GST Revenue Collection

₹1,60,122 crore gross GST revenue collected for March 2023

The gross GST revenue collected in the month of March 2023 is ₹1,60,122 crore of which CGST is ₹29,546 crore, SGST is ₹37,314 crore, IGST is ₹82,907 crore (including ₹42,503 crore collected on import of goods) and cess is ₹10,355 crore (including ₹960 crore collected on import of goods). It is for the fourth time, in the current financial year that the gross GST collection has crossed ₹1.5 lakh crore mark registering second highest collection since implementation of GST. This month witnessed the highest IGST collection ever.

The government has settled ₹33,408 crore to CGST and ₹28,187 crore to SGST from IGST as regular settlement. The total revenue of Centre and the States in the month of March 2023 after IGST settlement is ₹62,954 crore for CGST and ₹65,501 crore for the SGST.

The revenues for the month of March 2023 are 13% higher than the GST revenues in the same month last year. During the month, revenues from import of goods was 8% higher and the revenues from domestic transaction (including import of services) are 14% higher than the revenues from these sources during the same month last year. The return filing during March 2023 has been highest ever. 93.2% of statement of invoices (in GSTR-1) and 91.4% of returns (in GSTR-3B) of February were filed till March 2023 as compared to 83.1% and 84.7%, respectively same month last year.

The total gross collection for 2022-23 stands at ₹18.10 lakh crore and the average gross monthly collection for the full year is ₹1.51 lakh crore. The gross revenues in 2022-23 were 22% higher than that last year. The average monthly gross GST collection for the last quarter of the FY 2022-23 has been ₹1.55 lakh crore against the average monthly collection of ₹1.51 lakh crore, ₹1.46 lakh crore and ₹1.49 lakh crore in the first, second and third quarters respectively.

The chart below shows trends in monthly gross GST revenues during the current year.

Source: PIB Press Release dated 01.04.2023

15% increase in GST Collection Year-on-Year (Y-o-Y)

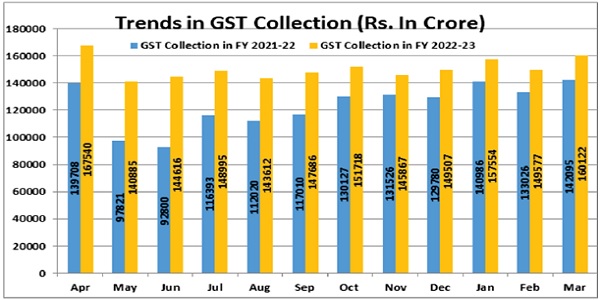

There has been an increase of 15% in GST Collection in the month of December (FY 2022-23) as compared to the month of December (FY 2021-22). This was stated by the Union Minister of State for Finance Shri Pankaj Chaudhary in a written reply to a question in Lok Sabha today.

Also, the Minister stated, the monthly GST revenue is more than 1.4 lakh crore for 11 consecutive months in the FY 202223. The details of GST collection for FY 2022-23 are as under:

(in Rs. crore)

| Month | 2021-22 | 2022-23 (till Feb, 2023) |

| April | 1,39,708 | 1,67,540 |

| May | 97,821 | 1,40,885 |

| June | 92,800 | 1,44,616 |

| July | 1,16,393 | 1,48,995 |

| August | 1,12,020 | 1,43,612 |

| September | 1,17,010 | 1,47,686 |

| October | 1,30,127 | 1,51,718 |

| November | 1,31,526 | 1,45,868 |

| December | 1,29,780 | 1,49,507 |

| January | 1,40,986 | 1,57,554 |

| February | 1,33,026 | 1,49,577 |

Source: PIB Press Release dated 27.03.2023

Third National Meeting of Group of Ministers (GoM) to suggest reforms in Goods & Services Tax (GST) collection system held on 13.02.2023

The 3rd National Meeting of Group of Ministers (GoM) to suggest reforms in Goods & Services Tax (GST) collection system held on 13.02.2023 at Sahyadri, Mumbai, with Maharashtra Deputy Chief Minister Devendra Fadnavis, Tamil Nadu Finance Minister Dr. Palanivel Thiagarajan, Haryana Deputy Chief Minister Dushyant Chautala. Officials from Maharashtra & Telangana attended the meeting in Mumbai, while Finance Ministers from Andhra Pradesh, Orissa and Delhi joined in the meeting via VC. A presentation was made before the GoM by the Senior Officials from the Union Finance Ministry.

