ECONOMIC SURVEY 2022-23: HIGHLIGHTS

Indian economy staging a broad based recovery across sectors, positioning to ascend to

pre-pandemic growth path in FY23

Retail inflation is back within RBI’s target range in November 2022

Direct Tax collections for the period April-November 2022 remains buoyant

Enhanced Employment generation seen in the declining urban unemployment rate and in the faster net registration in Employee Provident Fund

Creating public goods to enhance opportunities, efficiencies and ease of living, trust-based governance, enhancing agricultural productivity and promoting the private sector as a co-partner in development is the focus of the government reforms

Cleaner balance sheets led to enhanced lending by financial institutions

Growth in credit offtake, increased private capex to usher virtuous investment cycle

Non-food credit offtake by Scheduled Commercial Banks growing in double digits since April 2022

Gross Non-Performing Assets (GNPA) ratio of SCBs has fallen to a seven-year low of 5.0

Social sector expenditure (Centre and States combined) increases to Rs. 21.3 lakh crore in FY23 (BE) from Rs. 9.1 lakh crore in FY16

Central and State Government’s budgeted expenditure on health sector touched 2.1% of GDP in FY23 (BE) and 2.2% in FY22 (RE) against 1.6% in FY21

More than 220 crore COVID vaccine doses administered

Survey highlights the findings of the 2022 report of the UNDP on Multidimensional Poverty Index which says that 41.5 crore people exit poverty in India between 2005-06 and 2019-20

India declared Net Zero Pledge, to achieve net zero emissions goal by 2070

A mass movement LIFE– Life style for Environment launched

National Green Hydrogen Mission to enable India to be energy independent by 2047

Private investment in agriculture increases to 9.3% in 2020-21

Free foodgrains to about 81.4 crore beneficiaries under the National Food Security Act for one year

About 11.3 crore farmers were covered under PM KISAN in its April-July 2022-23 payment cycle

India stands at the forefront to promote millets through the International Year of Millets initiative

Investment of ₹47,500 crores under the PLI schemes in FY22- 106% of the designated target for the year

India’s e-commerce market is projected to grow at 18 per cent annually through 2025

Merchandise exports of US$ 332.8 billion for April-December 2022

India is the largest recipient of remittances globally receiving US$ 100 billion in 2022

PM GatiShakti National Master Plan creates comprehensive database for integrated planning and synchronised implementation across Ministries/ Departments

UPI-based transactions grew in value (121 per cent) and volume (115 per cent) terms, between 2019-2022, paving the way for its international adoption

Posted On: 31 JAN 2023 1:59PM by PIB Delhi

Union Minister for Finance and Corporate Affairs, Smt. Nirmala Sitharaman, presented the Economic Survey 2022-23 in the Union Parliament today. The highlights of the Survey are as follows:

State of the Economy 2022-23: Recovery Complete

- Recovering from pandemic-induced contraction, Russian-Ukraine conflict and inflation, Indian economy is staging a broad based recovery across sectors, positioning to ascend to the pre-pandemic growth path in FY23.

- India’s GDP growth is expected to remain robust in FY24. GDP forecast for FY24 to be in the range of 6-6.8 %.

- Private consumption in H1 is highest since FY15 and this has led to a boost to production activity resulting in enhanced capacity utilisation across sectors.

- The Capital Expenditure of Central Government and crowding in the private Capex led by strengthening of the balance sheets of the Corporates is one of the growth driver of the Indian economy in the current year.

- The credit growth to the MSME sector was over 30.6 per cent on average during Jan-Nov 2022.

- Retail inflation is back within RBI’s target range in November 2022.

- Indian Rupee performed well compared to other Emerging Market Economies in Apr-Dec2022.

- Direct Tax collections for the period April-November 2022 remain buoyant.

- Enhanced Employment generation seen in the declining urban unemployment rate and in the faster net registration in Employee Provident Fund.

- Economic growth to be boosted from the expansion of public digital platforms and measures to boost manufacturing output.

India’s Medium Term Growth Outlook: with Optimism and Hope

- Indian economy underwent wide-ranging structural and governance reforms that strengthened the economy’s fundamentals by enhancing its overall efficiency during 2014-2022.

- With an underlying emphasis on improving the ease of living and doing business, the reforms after 2014 were based on the broad principles of creating public goods, adopting trust-based governance, co-partnering with the private sector for development, and improving agricultural productivity.

- The period of 2014-2022 also witnessed balance sheet stress caused by the credit boom in the previous years and one-off global shocks, that adversely impacted the key macroeconomic variables such as credit growth, capital formation, and hence economic growth during this period.

- This situation is analogous to the period 1998-2002 when transformative reforms undertaken by the government had lagged growth returns due to temporary shocks in the economy. Once these shocks faded, the structural reforms paid growth dividends from 2003.

- Similarly, the Indian economy is well placed to grow faster in the coming decade once the global shocks of the pandemic and the spike in commodity prices in 2022 fade away.

- With improved and healthier balance sheets of the banking, non-banking and corporate sectors, a fresh credit cycle has already begun, evident from the double-digit growth in bank credit over the past months.

- Indian economy has also started benefiting from the efficiency gains resulting from greater formalisation, higher financial inclusion, and economic opportunities created by digital technology-based economic reforms.

- Thus Chapter 2 of the Survey shows that India’s growth outlook seems better than in the pre-pandemic years, and the Indian economy is prepared to grow at its potential in the medium term.

Fiscal Developments: Revenue Relish

- The Union Government finances have shown a resilient performance during the year FY23, facilitated by the recovery in economic activity, buoyancy in revenues from direct taxes and GST, and realistic assumptions in the Budget.

- The Gross Tax Revenue registered a YoY growth of 15.5 per cent from April to November 2022, driven by robust growth in the direct taxes and Goods and Services Tax (GST).

- Growth in direct taxes during the first eight months of the year was much higher than their corresponding longer-term averages.

