed to issue the notice as provided for in sub-section (1) in respect of such amount which falls short of the amount actually payable.

(8) Where any person chargeable with tax under sub-section (1) or sub-section (3) pays the said tax along with interest payable under section 50 within thirty days of issue of show cause notice, no penalty shall be payable and all proceedings in respect of the said notice shall be deemed to be concluded.

(9) The proper officer shall, after considering the representation, if any, made by person chargeable with tax, determine the amount of tax, interest and a penalty equivalent to ten per cent. of tax or ten thousand rupees, whichever is higher, due from such person and issue an order.

(10) The proper officer shall issue the order under sub-section (9) within three years from the due date for furnishing of annual return for the financial year to which the tax not paid or short paid or input tax credit wrongly availed or utilized relates to or within three years from the date of erroneous refund.

(11) Notwithstanding anything contained in sub-section (6) or sub-section (8), penalty under sub-section (9) shall be payable where any amount of self-assessed tax or any amount collected as tax has not been paid within a period of thirty days from the due date of payment of such tax.”

4.4. Determination of tax not paid or short paid or erroneously refunded or input tax credit wrongly availed or utilized by reasons of fraud or any willful misstatement or suppression of facts:

Section 74 –

“(1) Where it appears to the proper officer that any tax has not been paid or short paid or erroneously refunded or where input tax credit has been wrongly availed or utilized by reason of fraud, or any willful misstatement or suppression of facts to evade tax, he shall serve notice on the person chargeable with tax which has not been so paid or which has been so short paid or to whom the refund has erroneously been made, or who has wrongly availed or utilized input tax credit, requiring him/her to show cause as to why he/she should not pay the amount specified in the notice along with interest payable thereon under section 50 and a penalty equivalent to the tax specified in the notice.

Sec 74 is applicable when there are reasons of fraud or any willful misstatement or suppression of facts to evade tax

(2) The proper officer shall issue the notice under sub-section (1) at least six months prior to the time limit specified in sub-section (10) for issuance of order.

(3) Where a notice has been issued for any period under sub-section (1), the proper officer may serve a statement, containing the details of tax not paid or short paid or erroneously refunded or input tax credit wrongly availed or utilized for such periods other than those covered under sub-section (1), on the person chargeable with tax.

(4) The service of statement under sub-section (3) shall be deemed to be service of notice under sub-section (1) of section 73, subject to the condition that the grounds relied upon in the said statement, except the ground of fraud, or any willful-misstatement or suppression of facts to evade tax, for periods other than those covered under subsection (1) are the same as are mentioned in the earlier notice.

(5) The person chargeable with tax may, before service of notice under sub-section (1), pay the amount of tax along with interest payable under section 50 and a penalty equivalent to fifteen per cent. of such tax on the basis of his own ascertainment of such tax or the tax as ascertained by the proper officer and inform the proper officer in writing of such payment.

(6) The proper officer, on receipt of such information, shall not serve any notice under sub-section (1), in respect of the tax so paid or any penalty payable under the provisions of this Act or the rules made thereunder.

(7) Where the proper officer is of the opinion that the amount paid under subsection (5) falls short of the amount actually payable, he shall proceed to issue the notice as provided for in sub-section (1) in respect of such amount which falls short of the amount actually payable.

(8) Where any person chargeable with tax under sub-section (1) pays the said tax along with interest payable under section 50 and a penalty equivalent to twenty-five per cent. of such tax within thirty days of issue of the notice, all proceedings in respect of the said notice shall be deemed to be concluded.

(9) The proper officer shall, after considering the representation, if any, made by the person chargeable with tax, determine the amount of tax, interest and penalty due from such person and issue an order.

(10) The proper officer shall issue the order under sub-section (9) within a period of five years from the due date for furnishing of annual return for the financial year to which the tax not paid or short paid or input tax credit wrongly availed or utilized relates to or within five years from the date of erroneous refund. Determination of tax not paid or short paid or erroneously refunded or input tax credit wrongly availed or utilized by reason of fraud or any willful misstatement or suppression of facts.

(11) Where any person served with an order issued under sub-section (9) pays the tax along with interest payable thereon under section 50 and a penalty equivalent to fifty per cent. of such tax within thirty days of communication of the order, all proceedings in respect of the said notice shall be deemed to be concluded.

Explanation 1.—For the purposes of section 73 and this section, —

(i) the expression “all proceedings in respect of the said notice” shall not include proceedings under section 132;

(ii) where the notice under the same proceedings is issued to the main person liable to pay tax and some other persons, and such proceedings against the main person have been concluded under section 73 or section 74, the proceedings against all the persons liable to pay penalty under sections122, 125, 129 and 130 are deemed to be concluded.

Explanation 2.––For the purposes of this Act, the expression “suppression” shall mean non-declaration of facts or information which a taxable person is required to declare in the return, statement, report or any other document furnished under this Act or the rules made thereunder, or failure to furnish any information on being asked for, in writing, by the proper officer.”

4.5. General provisions relating to determination of tax:

Section 75 –

“(1) Where the service of notice or issuance of order is stayed by an order of a court or Appellate Tribunal, the period of such stay shall be excluded in computing the period specified in sub-sections (2) and (10) of section 73 or sub-sections (2) and (10) of section 74, as the case may be.

(2) Where any Appellate Authority or Appellate Tribunal or court concludes that the notice issued under sub-section (1) of section 74 is not sustainable for the reason that the charges of fraud or any willful misstatement or suppression of facts to evade tax has not been established against the person to whom the notice was issued, the proper officer shall determine the tax payable by such person, deeming as if the notice were issued under sub-section (1) of section 73.

(3) Where any order is required to be issued in pursuance of the direction of the Appellate Authority or Appellate Tribunal or a court, such order shall be issued within two years from the date of communication of the said direction.

(4) An opportunity of hearing shall be granted where a request is received in writing from the person chargeable with tax or penalty, or where any adverse decision is contemplated against such person.

(5) The proper officer shall, if sufficient cause is shown by the person chargeable with tax, grant time to the said person and adjourn the hearing for reasons to be recorded in writing: Provided that no such adjournment shall be granted for more than three times to a person during the proceedings.

