A. FAQs on Comparison of Liability Declared and ITC Claimed General

GST Tax Liabilities and ITC Comparison Report

Q.1 What is GST Tax Liabilities and ITC Comparison Report?

Ans: The GST Tax liabilities and ITC Comparison report is the comparison of liability declared and ITC claimed by the Taxpayer. The Tax Liabilities and ITC Comparison option under the Returns tab enables you to:

- View month- wise Tax liability declared in Form GSTR-3B and Form GSTR-1, and

- Compare ITC claimed in Form GSTR-3B and ITC accrued as per Form GSTR-2A/GSTR-2B

Tax liabilities and ITC comparison report comprises of the following reports:

- Tax liability and ITC statement (Summary)

- Tax liability other than export / reverse charge

- Tax liability due to reverse charge

- Tax liability due to export and SEZ supplies

- Input credit claimed and due (Other than import of goods)

- Input tax credit claimed and due (Import of goods)

The Tax liability and ITC Statement (Summary)

Q.2 From where can I view comparison of liability declared in Form GSTR-3B and Form GSTR-1 with ITC claimed in Form GSTR-3B and as accrued in Form GSTR-2A/2B?

Ans: Navigate to Services > Returns > Tax liabilities and ITC comparison > Select Financial Year and click the SEARCH button. The “Credit and Liability Statement” page is displayed that provides summary and tables containing comparative details of liability declared in Form GSTR-3B & Form GSTR-1 and ITC claimed in Form GSTR-3B and as accrued in Form GSTR-2A/GSTR-2B.

Q.3 What type of comparison reports are available on Credit and Liability Statement page?

Ans: Listed below are the comparison reports available on the “Credit and Liability Statement” page:

1. Tax Liability and Input Tax Credit (ITC) Statement (Summary)

2. Tax Liability other than export/ reverse charge

3. Tax Liability due to reverse charge

4. Tax Liability due to export and SEZ supplies

5. Input tax credit claimed and due (Other than import of goods)

6. Input tax credit claimed and due (Import of goods)

Q.4 How can I download my tax liability and ITC statement summary?

Ans: To download your tax Liability and ITC Statement summary, click the DOWNLOAD COMPARISON REPORT (EXCEL) button provided on the right-below corner of the Credit and Liability Statement page. The complete comparison reports will get downloaded in Excel format. Different reports are available in separate sheets.

Click the DOWNLOAD CSV button available under each report to download individual report in a CSV format.

Q.5 How frequently is the “Credit and Liability Statement” report generated?

Ans: The “Credit and Liability Statement” report is generated on near real time basis based on Form GSTR-1 and Form GSTR-3B filed by you and after generation of Form GSTR-2B. The report generation time is also displayed on the top white band of the Credit and Liability Statement page.

Tax Liability other than export/ reverse charge

Q.6 From where can I view the tax liability other than export/ reverse charge report?

Ans: 1. Navigate to Services > Returns > Select Financial Year > click the + icon on the right side of the Tax liability other than export/ reverse charge tab.

2. The tax liability other than export/ reverse charge details are displayed in a table.

3. Click the DOWNLOAD (CSV) button to download the table in a CSV format.

Q.7 What is the purpose of tax liability other than export/ reverse charge report?

Ans: The Tax liability other than export/ reverse charge report displays the following details:

- Liability as declared in table 3.1 (a) of Form GSTR-3B during the month

- Liability as declared in table 4A, 5, 6C, 7, 9A, 9B, 9C, 10, 11 of Form GSTR-1 (other than reverse charge supply) during the month

- Shortfall/ excess for the tax period and cumulative shortfall/excess for the financial year

This comparative table will help the taxpayer to have the overview of liabilities (other than export and reverse charge) declared in Form GSTR-3B and Form GSTR-1 and to check whether liability is correctly declared. Corrective actions on liability declared on these forms/ return can be taken by the taxpayer in case of any discrepancy. This may also be used as a reference to declare liability in Form GSTR-3B, once Form GSTR-1 is filed for such tax period.

