Introduction: The recent advisory on GSTR-1/IFF introduces two new tables, 14A and 15A, aimed at capturing amendments related to supplies made through e-commerce operators. This article delves into the implications of these additions for taxpayers and e-commerce operators.

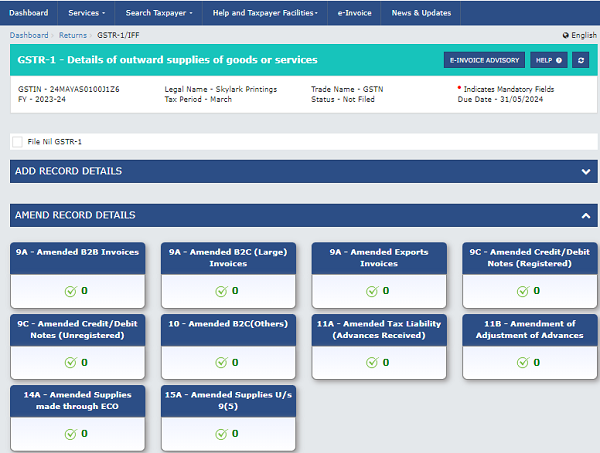

Detailed Analysis: Table 14A allows suppliers to amend details of original supplies reported in Table 14, pertaining to transactions where e-commerce operators are liable to collect tax under section 52 or liable to pay tax under section 9(5) of the CGST Act, 2017. Similarly, Table 15A enables e-commerce operators to amend details of original supplies reported in Table 15, categorized based on the type of supplier and recipient.

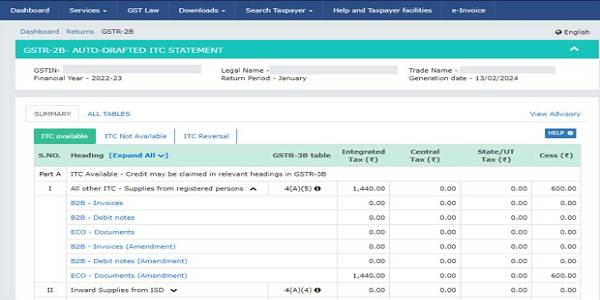

The introduction of these tables necessitates a thorough understanding of their implications. Amendments made in Table 14A will auto-populate taxable values in GSTR-3B, ensuring seamless compliance. Additionally, amendments in Table 15A impact tax liabilities across various supply categories, with values auto-populated in GSTR-3B accordingly.

E-commerce operators are advised to manually add e-invoice records related to section 9(5) supplies in Table 15A, as there is no auto-population functionality. Furthermore, the reporting of debit or credit notes related to section 9(5) services is mandated in Table 9C of GSTR-1/IFF.

The impact of these amendments extends to GSTR-2B, where a new table, “ECO – Documents (Amendment),” is introduced. Registered recipients can now view amended document details of supplies made through e-commerce operators liable to pay tax under section 9(5) in this table. Values are auto-populated from Table 15A, streamlining the reconciliation process for recipients.

Conclusion: The introduction of Tables 14A and 15A in GSTR-1/IFF represents a significant regulatory update aimed at enhancing transparency and compliance in e-commerce transactions. Taxpayers and e-commerce operators must familiarize themselves with these amendments to ensure seamless reporting and compliance. Additionally, the impact of these changes on GSTR-3B and GSTR-2B underscores the need for proactive adaptation to evolving GST regulations. By staying informed and implementing necessary measures, stakeholders can navigate these changes effectively and contribute to a more robust GST ecosystem.

****

GSTN

Goods and Services Tax

12th March 2024

It is informed to all taxpayers that as per Notification No. 26/2022 – Central Tax dated 26th December 2022 two new Table 14A and Table 15A have been introduced in GSTR-1 to capture the amendment details of the supplies made through e-commerce operators (ECO) on which e-commerce operators are liable to collect tax under section 52 or liable to pay tax u/s 9(5) of the CGST Act, 2017. These tables have now been made live on the GST common portal and will be available in GSTR-1/IFF from February 2024 tax period onwards. These amendment tables are relevant for those taxpayers who have reported the supplies in Table 14 or Table 15 in earlier tax periods. Please click here to view the complete advisory on the captioned subject.