- GST has stabilised as a vital revenue source for central and state governments, with the gross GST collections increasing at 24.8 per cent on YoY basis from April to December 2022.

- Union Government’s emphasis on capital expenditure (Capex) has continued despite higher revenue expenditure requirements during the year. The Centre’s Capex has steadily increased from a long-term average of 1.7 per cent of GDP (FY09 to FY20) to 2.5 per cent of GDP in FY22 PA.

- The Centre has also incentivised the State Governments through interest-free loans and enhanced borrowing ceilings to prioritise their spending on Capex.

- With an emphasis on infrastructure-intensive sectors like roads and highways, railways, and housing and urban affairs, the increase in Capex has large-scale positive implications for medium-term growth.

- The Government’s Capex-led growth strategy will enable India to keep the growth-interest rate differential positive, leading to a sustainable debt to GDP in the medium run.

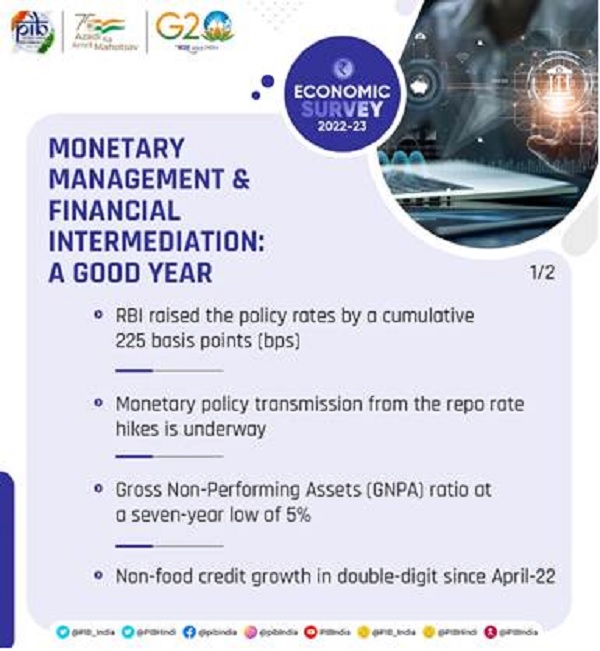

Monetary Management and Financial Intermediation: A Good Year

- The RBI initiated its monetary tightening cycle in April 2022 and has since raised the repo rate by 225 bps, leading to moderation of surplus liquidity conditions.

- Cleaner balance sheets led to enhanced lending by financial institutions.

- The growth in credit offtake is expected to sustain, and combined with a pick-up in private capex, will usher in a virtuous investment cycle.

- Non-food credit offtake by scheduled Commercial Banks (SCBs) has been growing in double digits since April 2022.

- Credit disbursed by Non-Banking Financial Companies (NBFCs) has also been on the rise.

- The Gross Non-Performing Assets (GNPA) ratio of SCBs has fallen to a seven-year low of 5.0.

- The Capital-to-Risk Weighted Assets Ratio (CRAR) remains healthy at 16.0.

- The recovery rate for the SCBs through Insolvency and Bankruptcy (IBC) was highest in FY22 compared to other channels.

Prices and Inflation: Successful Tight-Rope Walking

- While the year 2022 witnessed a return of high inflation in the advanced world after three to four decades, India caps the rise in prices.

- While India’s retail inflation rate peaked at 7.8 per cent in April 2022, above the RBI’s upper tolerance limit of 6 per cent, the overshoot of inflation above the upper end of the target range in India was however one of the lowest in the world.

- The government adopted a multi-pronged approach to tame the increase in price levels

- Phase wise reduction in export duty of petrol and diesel

- Import duty on major inputs were brought to zero while tax on export of iron ores and concentrates increased from 30 to 50 per cent

- Waived customs duty on cotton imports w.e.f 14 April 2022, until 30 September 2022

- Prohibition on the export of wheat products under HS Code 1101 and imposition of export duty on rice

- Reduction in basic duty on crude and refined palm oil, crude soyabean oil and crude sunflower oil

- The RBI’s anchoring of inflationary expectations through forward guidance and responsive monetary policy has helped guide the trajectory of inflation in the country.

- The one-year-ahead inflationary expectations by both businesses and households have moderated in the current financial year.

- Timely policy intervention by the government in housing sector, coupled with low home loan interest rates propped up demand and attracted buyers more readily in the affordable segment in FY23.

- An overall increase in composite Housing Price Indices (HPI) assessment and Housing Price Indices market prices indicates a revival in the housing finance sector. A stable to moderate increase in HPI also offers confidence to homeowners and home loan financiers in terms of the retained value of the asset.

- India’s inflation management has been particularly noteworthy and can be contrasted with advanced economies that are still grappling with sticky inflation rates.

Social Infrastructure and Employment: Big Tent

- Social Sector witnessed significant increase in government spending.

- Central and State Government’s budgeted expenditure on health sector touched 2.1% of GDP in FY23 (BE) and 2.2% in FY22 (RE) against 1.6% in FY21.

- Social sector expenditure increases to Rs. 21.3 lakh crore in FY23 (BE) from Rs. 9.1 lakh crore in FY16.

- Survey highlights the findings of the 2022 report of the UNDP on Multidimensional Poverty Index which says that 41.5 crore people exit poverty in India between 2005-06 and 2019-20.

- The Aspirational Districts Programme has emerged as a template for good governance, especially in remote and difficult areas.

- eShram portal developed for creating a National database of unorganised workers, which is verified with Aadhaar. As on 31 December 2022, a total of over 28.5 crore unorganised workers have been registered on eShram portal.

- JAM (Jan-Dhan, Aadhaar, and Mobile) trinity, combined with the power of DBT, has brought the marginalised sections of society into the formal financial system, revolutionising the path of transparent and accountable governance by empowering the people.

- Aadhaar played a vital role in developing the Co-WIN platform and in the transparent administration of over 2 billion vaccine doses.