(6) The proper officer, in his order, shall set out the relevant facts and the basis of his decision.

(7) The amount of tax, interest and penalty demanded in the order shall not be in excess of the amount specified in the notice and no demand shall be confirmed on the grounds other than the grounds specified in the notice.

(8) Where the Appellate Authority or Appellate Tribunal or court modifies the amount of tax determined by the proper officer, the amount of interest and penalty shall stand modified accordingly, taking into account the amount of tax so modified.

(9) The interest on the tax short paid or not paid shall be payable whether or not specified in the order determining the tax liability.

(10) The adjudication proceedings shall be deemed to be concluded, if the order is not issued within three years as provided for in sub-section (10) of section 73 or within five years as provided for in sub-section (10) of section 74.

(11) An issue on which the Appellate Authority or the Appellate Tribunal or the High Court has given its decision which is prejudicial to the interest of revenue in some other proceedings and an appeal to the Appellate Tribunal or the High Court or the Supreme Court against such decision of the Appellate Authority or the Appellate Tribunal or the High Court is pending, the period spent between the

date of the decision of the Appellate Authority and that of the Appellate Tribunal or the date of decision of the Appellate Tribunal and that of the High Court or the date of the decision of the High Court and that of the Supreme Court shall be excluded in computing the period referred to in sub-section (10) of section 73 or sub-section (10) of section 74 where proceedings are initiated by way of issue of a show cause notice under the said sections.

(12) Notwithstanding anything contained in section 73 or section 74, where any amount of self-assessed tax in accordance with a return furnished under section 39 remains unpaid, either wholly or partly, or any amount of interest payable on such tax remains unpaid, the same shall be recovered under the provisions of section 79.

(13) Where any penalty is imposed under section 73 or section 74, no penalty for the same act or omission shall be imposed on the same person under any other provision of this Act.”

4.6. Tax collected but not paid to the Government:

Section 76 –

“(1) Notwithstanding anything to the contrary contained in any order or direction of any Appellate Authority or Appellate Tribunal or court or in any other provisions of this Act or the rules made thereunder or any other law for the time being in force, every person who has collected from any other person any amount as representing the tax under this Act, and has not paid the said amount to the Government, shall forthwith pay the said amount to the Government, irrespective of whether the supplies in respect of which such amount was collected are taxable or not.

(2) Where any amount is required to be paid to the Government under sub-section (1) , and which has not been so paid, the proper officer may serve on the person liable to pay such amount a notice requiring him/her to show cause as to why the said amount as specified in the notice, should not be paid by him/her to the Government and why a penalty equivalent to the amount specified in the notice should not be imposed on him/her under the provisions of this Act.

(3) The proper officer shall, after considering the representation, if any, made by the person on whom the notice is served under sub-section (2), determine the amount due from such person and thereupon such person shall pay the amount so determined.

(4) The person referred to in subsection (1) shall in addition to paying the amount referred to in sub-section (1) or sub-section (3) also be liable to pay interest thereon at the rate specified under section 50 from the date such amount was collected by him/her to the date such amount is paid by him/her to the Government.

(5) An opportunity of hearing shall be granted where a request is received in writing from the person to whom the notice was issued to show cause.

(6) The proper officer shall issue an order within one year from the date of issue of the notice.

(7) Where the issuance of order is stayed by an order of the court or Appellate Tribunal, the period of such stay shall be excluded in computing the period of one year.

(8) The proper officer, in his order, shall set out the relevant facts and the basis of his decision.

(9) The amount paid to the Government under sub-section (1) or sub-section (3) shall be adjusted against the tax payable, if any, by the person in relation to the supplies referred to in sub-section (1).

(10) Where any surplus is left after the adjustment under sub-section (9), the amount of such surplus shall either be credited to the Fund or refunded to the person who has borne the incidence of such amount.

(11) The person who has borne the incidence of the amount, may apply for the refund of the same in accordance with the provisions of section 54.

4.7. Tax wrongfully collected and paid to the Central Government or State Government:

Section 77 –

(1) A registered person who has paid the central tax and State tax on a transaction considered by him/her to be an intra-State supply, but which is subsequently held to be an inter-State supply, shall be refunded the amount of taxes so paid in such manner and subject to such conditions as may be prescribed.

(2) A registered person who has paid integrated tax on a transaction considered by him/her to be an inter-State supply, but which is subsequently held to be an intra-State supply, shall not be required to pay any interest on the amount of State tax payable.

4. 8. Initiations of recovery proceedings:

Section 78 –

“Any amount payable by a taxable person in pursuance of an order passed under this Act shall be paid by such person within a period of three months from the date of service of such order failing which recovery proceedings shall be initiated:

Provided that where the proper officer considers it expedient in the interest of revenue, he may, for reasons to be recorded in writing, require the said taxable person to make such payment within such period less than a period of three months as may be specified by him/her.”

4. 9. Levy of late fee:

Section 47 –

“(1) Any registered person who fails to furnish the details of outward or inward supplies required under section 37 or section 38 or returns required under section 39 or section 45 by the due date shall pay a late fee of one hundred rupees for every day during which such failure continues subject to a maximum amount of five thousand rupees.

(2) Any registered person who fails to furnish the return required under section 44 by the due date shall be liable to pay a late fee of one hundred rupees for every day during which such failure continues subject to a maximum of an amount calculated at a quarter per cent. of his turnover in the State.”

4.10. Interest on delayed payment of tax:

Section 50 –

“(1) Every person who is liable to pay tax in accordance with the provisions of this Act or the rules made thereunder, but fails to pay the tax or any part thereof to the Government within the period prescribed, shall for the period for which the tax or any part thereof remains unpaid, pay, on his own, interest at such rate, not exceeding eighteen per cent., as may be notified by the Government on the

recommendations of the Council.

Provided that the interest on tax payable in respect of supplies made during a tax period and declared in the return for the said period furnished after the due date in accordance with the provisions of section 39, except where such return is furnished after commencement of any proceedings under section 73 or section 74 in respect of the said period, shall be levied on that portion of the tax that is paid by debiting the electronic cash ledger. [Proviso inserted on 01.09.2020 w-e-f 01.07.2017]

(2) The interest under sub-section (1) shall be calculated, in such manner as may be prescribed, from the day succeeding the day on which such tax was due to be paid.”

