Rule of Lapse & September Rush A New Jargon For ITC Seekers Under GST Law

Union Budget is based on the Principle of Annuality’ i.e Parliament grants money to the Government of India for one financial year. If Grants are not utilised by the end of the financial year, the unutilised grants shall expire and restored to the Consolidated Fund of India. This practice is known as ‘Rule of lapse’. However, compliance of this rule leads to heavy rush of expenditure at the close of the financial year. This March Run Up is popularly known as ‘March Rush’ and our bureaucrats are more tuned to bear this pressure.

Now it is going to be replicated in GSTR compliance for September 2018. So ‘September Rush’ will be buzz word for GST registered assesses (‘taxable assesses’). The eligible Input Tax Credit (ITC) during the financial year 2017-18 shall expire if it is not availed in accordance with Section 16(4) of the CGST Act 2017. In this article let us briefly analyse the common challenges faced by the taxable assesses for smooth availment of ITC.

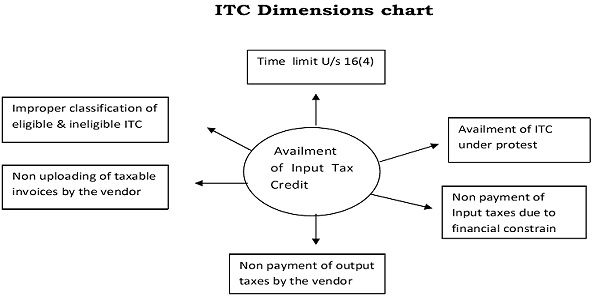

ITC Dimensions chart

Under GST Act there is time limit for availment of ITC i.e. the due date for filing September GST Return u/s 39 or filing of the annual return for the said year whichever is earlier in terms of Section 16(4) of the CGST Act. The format and form of Annual returns u/s 44 of the CGST Act is not yet notified by the Government. In the absence of the relevant Notification Effective date or cut off date for availing balance eligible input tax credit shall be assumed to be Oct 20th i.e. due date for filing September GST Return.

Though there are conditions and restrictions for availment of ITC under Section 16 read with Section 17(5)of CGST Act , due to improper classification of eligible and ineligible ITC ,the taxable assesses are understood to be not availing eligible ITC in their GST Returns properly.

To quote many Taxable Assesses are reported to be availing only 50% of ITC on capital goods instead of full 100% credit as per past practice. Similarly, there were confusions among the taxable assesses w.r.t. inputs/ input services/ capital goods used or intended to be used in course or furtherance of business. Example whether ITC can be availed on CSR expenditure incurred by the companies? These technical doubts/knowledge gaps lead to non availment of eligible ITC by the assesses.

Further, non uploading of taxable invoices is resulting in denial of ITC on the said taxable invoices to the assesses. For example non availment of ITC on bank charges due to non uploading of tax invoices by the banks. This results in loosing of ITC and excess cash outflow.

In recent times, we are also observing several insolvency petitions are pending before NCLT/DRT w.r.t entrepreneurs under financial crisis. It is seriously impacting their business operations as well as small and medium enterprises depending upon them. For example when there is default in the payment of output taxes, the goods/ services recipients from such stressed/ potential sick companies would be ineligible for ITC in terms of Section 16(2)(c) of the CGST Act.

So options should be weighed such as availment of ITC under protest / availment and reversal of ITC in GSTR-3B filed in the same month to avoid time limit restrictions.

In light of the above, proper verification of books of accounts needs to be done by the assesses as the due date for September GST Return is fast approaching. Appropriate care should also be taken for availment of ITC otherwise irregular availment of ITC attracts penal provisions in terms of Section 73 and Section 74 of CGST Act. So September GST Return is going to be “Tight Rope Walk” for all recipients of goods and services as far as ITC availment is concerned. The professional accountants play a key role to address these complexities and impending challenges.

Let the AXE OF RULE OF LAPSE does not fall on head of ITC claimant.

( The author of this article can be reached at prudhvitadepalli@gmail.com)

please elaborate more on how to avail the hidden itc

Good article . Written in simple and easy to understand by common person.

Thanks & Regards,

J.Janarthanan

We have broght forward sgst Rs 7864.00 from 2017-2018 but our busenss up to sept. 2018 is nill .Why i cannot avail.

Thanks for your information. dear please give me your cell no.