- Labour markets have recovered beyond pre-Covid levels, in both urban and rural areas, with unemployment rates falling from 5.8 per cent in 2018-19 to 4.2 per cent in 2020-21.

- The year FY22 saw improvement in Gross Enrolment Ratios (GER) in schools and improvement in gender parity. GER in the primary-enrolment in class I to V as a percentage of the population in age 6 to 10 years – for girls as well as boys have improved in FY22.

- Due to several steps taken by the government on health, out-of-pocket expenditure as a percentage of total health expenditure declined from 64.2% in FY14 to 48.2% in FY19.

- Infant Mortality Rate (IMR), Under Five mortality rate (U5MR) and neonatal Mortality Rate (NMR) have shown a steady decline.

- More than 220 crore COVID vaccine doses administered as on 06 January, 2023.

- Nearly 22 crore beneficiaries have been verified under the Ayushman Bharat Scheme as on 04 January, 2023. Over 1.54 lakh Health and Wellness Centres have been operationalized across the country under Ayushman Bharat.

Climate Change and Environment: Preparing to Face the Future

- India declared the Net Zero Pledge to achieve net zero emissions goal by 2070.

- India achieved its target of 40 per cent installed electric capacity from non-fossil fuels ahead of 2030.

- The likely installed capacity from non-fossil fuels to be more than 500 GW by 2030 resulting in decline of average emission rate by around 29% by 2029-30, compared to 2014-15.

- India to reduce emissions intensity of its GDP by 45% by 2030 from 2005 levels.

- About 50% cumulative electric power installed capacity to come from non-fossil fuel-based energy resources by 2030.

- A mass movement LIFE– Life style for Environment launched.

- Sovereign Green Bond Framework (SGrBs) issued in November 2022.

- RBI auctions two tranches of ₹4,000 crore Sovereign Green Bonds (SGrB).

- National Green Hydrogen Mission to enable India to be energy independent by 2047.

- Green hydrogen production capacity of at least 5 MMT (Million Metric Tonne) per annum to be developed by 2030. Cumulative reduction in fossil fuel imports over ₹1 lakh crore and creation of over 6 lakh jobs by 2030 under the National green Hydrogen Mission. Renewable energy capacity addition of about 125 GW and abatement of nearly 50 MMT of annual GHG emissions by 2030.

- The Survey highlights the progress on eight missions under the NAP on CC to address climate concerns and promote sustainable development.

- Solar power capacity installed, a key metric under the National Solar Mission stood at 61.6 GW as on October 2022.

- India becoming a favored destination for renewables; investments in 7 years stand at USD 78.1 billion.

- 62.8 lakh individual household toilets and 6.2 lakh community and public toilets constructed (August 2022) under the National Mission on Sustainable Habitat.

Agriculture and Food Management

- The performance of the agriculture and allied sector has been buoyant over the past several years, much of which is on account of the measures taken by the government to augment crop and livestock productivity, ensure certainty of returns to the farmers through price support, promote crop diversification, improve market infrastructure through the impetus provided for the setting up of farmer-producer organisations and promotion of investment in infrastructure facilities through the Agriculture Infrastructure Fund.

- Private investment in agriculture increases to 9.3% in 2020-21.

- MSP for all mandated crops fixed at 1.5 times of all India weighted average cost of production since 2018.

- Institutional Credit to the Agricultural Sector continued to grow to 18.6 lakh crore in 2021-22

- Foodgrains production in India saw sustained increase and stood at 315.7 million tonnes in 2021-22.

- Free foodgrains to about 81.4 crore beneficiaries under the National Food Security Act for one year from January 1, 2023.

- About 11.3 crore farmers were covered under the Scheme in its April-July 2022-23 payment cycle.

- Rs 13,681 crores sanctioned for Post-Harvest Support and Community Farms under the Agriculture Infrastructure Fund.

- Online, Competitive, Transparent Bidding System with 1.74 crore farmers and 2.39 lakh traders put in place under the National Agriculture Market (e-NAM) Scheme.

- Organic Farming being promoted through Farmer Producer Organisations (FPO) under the Paramparagat Krishi Vikas Yojana (PKVY).

- India stands at the forefront to promote millets through the International Year of Millets initiative.

Industry: Steady Recovery

- Overall Gross Value Added (GVA) by the Industrial Sector (for the first half of FY 22-23) rose 3.7 per cent, which is higher than the average growth of 2.8 per cent achieved in the first half of the last decade.

- Robust growth in Private Final Consumption Expenditure, export stimulus during the first half of the year, increase in investment demand triggered by enhanced public capex and strengthened bank and corporate balance sheets have provided a demand stimulus to industrial growth.

- The supply response of the industry to the demand stimulus has been robust.

- PMI manufacturing has remained in the expansion zone for 18 months since July 2021, and Index of Industrial Production (IIP) grows at a healthy pace.

- Credit to Micro, Small and Medium Enterprises (MSMEs) has grown by an average of around 30% since January 2022 and credit to large industry has been showing double-digit growth since October 2022.

- Electronics exports rise nearly threefold, from US $4.4 billion in FY19 to US $11.6 Billion in FY22.

- India has become the second-largest mobile phone manufacturer globally, with the production of handsets going up from 6 crore units in FY15 to 29 crore units in FY21.

- Foreign Direct Investment (FDI) flows into the Pharma Industry has risen four times, from US $180 million in FY19 to US $699 million in FY22.

- The Production Linked Incentive (PLI) schemes introduced across 14 categories, with an estimated capex of ₹4 lakh crore over the next five years, to plug India into global supply chains. Investment of ₹47,500 crores has been seen under the PLI schemes in the FY22, which is 106% of the designated target for the year. Production/sales worth ₹3.85 lakh crore and employment generation of 3.0 lakh have been recorded due to PLI schemes.

- Over 39,000 compliances have been reduced and more than 3500 provisions decriminalized as of January 2023.

Services: Source of Strength

- The services sector is expected to grow at 9.1% in FY23, as against 8.4% (YoY) in FY22.