4.11. General penalty:

Section 125 –

“Any person, who contravenes any of the provisions of this Act or any rules made thereunder for which no penalty is separately provided for in this Act, shall be liable to a penalty which may extend to twenty five thousand rupees.”

5. Obligation of the Auditee

During the course of audit, the authorized officer may ask the registered person, to provide the necessary facility to verify the books of account or other documents as he may require, and to furnish such information as he may require and render assistance for timely completion of audit.

[Sec 65(5)].

6. Dealing with the Auditee:

The main objective of audit is to quantify shortfall of revenue in a cost effective and transparent manner. The attitude of the officer conducting audit should reflect this. He should be aware that he is the main channel of communication between the department and the Auditee.

The officer conducting audit should maintain a good professional relationship with the registered taxable person (herein after referred to as the RTP). He should recognize the rights of the RTP, such as, uniform and transparent application of law and his right to be treated with courtesy and consideration. He should explain that a tax compliant RTP may reap a number of benefits from an

audit such as: –

i). They will be better equipped to comply with the laws and the relevant procedures;

ii). The preparation of prescribed returns and self-assessment of Goods and Services Tax will be better focused, correct and complete;

iii). The scrutiny of business accounts and returns submitted to various authorities, made in the course of audit would help in removing any deficiency in their accounting and internal control systems;

iv). Disputes and proceedings against them would be substantially reduced or even eliminated.

7. Principles of audit

The objective of audit is also to measure the level of compliance of the RTP in light of the provisions of the GST Act and the rules made there under. It should be consistent with the Notifications/Circulars/Orders issued.

The basic principles of audit

i). Adherence to risk factors identified by the Commissioner.

ii). Consistency with Departmental Circulars and using Professional methodology.

iii). Chalking out a sound prior-audit plan/audit program and conducting the audit accordingly.

iv). Emphasizing a systematic, flexible as well as penetrative audit.

v). Regular review of the audit plan and progress and modification of the audit program whenever necessary.

vi). Concentrating on scrutiny of records, the degree of which will depend on the identified risk areas.

vii). Identification of the veracity of Turnover declared, Taxes paid, Refund claimed and received, Input Tax Credit availed,

assessment of his compliances as per the provisions of the GST Act and the Rules made there-under.

viii). Recording of the proceedings of audit and findings thereof.

ix). Providing opportunity to the Auditee to be heard and to submit his contention

8. Pre-requisites of an audit officer conducting audit

- The officer should have a primary knowledge about the business & business pattern of the RTP with respect to the particular trade & industry.

- Officer should also be well aware of the existing trade practices, conventions and market trends.

- Section 133 of the Companies Act, 2013 read with Rule 7 of the Companies (Accounts) Rules, 2014 provides that the Final Accounts should comply with the Accounting Standards. The knowledge of the prevalent Indian Accounting Standards will help the audit officer in the examination of books of accounts.

- Officer should take an unbiased and judicious approach in the course of audit.

- An Audit Officer should be tactful to gain the goodwill and confidence of the RTP. He is expected to play the role of motivator ensuring voluntary compliance by the RTP.

- Technical lapses by the RTP which do not have any revenue implication, and have occurred due to oversight or ignorance, may be ignored on merit. However, any such incidence upon being detected should also be noted down in the course of audit.

- An Audit Officer should apprise the RTP of the provisions of the GST Acts and encourage him/her to make voluntary payment in the course of audit.

- An Audit Officer should be transparent in his actions. Before drawing the Final AuditReport, the discrepancies found upon audit should be communicated to the Auditee. The Auditee should be allowed due opportunity for filing his explanation in respect of such discrepancies as intimated by the Audit Officer. The Audit Officer should consider all the explanations and documents provided by the RTP, regarding the points of dispute, before drawing of the Final

Audit Report. - If necessary, Officer may consult Auditee’s immediate functional head to resolve any issue in the course of the audit. Where there is lack of co-operation or deliberate failure to provide information and records by the RTP or in case of other exigency, the audit officer should inform RTP’s immediate superior and follow it up by a written report, if necessary.

- Officer should preserve all the important documents submitted by the Auditee in the course of audit which is relevant to findings as office records preferably in electronic format.

- Confidentiality should be maintained in respect of sensitive and confidential information furnished, in the course of audit.

9. Audit flow chart:

1. Audit Selection: Commissioner may select any registered person for audit for a financial year or part or multiple thereof.

2. Allotment of selected RTP: The selected RTPs will be assigned to the departmental authorities.

3. Issuance of notice for audit: The audit officer will issue FORM GST ADT – 01 fixing date of hearing for audit, at least 15 working days in advance prior to the conduct of audit.

4. Prior-audit desk review: Basic ground work to chalk out the nature in which the audit will progress.

5. Commencement of audit: The date on which the records /documents, called for are made available by the registered person or the actual institution of audit at the place of business.

6. Preparation and approval of audit plan: Based on desk review, audit officer will prepare an audit plan and get the same approved.

7. Examination: In-depth checking of the records /documents/ books made available by the registered person during audit.

8. Communication of discrepancies found: The observations made upon audit are to be communicated to the Auditee in writing. The Auditee should be allowed due opportunity for filing his explanation in respect of such discrepancies as intimated.

9. Preparation and approval of Draft Audit Report (DAR): Drawing a DAR containing the observations made upon audit after considering explanations & documents provided by the Auditee in respect of such discrepancies and get the same approved as per extant circulars issued by the Department.

10. Preparation of Final Audit Report: After approval, a final report is to be drawn and issued to the Auditee

11. Audit consequences: i. Closure of audit (in case the observations are admitted by the RTP and the amount short paid as indicated is paid) or ii. Initiation of demand and recovery proceedings by issuance of show cause notice u/s. – 73/74

10. Different Steps of audit:

10.1. Selection for audit –

As per the provisions of section 65(1) read with rule 101(1), the Commissioner or any officer authorized by him/her, by way of a general or a specific order, may undertake audit of any registered person for a financial year or part thereof or multiples thereof.