Q.8 Which tables of Form GSTR-1 and Form GSTR-3B are included for comparison in tax liability other than export/ reverse charge report?

Ans: Following tables are included for comparison in tax liability other than export/ reverse charge report:

- The table 3.1(a) – Outward taxable supplies (other than zero rated, nil rated and exempted) of Form GSTR-3B is considered for the comparison of liabilities.

- The following tables of Form GSTR-1 have been considered for computing the liabilities:

- Table 4A – Supplies other than those attracting reverse charge and supplies made through e-commerce operator

- Table 5 – Taxable outward inter-State supplies to un-registered persons where the invoice value is more than Rs 2.5 lakh

- Table 6C – Deemed exports

- Table 7 – Taxable supplies (Net of debit notes and credit notes) to unregistered persons other than the supplies covered in Table 5

- Table 9 – Amendments to taxable outward supply details furnished in statements for earlier tax periods in Table 4A, 4C, 5 and 6C (including debit notes, credit notes issued during current period and amendments thereof)

- Table 10 – Amendments to taxable outward supplies to unregistered persons furnished in returns for earlier tax periods in Table 7

- Table 11 – Advances received/Advances adjusted in the current tax period/ Amendments of information furnished in earlier tax period

Q.9 Data from which tables of Form GSTR-1 are excluded from comparison of tax liability, other than export/ reverse charge report ?

Ans: Tables 4B, 6A, 6B, 9A, 9B and 9C, where the documents are for reverse charge, SEZ supplies and exports of Form GSTR-1 are excluded from comparison of tax liability, other than export/ reverse charge report.

Q.10 Why are certain values in the tax liability other than export / reverse charge highlighted in red?

Ans: Those values for which the tax liability reported in Form GSTR-1 is more than the tax liability reported in Form GSTR-3B in a specific tax period, under the different tax heads, would be highlighted in red.

Tax Liability due to reverse charge

Q.11 From where can I view the tax liability due to reverse charge supplies report?

Ans: 1. Navigate to Services > Returns > Tax liabilities and ITC comparison > Select Financial Year and then click the SEARCH button.

2. On the Credit and Liability Statement page, click the + icon against the Tax liability due to reverse charge tab.

3. The Tax liability due to reverse charge report is displayed in a table.

Q.12 What is the purpose of tax liability due to reverse charge report?

Ans: The Tax liability due to reverse charge report displays the following details:

- Reverse charge liability declared in table 3.1 (d) of Form GSTR-3B during the month

- Amount auto-populated in Form GSTR-2A as per Part-A/ FORM GSTR-2B (B2B, B2BA, CDNR and CDNRA)

- Shortfall/Excess in liability as per Form GSTR-3B and as per Form GSTR 2A/GSTR-2B and cumulative shortfall/excess for the financial year

This report may be used as a reference to declare or compare liability due to reverse charge on inward supplies in Form GSTR-3B, with auto-drafted details as appearing in Form GSTR-2A/ GSTR-2B, reported by corresponding suppliers in their Form GSTR-1.

Q.13 How can I download my tax liability due to reverse charge report?

Ans: To download the Tax liability due to reverse charge report, click the DOWNLOAD (CSV) button provided on the right side of the Tax liability due to reverse charge tab. The report will get downloaded in a CSV format.

Q.14 How frequently is the tax liability due to reverse charge report generated?

Ans: The Tax liability due to reverse charge report is generated on near real time basis, for a particular tax period, on basis of Form GSTR-3B return filed by you and Form GSTR-2B generated. The report generation time is also displayed on the top white band of the Credit and Liability Statement page.

Q.15 Data from which tables of Form GSTR-3B and Form GSTR-2A/GSTR-2B are included for comparison in the tax liability due to reverse charge report?

Ans: The Tax liability due to reverse charge report includes data from following tables of Form GSTR-3B and Form GSTR-2A/ GSTR-2B.

- The Table 3.1(d) – Inward Supplies (liable to reverse charge) of Form GSTR-3B is considered for the comparison of liabilities.