Thank You,

Team GSTN

Advisory on GSTR-1/IFF: Introduction of New 14A and 15A tables

It is informed to all taxpayers that as per Notification No. 26/2022 – Central Tax dated 26th December 2022 two new Table 14A and Table 15A have been introduced in GSTR-1 to capture the amendment details of the supplies made through e-commerce operators (ECO) on which e-commerce operators are liable to collect tax under section 52 or liable to pay tax u/s 9(5) of the CGST Act, 2017. These tables have now been made live on the GST common portal and will be available in GSTR-1/IFF from February 2024 tax period onwards. These amendment tables are relevant for those taxpayers who have reported the supplies in Table 14 or Table 15 in earlier tax periods.

Table 14A – Amended Supplies made through e-commerce operator (ECO) in GSTR-1

In this table, the supplier can amend the detail of original supplies that he has already reported in original table 14 under below two sections in earlier return periods.

1. 14(a) Liable to collect tax u/s 52(TCS)

2. 14(b) Liable to pay tax u/s 9(5)

Table 15A – Amended Supplies u/s 9(5) in GSTR-1/IFF

In this table, the e-commerce operator can amend the detail of original supplies that he has already reported in table 15 originally under following four sections in earlier return periods.

1. Registered Supplier and Registered Recipient (B2B)

2. Registered Supplier and Unregistered Recipient (B2C)

3. Unregistered Supplier and Registered Recipient (URP2B)

4. Unregistered Supplier and Unregistered Recipient (URP2C)

To view the table 14A/15A, taxpayer can navigate to Returns Dashboard > Selection of Period > Details of outward supplies of goods or services GSTR-1 > Prepare Online

Other Salient features: –

1. Amended taxable values will be auto-populated from table 14A(b) to Table 3.1.1(ii) of GSTR-3B.

2. Amended taxable value along with tax liabilities from all the four sections of table 15A i.e., B2B, B2C, URP2B and URP2C will be auto-populated to table 3.1.1(i) of GSTR-3B.

3. There will be no auto-population of e-invoice in Table -15A. E-invoices reported for 9(5) supplies will be populated in FORM GSTR-1 as per existing functionality. E-commerce operators are advised to examine and add such records in table 15A related to 9(5) supplies.

4. E-commerce operator shall report amendment of debit or credit notes related to such services notified u/s 9(5) in existing table 9C of GSTR-1/IFF.

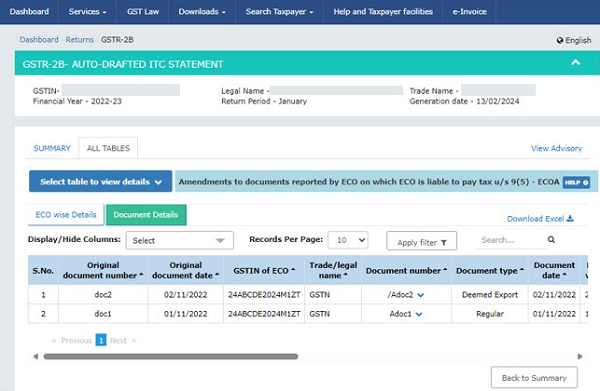

Impact of new tables of ECO-Documents in GSTR-2B

For the ease of registered recipient who are making supplies through e-commerce operator, a new table “ECO – Documents (Amendment)” is being added in GSTR-2B. In this table, the registered recipient can view the amended document details of the supplies made through e-commerce operator on which e-commerce operator is liable to pay tax under section 9(5) of the Act.

The values will be auto populated from Registered Supplier and Registered Recipient (B2B) and Unregistered Supplier and Registered Recipient (URP2B) section of table 15A to this new ECO – Documents table of GSTR-2B.

To view the ECO-Documents (Amendment) table, taxpayer can navigate to Returns Dashboard > Selection of Period > Auto- drafted ITC Statement for the month GSTR 2B > View.

To view the records in ECO-Documents (Amendment) table, taxpayer can navigate to Returns Dashboard > Selection of Period > Auto- drafted ITC Statement for the month GSTR 2B > View > ECO Documents (Amendment)