In this meeting, reforms were suggested to make GST collection stricter, to remove the difficulties faced by taxpayers to make the tax payment system easier and faster, automization of systems, data sharing between States.

Notifications

> Notification No. 02/2023– Central Tax dated 31.03.2023 regarding Amnesty to GSTR-4 non-filers

The Central Government vide the said Notification has waived late fees completely in case of FORM GSTR-4, if it is a NIL return, for the periods from July, 2017 till F.Y. 2021-22 and reduced to Rs 500/- in other cases provided the said returns are filed between 01.04.2023 to 30.06.2023.

> Notification No. 03/2023– Central Tax dated 31.03.2023 regarding extension of time limit for application for revocation of cancellation of registration

The Central Government vide the said Notification has provided amnesty scheme for registered persons whose registrations have been cancelled on or before 31.12.2022 due to non-filing of returns. The registered persons may apply for revocation of cancellation of their registrations till 30.06.2023, only after furnishing the returns due up to the effective date of cancellation of registration and after the payment of any amount due as tax, in terms of such returns, along with any amount payable towards interest, penalty and late fee in respect of the such returns. The said Notification also provides that no further extension of time period for filing application for revocation of cancellation of registration shall be available in such cases.

> Notification No. 04/2023– Central Tax dated 31.03.2023 regarding amendment in CGST Rules

The Central Government vide the said Notification has made certain amendments in Rule 8(4A) & Rule 8(4B) of the Central Goods and Services Tax Rules, 2017 pertaining to procedure regarding Aadhar authentication and biometric verification of applicants. The said changes shall be deemed to have come into force from 26.12.2022.

> Notification No. 05/2023– Central Tax dated 31.03.2023 seeking to amend Notification No. 27/2022 dated 26.12.2022

The Central Government vide the said Notification has amended Notification No. 27/2022 – Central Tax, dated 26.12.2022 wherein for the words, “provisions of”, the words “proviso to” shall be substituted. The said change shall be deemed to have come into force from 26.12.2022.

> Notification No. 06/2023– Central Tax dated 31.03.2023 regarding amnesty scheme for deemed withdrawal of assessment orders issued under Section 62 of the CGST Act

The Central Government vide the said Notification has notified that the registered persons who failed to furnish a valid return within a period of thirty days from the service of the assessment order issued on or before the 28.02.2023 under sub-section (1) of Section 62 of the CGST Act, as the classes of registered persons, in respect of whom said assessment order shall be deemed to have been withdrawn, provided that such registered persons follow the special procedures listed below:

i. the registered persons shall furnish the said return on or before 30.06.2023;

ii. the return shall be accompanied by payment of interest due under sub-section (1) of Section 50 of the CGST Act and the late fee payable under Section 47 of the said Act.

This would be irrespective of whether or not an appeal had been filed against such assessment order under Section 107 of the said Act or whether or not the appeal, if any, filed against the said assessment order has been decided.