- The following tables of Form GSTR-2A are considered for computing reverse charge liabilities:

- Table 3 – Inward supplies received from registered persons for supplies attracting reverse charge

- Table 4 – Amendment to inward supplies received from registered persons on which tax is to be paid on reverse charge

- Table 5 – Debit/ Credit notes received during the current tax period for supplies attracting reverse charge

- Table 6 – Amendments to Debit/ Credit notes for supplies attracting reverse charge.

- The following tables of Form GSTR-2B are considered for computing reverse charge liabilities:

- B2B – Invoices which are marked as reverse charge

- B2BA – Amendment to invoices which are amended and marked as reverse charge

- CDNR – Debit/ credit notes linked to invoices which are marked as reverse charge

- CDNRA – Amendment to Debit/ Credit notes linked to invoices which are marked as reverse charge

Tax Liability due to Export and SEZ supplies

Q.16 From where can I view the tax Liability due to export and SEZ supplies report?

Ans: 1. Navigate to Services > Returns > Tax liabilities and ITC comparison > Select Financial Year and then click the SEARCH button.

2. On the Credit and Liability Statement page tile, click the + icon against the Tax Liability due to export and SEZ supplies tab.

3. The Tax liability due to export and SEZ supplies report is displayed in a table.

Q.17 What is the purpose of tax Liability due to export and SEZ supplies report?

Ans: The Tax Liability due to export and SEZ supplies report displays the following:

- Liability as declared in table 3.1 (b) of Form GSTR-3B during the month

- Liability as declared in table 6A, 6B, 9A, 9B, 9C of Form GSTR-1 (Zero rated supplies) during the month

- Shortfall/ excess for the tax period and cumulative shortfall/ excess for the financial year

The table will help the taxpayer to have an overview of liabilities pertaining to zero rated supplies (Exports and SEZ supplies) declared in Form GSTR-3B and Form GSTR-1 and to see that liability is correctly declared. Corrective actions on liability declared on these forms/ return can be taken by the taxpayer in case of any discrepancy. This may also be used as a reference to declare liability in Form GSTR-3B, once Form GSTR-1 is filed for that tax period.

Q.18 How can I download my tax Liability due to export and SEZ supplies report?

Ans: To download Tax Liability due to export and SEZ supplies report, click the DOWNLOAD (CSV) button provided on the right side of the Tax Liability due to export and SEZ supplies tab. The report will get downloaded in a CSV format.

Q.19 How frequently is the tax Liability due to export and SEZ supplies report generated?

Ans: The Tax Liability due to export and SEZ supplies is generated on near real time basis for a particular tax period, on basis of Form GSTR-1 and Form GSTR-3B return filed by you. The report generation time is also displayed on the top white band of the Credit and Liability page.

20. Data from which tables of Form GSTR-1 and Form GSTR-3B are included for comparison in tax Liability due to export and SEZ supplies?

Ans: The Tax liability due to export and SEZ supplies report includes data from:

- The table 3.1(b) – Outward taxable supplies (zero rated) of GSTR-3B is considered for the comparison of liabilities.

- The following tables of Form GSTR-1 are considered for computing the liabilities:

- Table 6A – Exports

- Table 6B – Supplies made to SEZ unit or SEZ Developer

- Table 9 – Amendments to outward supply details furnished in returns for earlier tax periods in Table 6A, 6B [including debit notes, credit notes issued during current period and amendments thereof]

Q.21 Why are few values in the tax liability due to export and SEZ supplies highlighted in red?

Ans: For the tax periods for which the tax liability reported in GSTR-1 is more than the tax liability reported in GSTR-3B, then those specific values under the different tax heads are highlighted in red.

Input tax credit claimed and due (Other than import of goods)

Q.22 From where can I view the Input Tax Credit claimed and due (Other than import of goods) report?

Ans: 1. Navigate to Services > Returns > Tax liabilities and ITC comparison > Select Financial Year and then click the SEARCH button.