The principle of audit envisages selection of taxpayers for audit based on certain risk parameters. The Commissioner by a general or specific order may select any registered person for audit of his books of accounts for a specific period.

The Commissioner may fix the criteria of selection based on certain parameters as he may deem fit. Given the large number of registered taxpayers under GST, it is neither possible nor desirable to subject every taxpayer to audit each year with the available resources. Further, emphasis placed merely on coverage of more number of assesses and taxpayers would dilute the quality of audit and would be against the principles of GST, which is based on trust / voluntary compliance by the tax payers. Selection of taxpayers for audit in a scientific manner is extremely important as it permits the efficient use of audit resources viz. manpower and skills for achieving effective audit results. These taxpayers should be selected on the basis of assessment of the risk to revenue. This process, which is an essential feature of audit selection, is known as ‘Risk Evaluation’.

Certain representative selection criteria are stated as below:

- Selection based on Return related Risk Parameters: The list of potential high risk taxpayers may be prepared by selecting one or multiple criteria under different major risk heads from the available options, viz. :

Specific benchmarks may be fixed against the risk criteria for each of the above major heads such as:

a) Normal taxpayers, i.e. the taxpayers who are required to file Form GSTR- 3B and Form GSTR-1, may be selected.

b) Those tax-payers who have filed at least 06 (selection criteria for 2017-18) & 09 (selection criteria for each subsequent year) Form GSTR-3B in the financial year may be selected (department may select otherwise also).

c) The taxpayers’ pool may be divided into 3 segments namely Large, Medium & Small based on turnover in the State.

d) All risk parameters are required to be identified and all probable aspects need to be considered to identify non-compliance and non-payment / short payment of tax, interest, late fee, penalty etc and evasion of tax.

e) To select the tax payers for audit in an effective manner, secondary data source (such as VAT/Service Tax/Central Excise/Custom data, Income Tax data etc.) may be considered along with the primary data source (i.e. GST data).

f) The weightage of each parameter may vary depending upon its importance in selection of taxpayers for audit.

g) Based on the average weight considering all the parameters, a final score may be calculated on the basis of which the final selection may be done.

- Entity level risks (e.g. Turnover, Tax, ITC, Refund, Commodity such as Iron & Steel, Paints & Chemicals, Textiles, Cement, Medicine, Footwear, Branded food grain, Automobiles etc., Service: Works contract, Real Estate, Information Technology, Consultancy service, Manpower service, Hospitality, Travel & Tourism, Leasing etc).

- Risks associated with compliance behavior (e.g. late filer of return, non-submission of Form GSTR-1, Form GSTR-3B, Form GSTR-9 & Form GSTR-9C).

- Various ratios, g.

- Taxable turnover: Exempted turnover

- Output tax : Input tax

- Cash payment: Output tax

- Set-of using e-credit ledger : Set-of using e-cash ledger

- Inter-state supply: Intra-state supply etc.

- Exceptional Reports e.g.

> ITC claimed in Form GSTR-3B vs. ITC auto-populated in Form GSTR-2A/2B.

> Turnover declared in Form GSTR-3B vis-à-vis Form GSTR-1.

> Claim of ITC from cancelled RTPs, aggregate turnover in GST return vis-àvis Turnover disclosed in Income Tax return/Balance sheet.

> Turnover declared by RTP in Form GSTR3B compared to turnover on which TDS deducted as reflected in Form GSTR-7 submitted by TDS deductor.

> Turnover declared by RTP in Form GSTR-3B compared to turnover on which TCS collected as reflected in Form GSTR-8 submitted by TCS collector.

> Refund claimed against purchase from taxpayer having no auto-population of ITC in Form GSTR-2A/2B.

> Purchases from non-existent/cancelled/ab-initio cancelled RTPs.

> RTPs having adverse reports in VAT/Service Tax/Central Excise who are operative in GST etc.).

(The selection parameters are indicative and general in nature and the same are subject to change)

h) A certain percent of the selection of the tax payer may be done on random basis as well as considering local parameters.

Theme based audits

Issue based audits at state level may also be conducted in a co-ordinated manner based on a systematic and methodical risk analysis of internal data of taxpayer, economic indicators, third party information from tax and other regulatory authorities and other relevant sources of data. The issue for the audit could be a sensitive commodity/Service or any transaction involved. Theme based audits or sectoral audits may also be conducted.

10.2.Suo-moto selection: If an officer comes across any specific information relating to a RTP and has specific reasons to believe that Audit of the said RTP’s books of accounts is required to be done for one or more financial years, or, if any audit officer in the course of audit has specific reasons to believe that an observation made upon audit will have revenue impacts in other periods also, he may send a proposal in this regard to the Commissioner. Similarly, an audit officer or his/her higher authority can propose for any taxpayer to be selected by the Commissioner for audit upon mentioning adequate reasons. The proposal in all cases from field formations should have reasons/ justification for selection of case for audit along-with recommendation/comments of the supervisory/ Divisional Joint Commissioner of State tax. The Commissioner upon consideration of all such proposals may select some/all of such RTPs for audit.

10.3. Allotment of selected RTP –

As per provisions of sec 65(1) read with rule 101(1), any officer who is authorized by the Commissioner has the power to audit.

If the HQ feels that audit for a particular taxpayer need not to be carried out, the case can be dropped. In order to drop an audit case, proper and adequate reasons are required to be given along with any document in support of such reasons for dropping the same.

After the audit selection, the list of selected RTPs may be made available to the respective officers through the proper hierarchy.

10.4. Allocation of Taxpayer of Divisional Audit Head:

- The selected cases are required to be allocated to the audit officers.

- In case of already allocated Taxpayer(s), if the authority wants to modify the audit officer, he/she may do so after recording reasons for such change.

10.5. ASSIGNMENT OF CASES AND SUBORDINATES FOR AUDIT:

- After allocation, the next step is to assign the selected taxpayer to the Audit Officer, who will finally carry out the audit. Normally, such assignment will be done by the HQ officer. However, the same functionality has also been provided to the Divisional officer. So, the HQ officer, if he/she desires, can also assign the Audit Officer and subordinate staff on his/her own.