> Notification No. 07/2023– Central Tax dated 31.03.2023 regarding rationalisation of late fee for GSTR-9 and Amnesty to GSTR-9 non-filers

The Central Government vide the said Notification has rationalized the amount of late fee referred to in Section 47 of the CGST Act in respect of the return to be furnished under Section 44 of the said Act for the financial year 2022-23 onwards, which is in excess of amount as specified in Column (3) of the Table below, for the classes of registered persons mentioned in the corresponding entry in Column (2) of the Table below, who fails to furnish the return by the due date. The same has been tabulated below for easy understanding of our readers.

|

Sr No. . |

Class of Registered Persons

(2) |

Amount

(3) |

| 1. | Registered persons having an aggregate turnover of up to five crore rupees in the relevant financial year. | Twenty- five rupees per day, subject to a maximum of an amount calculated at 0.02 percent of turnover in the State or Union territory |

| 2. | Registered persons having an aggregate turnover of more than five crore rupees and up to twenty crore rupees in the relevant financial year. | Fifty rupees per day, subject to a maximum of an amount calculated at 0.02 percent of turnover in the State or Union territory |

The said Notification also provides that for the registered persons who have failed to furnish their annual returns for F.Y. 2017-18, 2018-19, 2019-20, 2020-21 or 2021-22 but furnish the same between 01.04.2023 to 30.06.2023, the total amount of late fee under section 47 of the said Act payable in respect of the said return, shall stand waived which is in excess of ten thousand rupees.

> Notification No. 08/2023– Central Tax dated 31.03.2023 regarding Amnesty to GSTR-10 non-filers

The Central Government vide the said Notification has provided amnesty scheme to waive the amount of late fee referred to in Section 47 of the CGST Act, which is in excess of five hundred rupees for the registered persons who fail to furnish the final return in FORM GSTR-10 by the due date but furnish the said return between the period from the 01.04.2023 to 30.06.2023.

> Notification No. 09/2023– Central Tax dated 31.03.2023 regarding extension of limitation under Section 168A of CGST Act

The Central Government vide the said Notification has invoked Section 168A of the CGST Act to extend the time limit for issuance of order under Section 73 of the said Act for recovery of tax not paid or short paid or of ITC wrongly availed or utilized. The extended due dates are reproduced herein below for ease of reference:

(I) for the financial year 2017-18, up to the 31st day of December, 2023;

(ii) for the financial year 2018-19, up to the 31st day of March, 2024;

(iii) for the financial year 2019-20, up to the 30th day of June, 2024.

Notifications – Compensation Cess

> Notification No. 01/2023 – Compensation Cess dated 31.03.2023 seeking to provide commencement date for Section 163 of the Finance Act, 2023

The Central Government vide the said Notification has notified the provisions of Section 163 of the Finance Act, 2023 relating to levy of compensation cess based on Retail Sale Price (RSP).

> Notification No. 02/2023 – Compensation Cess (Rate) dated 31.03.2023 seeking to further amend notification No. 1/2017-Compensation Cess (Rate), dated 28.06.2017

The Central Government vide the said Notification has notified to change compensation cess on tobacco and pan masala from ad valorem to RSP based.

Circulars

> Circular No. 191/03/2023-GST dated 27.03.2023 pertaining to clarification regarding GST rate and classification of ‘Rab’

Based on the recommendation of the GST Council in its 49th Meeting, held on 18.02.2023, 5% GST rate has been notified on Rab, when sold in pre-packaged and labelled, and Nil GST, when sold in other than pre-packaged and labelled. This change in rate came into force with effect from 01.03.2023.

The Central Government vide the said Circular has clarified that in view of the prevailing divergent interpretations and genuine doubts regarding the applicability of GST rate on ‘Rab’, the issue for the past period is regularized on “as is” basis.

State Best Practices

> Outreach Programme on improvement of compliance in e-Invoice organized by CGST Commissionerate, Udaipur

CGST Commissionerate, Udaipur organized an Outreach Programme on 25.03.2023 with special focus on budgetary changes in the Union Budget 2023-24 and for improvement of compliance in e-Invoice issuance by the eligible taxpayers. 87 Officers and taxpayers have attended the programme.