2. On the Credit and Liability Statement page tile, click the + icon against the Input Tax Credit claimed and due (Other than import of goods) tab.

3. The Input Tax Credit claimed and due (Other than import of goods) report is displayed in a table.

Q.23 What is the purpose of Input Tax Credit claimed and due (Other than import of goods) report?

Ans: The Input Tax Credit claimed and due (Other than import of goods) report displays the following:

- ITC claimed in table 4A (4) +4A (5) + 4D (1) + 4D (2) of Form GSTR-3B during the month

- ITC auto-populated in Part-A (as per GSTR-1) and Part-B (as per GSTR-6) of Form GSTR-2A or

- ITC auto-drafted in B2B, B2BA, CDNR, CDNRA, ISD and ISDA of Form GSTR-2B

- Shortfall/ excess for the tax period and cumulative shortfall/ excess for the financial year selected

This may be used as a reference to declare or compare ITC as claimed in Form GSTR-3B with auto-drafted details as appearing in Form GSTR-2A/GSTR-2B, reported by corresponding registered supplier in their Form GSTR-1 or by ISD in their Form GSTR-6. Corrective actions on credit claimed on these forms/ return can be taken by the taxpayer in case of any discrepancy.

Q.24 How can I download my Input Tax Credit claimed and due (Other than import of goods) report?

Ans: To download the Input Tax Credit claimed and due (Other than import of goods) report, click the DOWNLOAD (CSV) button provided on the right side of the Input Tax Credit claimed and due (Other than import of goods) tab. The report will get downloaded in a CSV format.

Q.25 How frequently is the Input Tax Credit claimed and due (Other than import of goods) report generated?

Ans: The Input Tax Credit claimed and due (Other than import of goods) is generated on near real time basis for a particular tax period, on basis of Form GSTR-3B filed by you and filing of Form GSTR-1 by your suppliers and generation of Form GSTR-2B. The report generation time is also displayed on the top white band of the Input Tax Credit claimed and due (Other than import of goods) page.

Q.26 Data from which tables of Form GSTR-2A/GSTR-2B and Form GSTR-3B are included for comparison in the Input Tax Credit claimed and due (Other than import of goods) report?

Ans: The Input tax credit claimed and due (Other than import of goods) report includes data from:

- The following tables of Form GSTR-3B are considered for computing the ITC claimed:

- Table 4(A)(4) – ITC available (whether in full or part) – Inward supplies from ISD

- Table 4(A)(5) – ITC available (whether in full or part) – All other ITC

- Table 4(D)(1) – Ineligible ITC as per Section 17(5)

- Table 4(D)(2) – Ineligible ITC (Others)

- The following tables from Form GSTR-2A are considered for computing ITC accrued:

- Table 3 – Inward supplies received from a registered person for supplies other than those attracting reverse charge

- Table 4 – Amendment to Inward supplies received from a registered person for supplies other than those attracting reverse charge

- Table 5 – Debit/ Credit notes received during the current tax period for supplies other than those attracting reverse charge

- Table 6 – Amendments to Debit/ Credit notes for supplies other than those attracting reverse charge.

- Table 7 – ISD credit received

- Table 8 – Amendments to ISD credit received

- The following tables of Form GSTR-2B are considered for computing ITC accrued:

- B2B – Invoices which are marked other than reverse charge

- B2BA – Amendment to invoices which are amended and marked other than reverse charge

- CDNR – Debit/ credit notes linked to invoices which are marked other than reverse charge

- CDNRA – Amendment to Debit/ Credit notes linked to invoices which are marked other than reverse charge

- ISD – ISD Invoices and credit notes received from ISD

- ISDA – Amendment to ISD invoices and credit notes received from ISD

Note: The details of reverse charge are not included from GSTR-2A/GSTR-2B

Q.27 Why are few values in the Input Tax credit claimed and due (Other than import of goods) highlighted in red?

Ans: For the tax periods for which the Input tax credit claimed in GSTR-3B is more than the Input tax credit due as per GSTR-2A/GSTR-2B, then those specific values under the different tax heads are highlighted in red.