- Robust expansion in PMI services, indicative of service sector activity, observed since July 2022.

- India was among the top ten services exporting countries in 2021, with its share in world commercial services exports increasing from 3 per cent in 2015 to 4 per cent in 2021.

- India’s services exports remained resilient during the Covid-19 pandemic and amid geopolitical uncertainties driven by higher demand for digital support, cloud services, and infrastructure modernization.

- Credit to services sector has grown by over 16% since July 2022.

- US$ 7.1 billion FDI equity inflows in services sector in FY22.

- Contact-intensive services are set to reclaim pre-pandemic level growth rates in FY23.

- Sustained growth in the real estate sector is taking housing sales to pre-pandemic levels, with a 50% rise between 2021 and 2022.

- Hotel occupancy rate has improved from 30-32% in April 2021 to 68-70% in November 2022.

- Tourism sector is showing signs of revival, with foreign tourist arrivals in India in FY23 growing month-on-month with resumption of scheduled international flights and easing of Covid-19 regulations.

- Digital platforms are transforming India’s financial services.

- India’s e-commerce market is projected to grow at 18 per cent annually through 2025.

External Sector

- Merchandise exports were US$ 332.8 billion for April-December 2022.

- India diversified its markets and increased its exports to Brazil, South Africa and Saudi Arabia.

- To increase its market size and ensure better penetration, in 2022, CEPA with UAE and ECTA with Australia come into force.

- India is the largest recipient of remittances in the world receiving US$ 100 bn in 2022. Remittances are the second largest major source of external financing after service export

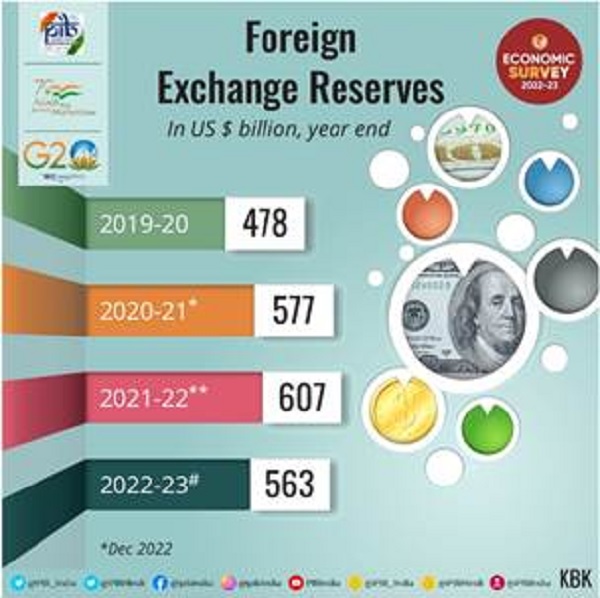

- As of December 2022, Forex Reserves stood at US$ 563 bn covering 9.3 months of imports.

- As of end-November 2022, India is the sixth largest foreign exchange reserves holder in the world.

- The current stock of external debt is well shielded by the comfortable level of foreign exchange reserves.

- India has relatively low levels of total debt as a percentage of Gross National Income and short-term debt as a percentage of total debt.

Physical and Digital Infrastructure

Government’s Vision for Infrastructure Development

- Public Private Partnerships

- In-Principal Approval granted to 56 projects with Total Project Cost of ₹57,870.1 crore under the VGF Scheme, from 2014-15 to 2022-23.

- IIPDF Scheme with ₹150 crore outlay from FY 23-25 was notified by the government on 03 November, 2022.

- National Infrastructure Pipeline

- 89,151 projects costing ₹141.4 lakh crore under different stages of implementation

- 1009 projects worth ₹5.5 lakh crore completed

- NIP and Project Monitoring Group (PMG) portal linkage to fast-track approvals/ clearances for projects

- National Monetisation Pipeline

- ₹ 9.0 lakh crore is the estimated cumulative investment potential.

- ₹ 0.9 lakh crore monetisation target achieved against expected ₹0.8 lakh crore in FY22.

- FY23 target is envisaged to be ₹1.6 lakh crore (27 per cent of overall NMP Target)

- GatiShakti

- PM GatiShakti National Master Plan creates comprehensive database for integrated planning and synchronised implementation across Ministries/ Departments.

- Aims to improve multimodal connectivity and logistics efficiency while addressing the critical gaps for the seamless movement of people and goods.

Electricity Sector and Renewables

- As on 30 September 2022, the government has sanctioned the entire target capacity of 40 GW for the development of 59 Solar Parks in 16 states.

- 17.2 lakh GWh electricity generated during the year FY22 compared to 15.9 lakh GWh during FY21.

- The total installed power capacity (industries having demand of 1 Mega Watt (MW) and above) increased from 460.7 GW on 31 March 2021 to 482.2 GW on 31 March 2022.

Making Indian Logistics Globally Competitive

- National Logistics Policy envisions to develop a technologically enabled, integrated, cost-efficient, resilient, sustainable and trusted logistics ecosystem in the country for accelerated and inclusive growth.

- Rapid increase in National Highways (NHs) /Roads Construction with 10457 km NHs/roads constructed in FY22 compared to 6061 km in FY16.

- Budget expenditure increased from ₹1.4 lakh crore in FY20 to ₹2.4 lakh crore in FY23 giving renewed push to Capital expenditure.

- 2359 Kisan rails transported approximately 7.91 lakh tonnes of perishables, as of October 2022.

- More than one crore air passengers availed the benefit of the UDAN scheme since its inception in 2016.

- Near doubling of capacity of major ports in 8 years.

- Inland Vessels Act 2021 replaced 100-year-old Act to ensure hassle free movement of Vessels promoting Inland Water Transport.

India’s Digital Public Infrastructure

- Unified Payment Interface (UPI)

- UPI-based transactions grew in value (121 per cent) and volume (115 per cent) terms, between 2019-22, paving the way for its international adoption.

