A. FAQs on GST Refund of Excess Amount from the Electronic Cash Ledger

Q.1 How can I claim refund of excess amount available in Electronic Cash ledger?

Ans: 1. Login to GST portal for filing refund application under refunds section.

2. Navigate to Services > Refunds > Application for Refund option.

3. Select the reason of Refund as ‘Refund on account of excess balance in cash ledger’. File refund application in GST RFD-01.

4. The amount available in Electronic Cash Ledger would be auto-populated in the refund application in a matrix.

5. Mention the amount of refund to be claimed in GST RFD-01 in refund claimed table and file the form.

Q.2 What is the amount limit for claim of refund in case of “Refund of excess amount from the cash ledger”?

Ans: There is no minimum limit restriction for refund of excess amount in Electronic Cash Ledger.

Q.3 What are the relied upon documents which I have to upload with refund application on account of excess payment of tax?

Ans: You have to upload documents as are required to be filed along with Form RFD-01, as notified under CGST Rules or Circulars issued in the matter and other such documents the refund sanctioning authority may require.

Taxpayers have an option to upload 10 documents with the refund application, of size up to 5 MB each. Any supporting document can be uploaded by the taxpayer, if required.

Q.4 To whom should I file my application with?

Ans: The taxpayer shall file the refund application in Form GST RFD-01 on GST portal. Taxpayer shall choose ground of refund as “Refund of excess balance in Electronic Cash Ledger” for claiming refund. After filing, refund application shall be assigned to Refund Processing Officer and refund applicant can track the status of refund application.

Q.5 Can I save the application for refund?

Ans: Application for refund can be saved at any stage of completion for a maximum time period of 15 days from the date of creation of refund application. If the same is not filed within 15 days, the saved draft will be purged from the GST database.

Note: To view your saved application, navigate to Services > Refunds > My Saved/Filed Applications option.

Q.6 Do I need to upload any statement for claiming refund?

Ans: No statement template is required to be uploaded for claiming refund. You need to mention the refund to be claimed details in the refund application screen while filing refund application.

Q.7 How will I know the balance available in my Electronic Cash Ledger?

Ans: Balance amount available in your Electronic Cash Ledger is auto-populated in Form GST RFD-01. You can enter the amount of Refund to be claimed for Integrated Tax, Central Tax, State/ UT Tax and Cess in table “Refund Claimed”.

However, the amount of refund to be claimed cannot be more than the balance amount available in Electronic Cash Ledger.

Q.8 Can I preview the refund application before filing?

Ans: Yes, you can preview the refund application in PDF format to check for any inconsistency or discrepancy before filing on the GST Portal.

Q.9 How can I track the status of application for refund?

Ans: To track your filed application, navigate to Services > Refunds > Track Application Status option.

Q.10 What is ARN?

Ans: Once the refund application is filed, Application Reference Number (ARN) receipt would be generated and ARN would be sent to your registered e-mail address and mobile number.

Q.11 How can I download the ARN?

Ans: To download Filed applications (ARNs) PDF documents navigate to Services > Refunds > My Applications command.

Q.12 Where can I download my filed refund application?

Ans: Navigate to Services > User Services > My Applications link to download your filed refund application.

Q.13 What happens when refund application in case of “Refund of excess balance from Electronic Cash Ledger” is filed?

Ans:

- GST Portal generates an ARN and displays it in a confirmation message, indicating that the refund application has been successfully filed.

- GST Portal sends the ARN to e-mail and SMS of the registered taxpayer.

- GST Portal also makes a Debit entry in the Electronic Cash Ledger for the amount claimed as refund.

Q.14 Whether there is any ledger entry on filing refund application?

Ans: Yes, there is a debit entry in Electronic Cash Ledger for the amount claimed as refund. The ledger entry would be posted to Electronic Cash Ledger only after filing of refund application.

Q.15 When / how will the refund Form RFD-01 be processed?

Ans: Once the ARN is generated on filing of refund application in Form RFD-01, the refund application along with the documents attached while filing the form would be assigned to Jurisdictional Refund Processing Officers for processing the refund. Tax payer can track the status of refund application using track status functionality.