> GST Symposium “KAR-TAVYA” organized by Jammu & Kashmir

GST Symposium “KAR-TAVYA” was organized by Jammu & Kashmir GST department and the GST symposium and Tax awareness initiative ‘Kar-Tavya’ for industries, traders associations, DDOs & other stakeholders were inaugurated by Lieutenant Governor Manoj Sinha. During his address the Lt. Governor stated that everyone must come forward in making J&K a dynamic and developed region of the country and he also invited suggestions from all sections of society for making better arrangements in property tax.

On the occasion, the Lt Governor unveiled ‘Kar-Tavya’ periodical and ‘Kar-Tavya’ booklet and also handed over the Letter of Appreciation to organizations and top taxpayers of the UT. The symposium was also attended by Dr. Arun Kumar Mehta, Chief Secretary; Dr. Rashmi Singh, Commissioner, State Taxes; Sh Ranjit Kumar Agarwal, National VP, Institute of Chartered Accountants India (ICAI), other senior officers and various stakeholders.

As part of Tax Awareness Initiative ‘Kar-Tavya’, Commissioner State Taxes Dr. Rashmi Singh interacted with trading Community and officers and she stressed that along with kartavya of citizens to pay taxes, it must also be kartavya of DDOs to file timely returns.

> Knowledge enhancement sessions under the aegis of NACIN, Faridabad and Mumbai and NADT.

The Central Excise & Service Module for the Officer Trainees (OTs) of 74th Batch of IRS (C&IT) was organized from 13.03.2023 to 24.03.2023 at NACIN, Faridabad. The objective of organizing it was to train the officers and educate them with the practices followed at ground level while implementing Excise and Service Tax.

Ms. Ashima Bansal, Joint Secretary and Mr. S.S. Shardool, Director, GST Council Secretariat addressed the trainees on 14.03.2023 and took the sessions on Registration and Assessment under Central Excise Act, 1944. During the session, they emphasized on the Valuation and Classification of goods under Central Excise Act and its correlation with the practice implemented in the GST regime.

Further, sessions on overview of GST Council Secretariat and its working, Cooperative Federalism and on the 48th GST Council meeting have also been taken on various fora. Knowledge sharing with NADT to elaborate on GST and information in returns that would be beneficial for officers of Income tax Department have also been held in the past for NADT along with senior officer from DGTPS.

> Workshop on “Cyber Forensics: Tracing Digital Footprints for effective investigation & prosecution under GST” for officers of Haryana and Delhi by CoE, NACIN

CoE, NACIN organized two days’ workshop on “Cyber Forensics: Tracing Digital Footprints for effective investigation & prosecution under GST” for officers of Haryana and Delhi. Sh. Anupam Prakash, Commissioner at CGST Delhi East inaugurated the workshop.

> Online Training on ‘GST Refresher Course’ by NACIN, Mumbai

NACIN, Mumbai on 15.03.2023 organised two days Online Training on ‘GST Refresher Course’. More than 225 Officers from CGST from pan India and SGST, Maharashtra attended the Online Training.

GST Portal Updates

> Advisory for the taxpayer wishing to register as “One Person Company” in GST

As per provision of Section 2(62) of The Companies Act, 2013 “One Person Company” is defined as a company which has only one person as member.

Some issues have been raised by the persons registering as ‘One Person Company’ while they take GST registration. Upon analysis, it was noticed that the option of choosing One Person Company is not there in form notified by CGST/SGST Acts and hence it is not available on the GSTN portal.

As a work around, GSTN has advised that in the ‘Part B’ of GST Registration Form ‘REG-01’, applicant may select (Constitution of Business under ‘Business Details’ tab using dropdown list) option “Others”, if the taxpayer wants to register for GST as “One Person Company”. After selecting option as “Others”, the applicant shall also mention “One Person Company” in the text field and follow the steps for a normal registration application to complete the process.

