Out of many controversial issues under GST, one of the most discussed issues is applicability of GST ocean freight under reverse charge mechanism (in case of goods imported on CIF basis). Some of the professional are of the view that pay tax under reverse charge mechanism and take the credit of it. However, it is interesting whether the credit of the same would be available?

In this article we shall be discussing applicability of GST on ocean freight payable upon import of goods from technical point of view.

The Central Government has imposed service tax on ocean freight with effect from 22 Jan 2017 and similar provisions are continued under GST regime.

Broadly we have discussed following in the article

√ Basic provisions

√ Scope of the charging section

√ Delegated legislation

√ Composite Supply

√ Double Taxation

√ Determination of place of supply

√ Availability of Input tax credit

√ Concluding remarks

Background

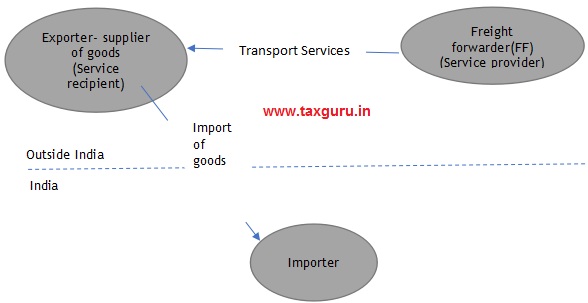

Typically, in a transaction, following parties are involved (viz Supplier of goods (exporter), freight forwarder (Transporter) and Importer of Goods:

Before going ahead it is worthwhile to refer charging section 5(3) of the Integrated Goods and Service Tax Act, 2017 (‘the IGST Act’), which provides for reverse charge on goods or services or both as may be notified by the Government.

The relevant provision is reproduced below for ease of reference:

The Government may, on the recommendations of the Council, by notification, specify categories of supply of goods or services or both, the tax on which shall be paid on reverse charge basis by the recipient of such goods or services or both and all the provisions of this Act shall apply to such recipient as if he is the person liable for paying the tax in relation to the supply of such goods or services or both

On the perusal of the above section, it is apparent that the Government can notify such class of goods or services or both under reverse charge on recipient of supply. Before moving further, it is therefore worthwhile to refer definition of recipient:

“recipient” of supply of goods or services or both, means—

(a) where a consideration is payable for the supply of goods or services or both, the person who is liable to pay that consideration;

(b) where no consideration is payable for the supply of goods, the person to whom the goods are delivered or made available, or to whom possession or use of the goods is given or made available; and

c) where no consideration is payable for the supply of a service, the person to whom the service is rendered, and any reference to a person to whom a supply is made shall be construed as a reference to the recipient of the supply and shall include an agent acting as such on behalf of the recipient in relation to the goods or services or both supplied;

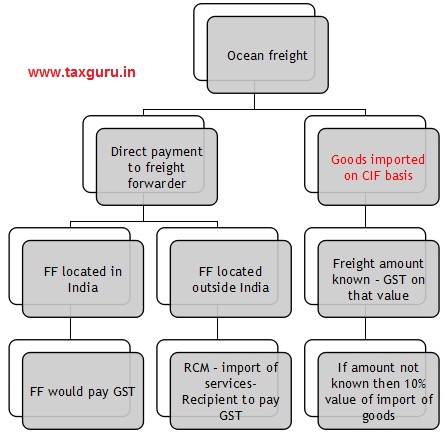

By exercising power vested under section 5(3) of the IGST Act, Government issued Notification No. 10/2017-Integrated Tax (Rate), dated 28-6-2017 – the relevant entry is reproduced below:

| Sl. No. | Category of Supply of Services | Supplier of service | Recipient of service |

| 10. | Services supplied by a person located in non-taxable territory by way of transportation of goods by a vessel from a place outside India up to the customs station of clearance in India. | A person located in non-taxable territory | Importer, as defined in clause (26) of Section 2 of the Customs Act, 1962 (52 of 1962), located in the taxable territory. |

Where the value of taxable service provided by a person located in non-taxable territory to a person located in non-taxable territory by way of transportation of goods by a vessel from a place outside India up to the customs station of clearance in India is not available with the person liable for paying integrated tax, the same shall be deemed to be 10 % of the CIF value (sum of cost, insurance and freight) of imported goods

In this article we are discussing applicability of GST under reverse charge basis on freight portion in case of goods imported on CIF basis, where service provider and receiver both are located outside India.

By way of Notification, the Government has included ‘importer’ in the category recipient of services. Now, the question arises when section has empowered to levy a tax on recipient, can Notification expand the scope of ‘service recipient’ ?

In nutshell following scenario would emerge:

Scope of the charging section

It is settled principal of law that charging section should be construed strictly.