The application will be processed and refund will be disbursed by the Jurisdictional Authority after scrutiny.

Q. No. 16 to 17 are FAQs related to Creation of new UT of Ladakh and consequent changes of GST for taxpayers

Q.16 I have received an intimation that a new GSTIN has been assigned to me for UT of Ladakh. I have already filed a refund application with my old GSTIN. What will happen to that refund application?

Ans: All refund applications filed under old GSTIN, will be processed by designated Tax officials of the old GSTIN and amounts will be credited to your Bank detail as provided in old GSTIN. You do not need to file a fresh refund application, in these cases, using your new GSTIN.

Q.17 I have received an intimation that a new GSTIN has been assigned to me for UT of Ladakh. Where do I need to file my refund application?

Ans: You need to file all your refund applications, for the refund due under new GSTIN, in the new jurisdiction assigned to you, for the period effective from 1st January 2020.

Q. No. 18 to 19 are FAQs related to Merger of UT of Daman & Diu with UT of Dadra and Nagar Haveli and consequent changes on GST Portal for taxpayers

Q.18 I have received an intimation that a new GSTIN has been assigned to me for UT of Dadra and Nagar Haveli and Daman and Diu. I have already filed a refund application with my old GSTIN. What will happen to that refund application?

Ans: All refund applications filed under old GSTIN, will be processed by designated Tax officials of the old GSTIN and amounts will be credited to your Bank detail, as provided in old GSTIN. You do not need to file a fresh refund application for these cases, using your new GSTIN.

Your refund applications for the refund due under old GSTIN for the period upto 31st July, 2020 are to be filed under old GSTIN only.

Q.19 I have received an intimation that a new GSTIN has been assigned to me for UT of Dadra and Nagar Haveli and Daman and Diu. Where do I need to file my refund application?

Ans: You need to file all your refund applications, for the refund due under new GSTIN, in the new jurisdiction assigned to you, for the period effective from 1st August 2020 However, your refund applications for the refund due under old GSTIN for the period upto 31st July, 2020 are to be filed under old GSTIN only.

B. Manual on GST Refund of Excess Balance in Electronic Cash Ledger

How can I file the application for refund of excess balance in Electronic Cash Ledger on the GST Portal?

To file the application for refund of excess balance in Electronic Cash Ledger on the GST Portal, perform following steps:

1. Access the https://www.gst.gov.in/ URL. The GST Home page is displayed.

2. Click the Services > Refunds > Application for Refund command.

3. The Select the refund type page is displayed. Select the reason as Refund of Excess Balance in Electronic Cash Ledger option.