Input tax credit claimed and due (Import of goods)

Q.28 From where I can view the input tax credit claimed and due (Import of goods) report?

Ans: 1. Navigate to Services > Returns > Tax liabilities and ITC comparison > Select Financial Year and then click the SEARCH button.

2. On the Credit and Liability Statement page tile, click the + icon against the Input tax credit claimed and due (Import of goods) tab.

3. The Input Tax Credit claimed and due (Import of goods) report is displayed in a table.

Q.29 What is the purpose of Input Tax Credit claimed and due (Import of goods) report?

Ans: The Input Tax Credit claimed and due (Import of goods) report contains the details of ITC claimed in GSTR-3B and accrued as per GSTR-2B under different tax heads i.e. Integrated tax (IGST), Central tax (CGST), State/Union Territory tax (SGST/UTGST) and Cess (Cess).

The following tables are considered for the ITC claimed on import of goods:

- The table 4(A)(1) of Form GSTR-3B is considered for the ITC claimed on import of goods.

- The following tables of Form GSTR-2B are considered for computing ITC accrued:

- IMPG – Bill of entry details received from ICEGATE

- IMPGSEZ – Bill of entry details received from ICEGATE on inward supplies from SEZ units/Developers

Q.30 How can I download my Input Tax Credit claimed and due (Import of goods) report?

Ans: To download the Input Tax Credit claimed and due (Import of goods) report, click the DOWNLOAD (CSV) button provided on the right side of the Input Tax Credit claimed and due (Import of goods) tab. The report will get downloaded in a CSV format.

Q.31 How frequently is the Input Tax Credit claimed and due (Import of goods) report generated?

Ans: The Input Tax Credit claimed and due (Import of goods) is generated on near real time basis for a particular tax period, on basis of Form GSTR-2B and filing of Form GSTR-3B. The report generation time is also displayed on the top white band of the Input Tax Credit claimed and due (Import of goods) page.

Q.32 Why are few values in the Input Tax credit claimed and due (Import of goods) highlighted in red?

Ans: For the tax periods for which the input tax credit claimed in GSTR-3B is more than the input tax credit due as per GSTR-2B, then those specific values under the different tax heads are highlighted in red.

Q.33 From which tax periods, the details from GSTR-2A and from which tax periods details from GSTR-2B are considered?

Ans:

- In the reports no. 2 & 4 the details are computed from GSTR-2A from the tax periods July 2017 till June 2020

- From July 2020, the details in reports no. 2 & 4 are computed from GSTR-2B and not from GSTR-2A

- Report 5 is applicable only from the return period from which GSTR-2B is implemented and will not be available for FY 2017-18, 2018-19 and 2019-20

Note: The details of GSTR-2A will become static and will not change as GSTR-2B is implemented from July 2020.

B. Manual on Comparison of Liability Declared and ITC Claimed

How can I compare liability declared in Form GSTR-3B and Form GSTR-1 with ITC claimed in Form GSTR-3B and as accrued in Form GSTR-2A?

To compare liability declared in Form GSTR-3B and Form GSTR-1 and ITC claimed in Form GSTR-3B and as accrued in Form GSTR-2A, GST Portal provides the following comparison Reports:

- Liability (other than zero rated (Export and SEZ Supplies) and reverse charge supply

- Liability due to receipt of reverse charge supplies

- Liability (Export and supplies to SEZ)

- ITC Credit Claimed and Due

To access the Comparison Reports, perform following steps:

1. Access the www.gst.gov.in URL. The GST Home page is displayed.

2. Login to the GST Portal with valid credentials.

3. Click the Services > Returns > Returns Dashboard command.

Alternatively, you can also click the Returns Dashboard link on the Dashboard.

4. The File Returns page is displayed. Select the Financial Year & Return Filing Period from the drop-down list.

5. Click the SEARCH button.

6. The File Returns page is displayed. In the “Comparison of liability declared and ITC claimed” tile, click the VIEW button.