- Telephone and Radio – For Digital Empowerment

- Total telephone subscriber base in India stands at 117.8 crore (as of Sept,22), with 44.3 per cent of subscribers in rural India.

- More than 98 per cent of the total telephone subscribers are connected wirelessly.

- The overall tele-density in India stood at 84.8 per cent in March 22.

- 200 per cent increase in rural internet subscriptions between 2015 and 2021.

- Prasar Bharati (India’s autonomous public service broadcaster) – broadcasts in 23 languages, 179 dialects from 479 stations. Reaches 92 per cent of the area and 99.1 per cent of the total population.

- Digital Public Goods

- Achieved low-cost accessibility since the launch of Aadhaar in 2009

- Under the government schemes, MyScheme, TrEDS, GEM, e-NAM, UMANG has transformed market place and has enabled citizens to access services across sectors

- Under Account Aggregator, the consent-based data sharing framework is currently live across over 110 crore bank accounts.

- Open Credit Enablement Network aims towards democratising lending operations while allowing end-to-end digital loan applications

- National AI portal has published 1520 articles, 262 videos, and 120 government initiatives and is being viewed as viewed as a tool for overcoming the language barrier e.g. ‘Bhashini’.

- Legislations are being introduced for enhanced user privacy and creating an ecosystem for standard, open, and interoperable protocols underlining robust data governance.

***

SUMMARY OF THE ECONOMIC SURVEY 2022-23

INDIA TO WITNESS GDP GROWTH OF 6.0 PER CENT TO 6.8 PER CENT IN 2023-24, DEPENDING ON THE TRAJECTORY OF ECONOMIC AND POLITICAL DEVELOPMENTS GLOBALLY

ECONOMIC SURVEY 2022-23 PROJECTS A BASELINE GDP GROWTH OF 6.5 PER CENT IN REAL TERMS IN FY24

ECONOMY IS EXPECTED TO GROW AT 7 PER CENT (IN REAL TERMS) FOR THE YEAR ENDING MARCH 2023, THIS FOLLOWS AN 8.7 PER CENT GROWTH IN THE PREVIOUS FINANCIAL YEAR

CREDIT GROWTH TO THE MICRO, SMALL, AND MEDIUM ENTERPRISES (MSME) SECTOR HAS BEEN REMARKABLY HIGH, OVER 30.5 PER CENT, ON AVERAGE DURING JAN-NOV 2022

CAPITAL EXPENDITURE (CAPEX) OF THE CENTRAL GOVERNMENT, WHICH INCREASED BY 63.4 PER CENT IN THE FIRST EIGHT MONTHS OF FY23, WAS ANOTHER GROWTH DRIVER OF THE INDIAN ECONOMY IN THE CURRENT YEAR

RBI PROJECTS HEADLINE INFLATION AT 6.8 PER CENT IN FY23, WHICH IS OUTSIDE ITS TARGET RANGE

RETURN OF MIGRANT WORKERS TO CONSTRUCTION ACTIVITIES HELPED HOUSING MARKET WITNESSING A SIGNIFICANT DECLINE IN INVENTORY OVERHANG TO 33 MONTHS IN Q3 OF FY23 FROM 42 MONTHS LAST YEAR

SURGE IN GROWTH OF EXPORTS IN FY22 AND THE FIRST HALF OF FY23 INDUCED A SHIFT IN THE GEARS OF THE PRODUCTION PROCESSES FROM MILD ACCELERATION TO CRUISE MODE

PRIVATE CONSUMPTION AS A PERCENTAGE OF GDP STOOD AT 58.4 PER CENT IN Q2 OF FY23, THE HIGHEST AMONG THE SECOND QUARTERS OF ALL THE YEARS SINCE 2013-14, SUPPORTED BY A REBOUND IN CONTACT-INTENSIVE SERVICES SUCH AS TRADE, HOTEL AND TRANSPORT

SURVEY POINTS TO THE LOWER FORECAST FOR GROWTH IN GLOBAL TRADE BY THE WORLD TRADE ORGANISATION, FROM 3.5 PER CENT IN 2022 TO 1.0 PER CENT IN 2023

Posted On: 31 JAN 2023 2:00PM by PIB Delhi

India to witness GDP growth of 6.0 per cent to 6.8 per cent in 2023-24, depending on the trajectory of economic and political developments globally.

The optimistic growth forecasts stem from a number of positives like the rebound of private consumption given a boost to production activity, higher Capital Expenditure (Capex), near-universal vaccination coverage enabling people to spend on contact-based services, such as restaurants, hotels, shopping malls, and cinemas, as well as the return of migrant workers to cities to work in construction sites leading to a significant decline in housing market inventory, the strengthening of the balance sheets of the Corporates, a well-capitalised public sector banks ready to increase the credit supply and the credit growth to the Micro, Small, and Medium Enterprises (MSME) sector to name the major ones.

The Union Minister for Finance & Corporate Affairs Smt. Nirmala Sitharaman tabled the Economic Survey 2022-23 in Parliament today, which projects a baseline GDP growth of 6.5 per cent in real terms in FY24. The projection is broadly comparable to the estimates provided by multilateral agencies such as the World Bank, the IMF, and the ADB and by RBI, domestically.

It says, growth is expected to be brisk in FY24 as a vigorous credit disbursal, and capital investment cycle is expected to unfold in India with the strengthening of the balance sheets of the corporate and banking sectors. Further support to economic growth will come from the expansion of public digital platforms and path-breaking measures such as PM GatiShakti, the National Logistics Policy, and the Production-Linked Incentive schemes to boost manufacturing output.

The Survey says, in real terms, the economy is expected to grow at 7 per cent for the year ending March 2023. This follows an 8.7 per cent growth in the previous financial year.

Despite the three shocks of COVID-19, Russian-Ukraine conflict and the Central Banks across economies led by Federal Reserve responding with synchronised policy rate hikes to curb inflation, leading to appreciation of US Dollar and the widening of the Current Account Deficits (CAD) in net importing economies, agencies worldwide continue to project India as the fastest-growing major economy at 6.5-7.0 per cent in FY23.