4. Click the CREATE button.

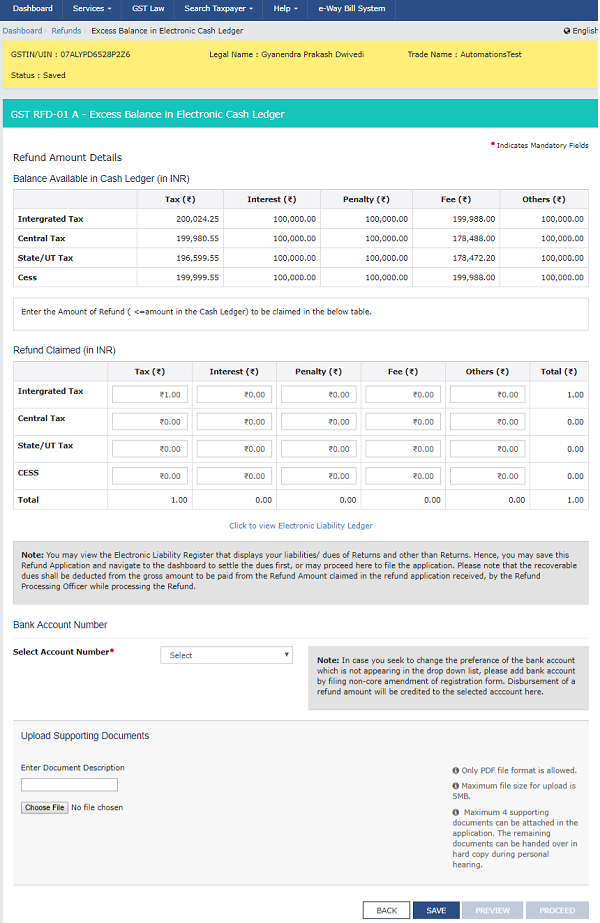

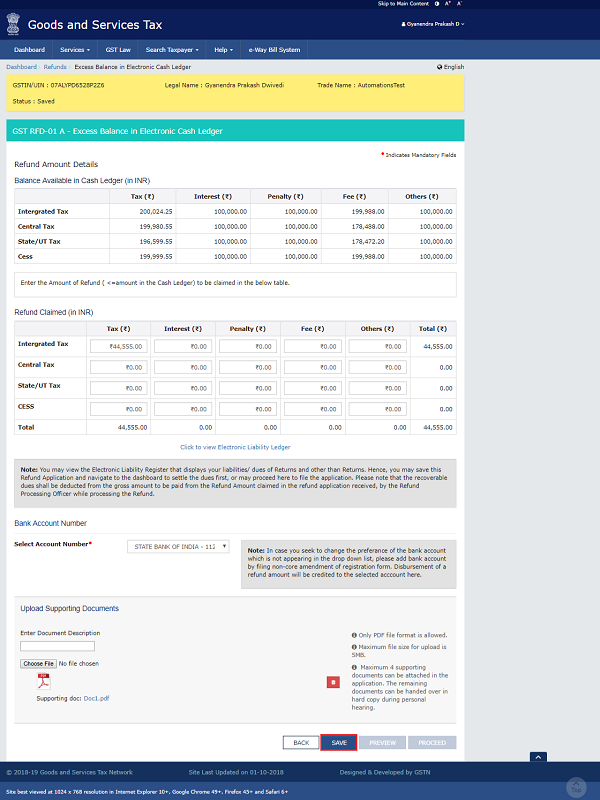

5. The GST RFD-01 A – Excess Balance in Electronic Cash Ledger page is displayed.

6. Balance amount available in Electronic Cash Ledger is displayed.

7. Enter the amount of Refund to be claimed for Integrated Tax, Central Tax, State/ UT Tax and Cess in table “Refund Claimed”.

8. You can click the hyper link Click to view Electronic Liability Ledger to view details of Electronic Liability Ledger that displays your liabilities/ dues of Returns and other than Returns.

9. Click the GO BACK TO REFUND FORM to return to the refund application page.

10. Select the Account Number from the Select Account Number drop-down list.

11. Under section upload Supporting Documents, you can upload supporting documents (if any).

12. Enter the Document Description.

13. Click the ADD DOCUMENT button.

14. Click the Delete button, in case you want to delete any document.

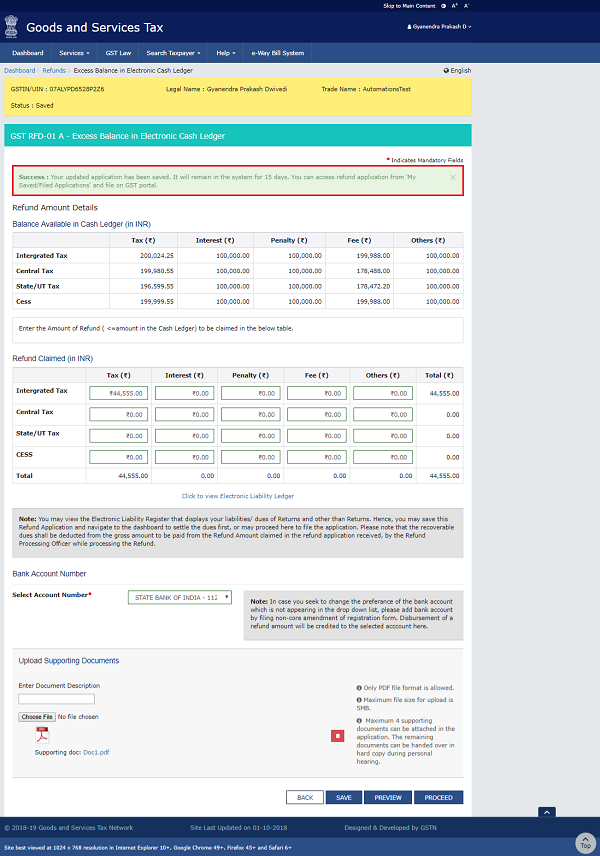

15. Click the SAVE button.

16. A success message is displayed that “Your application has been saved. You can retrieve this application and submit within 15 days from today. You can access the Application from Services > Refunds > My Saved/Filed Applications and file on the GST Portal.”