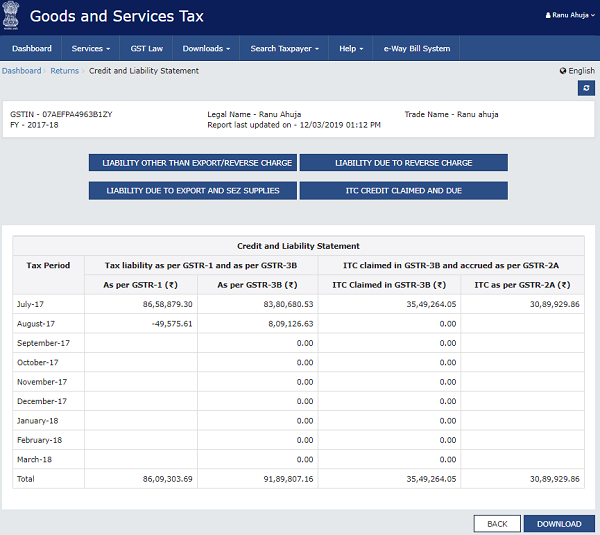

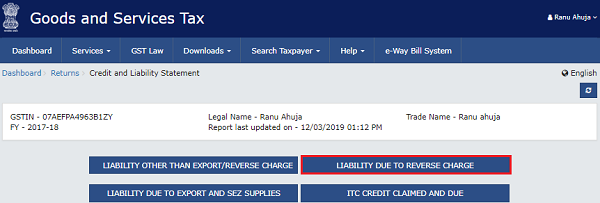

7. The Credit and Liability Statement page is displayed, with the following information:

- The White band on the top displays your GSTIN, Legal/Trade Name, Financial Year Period and the Date & Time when the Report was last updated.

- Below the while band, buttons are provided that you can click to access each of the following Comparison Reports: Liability (other than zero rated (Export and SEZ Supplies) and reverse charge supply), Liability due to receipt of reverse charge supplies, Liability due to Export and supplies to SEZ and ITC Credit Claimed and Due

- Below the buttons, Credit and Liability Statement Table is provided that shows the tax liability as declared in Form GSTR-3B and Form GSTR-1, tax period wise, based on returns filed by you and the ITC as claimed in Form GSTR-3B filed by you and as accrued to you in Form GSTR-2A, based on returns filed by your supplier.

- Click the DOWNLOAD button to the download the Credit and Liability Statement in Excel format.

- To go to the previous page, click BACK.