Apex court in case of State of Rajasthan Versus Basant Agrotech (India) Ltd. (2014 (302) E.L.T. 3 (S.C.)) relied decision in Commissioner of Wealth Tax, Gujarat-III, Ahmedabad v. Ellis Bridge Gymkhana (AIR 1998 SC 120) -, it has been observed thus :-

“The rule of construction of a charging section is that before taxing any person, it must be shown that he falls within the ambit of the charging section by clear words used in the section. No one can be taxed by implication. A charging section has to be construed strictly. If a person has not been brought within the ambit of the charging section by clear words, he cannot be taxed at all.”

Commissioner of Central Excise, Pondicherry versus Acer India Ltd. 2004 (172) E.L.T. 289 (S.C.), Supreme Court relied on in Mathuram Agrawal v. State of Madhya Pradesh [(1999) 8 SCC 667], the law is stated in the following terms :

“…The intention of the legislature in a taxation statute is to be gathered from the language of the provisions particularly where the language is plain and unambiguous. In a taxing Act it is not possible to assume any intention or governing purpose of the statute more than what is stated in the plain language. It is not the economic results sought to be obtained by making the provision which is relevant in interpreting a fiscal statute. Equally impermissible is an interpretation which does not follow from the plain, unambiguous language of the statute. Words cannot be added to or substituted so as to give a meaning to the statute which will serve the spirit and intention of the legislature. The statute should clearly and unambiguously convey the three components of the tax law i.e. the subject of the tax, the person who is liable to pay the tax and the rate at which the tax is to be paid. If there is any ambiguity regarding any of these ingredients in a taxation statute then there is no tax in law. Then it is for the legislature to do the needful in the matter.”

(Emphasis Supplied)

[See also Indian Banks’ Association, Bombay and Ors. v. M/s. Devkala Consultancy Services and Ors., JT 2004 (4) SC 587].

Further, in case of State of Rajasthan versus Rajasthan Chemists Association (2006 (202) E.L.T. 217 (S.C.)), Supreme Court relied on its own judgment in M/s. Govind Saran Ganga Saran v. Commissioner of Sales Tax &Ors. (AIR 1985 SC 1041) on analysing Article 265 noted as follows:

“The components which entered into tax are well known. The first is the character of the imposition known by its nature which transpires attracting the levy. The second is a clear communication of the person on whom the levy is imposed and which is obliged to pay the tax. The third is rate at which the tax is imposed and the fourth is the measure or value to which the rate is applied for computing the tax liability”.

Obviously, all the four components of a particular concept of tax has to be inter related having nexus with each other. Having identified tax event, tax cannot be levied on a person unconnected with event, nor the measure or value to which rate of tax can be applied can be altogether unconnected with the subject of tax, though the contours of the same may not be identified.

In case of goods imported on CIF basis, importer is nowhere connected with ocean freight services provided by freight forwarder.

Given the above discussion, it can be construed that scope of the charging section cannot be widen and person who is not included in the scope of charging section, then the same cannot be taxed.

Delegated legislation

Charging section 5 (3) has delegated power to government to notify such class of goods or services or both on which reverse charge would be applicable. In this regard, it is pertinent to note that such delegated power cannot go beyond the provisions of the mother Act.

The Supreme Court in the case of General Officer Commanding-in-Chief v. Dr. Subhash Chandra Yadav (AIR 1988 SC 876), laid down condition to rule that can have the effect of a statutory provision, two conditions must be fulfilled, namely

(1) it must conform to the provisions of the statute under which it is framed; and

(2) it must also come within the scope and purview of the rule making power of the authority framing the rule.

If either of these two conditions is not fulfilled, the rule so framed would be void.

In Ahmedabad Urban Development Authority v. Sharad kumar Jayantikumar Pasawalla and Others – AIR 1992 SC 2038, a three-Judge Bench has ruled thus “… in a fiscal matter it will not be proper to hold that even in the absence of express provision, a delegated authority can impose tax or fee. In our view, such power of imposition of tax and/or fee by delegated authority must be very specific and there is no scope of implied authority for imposition of such tax or fee. It appears to us that the delegated authority must act strictly within the parameters of the authority delegated to it under the Act and it will not be proper to bring the theory of implied intent or the concept of incidental and ancillary power in the matter of exercise of fiscal power.”

Further, in Additional District Magistrate (Rev.), Delhi Administration v. Shri Ram AIR 2000 SC 2143, it has been held that it is a well recognized principle that conferment of rule making power by an Act does not enable the rule making authority to make a rule which travels beyond the scope of the enabling Act or which is inconsistent therewith or repugnant thereto.