- The allocating officer can fetch a list of allocated taxpayers that are pending for assignment. The allocation process involves the following steps:-

> Assign Audit Officer– The HQ/Divisional Officer, while assigning a Taxpayer for Audit to a particular ‘Audit officer’ can view the existing assignments i.e. category wise (large, medium & small) number of audit cases assigned to that particular Audit officer. This will help them to assign taxpayers keeping in view the existing workload on an audit officer and thereby maintain uniformity in workload on the audit officers in his/her jurisdiction. At any stage, if a need of change of Audit officer arises, the same can be done through the system by reassigning such role to another officer.

> Assign Audit Officer’s subordinates – After assigning the Audit officer, the HQ/Divisional officer can go ahead with assigning the subordinate Members who may or may not be working directly under that Audit officer. The names of the available subordinates along with their designation and existing work allocation will also be viewed on system and maintaining uniformity in work allocation, subordinate staff can also be assigned. If needed, subordinates can also be changed with other available staff.

10.6. Issuance of Notice in FORM GST ADT-01:

Once the RTP is allotted to a particular Audit officer, a notice for commencement of audit is to be issued to the Auditee in FORM GST ADT-01.

Intimation of audit is to be issued to the taxable person at least 15 days in advance prior to the conduct of audit, by way of a notice, in FORM GST ADT-01. [Sec 65(3), Rule 101(2)].

The format of Form GST ADT-01 is provided in this manual as Annexure- 1

Form GST ADT–01 preferably be issued within fifteen (15) working days of allotment of files to an Audit officer.

It has been observed from the past experience that asking for all the books of accounts and records from an Auditee with a large volume of business on the very first day of audit causes inconvenience for both the Auditee and the auditor.

It is difficult for an audit officer to examine all the documents with equal importance on one single occasion by all practical purposes.

As a result, it would be prudent to ask a RTP to keep all his Books of Accounts and records ready to be made available for examination during the course of audit and to produce those in a staggered manner as decided by the audit officer. For example, the Audit Officer may ask for the first set of documents on the first day of hearing which is required for a thorough study of the annual business performances of the RTP, by issuing a separate letter along with the FORM GST ADT-01. This will help the Audit officer to chalk out an effective audit plan.

However, in cases, where the volume of business is not significant, the relevant documents and records may be asked to be produced on the first day of hearing as scheduled in FORM GST ADT-01.

Furthermore, the Audit Officer may send –

- a letter seeking mutual assistance to complete the audit in focused manner (Annexure -2)

- a questionnaire to the RTP for production of the same upon being filled up, before the audit Officer(Annexure -3)

- a list showing statements, summary, documents and records may be asked for on the date specified by the Audit Officer as per FORM GST ADT- 01(Annexure -4).

This questionnaire will help both the Auditee and auditor to complete the audit process in a focused and planned manner.

This is needless to say that the questionnaire will change according to the need of the concerned case. The questionnaire should be issued as attachment with ADT – 01.

The following set of documents and records pertaining to a financial year (or part of it) may be called for on the first date of Audit: –

- Annual report and Director’s report for the FY …………

- Profit & Loss A/c, trial balance, cash flow statements for the year ended on 31st March…

- Balance Sheet with its notes as they stood on 31st March …

- Auditor’s Notes to the A/c for the FY …………………

- If GSTR -9C is not submitted for the period under audit then Trial Balance (it is applicable where the RTP has multiple GSTIN)

- Consolidated statement (party-wise total for the period under audit) of inward & outward supplies including exempted and non-GST supply:

- List of HSN code of goods and SAC of services in respect of your supply.

- Reconciliation statement in respect of Turnover as disclosed in GSTR 3B and GSTR 1 and as per books of accounts.

- ITC as claimed in GSTR 3B and as auto populated in GSTR-2A/2B

On production of such documents and records by the RTP on the first date of audit as per FORM GST ADT-01, audit will commence and the Audit officer will start chalking out his audit plan.

The remaining books of accounts, ledgers, statements, documents, records etc may be asked from time to time on the basis of the audit plan in the respective case. A letter may be attached/uploaded with the ADT – 01 along with the questionnaire.

10. 7. Prior to audit, desk review –

This is the first phase of the audit programme done in the office by the audit officer. This process needs to be completed by the Audit Officer on the first date of appearance of the Auditee as per FORM GST ADT-01. The idea behind this process is that the Audit Officer would get accustomed with the nature of business of the Auditee vis-a-vis the information available with him/her. In this context, the Department may provide certain information relating to the selected RTP in format named as “Tax payer at a Glance (TAG)”.

This TAG will contain the basic profiling of the selected RTP in respect of registration, return, ITC, payment of tax, EWB utilization and any other pertinent information (e.g. exceptional reports). The officer can also examine the GSTR 9 & GSTR 9C and Balance Sheet, if available.

Upon studying this information as made available, the officer should be well accustomed with the following: –

- Reason(s) for selection.

- Profile of the Auditee with details of ownership, numbers of registered person under the same PAN within the State, principal and additional places of business, migration status (if any), business trend and compliance level of the RTP in the pre-GST period as well as in the GST regime, business trend of the RTP vis-a-vis the trends of the industry etc.

- Broad types of supply involved (i.e., resale, manufacturing, export, import, service, works contract, job work, ISD, etc).

- Business pattern of the Auditee i.e. nature of goods and/or services dealt along with classification (e.g. importer of medicine, exporter of leather goods, reseller of iron & steel, manufacturer of jute goods, restaurant service, manpower supply, travel agent, aviation, transport, etc).

- Return filing & tax compliance pattern of the Auditee in GST for the period under audit. If irregularity is found in case of submission of Return, the Audit Officer should calculate the Late Fees & Interest payable at the desk-review stage itself. Furthermore, there may be chances of mismatch of Turnover and Tax as disclosed in Form GSTR-3B vis-à-vis Form GSTR-1. Similarly, there may be a mismatch between ITC claimed in Form GSTR-3B vis-à-vis ITC auto-populated in Form GSTR-2A.