8.1. Liability other than Export/Reverse Charge

8.2. Liability due to Reverse Charge

8.3. Liability due to Export and SEZ Supplies

8.4. ITC Credit Claimed and Due

8.1. Liability other than Export/Reverse Charge

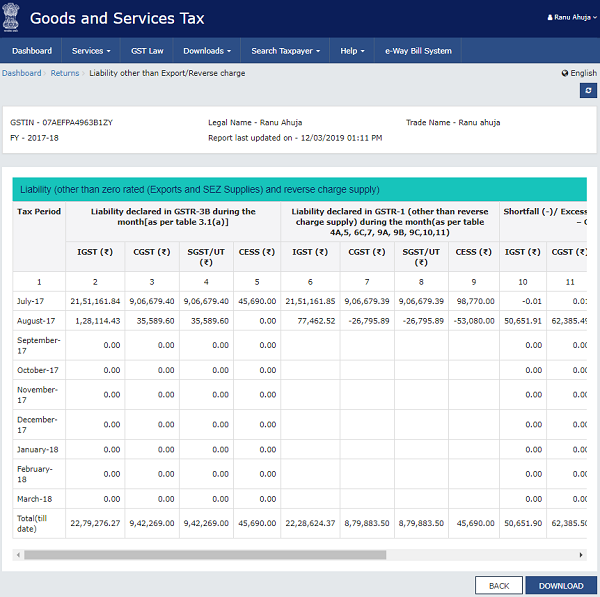

8.1.1. Click the LIABILITY OTHER THAN EXPORT/REVERSE CHARGE button.

8.1.2. The Liability other than Export/Reverse Charge page is displayed, containing the following details:

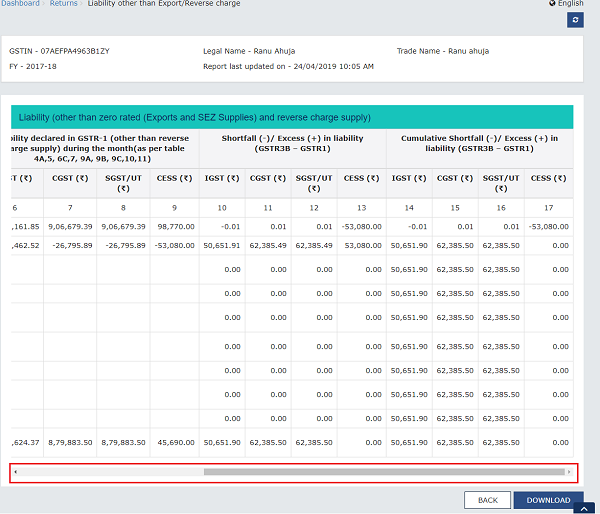

- Liability as declared in table 3.1 (a) of Form GSTR-3B during the month

- Liability as declared in table 4a, 5, 6C, 7, 9A, 9B, 9C, 10, 11 of Form GSTR-1 (other than reverse charge supply) during the month

- Shortfall/excess for the tax period and cumulative shortfall/excess for the financial year

Note:

- The comparison is generated tax-period wise for the selected financial year up to the current date. The report of previous tax periods of the financial year is also shown in the report.

- This comparative table will help the taxpayer to have the overview of liabilities (other than zero rated & reverse charge) declared in Form GSTR-3B and Form GSTR-1 and to see that liability is correctly declared and liquidated. Corrective actions on liability declared on these forms/ return can be taken by taxpayer in case any discrepancy is noticed. This may also be used as a reference to declare liability in Form GSTR-3B, once Form GSTR-1 is filed for such tax period.

8.1.2. Scroll to the right to view the complete report.

8.1.3. Click DOWNLOAD button to the download the details in Excel format. To go to the previous page, click BACK.

8.2. Liability due to Reverse Charge

8.2.1. Click the LIABILITY DUE TO REVERSE CHARGE button.

8.2.2. The Liability due to Reverse Charge page is displayed, containing the following details:

- Reverse charge liability declared in table 3.1 (d) of Form GSTR-3B during the month, as filled by you.

- Auto-populated amount, as available in Part-A of Form GSTR-2A (as uploaded by supplier)

- Shortfall/Excess in liability as per Form GSTR-3B-Form GSTR 2A

Note: This report may be used as a reference to declare or compare liability due to reverse charge on inward supplies in Form GSTR-3B with auto-drafted details as appearing in Form GSTR-2A, reported by corresponding registered suppliers in their Form GSTR-1.

