Introduction:-

- Time has been arrived for filing of GST Returns but in some transactions we are not very much clear whether ITC has been availed for a particular transactions or not. Section-17(5) of CGST Act, 2017 will provide light in this matter.

- This article will provide detail lists of Input not eligible for Input Tax Credit (ITC) under GST:-

Main Provision:-

As per Section-17(5) of CGST Act, 2017, Input Tax Credit (ITC) shall not be available in respect of the following namely:-

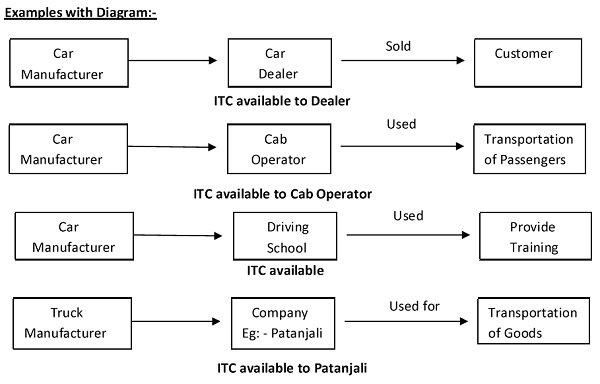

♠ Motor Vehicles and other conveyances except when they are used

(i) For making the following taxable sup lies, namely

(ii) For Transportation of Goods

(ii) For Transportation of Goods

♠ Supply of Goods or Services or both:-

(i) Food and Beverages,

Outdoor Catering,

Beauty Treatment,

Health Services,

Cosmetic and Plastic Surgery

Except:‑

Where a such inward supply of Goods or Services or both of a particular category is used by person registered person for making an outward taxable supply of the same category of Goods or services or both or as an element of a taxable composite or mixed supply.

(ii) ITC not allowed on Membership of:-

- Health,

- Club,

- and fitness centre.

(iii) Rent-a-Cab,

Life Insurance,

Health Insurance

Except where:‑

(a) notifies the services which are obligatory for an employer to provide to its employees under any law for the time being in force,

(b) Such inward supply of Goods or Services or both of a particular category is used by a registered person for making an outward taxable supply of the same category of Goods and services or both or as part of a taxable composite or mixed supply.

(iv) ITC not allowed on Travel benefits extended to employees on vacation such as

- Leave or

- home travel concession.

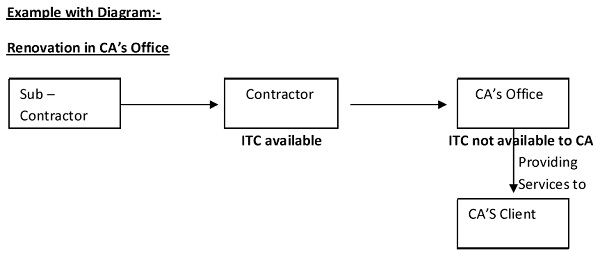

♠ Work contract services when supplied for construction of immovable property (other than plant and machinery).

Except:‑

Where it is an input services for further supply of works contract services.

♣ Goods or services or both received by a taxable person for construction of an immovable property (other than plant or machinery) on his own account including when such goods or services or both are used in the course or furtherance of business.

Explanation:‑

Construction includes re-construction, renovation, additions or alterations or repairs to the extent of capitalisation of said immovable property, i.e. ITC not available (if capitalised).

♣ Goods or services or both on which tax has been paid u/s 10 (Composition Levy).

♣ Goods or services or both received by a non-resident taxable person* except on goods imported by him.

♣ Goods or services or both used for personal consumption.

♣ Goods lost, stolen, destroyed, written off, or disposed of by way of gift or free samples.

♣ Any tax paid in accordance with the provisions of Section-74, 129, & 130.

Non-resident taxable person*

Non resident taxable person means a taxable person who occasionally undertakes transactions involving supply of goods or services or both whether as principal or agent or in any other capacity but who has no fixed place of business in India.

sir.

i have wrongly filed one firm invoices into another firm gst account.i filed bot gstr1 and gstr3b.pls help how can i rectify this problem?

dear sir

Fixed Assets Treatment under gst

As the new rate is 5% with no ITC for restaurant even if the turnover is less or more than 1 cr.. it means if it opts for composition subject to turnover limit then it can not recover 5% and if restaurant is not opting composition then it can recover from customer.

please confirm this understanding.

Sir can you please give an example where life insurance services are taken as an inward supply and an outward supply is being made of the same.

Good coverage giving all aspects of the provisions. Good attempt made by the author. Very useful for any one to know the real picture.

Loss in the quantity of gold during process is not covered under this clause of U/S 17. Once we are making any article of gold or silver or jewelry there is a value addition for all such process losses so the quantity difference because of process loss is not covered under Goods lost, stolen, destroyed, written off, or disposed of by way of gift or free samples.

In your example of a CA ‘s office ,if the repairs are taken to revenue, you get Input credit.Input will not be available only if the same is capitalised.

Mr A registered under GST engaged in the business of supply of tangible assets i. e. bulldozers on hourly basis. Whether he is eligible for ITC of GST paid on purchase of new bulldozers?

Goods lost, stolen, destroyed, written off, or disposed of by way of gift or free samples.:Whether “Wastage” item in Gold industry i.e Gold lost in processing is covered byy this cluaes U/s17? Or can we apply/interpret with erstwhile provision of CENVAT Rules where in goods lost in the processing being normal loss allowed to be eligible credit item?