Why E-Invoicing? – 5 Main Reasons

1. Government wants to have a Real Time GST Collection Figure – Dealers may get calls for advance tax payment during the month

2. Risky dealers may be mandated to generate Invoices of liability only to the extent of balance in their cash ledger – A Rule in the nature of Rule 86A may be a reality

3. Your Stock in hand will be on the finger tips of the revenue authorities – Invocation of Sec 71 (Access to business premises may be frequent)

4. No more Memorandum Invoice Numbers – The changes in invoices will leave an audit trail

5. No more Fake bills – Any fake bills dealer will get tracked immediately rather than after months

What is E-Invoicing?

The GST Council has approved introduction of ‘E-invoicing’ or ‘electronic invoicing’ in a phased manner for reporting of business to business (B2B) invoices to GST System.

- Starting from 1st January 2020 on Voluntary basis

- And from April,2020 it is mandatory for all the enterprises having a turnover of > 100 Cr.

- Taxpayer will be required to report the same to Invoice Registration Portal (IRP) of GST, which in turn will generate a unique Invoice Reference Number (IRN) and digitally sign the e-invoice and generate the QR code.

What type of documents are to be reported to GSTN System?

- Invoice by Supplier

- Credit Note by Supplier

- Debit Note by Supplier

- Any other document as required by law to be reported by the creator of the document

Legal Aspects

Notification No 31/2019 & 71/2019

- 5. In the said rules, in rule 46, after the fifth proviso, with effect from a date to be notified later, the following proviso shall be inserted, namely:- “Provided also that the Government may, by notification, on the recommendations of the Council, and subject to such conditions and restrictions as mentioned therein, specify that the tax invoice shall have Quick Response (QR) code.”.

- In exercise of the powers conferred by rule 5 of the Central Goods and Services Tax (Fourth Amendment) Rules, 2019, made vide notification No. 31/2019 – Central Tax, dated the 28th June, 2019, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i), vide number G.S.R 457(E), dated the 28th June,2019, the Government, on the recommendations of the Council, hereby appoints the 1st day of April, 2020, as the date from which the provisions of the said rule, shall come into force.

- “R48(4) The invoice shall be prepared by such class of registered persons as may be notified by the Government, on the recommendations of the Council, by including such particulars contained in FORM GST INV-01 after obtaining an Invoice Reference Number by uploading information contained therein on the Common Goods and Services Tax Electronic Portal in such manner and subject to such conditions and restrictions as may be specified in the notification.

- (5) Every invoice issued by a person to whom sub-rule (4) applies in any manner other than the manner specified in the said sub-rule shall not be treated as an invoice.

- (6) The provisions of sub-rules (1) and (2) shall not apply to an invoice prepared in the manner specified in sub-rule (4).”.

- In exercise of the powers conferred by sub-rule (4) to rule 48 of the Central Goods and Services Tax Rules, 2017, the Government, on the recommendations of the Council, hereby notifies registered person, whose aggregate turnover in a financial year exceeds one hundred crore rupees, as a class of registered person who shall prepare invoice in terms of sub-rule (4) of rule 48 of the said rules in respect of supply of goods or services or both to a registered person.

- 3. This notification shall come into force from the 1st day of April, 2020

- the Central Government, on the recommendations of the Council, hereby, notifies the following as the Common Goods and Services Tax Electronic Portal for the purpose of preparation of the invoice in terms of sub-rule(4) of rule 48 of the aforesaid rules, namely:-

(i) www.einvoice1.gst.gov.in;

(ii) www.einvoice2.gst.gov.in;

(iii)www.einvoice3.gst.gov.in;

(iv) www.einvoice4.gst.gov.in;

(v) www.einvoice5.gst.gov.in;

(vi) www.einvoice6.gst.gov.in;

(vii) www.einvoice7.gst.gov.in;

(viii) www.einvoice8.gst.gov.in;

(ix) www.einvoice9.gst.gov.in;

(x) www.einvoice10.gst.gov.in.

- Explanation.-For the purposes of this notification, the above mentioned websites mean the websites managed by the Goods and Services Tax Network, a company incorporated under the provisions of section 8 of the Companies Act, 2013 (18 of 2013).