8.2.2. Scroll to the right to view the complete report.

8.2.3. Click DOWNLOAD button to the download the details in Excel format. To go to the previous page, click BACK.

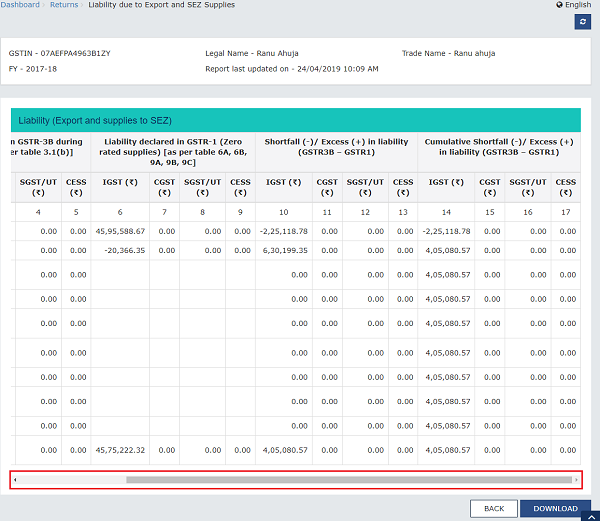

8.3. Liability due to Export and SEZ Supplies

8.3.1. Click the LIABILITY DUE TO EXPORT AND SEZ SUPPLIES button.

8.3.2. The Liability due to Export and SEZ Supplies page is displayed, containing the following details:

- Liability as declared in table 3.1 (b) of Form GSTR-3B during the month

- Liability as declared in table 6A, 6B, 9A, 9B, 9C of Form GSTR-1 (Zero rated supplies) during the month

- Shortfall/excess for the tax period and cumulative shortfall/excess for the financial year

Note: This comparative table will help the taxpayer to have the overview of liabilities pertaining to zero rated supplies declared in Form GSTR-3B and Form GSTR-1 and to see that liability is correctly declared and liquidated. Corrective actions on liability declared on these forms/ return can be taken by taxpayer in case any discrepancy is noticed. This may also be used as a reference to declare liability in Form GSTR-3B, once Form GSTR-1 is filed for such tax period.

8.3.2. Scroll to the right to view the complete report.

8.3.3. Click DOWNLOAD button to the download the details in Excel format. To go to the previous page, click BACK.

8.4. ITC Credit Claimed and Due

8.4.1. Click the ITC CREDIT CLAIMED AND DUE button.

8.4.2. The ITC Credit Claimed and Due page is displayed, containing the following details:

- ITC claimed in table 4A(3)+4A(4)+4A(5)+4D(1)+4D(2)-4B(1)-4B(2) of Form GSTR-3B during the month

- ITC auto-populated in Part-A (as per GSTR-1) and Part-B (as per GSTR-6) of Form GSTR-2A

- Shortfall/excess for the tax period and cumulative shortfall/excess for the financial year

Note: This may be used as a reference to declare or compare ITC as claimed in Form GSTR-3B with auto-drafted details as appearing in Form GSTR-2A, reported by corresponding registered supplier in their Form GSTR 1 or by ISD distributors in their Form GSTR 6. Corrective actions on credit claimed on these forms/ return can be taken by taxpayer in case any discrepancy is noticed.

8.4.2. Scroll to the right to view the complete report.

8.4.3. Click DOWNLOAD button to the download the details in Excel format. To go to the previous page, click BACK.

(Republished with amendments)

****

Disclaimer: The contents of this article are for information purposes only and does not constitute an advice or a legal opinion and are personal views of the author. It is based upon relevant law and/or facts available at that point of time and prepared with due accuracy & reliability. Readers are requested to check and refer relevant provisions of statute, latest judicial pronouncements, circulars, clarifications etc before acting on the basis of the above write up. The possibility of other views on the subject matter cannot be ruled out. By the use of the said information, you agree that Author / TaxGuru is not responsible or liable in any manner for the authenticity, accuracy, completeness, errors or any kind of omissions in this piece of information for any action taken thereof. This is not any kind of advertisement or solicitation of work by a professional.

i have checked that all my purchase bill are in gstr 2A not a single purchase bill is missing or not uploaded by my parties from whome i made purchase but still there is a mismatch ,please help

ITC AVAILABLE IN GSTR 2A & ALSO AVAILABLE ITC IN GSTR 2B SUPPLIER FILLED GSTR 1FOR THE MONTH OF AUGUST 2020 BUT ITC NOT SHOWN TAX LIABILITIES & ITC COMPARISON . GSTR 3B NOT FILLED FOR AUGUST 2020 DUE TO ITC NOT SHOWN IN TAX LIABILITIES & ITC COMPARISON . PLEASE SOLVE THE MATTER.

Data from 3.1 table reverse charge is taken in itc claimed amount but not in itc available 2a. This is creating mismatch every month. How to resolve

is it possible to edit 3-B TURNOVER IN GSTR-9

SINCE THERE IS A DIFF.BETWEEB GSTR1

AND GSTR-3B PLEASE CLARIFY