According to Survey, India’s economic growth in FY23 has been principally led by private consumption and capital formation and they have helped generate employment as seen in the declining urban unemployment rate and in the faster net registration in Employee Provident Fund. Moreover, World’s second-largest vaccination drive involving more than 2 billion doses also served to lift consumer sentiments that may prolong the rebound in consumption. Still, private capex soon needs to take up the leadership role to put job creation on a fast track.

It also points out that the upside to India’s growth outlook arises from (i) limited health and economic fallout for the rest of the world from the current surge in Covid-19 infections in China and, therefore, continued normalisation of supply chains; (ii) inflationary impulses from the reopening of China’s economy turning out to be neither significant nor persistent; (iii) recessionary tendencies in major Advanced Economies (AEs) triggering a cessation of monetary tightening and a return of capital flows to India amidst a stable domestic inflation rate below 6 per cent; and (iv) this leading to an improvement in animal spirits and providing further impetus to private sector investment.

The Survey says, the credit growth to the Micro, Small, and Medium Enterprises (MSME) sector has been remarkably high, over 30.6 per cent, on average during Jan-Nov 2022, supported by the extended Emergency Credit Linked Guarantee Scheme (ECLGS) of the Union government. It adds that the recovery of MSMEs is proceeding apace, as is evident in the amounts of Goods and Services Tax (GST) they pay, while the Emergency Credit Linked Guarantee Scheme (ECGLS) is easing their debt servicing concerns.

Apart from this, increase in the overall bank credit has also been influenced by the shift in borrower’s funding choices from volatile bond markets, where yields have increased, and external commercial borrowings, where interest and hedging costs have increased, towards banks. If inflation declines in FY24 and if real cost of credit does not rise, then credit growth is likely to be brisk in FY24.

The Capital Expenditure (Capex) of the central government, which increased by 63.4 per cent in the first eight months of FY23, was another growth driver of the Indian economy in the current year, crowding in the private Capex since the January-March quarter of 2022. On current trend, it appears that the full year’s capital expenditure budget will be met. A sustained increase in private Capex is also imminent with the strengthening of the balance sheets of the Corporates and the consequent increase in credit financing it has been able to generate.

Dwelling on halt in construction activities during the Pandemic, the Survey underscores that vaccinations have facilitated the return of migrant workers to cities to work in construction sites as the rebound in consumption spilled over into the housing market. This is evident in the housing market witnessing a significant decline in inventory overhang to 33 months in Q3 of FY23 from 42 months last year.

It also says that the Mahatma Gandhi National Rural Employment Guarantee Scheme (MGNREGS) has been directly providing jobs in rural areas and indirectly creating opportunities for rural households to diversify their sources of income generation. Schemes like PM-Kisan and PM Garib Kalyan Yojana have helped in ensuring food security in the country, and their impact was also endorsed by the United Nations Development Programme (UNDP). The results of the National Family Health Survey (NFHS) also show improvement in rural welfare indicators from FY16 to FY20, covering aspects like gender, fertility rate, household amenities, and women empowerment.

The Survey notes with optimism that Indian economy appears to have moved on after its encounter with the pandemic, staging a full recovery in FY22 ahead of many nations and positioning itself to ascend to the pre-pandemic growth path in FY23. Yet in the current year, India has also faced the challenge of reining in inflation that the European strife accentuated. Measures taken by the government and RBI, along with the easing of global commodity prices, have finally managed to bring retail inflation below the RBI upper tolerance target in November 2022.

It, however, cautions that the challenge of the depreciating rupee, although better performing than most other currencies, persists with the likelihood of further increases in policy rates by the US Fed. The widening of the CAD may also continue as global commodity prices remain elevated and the growth momentum of the Indian economy remains strong. The loss of export stimulus is further possible as the slowing world growth and trade shrinks the global market size in the second half of the current year.

Therefore, the Global growth has been projected to decline in 2023 and is expected to remain generally subdued in the following years as well. The slowing demand will likely push down global commodity prices and improve India’s CAD in FY24. However, a downside risk to the Current Account Balance stems from a swift recovery driven mainly by domestic demand, and to a lesser extent, by exports. It also adds that the CAD needs to be closely monitored as the growth momentum of the current year spills over into the next.

The Survey brings to the fore an interesting fact that in general, global economic shocks in the past were severe but spaced out in time, but this changed in the third decade of this millennium, as at least three shocks have hit the global economy since 2020.

It all started with the pandemic-induced contraction of the global output, followed by the Russian-Ukraine conflict leading to a worldwide surge in inflation. Then, the central banks across economies led by the Federal Reserve responded with synchronised policy rate hikes to curb inflation. The rate hike by the US Fed drove capital into the US markets causing the US Dollar to appreciate against most currencies. This led to the widening of the Current Account Deficits (CAD) and increased inflationary pressures in net importing economies.

The rate hike and persistent inflation also led to a lowering of the global growth forecasts for 2022 and 2023 by the IMF in its October 2022 update of the World Economic Outlook. The frailties of the Chinese economy further contributed to weakening the growth forecasts. Slowing global growth apart from monetary tightening may also lead to a financial contagion emanating from the advanced economies where the debt of the non-financial sector has risen the most since the global financial crisis. With inflation persisting in the advanced economies and the central banks hinting at further rate hikes, downside risks to the global economic outlook appear elevated.

India’s Economic Resilience and Growth Drivers

The Survey points out that factors like monetary tightening by the RBI, the widening of the CAD, and the plateauing growth of exports have essentially been the outcome of geopolitical strife in Europe. As these developments posed downside risks to the growth of the Indian economy in FY23, many agencies worldwide have been revising their growth forecast of the Indian economy downwards. These forecasts, including the advance estimates released by the NSO, now broadly lie in the range of 6.5-7.0 per cent.

Despite the downward revision, the growth estimate for FY23 is higher than for almost all major economies and even slightly above the average growth of the Indian economy in the decade leading up to the pandemic.