- …hereby notifies that an invoice issued by a registered person, whose aggregate turnover in a financial year exceeds five hundred crore rupees, to an unregistered person (hereinafter referred to as B2C invoice), shall have Quick Response (QR)code:

- Provided that where such registered person makes a Dynamic Quick Response (QR) code available to the recipient through a digital display, such B2C invoice issued by such registered person containing cross-reference of the payment using a Dynamic Quick Response (QR) code, shall be deemed to be having Quick Response (QR) code.

- 2. This notification shall come into force from the 1st day of April, 2020

E-Invoicing Workflow

- Two Major parts :

> Interaction between the business (supplier in case of invoice) and IRP

> Interaction between the IRP and the GST/E-Way Bill Systems and the Buyer

Critical Aspects of E-Invoicing

- Generation of invoice in standard format – The most important point here is that the invoice must have mandatory parameters and must conform to the e-invoice standard( schema) published in GST common portal. (https://www.gstn.org/e-invoice/.) The optional parameters can be according to the business need of the supplier. The supplier’s software should be capable to generate a JSON of the invoice that is ready to be uploaded to Invoice reference portal( IRP) of GST.

- Reporting of e- invoice to a central system – Invoice Registration portal( IRP) of GST will check from Central Registry of GST system to ensure that same invoice from same supplier pertaining to same financial year is not being uploaded again. On receipt of confirmation, it will generate a unique Invoice Reference Number (IRN) and digitally sign the invoice and also generate a QR Code. Portal will return the same to the taxpayer who generated the document. The IRP will also send the signed e invoice to the recipient of the document

- Signature on e invoice The e-invoice will be digitally signed by the IRP after it has been validated. Once it is registered, it will not be required to be signed by anyone else.

- Signature on e invoice The e-invoice will be digitally signed by the IRP after it has been validated. Once it is registered, it will not be required to be signed by anyone else.

- Printing of QR Code on invoice :- The QR code will be provided to the seller once he uploads the invoice into the Invoice Registration system and the same is registered there..Seller can at his option may print the same on Invoice.

- QR Code on B2C Invoice is mandatory for registered person, whose aggregate turnover in a financial year exceeds five hundred crore rupees (>500 crores) w.e.f 1st April, 2020. (Notification No. 72/2019 – Central Tax dated 13 December, 2019)

- Validity of invoice without Invoice Reference No. (IRN) ;Invoice will be valid only if it has IRN.

- Printing of e -invoice It will be possible for both the seller as well as the buyer to print the invoice, using the QR code as well as signed e-invoice returned by the Invoice Registration Portal(IRP).

- Cancellation of e invoices:- The e-invoice mechanism enables invoices to be cancelled. This will have to be reported to IRN within 24 hours. Any cancellation after 24 hrs could not be possible on IRN, however one can manually cancel the same on GST portal before filing the returns. E-Invoice can’t be partially cancelled. It has to be fully cancelled

- Amendments to the e-invoice Amendments are allowed on GST portal as per provisions of GST law. All amendments to the e-invoice will be done on GST portal only.

- E invoices for Exports The e-invoice schema also caters to the export invoices as well. The e-invoice schema is based on most common standard, this will help buyer’s system to read the e-invoice.

- E-invoice schema for reverse charge mechanism:- E-invoice system has a reverse charge mechanism reporting as well.

E-invoice Template

How will E-Invoice Look like

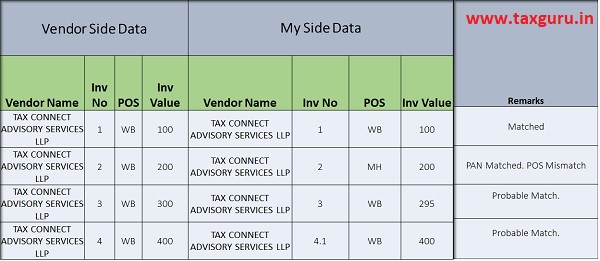

PAN Wise Matching & Other AI

Supplier Analytics

Supplier Analytics

Author Bio