Portal update on 21.03.2023

> Advisory: GSTN launches e-Invoice registration services with private IRPs

In another step towards further digitization of the business process flow, GSTN has launched the e-Invoice registration services through multiple private IRPs at the recommendation of the GST Council. Four private companies viz. Clear Tax, Cygnet, E&Y and IRIS Business Ltd were empaneled by GSTN for providing these e-Invoice registration services to all GST taxpayers of the country. The details of the existing and new IPRs is available at https://einvoice.gst.gov.in/einvoice/dash board

The taxpayers now have a choice of more than one IRP (earlier being the only single portal of NIC), which they can use to register their e-invoices. This adds significant capacity to the single e-invoice registration portal which existed earlier.

The end-to-end flow of a digitally signed e-invoice between sellers and buyers by integration with the GST system will lead to ease of compliance for the taxpayers. It will also lead to facilitation of auto-drafting and auto-populating of invoice details in the GST returns which would lead to increased accuracy, correctness of reporting of supplies and availing of ITC by the recipients of the supply.

Portal update on 04.03.2023

> HSN Code Reporting in e-Invoice on IRPs Portal

As per the Notification No. 78/2020 – Central Tax dated 15th October 2020, it is now mandatory for taxpayers to report a minimum of six-digit valid HSN code for their outward supplies having AATO of more than 5 crores in any previous financial year. This requirement has already been implemented in the GST system, and GSTN is in the process of implementation of the same at IRP portal in collaboration with GSTN IRP partners including NIC. It is further suggested that in case wherever valid six digit HSN code is not available, a corresponding valid eight digit HSN code be reported instead of artificially creating six digit HSN code.

Portal update on 04.03.2023

Legal Corner

> Ubi Jus Ibi Remedium

“Ubi Jus Ibi Remedium” is a Latin maxim that translates to mean “where there is a right, there is a remedy”. This maxim stipulates that that where law has established a right there should be a corresponding remedy for its breach. The word “jus” means legal authority to do something or to demand for something. The word “remedium” means that person has the right of action in the court of law. It essentially means that when the law clothes a man with a right he must have means to vindicate and maintain it and remedy if he is injured in the exercise and enjoyment of it.

The law of torts has developed on the premises of this maxim. However, it is to be understood that in order to rely on this doctrine, the injury occasioned to the person must be in consequence of breach of a legally vested right. It cannot be made in case of moral wrongs which are not per se actionable. Further, the applicability of this doctrine is barred in cases where a statute specifically bars the remedy.

This principle is fundamental to the rule of law, and it ensures that individuals can seek justice and obtain a remedy for any harm suffered as a result of the violation of their legal rights. It is a guiding principle for courts and other dispute resolution mechanisms to ensure that they provide effective remedies to those who have suffered a legal wrong.

> Respondeat Superior

“Respondeat Superior” is a Latin term that translates to mean “let the master answer” . In legal terms, it refers to the principle of vicarious liability, where an employer or superior is held responsible for the actions of their employees or agents performed within the scope of their employment or agency. When Respondeat Superior applies, an employer will be liable for an employee’s negligent actions or omissions that occur during the course and scope of the employee’s employment. This means that the employee must be performing duties for the employer at the time of the negligence for the employer to be held liable under Respondeat Superior.

This principle is based on the idea that employers or principals have control and authority over their employees or agents and therefore, should be responsible for their actions. Respondeat Superior is often applied in cases of personal injury, medical malpractice, or negligence, where an employee’s actions have caused harm to another person.

To establish liability under Respondeat Superior, it must be shown that the employee or agent was acting within the scope of their employment or agency when the wrongful act occurred. If the employee was acting outside the scope of their employment or agency, the employer or principal may not be held liable under this principle.

Farewell

Additional Secretary Sh. Pankaj Kumar Singh bidding farewell to Mr. Shubham Singh Rathore, Research Fellow (law).

Mr. Shubham Singh Rathore is an Advocate and joined GST Council Secretariat on 15.06.2021. He contributed in the legal matters and kept himself abreast with the latest case laws on the GST. He was relieved on 31.03.2023. We wish him the best in his future endeavours.

Source of Newsletter – https://gstcouncil.gov.in/