IMF estimates India to be one of the top two fast-growing significant economies in 2022. Despite strong global headwinds and tighter domestic monetary policy, if India is still expected to grow between 6.5 and 7.0 per cent, and that too without the advantage of a base effect, it is a reflection of India’s underlying economic resilience; of its ability to recoup, renew and re-energise the growth drivers of the economy. India’s economic resilience can be seen in the domestic stimulus to growth seamlessly replacing the external stimuli. The growth of exports may have moderated in the second half of FY23. However, their surge in FY22 and the first half of FY23 induced a shift in the gears of the production processes from mild acceleration to cruise mode.

Manufacturing and investment activities consequently gained traction. By the time the growth of exports moderated, the rebound in domestic consumption had sufficiently matured to take forward the growth of India’s economy. Private Consumption as a percentage of GDP stood at 58.4 per cent in Q2 of FY23, the highest among the second quarters of all the years since 2013-14, supported by a rebound in contact-intensive services such as trade, hotel and transport, which registered sequential growth of 16 per cent in real terms in Q2 of FY23 compared to the previous quarter.

Although domestic consumption rebounded in many economies, the rebound in India was impressive for its scale. It contributed to a rise in domestic capacity utilisation. Domestic private consumption remains buoyant in November 2022. Moreover, RBI’s most recent survey of consumer confidence released in December 2022 pointed to improving sentiment with respect to current and prospective employment and income conditions.

The Survey also points to another recovery and adds that the “release of pent-up demand” was reflected in the housing market too as demand for housing loans picked up. Consequently, housing inventories have declined, prices are firming up, and construction of new dwellings is picking up pace and this has stimulated innumerable backward and forward linkages that the construction sector is known to carry. The universalisation of vaccination coverage also has a significant role in lifting the housing market as, in its absence, the migrant workforce could not have returned to construct new dwellings.

Apart from housing, construction activity, in general, has significantly risen in FY23 as the much-enlarged capital budget (Capex) of the central government and its public sector enterprises is rapidly being deployed.

Going by the Capex multiplier estimated for the country, the economic output of the country is set to increase by at least four times the amount of Capex. States, in aggregate, are also performing well with their Capex plans. Like the central government, states also have a larger capital budget supported by the centre’s grant-in-aid for capital works and an interest-free loan repayable over 50 years.

Also, a capex thrust in the last two budgets of the Government of India was not an isolated initiative meant only to address the infrastructure gaps in the country. It was part of a strategic package aimed at crowding-in private investment into an economic landscape broadened by the vacation of non-strategic PSEs (disinvestment) and idling public sector assets.

Here, three developments support this firstly the significant increase in the Capex budget in FY23, as well as its high rate of spending, secondly direct tax revenue collections have been highly buoyant, and so have GST collections, which should ensure the full expending of the Capex budget within the budgeted fiscal deficit. The growth in revenue expenditure has also been limited to pave the way for higher growth in Capex and thirdly the pick-up in private sector investment since the January-March quarter of 2022. Evidence shows an increasing trend in announced projects and capex spending by the private players.

While an increase in export demand, rebound in consumption, and public capex have contributed to a recovery in the investment/manufacturing activities of the corporates, their stronger balance sheets have also played a big part equal measure to realising their spending plans. As per the data on non-financial debt from the Bank for International Settlements, in the course of the last decade, Indian non-financial private sector debt and non-financial corporate debt as a share of GDP declined by nearly thirty percentage points.

The banking sector in India has also responded in equal measure to the demand for credit as the Year-on-Year growth in credit since the January-March quarter of 2022 has moved into double-digits and is rising across most sectors.

The finances of the public sector banks have seen a significant turnaround, with profits being booked at regular intervals and their Non-Performing Assets (NPAs) being fast-tracked for quicker resolution/liquidation by the Insolvency and Bankruptcy Board of India (IBBI). At the same time, the government has been providing adequate budgetary support for keeping the PSBs well-capitalized, ensuring that their Capital Risk-Weighted Adjusted Ratio (CRAR) remains comfortably above the threshold levels of adequacy. Nonetheless, financial strength has helped banks make up for lower debt financing provided by corporate bonds and External Commercial Borrowings (ECBs) so far in FY23. Rising yields on corporate bonds and higher interest/hedging costs on ECBs have made these instruments less attractive than the previous year.

RBI has projected headline inflation at 6.8 per cent in FY23, which is outside its target range. At the same time, it is not high enough to deter private consumption and also not so low as to weaken the inducement to invest.

Macroeconomic and Growth Challenges in the Indian Economy

After the impact of the two waves of the pandemic seen in a significant GDP contraction in FY21, the quick recovery from the virus in third wave of Omicron contributed to minimising the loss of economic output in the January-March quarter of 2022. Consequently, output in FY22 went past its pre-pandemic level in FY20, with the Indian economy staging a full recovery ahead of many nations. However, the conflict in Europe necessitated a revision in expectations for economic growth and inflation in FY23. The country’s retail inflation had crept above the RBI’s tolerance range in January 2022 and it remained above the target range for ten months before returning to below the upper end of the target range of 6 per cent in November 2022.

It says that the Global commodity prices may have eased but are still higher compared to pre-conflict levels and they have further widened the CAD, already enlarged by India’s growth momentum. For FY23, India has sufficient forex reserves to finance the CAD and intervene in the forex market to manage volatility in the Indian rupee.

Outlook: 2023-24

Dwelling on the Outlook for 2023-24, the Survey says, India’s recovery from the pandemic was relatively quick, and growth in the upcoming year will be supported by solid domestic demand and a pickup in capital investment. It says that aided by healthy financials, incipient signs of a new private sector capital formation cycle are visible and more importantly, compensating for the private sector’s caution in capital expenditure, the government raised capital expenditure substantially.