- Analysis of business operations as declared by the Auditee in the GST Returns in light of other data sources available in the GST portal itself. The Audit Officer should verify the turnover declared by the RTP in the GSTR Returns for the concerned period vis-à-vis footprint of payments made to the RTP as per GSTR-7 or GSTR-8 filed by TDS deductors or TCS collectors, as the case may be. The Audit Officer should also consult the various exceptional reports made available.

- Analysis of business operations as declared by the Auditee in the GST Returns in light of secondary data sources, e.g. turnover declared by the RTP in the GSTR Returns for the concerned period vis-à-vis the turnover declared in income tax return(s)/tax audit report or any other source, if available.

- An audit officer is required to study each case from a holistic point of view of applicability of statutory provisions and amendments thereof, notifications, circulars and orders, advance rulings and various court decisions relevant for the audit period. There are various instances where a specific transaction when looked from a wider perspective, yielded interesting conclusions. Many of these instances are covered by various clarificatory Circulars issued both by the Central Government and the State Government.

- An illustrative list of some of the specific transactions demanding a different look which are clarified by various Circulars is given below. This list is merely indicative and certainly not exhaustive.

So, it is desirable that an Audit Officer will be prudent enough to:

- Read the entire original document as available in various public domains,

- Understand the reasons and contexts of such clarifications,

- Cite any relevant portion of the clarification from such original document only and not from any truncated reference.

Some examples of interesting issues covered under various Circulars and orders passed by Advance Ruling Authorities:

1. A reseller is returning time expired goods to his distributor. Suppose, both the reseller and the distributor are registered as normal tax payers.

If, in the supply chain someone destroys the expired goods what will be the treatment in GST? If the reseller in above example is under composition scheme or unregistered person then what are the processes?

So, many questions may arise. Circular No. 72/46/2018-GST dt.26.10.2018 clarifies some of these aspects.

2. During audit the officer noticed that Mr. X is an independent director of the Auditee to whom the company paid Rs.1.5 Cr. as yearly remuneration. Whether this remuneration is leviable to GST?

The services provided by the directors who are not the employees of the company are outside the scope of Schedule III of the GGST Act and are therefore taxable. In terms of entry at Sl. No. 6 of the Table annexed to notification No. 13/2017 – CT (R) dated 28.06.2017, the recipient of the said services i.e. the Company, is liable to discharge the applicable GST on it on reverse charge basis. Clarification in Circular No: 140/10/2020 – GST dt. 10.06.2020 is relevant for audit officers in this case.

3. ABC Printers has made supplies against two different printing orders:

a. Printing of brochures of a real-estate company where only the content is provided by the real-estate company.

b. Printing of envelopes and letter pads with the logo of the developer. Whether the above supplies are supplies of goods or service?

The first case is a composite supply of goods (paper, ink) as well as services (printing) where printing of the content supplied by the recipient of supply is the principal supply. Hence, tax in this case will be guided by the tax rate of printing services.

Clarification in Circular No: 11/11/2017-GST dated: 20.10.2017

In the second case too, the printing has been made as a part of composite supply, but the supply of printing of the content supplied by the recipient of supply is ancillary to the principal supply of goods. Therefore, in the second case, the tax rate of goods will prevail.

4. Fabrication of buses may involve the following two situations:

a) Bus body builder builds a bus, working on the chassis owned by him and supplies the built-up bus to the customer.

b) Bus body builder builds body on chassis provided by the principal for body building.

Whether the above supplies are supply of goods or service?

In the above context, for situation (a) above, the supply made is that of bus, and accordingly supply would attract GST@ 28%. In situation (b) above, fabrication of body on chassis provided by the principal (not on account of bodybuilder), the supply would be treated as service, and 18% GST as applicable will be charged accordingly.

5. Popcorn is available in packets both as ready to eat and ready to fry. Whether GST rate is same in both the cases?

A packet of corn, which needs to be heated before eating would attract GST @5%. But, ready to eat popcorn bag or packet attracts 18% GST.

Vide, AAR- Gujarat: Jay Jalaram

Enterprises [2020]117.

6. A manpower agency is extracting minerals from a mine owned by another person. Is it supply of goods or services?

Applicant is providing a support in extraction of mineral and therefore it is a kind of supplying support Service.

In view of the above, we find that the Applicant is providing supporting service related to mining. The said service is classifiable under HSN 998622. The rate of GST on the said service is 18% (CGST 9% + SGST 9%) as provided under the Notification No. 11/2017-Central Tax (Rate) dated 28.06.2017. AAR-Rajasthan (KSC Buildcon (P) Ltd.]

7. As per sec 17(5)(d) ITC is blocked when an RTP procures goods and services for construction of any immovable property on his own account, which is capitalized, including when such goods or services or both are used in the course or furtherance of business.

Now, whether ITC is admissible on lease rent paid during pre-operative period for the leasehold land on which a resort is being constructed to be used for furtherance of business?

Input Tax Credit is not available for lease rent paid during pre-operative period for the leasehold land on which the resort is being constructed on his own account to be used for furtherance of business, when the same is being capitalized and treated as capital expenditure. Vide, AAR, WB, GGL Hotel & Resort Company Limited, 30/WBAAR/2018-19 dated 08/01/2019

8. If consumable inputs like furnace oil, zinc etc. are not returned to any principal from a job performing job of galvanizing within the specified time limit whether it will be treated as supply in GST?

The goods like furnace oil, zinc etc. consumed in the process of galvanizing are inseparable from the galvanized goods. If return of the galvanized goods to the principal satisfies the condition of receiving back the inputs in accordance with section 143(1)(a) of the GST Act and the goods like furnace oil, zinc etc. have been entirely used up in the process of galvanizing then question of returning of furnace oil, zinc etc. should not arise and not be treated as supply.

[Vide, AAR, WB, Ratan Projects & Engineering Co Private Limited, 49/WBAAR/2018-19 dated 28/03/2019].

9. Whether any sale done by the liquidator of the assets of a corporate debtor under the provisions of the Insolvency and Bankruptcy Code, 2016 is a “supply” under GST?

