1. Background:

1.1. This is the right time to discuss the framework of GST as its likely to be a reality with effect from 01 July 2017. GST law is dual tax mechanism where the State and Center both will be charge the tax.

1.2. The GST law is known to be One Nation, One Tax. But if we go through the law, it provides many situations where we find this slogan is not workable. We have focused on the major concern of GST law that What is Inter-State or Intra- State Transactions?, Why it is important to determine?, How this can be determined and any other implications ?. We will also discuss the industry specific charge ability on whether to charge IGST or CGST/SGST/UTGST.

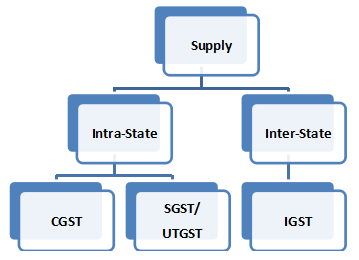

2. What is Intra- State and Inter- State Supply:

The above two terms have been defined under Section 7 and 8 of IGST Act, 2017. Section 7 provides for determination of Inter-State Supply whereas Section 8 provides for determining the Intra- State Supply.

3. How to distinguish between Intra- State Supply and Inter- State Supply:

3.1. A supply can be categorized as Intra- State Supply if the following conditions are satisfied:

3.1.1. The Location of Supplier and Place of Supply are in the same State or Union Territory;

3.2. A supply can be categorized as Inter-State Supply in the following situations:

3.2.1. The Location of Supplier and Place of Supply are in different State or Union Territory;

3.2.2. The imported goods till they cross the customs frontiers of India(CFI);

3.2.3. The import of services;

3.2.4. The export of goods;

3.2.5. The export of services;

3.2.6. The location of supplier in India and Place of supply outside India;

3.2.7. Supply to or by SEZ Developer/ unit;

“location of the supplier of services” means,–

(a) where a supply is made from a place of business for which the registration has been obtained, the location of such place of business;

(b) where a supply is made from a place other than the place of business for which registration has been obtained (a fixed establishment elsewhere), the location of such fixed establishment;

(c) where a supply is made from more than one establishment, whether the place of business or fixed establishment, the location of the establishment most directly concerned with the provision of the supply; and

(d) in absence of such places, the location of the usual place of residence of the supplier;

The place of supply for goods is defined as per section 10 & 11 and for services is defined as per section 12 & 13 of IGST Act, 2017;

3.3. The GST law does not define the location of supplier for goods. Considering that the location of supplier will be location of goods, in this type of transaction there will not be any inter- State supply since the location of the supplier and the place of supply will be in the same State.

However, the most crucial thing is to determine the Place of Supply of services or goods. The IGST law shall be referred for section 10, 11, 12 & 13 to determine the place of supply.

4. Why supply is required to be differentiated?

4.1. Under GST regime, 4 types of taxes i.e. CGST, SGST, UTGST and IGST. If a transaction/supply is determined as Intra- State Supply then CGST and SGST/UTGST shall be chargeable and payable whereas in case of Inter-State Supply then IGST shall be chargeable and payable.

4.2. Therefore, it is well established that different taxes is to be paid on respective supplies and it becomes more important to determine the Supply to be Intra- State and Inter-State supply.

5. What are the Consequences of wrongfully taxes collected and paid?

5.1. As per section 77 of CGST Act, 2017, where a registered taxable person who has paid the CGST & SGST/UTGST considering a transaction to be an Intra- State supply but subsequently such transaction held to be an Inter-State Supply, then IGST shall be payable (with no interest) and refund would be claimable of CGST & SGST/UTGST under the provisions of refund;

5.2. In the same line, section 19 of IGST Act, 2017 provides for refund of IGST and payment of correct tax i.e. CGST & SGST/UTGST;

5.3. Wrong paid tax shall be refundable and correct tax would be required to be paid;

5.4. Therefore, it becomes most important and critical to correctly determine the category of supply;

6. The following are industry specific cases/instances denoting the applicability of CGST & SGST/UTGST or IGST:

| S.No. | Nature of business | Category of Supply | Applicable tax |

| 1 | Hotel, Inns, etc. | Intra- State Supply | CGST & SGST/ UTGST |

| 2 | Restaurants | Intra- State Supply | CGST & SGST/ UTGST |

| 3 | Import/Export of goods | Inter-State Supply | IGST |

| 4 | Import/ Export of services | Inter-State Supply | IGST |

| 5 | Renting of immovable property | Intra- State Supply (If landlord and property is located in same State) | CGST & SGST/ UTGST |

| 6 | Renting of immovable property | Inter-State Supply (If landlord and property is located in different State) | IGST |

7. Conclusion:

We have discussed the determining fundamentals of IGST and CGST/SGST/UTGST and implications of wrong tax payment. It is pertinent to note that refund can be claimed within 2 years from the relevant date however the assessment from department can be concluded within 3 years or 5 years from the due date of furnishing of annual return for the Financial Year to which tax relates.

Keeping the above provisions, it is very important to define and document a transaction as Inter-State Transaction and Intra- State Transaction.

Disclaimer: The entire contents of this document have been prepared on the basis of relevant provisions and as per the information existing at the time of the preparation. The observations of the authors are personal view and this cannot be quoted before any authority without the written permission of the authors. This article is meant for general guidance and no responsibility for loss arising to any person acting or refraining from acting as a result of any material contained in this article will be accepted by authors. It is recommended that professional advice be sought based on the specific facts and circumstances. This article does not substitute the need to refer to the original pronouncements on GST.

(Authors– CA Neeraj Kumar and CA Deepak Arya, RAPG & Co. Chartered Accountants from Delhi and can be reached at info@rapg.in, 9999836182/9818449179)

My GST number is registered in Delhi. A present I have taken only single registration for delhi and have shown my residence as place of business, which is similar to what I had during service tax registration.

I have given commercial space on rent to two parties in Gurugram, Haryana.

one with registration in Haryana and

other with registration in Tamilnadu.

Do I need to take separate registrations for both

places. (Place of supply in both cases is same ie. Gurugram).

What would be applicable tax/es to be charged from them.

Thanks and regards.