Budgeted capital expenditure rose 2.7 times in the last seven years, from FY16 to FY23, re-invigorating the Capex cycle. Structural reforms such as the introduction of the Goods and Services Tax and the Insolvency and Bankruptcy Code enhanced the efficiency and transparency of the economy and ensured financial discipline and better compliance, the Survey added.

Global growth is forecasted to slow from 3.2 per cent in 2022 to 2.7 per cent in 2023 as per IMF’s World Economic Outlook, October 2022. A slower growth in economic output coupled with increased uncertainty will dampen trade growth. This is seen in the lower forecast for growth in global trade by the World Trade Organisation, from 3.5 per cent in 2022 to 1.0 per cent in 2023.

On the external front, risks to the current account balance stem from multiple sources. While commodity prices have retreated from record highs, they are still above pre-conflict levels. Strong domestic demand amidst high commodity prices will raise India’s total import bill and contribute to unfavourable developments in the current account balance. These may be exacerbated by plateauing export growth on account of slackening global demand. Should the current account deficit widen further, the currency may come under depreciation pressure.

Entrenched inflation may prolong the tightening cycle, and therefore, borrowing costs may stay ‘higher for longer’. In such a scenario, global economy may be characterised by low growth in FY24. However, the scenario of subdued global growth presents two silver linings – oil prices will stay low, and India’s CAD will be better than currently projected. The overall external situation will remain manageable.

India’s Inclusive Growth

The Survey emphasises that growth is inclusive when it creates jobs. Both official and unofficial sources confirm that employment levels have risen in the current financial year, as the Periodic Labour Force Survey (PLFS) shows that the urban unemployment rate for people aged 15 years and above declined from 9.8 per cent in the quarter ending September 2021 to 7.2 per cent one year later (quarter ending September 2022). This is accompanied by an improvement in the labour force participation rate (LFPR) as well, confirming the emergence of the economy out of the pandemic-induced slowdown early in FY23.

In FY21, the Government announced the Emergency Credit Line Guarantee Scheme, which succeeded in shielding micro, small and medium enterprises from financial distress. A recent CIBIL report (ECLGS Insights, August 2022) showed that the scheme has supported MSMEs in facing the COVID shock, with 83 per cent of the borrowers that availed of the ECLGS being micro-enterprises. Among these micro units, more than half had an overall exposure of less than Rs10 lakh.

Furthermore, the CIBIL data also shows that ECLGS borrowers had lower non-performing asset rates than enterprises that were eligible for ECLGS but did not avail of it. Further, the GST paid by MSMEs after declining in FY21 has been rising since and now has crossed the pre-pandemic level of FY20, reflecting the financial resilience of small businesses and the effectiveness of the pre-emptive government intervention targeted towards MSMEs.

Moreover, the scheme implemented by the government under the Mahatma Gandhi National Rural Employment Guarantee Act (MGNREGA) has been rapidly creating more assets in respect of “Works on individual’s land” than in any other category. In addition, schemes like PM-KISAN, which benefits households covering half the rural population, and PM Garib Kalyan Anna Yojana have significantly contributed to lessening impoverishment in the country.

The UNDP Report of July 2022 stated that the recent inflationary episode in India would have a low poverty impact due to well-targeted support. In addition, the National Family Health Survey (NFHS) in India shows improved rural welfare indicators from FY16 to FY20, covering aspects like gender, fertility rate, household amenities, and women empowerment.

So far, India has reinforced the country’s belief in its economic resilience as it has withstood the challenge of mitigating external imbalances caused by the Russian-Ukraine conflict without losing growth momentum in the process. India’s stock markets had a positive return in CY22, unfazed by withdrawals by foreign portfolio investors. India’s inflation rate did not creep too far above its tolerance range compared to several advanced nations and regions.

India is the third-largest economy in the world in PPP terms and the fifth-largest in market exchange rates. As expected of a nation of this size, the Indian economy in FY23 has nearly “recouped” what was lost, “renewed” what had paused, and “re-energised” what had slowed during the pandemic and since the conflict in Europe.

The global economy battles through a unique set of challenges

The Survey narrates about six challenges faced by the Global Economy. The three challenges like COVID-19 related disruptions in economies, Russian-Ukraine conflict and its adverse impact along with disruption in supply chain, mainly of food, fuel and fertilizer and the Central Banks across economies led by Federal Reserve responding with synchronised policy rate hikes to curb inflation, leading to appreciation of US Dollar and the widening of the Current Account Deficits (CAD) in net importing economies. The fourth challenge emerged as faced with the prospects of global stagflation, nations, feeling compelled to protect their respective economic space, thus slowing cross-border trade affecting overall growth. It adds that all along, the fifth challenge was festering as China experienced a considerable slowdown induced by its policies. The sixth medium-term challenge to growth was seen in the scarring from the pandemic brought in by the loss of education and income-earning opportunities.

The Survey notes that like the rest of the world, India, too, faced this extraordinary set of challenges but withstood them better than most economies.

In the last eleven months, the world economy has faced almost as many disruptions as caused by the pandemic in two years. The conflict caused the prices of critical commodities such as crude oil, natural gas, fertilisers, and wheat to soar. This strengthened the inflationary pressures that the global economic recovery had triggered, backed by massive fiscal stimuli and ultra-accommodative monetary policies undertaken to limit the output contraction in 2020. Inflation in Advanced Economies (AEs), which accounted for most of the global fiscal expansion and monetary easing, breached historical highs. Rising commodity prices also led to higher inflation in the Emerging Market Economies (EMEs), which otherwise were in the lower inflation zone by virtue of their governments undertaking a calibrated fiscal stimulus to address output contraction in 2020.

The Survey underlines that Inflation and monetary tightening led to a hardening of bond yields across economies and resulted in an outflow of equity capital from most of the economies around the world into the traditionally safe-haven market of the US. The capital flight subsequently led to the strengthening of the US Dollar against other currencies – the US Dollar index strengthened by 16.1 per cent between January and September 2022. The consequent depreciation of other currencies has been widening the CAD and increasing inflationary pressures in the net importing economies.

****