The sale of the assets of a corporate debtor is a supply of goods by the liquidator, who is required to take registration u/s 24 of the GST Act. If she is already registered as a distinct person of the corporate debtor in terms of Notification No. 11/2020 – Central Tax dated 21/03/2020, she should continue to remain registered till her liability ceases under section 29 (1) (c) of the GST Act.

Vide, AAR, WB,M/s Mansi Oils and Grains Pvt Ltd,02/WBAAR/2020-21 dt 29/06/2020

10. Whether medicines and surgical goods supplied by Hospitals and nursing homes to the inpatients and outpatients are exempted?

The supply of medicines & other surgical goods by the hospital from its pharmacy to inpatients are in the course of providing health care services which are bundled and are provided in conjunction with each other, would be considered as “Composite Supply” &

eligible for exemption under ‘health care services’.

The supply of medicines & other surgical goods by the hospital from its pharmacy to outpatients not a part of health care services is a taxable supply of goods and thereby GST is applicable. [Vide, AAR, Kerala, M/s Baby Memorial Hospital Ltd, KER/57/2019 dt 05.09.2019]

11. Whether Input credit on Purchase of Lift would be available to Hotel as it has been used in the course or for the furtherance of business?

The input tax credit of tax paid on Lifts procured and installed in hotel building shall not be available to the applicant as the same is blocked in terms of Section 17(5)(d) of the CGST Act 2017, become an integral part of the building which is immovable property. [Vide:- Jabalpur Hotels Pvt Ltd (GST AAR Madhya Pradesh), Order No. 10/2020, dt 08/06/2020]

A representative list of such Circulars and order passed by Authority of Advance Ruling on different issues has been provided in Annexure 16 and Annexure 17 respectively.

The idea of this desk review is that the officer(s) should gather relevant information about the RTP before actual commencement of audit enabling him/her to be fully prepared from the very first day of visiting the Auditee’s place or examining the books produced by the Auditee for audit.

10.8. Commencement of Audit:

As per explanation to Section 65(4) of the GGST Act, 2017, ‘commencement of audit’ shall mean the date on which the records and other documents, called for by the tax authorities, are made available by the registered person or the actual institution of audit at the place of business, whichever is later.

Thus, audit will commence on the first date of hearing as per GST ADT-01 on provided the Auditee produces the requisite documents and records as have been asked for.

10.9. Preparation and approval of Audit plan–

The objective of preparing an audit plan is to outline a logical series of review and examination steps that would meet the goals and standards of an audit in an efficient and effective manner. Audit Plan is the roadmap for the sound performance of audit and is most important stage before conduct of audit. All the previous steps are actually aimed at preparation of a purposeful Audit Plan. By now, the Audit Officer is in a position to take a reasonable view regarding the vulnerable areas, the weak points in the systems, abnormal trends and unusual occurrences that warrant detailed verification. Certain unanswered or inadequately answered queries about the affairs of the taxpayer may also be added to this list. Audit plan should be a detailed plan of action. The audit plan should be consistent with the complexity of the audits.

10.9.1. How to make an effective audit plan?

An effective audit plan actually starts building up from the stage of desk review. But on the basis of scrutiny of the set of documents and records and the filled in questionnaire produced by the RTP on the first date of hearing as per the FORM GST ADT-01 new angles may emerge. Inclusion of these points in effect does a value addition to the audit plan.

Audit Plan is the most important stage before conducting of audit. Thus, each Audit Officer will prepare an Audit Plan for each individual. Auditee based on the information gathered from such documents, records, questionnaire in addition to the observations made upon prior-audit desk review and data analysis done by them in relation to the Auditee’s business performance. The information

available from the GST back-office portal, MIS available internally and various reports like BI Tool, BIFA, etc. (if available) should be analyzed to prepare an effective audit plan. Any other pertinent information (e.g. received from any enforcement unit) in respect of the said Auditee may also be taken into account.

The Audit plan should preferably be prepared within seven (07) working days of date mentioned in notice Form GST ADT-01 and under no circumstances, it should go beyond 15 working days.

An effective audit plan will be a guiding track for Audit conducted under both “Field Audit Method” (Audit at RTP’s place) as well as “Desk Audit Method” (Audit at Audit Officer’s place).

10.9.2. Approval of audit plan

The Audit Officer shall get each Audit plan approved as per the departmental guidelines issued from time to time. In case an Audit Officer finds it necessary to modify the audit plan in the course of the audit, details of the same with reasons thereof shall be placed for approval.

10.10. Examination of Books of Accounts and records–

Examination of Books of accounts and records involves verification of data and information and actual verification of documents submitted by the RTP in the course of audit and verification of the points mentioned in the audit plan. This is the most vital part of the audit process. The entire outcome of audit depends on examination of books of accounts systematically and in a planned manner.

- The officer should have a primary knowledge about the business pattern of the RTP with respect to the particular trade & industry.

- He should also be well aware of the existing trade practices, conventions and market trends.

- The Audit Officer should be well aware of the statutory provisions, rates of taxes, Circulars, Orders, Advance Rulings, Court Orders etc. as applicable for the particular period of audit.

- An Audit Officer should apprise the RTP of the provisions of the GST Acts in respect of maintenance of books.

- He/She should preserve all the documents submitted by the Auditee in the course of audit as office records preferably in electronic format.

- Physical copy duly authenticated or digitally signed copies wherever possible should be collected which are pertinent to the queries/audit para of the audit officer.

- He should take an unbiased and judicious approach in the course of audit.

- An Audit Officer should be tactful to gain the goodwill and confidence of the RTP.

- Technical lapses by the RTP which do not have any revenue implication, and has occurred out of oversight or ignorance, should be ignored. However, any such incidence upon being detected should be noted down in the course of audit.

- Confidentiality should be maintained in respect of sensitive and confidential information furnished, in the course of audit.

- Understanding of the Indian Accounting Standards and the impact of GST thereupon while examining the Books of Accounts will facilitate an Audit Officer while examining Books of Accounts.

