E-way Bill for Inter-state transactions become mandatory with effect from 1st of April’2018 and for Intra- State in a phased manner but before 30th June’2018. Already five states – Andhra Pradesh, Gujarat, Kerala, Telangana, uttar Pradesh decided to go with E-Way Bill for Intra-State transactions in their respective states.

e-way bill is a document required to be carried by a person in charge of the conveyance carrying any consignment of goods of value exceeding fifty thousand rupees as mandated by the Government in terms of Section 68 of the Goods and Services Tax Act, 2017 read with Rule 138 of the rules framed thereunder. It is generated from the GST Common Portal for e-Way bill system by the registered persons or transporters who cause movement of goods of consignment before commencement of such movement.

There are certain doubts and apprehensions regarding generation of E-way Bills in case of Import Consignments. Let us discuss in this paper regarding those aspects in detail.

Also Read- How to Generate E-Way Bill for Import

Import – Imported Goods – Importer:

As per Sec 2(23) of Customs Act 1962, “import“, with its grammatical variations and cognate expressions, means bringing into India from a place outside India;

Sec 2(24) of Customs Act 1962 “import manifest” or “import report” means the manifest or report required to be delivered under section 30;

Sec 2(25) of Customs Act 1962 “imported goods” means any goods brought into India from a place outside India but does not include goods which have been cleared for home consumption;

As per Sec 2(10) of IGST Act : ‘‘import of goods” with its grammatical variations and cognate expressions, means bringing goods into India from a place outside India.

Sec 2(26) of Customs Act 1962: “importer“, in relation to any goods at any time between their importation and the time when they are cleared for home consumption, includes 18[any owner, beneficial owner] or any person holding himself out to be the importer;

Se 2(27) of Customs Act 1962: “India” includes the territorial waters of India.

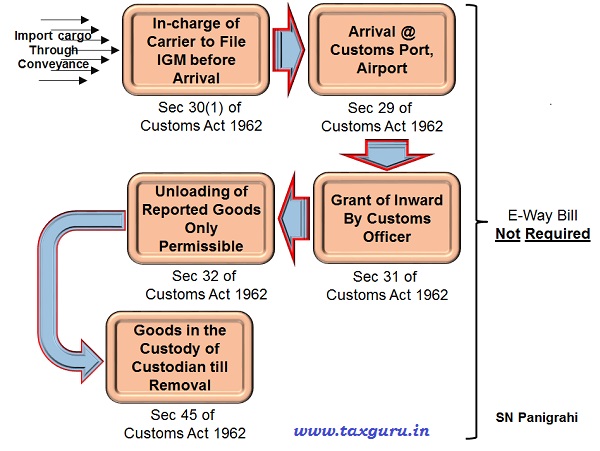

Conveyances Carrying Imported Goods – Arrival at Customs Port or Airport :

Sec 29(1) of Customs Act, provides that the person-in-charge of a vessel or an aircraft entering India from any place outside India shall call or land at customs port or a customs airport, as the case may be. Further Sec 30(1) of Customs Act provides that the person-in-charge of – a vessel; or an aircraft; or a vehicle, carrying imported goods shall, file an import manifest (generally called IGM – Import General Manifesto) by presenting electronically twelve hours prior to the arrival of the vessel or the aircraft. After delivery of Import Manifesto customs offices grants Entry Inwards under Sec 31 of Customs Act. Sec 32 of the Customs Act provides that only those goods mentioned in the Import Manifesto can be unloaded.

As per Sec 45 of the Customs Act, import goods after unloaded, remains in the custody of Port Trust Authority in case of major ports and Air Ports Authority of India in case of airports, but under control of Customs Officers till goods are cleared.

Customs Entry Inward – E-Way Bill Not Required:

Until the imported goods are cleared and given Out of Customs Charge order by customs officer, such goods are in the custody of customs. Therefore, for entry of imported goods to Indian customs from a place outside India no E-Way Bill is required.

Transport from Customs Port / Airport to ICD / IFS: E-Way Bill Not Required

Import consignments after unloaded at Customs Port / Airport are generally moved to Inland Container Depot (ICD) or a Container Freight Station (IFS) for clearance by Customs.

As per Rule 138(14)(c) of CGST Rules, No E-Way Bill is required where the goods are being transported from the customs port, airport, air cargo complex and land customs station to an inland container depot or a container freight station for clearance by Customs.

Entry of Goods on Importation – Clearance by Customs:

As per Sec 46(1) of Customs Act, the importer of any goods, shall make entry thereof by presenting electronically to the proper officer a bill of entry for home consumption or warehousing in the prescribed form.