In B.K. Garad v. Nasik Merchants Co-op. Bank Ltd, AIR 1984 SC 192, it has been held that if there is any conflict between a statute and the subordinate legislation, the statute shall prevail over the subordinate legislation and if the subordinate legislation is not in conformity with the statute, the same has to be ignored.

Similarly, Delhi High Court in decision dated 04 March 2011 in Federation of Indian Airlines v. Union of India (WP (C) No. 8004/2010) has elaborately discussed the above proposition of law. The relevant extract of the judgment reads as under:

The basic test is to determine whether a rule to have effect must have its source of power which is relatable to the rule making authority. Similarly, a notification must be in accord with the rules, as it cannot travel beyond it.

Anant Sadashiv vs. Ratnagiri Jilha District Local Board

It is settled law that rules framed under the rule making power cannot go beyond the scope of the enactment. Rules cannot be framed in conflict with or derogating from the statute under which they are framed and whenever the rules are broad in their import and therefore inconsistent with the statute, they must yield to the statute.

Bhuwalka Steel Industries Ltd versus Union of India, 2017 (348) E.L.T. 393 (S.C.)

The Government to whom the power to make rules was given under Section 33 and the committee to whom power to make bye-laws was given under Section 34 widened the scope of “presumption” by providing further that if a notified agricultural produce is weighed, measured or counted within the notified area, it shall be deemed to have been sold or purchased in that area. The creation of legal fiction is thus beyond the legislative policy. Such legal fiction could be created only by the legislature and not by a delegate in exercise of the rule-making power.We are, therefore, in full agreement with the High Court that Rule 74(2) and Bye-law 24(5) are beyond the scope of the Act and, therefore, ultra vires…..

Further, it has been held that if it is in conflict with a longsettled line of authorities that subordinate legislation which is in conflict with the parent enactment is unsustainable.

2003 (158) E.L.T. 403 (S.C.)

ITW Signode India Ltd. versus Collector of Central Excise

…a rule framed thereunder even in case of conflict must give way to the substantive statute. It is a well-settled principle of law that in case of a conflict between a substantive act and delegated legislation, the former shall prevail inasmuch as delegated legislation must be read in the context of the primary/legislative act and not the vice-versa….

From the above discussion it could be inferred that a subordinate legislation can-not crosses the limits of the parameters laid down by the Act. Further, notification cannot go beyond nor be repugnant to the statute and it cannot extend beyond the scope or ambit of the parent Act.

Composite supply vs separate supply

In case of import of goods on CIF basis, it cannot be treated as there are two distinct supplies one is supply of goods and other is supply of services. It is a composite supply, in this regard a reference to section 2(30) of the CGST Act is invited, which defines composite supply as:

“composite supply” means a supply made by a taxable person to a recipient consisting of two or more taxable supplies of goods or services or both, or any combination thereof, which are naturally bundled and supplied in conjunction with each other in the ordinary course of business, one of which is a principal supply;

Illustration: Where goods are packed and transported with insurance, the supply of goods, packing materials, transport and insurance is a composite supply and supply of goods is a principal supply.

From the above illustration it is very clear that transport charges would be composite supply and hence co-joint reading with section 8 of the GST act, principal supply would goods and it cannot be treated as distinct supply.

Double Taxation

In case of import of goods, customs duties are leviable on CIF value of imports and accordingly IGST is also paid on the same. Given that, there is double taxation on the same value.

In this regard, Supreme Court in case of Union of India versus Intercontinental Consultants And Technocrats Pvt. Ltd. 2018 (10) G.S.T.L. 401 (S.C.)

The High Court even went on to hold further pointed out that it may even result in double taxation inasmuch as expenses on air travel tickets are already subject to service tax and are included in the bill. No doubt, double taxation was permissible in law but it could only be done if it was categorically provided for and intended; and could not be enforced by implication as held in Jain Brothers v. Union of India [(1970) 77 ITR 107]. The High Court has also referred to many judgments of this Court for the proposition that Rules cannot be over-ride or over-reach the provisions of the main enactment [Central Bank of India &Ors. v. Workmen, etc., (1960) 1 SCR 200; Babaji Kondaji Garad v. Nasik Merchants Co-Operative Bank Ltd., (1984) 2 SCC 50; State of U.P. &Ors. v. Babu Ram Upadhya, (1961) 2 SCR 679; CIT v. S. Chenniappa Mudaliar, (1969) 74 ITR 41; Bimal Chandra Banerjee v. State of M.P. &Ors., (1971) 81 ITR 105 and CIT, Andhra Pradesh v. Taj Mahal Hotel, (1971) 82 ITR 44]. The High Court also referred to the judgment of Queens Bench of England in the case of Commissioner of Customs and Excise v. Cure and Deeley Ltd. [(1961) 3 WLR 788 (QB)].

Further, in case of Sri Krishna Das vs. Town Area Committee, Chirgaon .

Nothing can be said to be double taxation, unless there is taxing of the same property or subject twice, for the same purpose, for the same period and in the same territory. To constitute double taxation, the two or more taxes must have been:

(1) levied on the same property or subject-matter,

(2) by the same Government or authority,

(3) during the same taxing period, and

(4) for the same purpose.

Strictly speaking, there is no double taxation where

(a) the taxes are imposed by different States,

(b) one of the imposition is not a tax,

(c) one tax is against property and the other is not a property tax, or

(d) the double taxation is indirect rather than direct. (See in this connection the – judgment of the Supreme Court in Sri Krishna Das v. Town Area Committee, Chirgaon, AIR 1991 SC 2096.

However, in case of 2018 (17) G.S.T.L. 561 (S.C.) Union of India Versus Mohit Mineral Pvt. Ltd., has ruled out that compensation cess is not amounting double taxation

The principle is well settled that two taxes/imposts which are separate and distinct imposts and on two different aspects of a transaction are permissible as “in law there is no overlapping”.

However, in the current scenario it can be argued that even at the time of Import IGST is payable and under Reverse Charge Mechanism IGST would be payable on the same subject matter, by the same government, at the same time and for the same purpose and hence it is amounting to double taxation.

Place of supply in case of ocean freight for goods imported on CIF basis

In case of goods imported on CIF basis, service provider is located outside India and services receiver is also located outside India and question would arise how to determine nature of supply and place of Supply.

Section 12 of the IGST Act provide for place of supply where location of supplier and recipient is in India and section 13 provide for place of supply of services where location of supplier or location of recipient is outside India.

In the current scenario both service provider and services receiver are located outside India and hence place of supply cannot be determined.

Section 7 of the IGST Act has been reproduced below:

Supply of goods or services or both,––

(a) when the supplier is located in India and the place of supply is outside India;

(b) to or by a Special Economic Zone developer or a Special Economic Zone unit; or

(c) in the taxable territory, not being an intra-State supply and not covered elsewhere in this section, shall be treated to be a supply of goods or services or both in the course of inter-State trade or commerce.

In the instant scenario, if supply (place of supply) is in taxable territory, and if the same is not covered under any other provision, then it will be considered as inter-state supply.

Since the nature of supply cannot be determine and accordingly tax liability cannot be determined.

Input tax credit

People are arguing, pay tax under reverse charge and take the credit and close the matter. However, one should also note that section 16 (2)(b) of the Central Goods and Service Tax Act, 2017 (the CGST Act).

Notwithstanding anything contained in this section, no registered person shall be entitled to the credit of any input tax in respect of any supply of goods or services or both to him unless,…..(b) he has received the goods or services or both

In the instant case, service receiver is located outside and he has received the services and it cannot be construed as importer has received services. In the notification itself stated that service provided by a person located in non-taxable territory to a person located in non-taxable territory. If both are located outside, it means the services are not received by importer who is located in India.

Concluding remarks

There are already many writ petitions filed before various High Courts across India challenging levy on ocean freight.

Given the above discussion GST should not applicable on ocean freight on following reasons:

– Importer cannot be considered services recipient and the service provider and service recipient both are outside the territory of India

– Notification is travelling beyond the scope of section

– At the time of import of goods, IGST is already paid and hence it amounting double taxation

– In case of goods imported on CIF basis, value of goods and transportation is composite supply and the same cannot be artificially bifurcated

– Place of supply cannot be determined and hence levy itself failed

Further, even if tax paid tax under RCM, there would be challenges on input tax credit since one of the condition for availing input tax credit, service has to be received.

Word of caution:

In following ruling by Authority for Advance Ruling(AAR) has ruled that the applicant is liable to pay IGST on transportation of goods by vessel under RCM under said Notification

- In re M/s. Chambal Fertilizers And Chemicals Limited (GST AAR Rajasthan); Advance Ruling No. RAJ/AAR/2018-19/14; Dated- 25/08/2018

- In re Bahl Paper Mills Ltd. (AAR Uttarakhand); Advance Ruling No. 03/2018-19; Dated-04/05/2018

(views are personal and author can be reached at nilesh@bsllp.in)

Whole system of RCM is double work for businesses and unproductive. Further GST on ocean freight is double tax as cost of imported goods already includes freight for duty and GST calculations then why GST on ocean freight by importer again on RCM.

Why don’t government completely scrap RCM and why carry legacy of Chidambaram? He was fond of making provisions for troubles to businesses they this government has not improved at all.

So pathetic. Soon this government will loose all credibility….