Some illustrative examples for primary understanding of accounting standard vis-à-vis GST are given as Annexure 22. It is desirable that an Audit Officer would be inspired from the representative illustrations given in the aforesaid Annexure and may study such Accounting Standards.

Some indicative parameters of examination are discussed in this chapter. While carrying on examination in the practical field, the audit officer is expected to explore many more effective areas of concern. Registration/Migration Analysis, Return Analysis, Ratio analysis, Trend Analysis, Balance sheet study are some of the vital areas of Examination/Verification of Books of Accounts and records in the course of audit.

10.10.1.Registration/Migration analysis:

Previous registration details (if any) under earlier Acts are to be verified. If such is not disclosed there may be a tendency to hide earlier history of compliance behavior.

Up to date details of business promoters, additional place of business, bank accounts, and details of authorized signatory. If such is not provided, the Auditee should be asked to provide such numbers and information.

Furthermore, the Audit Officer shall analyze the trends and patterns of Turnover, Tax payment, nature of business etc. from the pre-GST registration data, if available.

10.10.2.Return Analysis:

This is the most vital area before commencement of the Audit program. A great deal of the groundwork can be done upon analysis of the available return figures and thereby having a prima-facie idea of the business trend of the Auditee.

Following illustrative steps may be considered for an effective Return Analysis:

✓ HSN code of the goods and/or SAC of the services dealt in by the RTP should be verified to ensure that such are in conformity with the schedules/notifications and it is to be checked that the proper rate of tax thereupon was applied on outward supplies as shown in Form GSTR-1 & Form GSTR-3B.

✓ Time of filing of returns should be noted and should be checked to confirm whether the returns were filed within the prescribed time.

✓ Outward supplies as declared in Form GSTR-1, Form GSTR-3B should be compared with the Books of Accounts as maintained and produced by the Auditee. The reconciliation statement, in case of any difference, is required to be examined with supporting documents and explanations along with Form GSTR-9/9A and Form GSTR-9C, if such have been submitted by the Auditee.

✓ Claim of the RTP under different heads like –Zero-rated, Nil rated, Exempted and non-GST outward supplies etc. as shown in Form GSTR-1, Form GSTR-3B. The reconciliation statement, in case of any difference, is required to be examined with supporting documents and explanations along with Form GSTR9/ 9A and Form GSTR-9C, if such have been submitted by the Auditee.

✓ Amount appearing under the head “Advance received” needs to be reviewed carefully since GST is applicable on “Advance received” against future “supply of services”. As per Notification No.66/2017 – CT. dated 15.11.2017, payment has been delinked to determine time of supply in case of supply of goods.

✓ Transactions like import of services and transactions between related parties and activities specified in Schedule-I which are required to be considered as supply even without consideration are required to be examined thoroughly. There may or may not be any reflection of such transactions in the GST returns.

These cases would require very cautious examination of the books of accounts, final accounts, P/L account and balance sheet to determine whether there are any such transactions which are not reflected in the returns. Some illustrative examples are given in Annexure 21for understanding of the matter.

✓ Goods sent for approval and goods sent to job workers are required to be examined with the books of accounts.

✓ Data in respect of e-way bills, both inward and outward, should be verified with the books for compliance level analysis. It may happen that the total value of outward e-waybill grossly differs with the total outward supply. In that case one should go through the details into the accounts.

✓ Refund may be made to the Auditee on account of export with or without payment of tax. In such cases, the veracity of export claims need to be checked. For this, the shipping bill details should be checked with the ICEGATE portal; in case of high volume of export through non-EDI check posts where the shipping bill details cannot be verified through ICEGATE portal, extra caution should be exercised in scrutinizing the shipping bills in support of the export claims.

✓ In case of export with payment of tax, if the value of export is found to be significantly higher than similar products sold in the domestic market in depth scrutiny of the payment received in respect of the export is required since there may be a possibility of monetizing excess ITC.

✓ In respect of claim for refund of unutilized ITC on a/c of zero-rated supply, adequate caution is required to be taken so that, ITC on account of transitional credit, capital goods are not claimed for refund.

✓ Claim for refund of unutilized ITC may be made on account of inverted tax structure. In such cases, (i) verification of the classification of inputs and output supplies and the respective rates of taxes attracted by them is very crucial; (ii) Refund of unutilized ITC in accordance with section 54(3)(ii) of the GGST Act is provided where credit has accumulated on account of rate of tax on inputs being higher than rate of tax on output supplies. Hence, it would not be applicable in cases where the input and the output supplies are the same (i.e. in cases of trading activities). Therefore, adequate caution must be exercised to verify that “Turnover of Inverted-rated supply” does not include any turnover related to trading activity. Similarly, “Net ITC” for the purpose of refund should not include any ITC relatable to trading activity; nor should it include ITC on account of capital goods or input services.

✓ The claim of ITC of an Auditee is subject to fulfillment of the conditions laid down in the Acts and Rules made thereunder.

✓ If usage of ITC for payment on account of export is significantly high, in depth scrutiny of the availment of ITC is warranted.

✓ In depth checking is needed in respect of goods and services on which credit is blocked.

✓ Query should be made to confirm whether any specific Advance Ruling/Appeal Order of Advance Ruling is applicable for any of the supplies made by the Auditee.

✓ Output tax payment is required to be examined to ascertain interest liability. Any output liability which has been discharged other than by Form GSTR 3B is required to be examined as to whether interest (if applicable) has also been paid for the same or not.

✓ Checking should be done in respect of interest and late fee payable as per notification(s).

✓ All possible areas related to compliance issue that may result in short payment or evasion of tax are also required to be checked.

Some illustrations in respect of the provisions of input tax credit is attached as Annexure 15.

The intention of these annexures is to create attention of Officers in the subject so that an Audit Officer looks into the statutory provisions in details.

It may be mentioned in this regard that this Annexure is merely indicative in nature. However, it is desirable that Audit Officers will not confine themselves to these indicative illustrations and will be prudent enough to go through the provisions of law and rule, various clarifications issued in different circulars, judgments passed by various Courts of Law and Rulings passed by AAR & AAAR in this respect in detail.

10.10.3.Trend Analysis: