About GIFT city: GIFT City is the only operational green smart city in India, located between Ahmedabad and Gandhinagar on the bank of the river Sabarmati.

GIFT city includes Office spaces, Residential Apartments, Schools, Hospital, Hotels, Clubs, Retail and various Recreational facilities, which makes this City a truly “Walk to Work” City. GIFT City consist of a conducive Multi-Service SEZ (Special Economic Zone) and an exclusive Domestic Area.

It is being developed as a multi-service special economic zone and a global financial service hub having a competitive tax regime to attract financial service providers such as banking units, insurance companies, capital market intermediary and ancillary services providers to provide their services globally and also invite inbound and outbound individuals and corporates around the world to use the quality financial service products at India’s first IFSC platform.

In this presentation we providing the brief about an setting up an Alternative Investment Fund (AIF) in GIFT-SEZ IFSC, GIFT city, Gandhinagar.

AIF set up in GIFT-SEZ IFSC will allow investors as well as promoters to invest in the listed or unlisted securities and other financial products available across the globe and avail various tax benefits under taxation laws of the India.

AIF is a privately pooled investment vehicle registered under SEBI, Which collect funds from defined class of investors, and invest accordance to investment policy defined by SEBI, but it does not include followings:

Key Benefits for AIF & Investors

KEY BENEFITS FOR AIFs IN IFSC

- Lower Operating Costs

- Competitive Tax Regime

- No limits on outbound investments

- Engagement with unified financial regulator

- Permitted to borrow funds and engage in leveraging activities

- Enabling ecosystem for fund management with presence of key stakeholders including custodians and fund administrators

- No diversification limits on investments made by an AIF in IFSC provided the investment made is in line with the risk appetite of the investors and appropriate disclosures are made.

Benefits for Relocation of offshore funds

Relocation of Off shore Fund to a resultant fund in IFSC to be tax neutral for Off-shore Fund, resultant fund and its shareholders/ unit holders as follows:

- Transfer of assets of an Off shore Fund or its Wholly owned subsidiary (1WOS”) to a Resultant Fund, upon relocation to IFSC on or before 31 March 2023 is not regarded as transfer,

- Exemption also provided to non-resident shareholders of Off shore Fund I Off shore Fund on transfer of units/ beneficial interest of Off shore fund In consideration of units/ beneficial interest of Resultant fund in IFSC

- Grandfathered investments i n the fund will continue to enjoy capital gains exemption on future sales by the Resultant fund n IFSC

- Period of holding and cost to previous owner are available to Resultant Fund.

- Deemed income provisions under the Indian tax laws are not applicable to the Resultant fund on relocation.

- Carry fon Nard losses of portfolio company are not impacted on such relocation.

- Sponsor and/or manager contribution made voluntary.

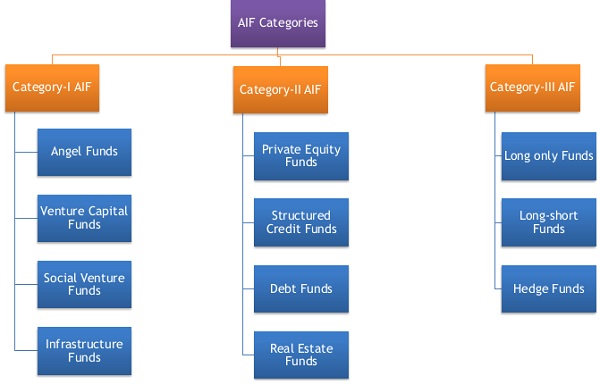

Categories of Alternative Investment Fund (AIF)

Category-I AIF

AIF which invest in start-ups or early stage of ventures, also knows as “Venture Capital Company” or “Venture Capital Fund”

Category-II AIF

- Funds which do not fall in Category-I and category-III

- may undertake leverage subject to consent of investors and with disclosure of methodology of calculation of leverage in placement memorandum with and shall have comprehensive risk management framework according to size and risk profile of fund.

Category-III AIF

- Funds which employs diverse or complex trading strategies and may employ leverage through invest in listed or unlisted derivatives.

- Open and close ended funds mainly interested in making short term returns.

- Invest in securities of listed and unlisted investee companies, derivatives, complex or structured products.

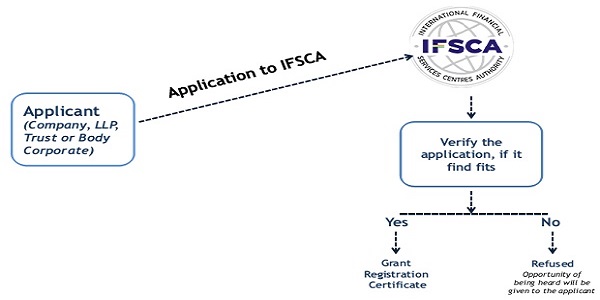

Registration of AIF with IFSCA

Eligibility Criteria of AIF

Entity should be permits to carry on the activity of an AIF by MOA, trust deed and LLP deed in case of company, trust and LLP respectively.

> AIF should be restrained from public subscription.

> Applicant, Sponsor and manager should be proper and competent person.

> Composition of Management Team:

- At least one key personnel having minimum 5 years experience in security market transactions.

- At least one key personnel with professional qualification in finance, accountancy, economics, Management, Capital market from recognised university or institution.

> Should have necessary infrastructure and manpower.

> Investment objective, targeted investors, proposed corpus and investment style and strategy should be clear.

> Any application by same manager or sponsor should not be refused by SEBI/IFSCA previously.

> IFSCA may grant certificate of registration of AIF, with or without conditions, if it is satisfied that applicant fulfills all the necessary requirements.

Structure of AIF

AIF in IFSC

| Criteria | Category –I AIF | Category –II AIF | Category –III AIF |

| IFSCA Application Fee | $ 2,500 | $ 2,500 | $ 2,500 |

| IFSCA Registration Fee | $ 7,500 | $ 15,000 | $ 22,500 |

| Minimum Corpus

(Each Scheme) |

$ 3 Million | $ 3 Million | $ 3 Million |

| FDI Direct Root | Permitted | Permitted | Permitted |

| Investment scheme type | Close ended | Close Ended | Open / Close Ended |

| Tenure of scheme | 3 years minimum | 3 years minimum | As per placement memorandum |

| Maximum investment in single investee company | No limit | No limit | No limit |

| Leverage | Allowed | Allowed | Allowed |

Raising of fund by AIF in GIFT SEZ-IFSC

- Raise fund through private placement.

- AIF should be restrained from public subscription.

- AIF Need to prepare placement memorandum.

- File Placement Memorandum with IFSCA, 30 days before launch of scheme.

- No scheme fees payable for first scheme launch by AIF.

Investor in IFSC-AIF

- Non resident including NRI

- Domestic institutional investors

- Resident individuals having net worth =>1 million USD

Investment by AIF

General investment conditions

- AIF allowed to invest in securities of company incorporate outside India subject to RBI Guidelines.

- The capping limit of investment i.e. 25% or 10% not applied to AIF in IFSC, provided that appropriate disclosers have been made in placement memorandum.

- AIFs shall not invest in associates without approval of 75% of investor by value in AIF.

- Un-invested portion fund may be invested in higher liquid funds like bank deposit, liquid mutual funds, Treasury Bills etc.

- AIF in IFSC are permitted in to co-invest in a portfolio company through segregated portfolio by issuing a separate class of units (not at more favorable conditions than common portfolio).

Deployment of funds by IFSC-AIF

IFSC AIFs have 5 investment avenues to deploy funds-

- Securities listed in IFSC;

- Securities issued by companies incorporated in IFSC;

- Securities issued by companies incorporated in India or foreign jurisdiction

- Units of an AIF

- Securities which a domestic AIF is permitted to invest in.

For investments in India, FPI/ FDI/ FVCI limits would apply. However, existing conditions on outbound investments by AIFs do not apply to IFSC AIFs i.e., no SEBI approval required for investments outside India.

Category – I AIF

- Allowed investment for all sub categories:

- Companies

- Venture capital

- Special purpose vehicles

- LLPs

- Units of category-I AIF (same sab category)

- Can borrow funds subject to consent of investors and with disclosure of methodology of calculation of leverage in placement memorandum with and shall have comprehensive risk management framework according to size and risk profile of fund.

Venture capital funds

- 2/3 of investable fund shall be invested in:

- Unlisted equity shares.

- Equity linked instrument (ELI) of venture capital undertaking (VCU).

- Companies listed or proposed to be listed on SME Exchange.

- Not more than 1/3 of investable fund shall be invested in:

- IPO of VCU.

- Debt of VCU in which investment are already made.

- Preferential allotment of equity shares or ELI of listed company subject to 1 year lock in period.

- Equity shares of listed financially weak company or sick industrial company.

- Special purpose vehicle created by fund.

- May enter into agreement with merchant banker for market making.

- Exempt from regulation 3 & 3A SEBI (Prohibition of Insider Trading) Regulation 1992 in case of investment in SMEs.

SME funds

- 3/4 of investable fund shall be invested in:

- Unlisted securities SME companies.

- Partnership interest of SME venture capital undertaking (VCU).

- Companies listed or proposed to be listed on SME Exchange.

- May enter into agreement with merchant banker for market making.

- Exempt from regulation 3 & 3A SEBI (Prohibition of Insider Trading) Regulation 1992 in case of investment in SMEs.

- Investment in listed SMEs shall have lock in period of one year.

Social venture funds

- 3/4 of investable fund shall be invested in:

- Unlisted securities or partnership interest of social ventures.

- May accept grants, subject to minimum 25 lakhs rupees value, no profit to be accrue to provider.

- May give grants to social ventures.

- May accept lower than prevailing returns on their investment.

Infrastructure funds

- 3/4 of investable fund shall be invested in following entities engaged in or formed for the purpose of operating, developing, or holding infrastructure projects:

- Unlisted securities or units of companies.

- Partnership interest of venture capital undertaking (VCU).

- Special purpose vehicle

- Listed securitized debt instruments.

- Listed debt securities.

Investment by Category-II AIF

- Invest primarily in unlisted investee companies or units of other AIF specified in placement memorandum.

- May invest in units of category I & II AIFs, shall not invest in units of other fund of funds.

- Can borrow funds subject to consent of investors and with disclosure of methodology of calculation of leverage in placement memorandum with and shall have comprehensive risk management framework according to size and risk profile of fund.

- May engage in hedging.

- May enter into agreement with merchant banker for market making.

- Exempt from regulation 3 & 3A SEBI (Prohibition of Insider Trading) Regulation 1992 in case of investment in SMEs.

- Investment in listed SMEs shall have lock in period of one year

Investment by Category-III AIF

- May invest in securities of listed or unlisted investee companies or derivatives or complex or structured products.

- May deal in goods received in physical settlement of commodity derivatives.

- May invest in units of category I & II AIFs, shall not invest in units of other fund of funds.

- Can borrow funds or engage leverage with consent of investor, up to limit specified by board.

Taxation of AIF in IFSC

Category I & II AIFs

- Business income of AIF is taxable in than hand of AIF for which 100% tax exemption can be claimed for consecutive 10 years out of block of 15 years.

- Investor are taxed on the income from investment made by AIF as if investment made directly be them. Investor are allowed to claim losses subject to holding more than 12 months.

- Income accruing or arising or received by non-resident investors from offshore investments through a Category I and II AIF is not taxable in India.

- Non resident are exempt from filing ITR subject to earning income from investment made in only CAT-I & Cat-II AIF funds and Tax has been deducted on distribution made by AIF.

Category III AIF

- No tax on income earned by CAT-III AIF on overseas investment made, which are attributable to Non resident investors.

- Income on transfer of shares on an Indian company is liable to capital gain tax as follows:

- Short-term Capital Gains -15%

- Long-term Capital Gains -10%

- Income in respect of securities (such as interest, dividend) is taxable to the Category III AIF at the rate of 10% (5% in case of interest income on certain rupee denominated bonds, government securities or municipal debt securities referred to in section 194LD)

- Any income accruing or arising to or received from the Category III AIF or on transfer of its units is exempt from tax in the hands of investors.

- Exemption from stamp duty, Securities Transaction Tax and Commodities Transaction Tax for transactions carried out on IFSC exchanges.

Article is contributed by RRBP CORPSERVE LLP (SEZ IFSC Consultants) through Bharat Prajapat (Managing Partner) and he can be reached at cs@rrbp.in.