17. Click the PREVIEW button to download the form in PDF format.

18. Form is downloaded in the PDF format.

19. Click the PROCEED button.

20. Select the Declaration checkbox.

21. In the Name of Authorized Signatory drop-down list, select the name of authorized signatory.

22. Click the FILE WITH DSC or FILE WITH EVC button.

23 (a) In Case of DSC:

23.1. Click the PROCEED button.

23.2. Select the certificate and click the SIGN button.

23 (b) In Case of EVC:

23.1. Enter the OTP sent to email and mobile number of the Authorized Signatory registered at the GST Portal and click the VERIFY button.

24. The success message is displayed and status is changed to Submitted.Application Reference Number (ARN)receipt is downloaded and also sent on your e-mail address and mobile phone number. Click the PDF to open the receipt.

Notes:

- The system generates an ARN and displays it in a confirmation message, indicating that the refund application has been successfully filed.

- GST Portal sends the ARN to e-mail and SMS of the registered taxpayer.

- GST Portal also makes a Debit entry in the Electronic Cash Ledger for the amount claimed as refund.

- Filed applications (ARNs) can be downloaded as PDF documents using the My Saved/Filed Applications option under Refunds.

- Filed applications can be tracked using the Track Application Status option under Refunds.

- Once the ARN is generated after filing of form RFD-01A, taxpayer needs to take prints of the filed application and the Refund ARN Receipt generated at the portal, and submit the same along with supporting documents to the jurisdictional authority. The application will be processed and refund will be sanctioned manually.

- The disbursement is made once the concerned Tax Official processes and sanctions the refund application.

25. ARN receipt is displayed.

26. Navigate to Services > Ledgers > Electronic Cash Ledger to view the debit entry in the Electronic Cash Ledger for the amount claimed as refund.

27. The Electronic Cash Ledger is displayed. Click the Electronic Cash Ledger link.

28. Select the From and To date using the calendar to select the period for which you want to view the transactions of Electronic Cash Ledger.

29. Click the GO button.

30. The Electronic Cash Ledger details are displayed. Notice the debit entry in the Electronic Cash Ledger for the amount claimed as refund.

(Republished with amendments)

****

Disclaimer: The contents of this article are for information purposes only and does not constitute an advice or a legal opinion and are personal views of the author. It is based upon relevant law and/or facts available at that point of time and prepared with due accuracy & reliability. Readers are requested to check and refer relevant provisions of statute, latest judicial pronouncements, circulars, clarifications etc before acting on the basis of the above write up. The possibility of other views on the subject matter cannot be ruled out. By the use of the said information, you agree that Author / TaxGuru is not responsible or liable in any manner for the authenticity, accuracy, completeness, errors or any kind of omissions in this piece of information for any action taken thereof. This is not any kind of advertisement or solicitation of work by a professional.

Source- gst.gov.in

Can refund of excess balance in cash ledger be allowed after cancellation of gst registration? There is balance in cash ledger but gst registration no. was cancelled in 2019.

IN HOW MANY DAYS, I GOT MY REFUND OF EXCESS BALANCE IN ELECTRONIC CASH LEDGER, IN MY BANK ACCOUNT AFTER APPLIED ?

CAN WE CLAIM REFUND OF GST TDS WHICH IS AVAILABLE IN OUR CASH LEDGER IF YES KINDLY PROVIDE COPY OF NOTIFICATION

CAN I CLAIM REFUND FOR EXCESS IN CASH LEDGER AFTER 2 YEARS. IS THERE ANY TIME LIMIT.