Sec 46(3) of Customs Act provides that the importer shall present the bill of entry under sub-section (1) before the end of the next day following the day (excluding holidays) on which the aircraft or vessel or vehicle carrying the goods arrives at a customs station at which such goods are to be cleared for home consumption or warehousing.

Clearance of Goods for Home Consumption – Transport After Clearance: E-Way Bill Required

As per Sec 47(1) of Customs Act, where the proper officer is satisfied that any goods entered for home consumption are not prohibited goods and the importer has paid the import duty, the proper officer may make an order permitting clearance of the goods for home consumption.

After the Customs clearance for Home Consumption, the importer may take the goods to his place of business. For Transport After Customs Clearance E-Way bill is Required to be generated by the Importer or his Authorized Transporter.

Clearance of goods for Ware-House – Transport to Ware-House: E-Way Bill Not Required

As per Sec 59 (1) of Customs Act, the importer shall execute a ware-house bond for a sum equal to twice the amount of the duty assessed on such goods for keeping the goods in warehouse without payment of duty and latter clearing on payment of duty when required. As per Sec 60 the proper officer may make an order permitting the deposit of the goods in a warehouse when the provisions of section 59 have been complied with in respect of any goods. In such case the goods move from Customs Station to Warehouse under Customs Seal.

Rule 138(14)(h)(ii) of CGST Rules, provides that No E-way Bill Required where the goods are being transported under customs seal.

Clearance of Warehoused Goods for Home Consumption – Ex-Bond Clearance – Transport to Importers Place of Business: E-Way Bill Required

The importer of any warehoused goods under Sec 68 of Customs Act may clear them for home consumption, by filling bill of entry for home consumption in respect of such goods and on payment of import duty leviable on such goods and an order for clearance of such goods for home consumption has been made by the proper officer.

After such Ex- Bond Clearance by importer the goods may be transported to any business place of the importer. For such transportation E-Way Bill is required.

General Exemptions for E-Way Bill are Also Applicable

In all the above discussions where it has been mentioned that E-Way Bill is required are also subject to general provisions exempting the requirement of E-Way Bill as per Rule 138 (14), such as goods as mentioned in Annexure to the Rule, alcoholic liquor for human consumption, petroleum crude, high speed diesel, motor spirit (commonly known as petrol), natural gas or aviation turbine fuel; Exempted goods etc

For example, if the Imported goods are exempted under GST, in such case for transportation for home consumption after customs clearance, No E-Way Bill is Required

Disclaimer : The views and opinions; thoughts and assumptions; analysis and conclusions expressed in this article are those of the authors and do not necessarily reflect any legal standing.

Author : SN Panigrahi, GST Consultant, Practitioner, Corporate Trainer & Author

Can be reached @ snpanigrahi1963@gmail.com

is e way bill required for import by 100% EOU located in same state

We are importing high end equipments/machinery/perishable/hazardous chemicals etc. In most of the cases Indian Agent/Indian Arm company is involved in clearing the consignments. In such cases after clearance of the consingment who will have to generate the e way bill. Whether the clearing agent or the Importer.

We are GST Regd Manufacturing Unit & importing COAL TAR PITCH Cargo from the Country EGYPT & the Vessels will be arrive on 24th April 2018 in Vizag Sea Port,mean while we are processing Customs Documentation i.e Filing B.E & Duty Payment etc.. with our CHA. after that the Container will be move to CFS Gate Way, Visahapatnam ( AP ) & from there we have to Lift the Cargo through our Transport Vehicle to our Factory Premises,Visahapatnam.( 50 Km Distance from CFS Gate Way to our Factory )

Sir with refer above we want to know is it require GST E- Way Bill for Import Cargo during Transportation of ? & if Yes plz guide us how to generate the Import GST E-Way Bill & how the value will be calculated…

triple duty bond under section 59 of CA.

Exempted goods under GST for imported goods may be explained. If the goods are cleared under Advance Lce, EOU ( annexure) , then Way bill is compulsory or not.

Very well explained

Nicely explained Article.

Very well described atleast the customs Act part makes eway more complicated which is well explained.

My above query is very important for generation of online waybill for transportation of the goods from customs to the business place in other State. If name of the importer is mentioned at both places, system is not considering IGST separately.

if transporter LIke DHL is carrying goods from foreing country to india company, door to door. service.

How e way bill is to issued?

what will be address of supllier to mention on e way bill as maximum 4000 km is permissible

In cases f=of ‘E-Waybill Required” who is the consignor, details of CHA & his GSTIN be used to generate e-waybill

Please inform whose name is to be mentioned in the delivery challan as sender – whether the exporter’s name or the importer’s name himself at both the places “Sender” and “Receiver” while carrying the goods from customs to the importer’s business place in other State.