As per Notification No. 14/2022 – Central Tax dated July 5, 2022, along with circular 170/02/2022-GST dated July 6, 2022, the government has brought in certain modifications to Table 4 of Form GSTR-3B. These changes aim to help taxpayers accurately report information related to ITC availed, ITC reversal, ITC re-claimed, and ineligible ITC.

To make it easier for taxpayers to report ITC reversal and reclaims accurately and avoid clerical errors, a new ledger called the Electronic Credit and Reclaimed Statement has been introduced on the GST portal. This statement helps taxpayers keep track of their ITC that has been reversed in Table 4B(2) and then reclaimed in Table 4D(1) and 4A(5) for each return period. This new feature will be available starting from the August return period.

The Detailed advisory is discussed below along with the procedures:

The Advisory

Introduction

A new ledger Electronic Credit and Re-claimed Statement is being introduced on the GST Portal. This statement shall facilitate that while re-claiming ITC in GSTR-3B, the amount aligns appropriately with the corresponding reversed ITC.

Effective Periods

For Monthly taxpayers: The specified return period pertains to August 2023.

For Quarterly taxpayers: The specified return period corresponds to Q2 of the financial year 2023-24, encompassing the months of July – September 2023.

<< The Report is available on GST portal from the Period August 2023>>

Reporting of Opening Balances

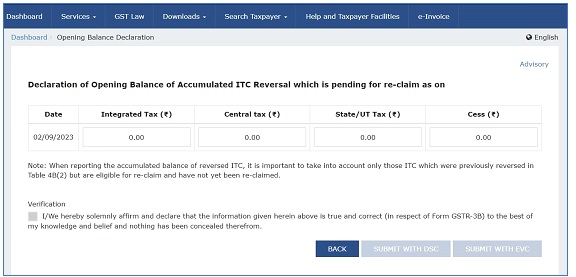

Taxpayers are being provided a facility to report their cumulative ITC reversal (ITC that has been reversed earlier and has not yet been reclaimed) as opening balance for “Electronic Credit Reversal and Re-claimed Statement” if any.

<< Taxpayers must report the opening balance of Input Tax Credit (ITC) previously reversed but not reclaimed. This balance will be used as the opening balance of the ITC ledger. Taxpayers are required to file a declaration of the opening balance..>>

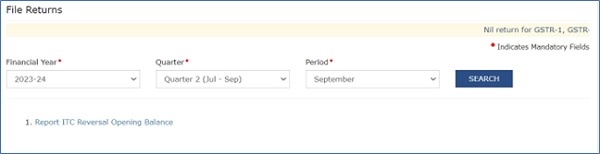

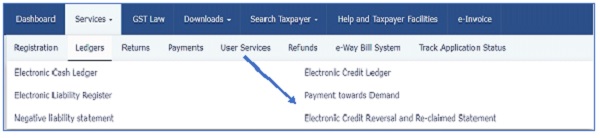

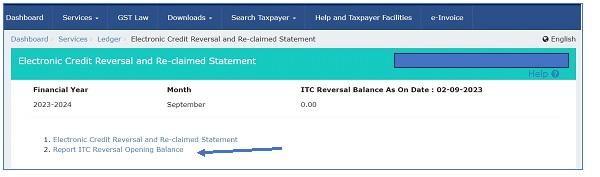

The navigation to report ITC reversal balance:

Login >> Report ITC Reversal Opening Balance>> fill required information >> Submit with EVC or DSC.

Or

Services >> Ledgers >> Electronic Credit Reversal and Re-claimed Statement >> Report ITC Reversal Opening Balance>> fill required information >> Submit with EVC or DSC.

–

–

Other Highlights

- Taxpayers having monthly filing frequency are required to report their opening balance considering the ITC reversal done till the return period of July 2023.

- In contrast, quarterly taxpayers shall report their opening balance up to Q1 of the financial year 2023-24, considering the ITC reversal made till the April-June 2023 return period.

- The taxpayers have the opportunity to declare their opening balance for ITC reversal Until 30th November 2023.

- The taxpayers shall also be provided 3 (three) amendment opportunities to correct their opening balance in case of any mistakes or inaccuracies in reporting. Importantly, until 30th November 2023, both reporting and amendment facilities are accessible.

- However, after 30th November till 31st December 2023, only amendments will be permitted and the option for fresh reporting will not be available. This amendment facility shall be discontinued after 31st December 2023.

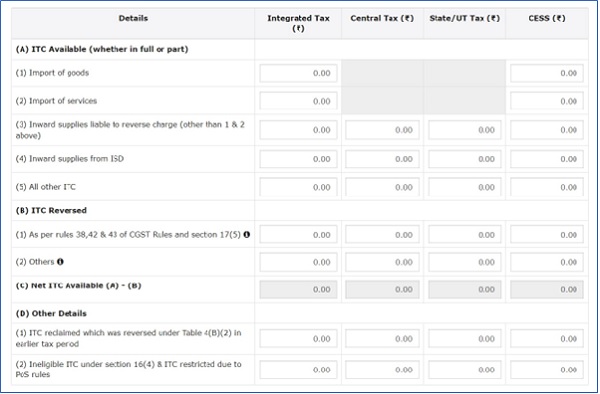

Reporting of Reclaim & Reversal in GSTR-3B guide

- ITC reversal which to be re-claimed later to be done in 4(B)(2) that would later transfer in the statement as ITC available for re-claim.

- ITC Re-claim to be made in 4(A)(5) including the other eligible ITC available in GSTR-2B of said Month.

- ITC-Re-claim mandatorily to be reported in 4(D)(1) specifically which would later transfer in the statement introduced as ITC re-claimed.

- If the amount reported in 4(D)(1) exceeds the amount available for re-claiming, the system will alert taxpayer for claiming excess ITC as compared to the re-claim statement.

Conclusion

This statement is crucial for taxpayers as it helps them track their Input Tax Credit (ITC) that has been reversed in Table 4B(2) and later re-claimed in Table 4D(1) and 4A(5) for each return period. The introduction of this statement by the GST department aims to improve the comparison system of ITC reported in 4(A)(5) with GSTR-2B.

Recently the GST department has introduced the rule 88D and form DRC-01C for intimating the mismatch between GSTR-2B and GSTR-3B.

According to said rule, if any mismatch of ITC is reflected between GSTR-3B vs GSTR-2B then notice in form DRC-01C will be sent to the taxpayer and he has to explain the reasons for the said mismatch or pay the tax excess claimed through DRC-03 along with the interest thereon.

Since, GSTIN is about to send intimation for the ITC differences, GST department eliminated the main reason for the Difference between GSTR-2B and GSTR-3B, ITC-Re-claim.

From now on, if there is a genuine mismatch between GSTR-2B and GSTR-3B, even after considering the re-claim, the department will inform the taxpayer and the taxpayer will have to provide a reason for the mismatch.

If a taxpayer forgets to report their re-claims, they will have to pay back the re-claim made in that month along with the interest. Therefore, it is important to report accurate figures in GSTR-3B to avoid such intimations.

Hope above fits fine.

********************************************

Author’s Note: This article is intended solely for educational purposes. The author will not be held responsible for any errors or discrepancies that may arise from the implementation of the information provided that may arise from the implementation of the information provided.