1. Introduction:

1.1 The imported goods before clearance for home consumption or for warehousing are required to comply with prescribed Customs clearance formalities. This includes presentation of a Bill of Entry containing details such as description of goods, value, quantity, exemption notification, Customs Tariff Heading etc. The Bill of Entry is subject to verification by the proper officer of Customs (under self-assessment scheme) and may be reassessed if declarations are found to be incorrect. Normally import declarations made are scrutinized with reference to documents and other information about the value / classification etc., without prior examination of goods. It is at the time of clearance of goods that these are examined by the Customs to confirm the nature of goods, valuation and other aspects of the declarations. However, it may be noted that examination of goods is carried out only after facilitation level is decided by the Risk Management System. In case no discrepancies are observed at the time of examination of goods ‘Out of Charge’ order is issued and thereafter the goods can be cleared. Similarly, Customs clearance formalities for goods meant for export have to be fulfilled by presenting a Shipping Bill and other related documents. These documents are verified for correctness of assessment and after examination of the goods, if warranted, “Let Export Order” is given on the Shipping Bill.

2. Import procedure – Bill of Entry:

2.1 Goods imported into the country attract Customs duty and are also required to confirm to relevant and corresponding legal requirements. Thus, unless the imported goods are not meant for Customs clearance at the port/airport of arrival such as those intended for transit by the same vessel/aircraft or transshipment to another Customs station or to any place outside India, detailed Customs clearance formalities have to be followed by the importers. In contrast, in terms of Section 52 to 56 of the Customs Act, 1962, the goods mentioned in the IGM or Import Report for transit to any place outside India or meant for transshipment to another Customs station in India are allowed transit without payment of duty. In case of goods meant for transshipment to another Customs station, simple transshipment procedure has to be followed by the carrier and the concerned agencies at the first port/airport of landing and the Customs clearance formalities have to be complied with by the importer after arrival of the goods at the other Customs station where goods are intended to be delivered to the importer. There could also be cases of transshipment of the goods after unloading to a port outside India. For this purpose, a simple procedure is prescribed and no duty is required to be paid.

2.2 For goods which are offloaded at a port/airport for clearance, the importers have the option to clear the goods for home consumption after payment of duties leviable or to clear them for warehousing without immediate discharge of the duties leviable in terms of the warehousing provisions of the Customs Act, 1962. For the purpose of clearance of imported goods, every importer is required to file, in terms of the Section 46 ibid, a Bill of Entry for home consumption or warehousing, as the case may be, in the form prescribed under the relevant regulations. In cases where it is not feasible to make entry electronically on the customs automated system, Principal Commissioner of Customs or Commissioner of Customs, allow an entry in any other manner.

2.3 Foreign Trade Policy provides that Importer-Export Code (IEC) number, a 10-character alphanumeric allotted to a person by the Directorate General of Foreign Trade (DGFT) is mandatory for undertaking any export/import activities. However, exempt categories and corresponding permanent IEC numbers are provided in Para 2.07 of Handbook of Procedures issued by DGFT.

2.4 For clearance of goods through the EDI system, the importer is required to file a cargo declaration having prescribed particulars required for processing of the Bill of Entry for Customs clearance.

2.5 Under the EDI system, the importer by himself or through his authorized customs broker may file the declarations in electronic format through the service centre or ICEGATE. Facility of uploading scanned documents along with the declaration for filing a bill of Entry, is also available through “e Sanchit’ programme.

2.6 As already explained under Chapter 1 (under paras 8.7 and 9.2), CBIC has implemented Faceless Assessment on imports whereby assessment of Bills of Entry are now being done by an officer located in a remote office other than the Customs station where the goods are presented for Customs clearance.

3. Self-assessment of imported and export goods:

3.1 Section 17 of the Customs Act, 1962 provides that an importer entering any imported goods under section 46 or an exporter entering any export goods under section 50 shall self-assess the duty. Thus, under self-assessment, it is the importer or exporter who will ensure that he declares the correct classification, applicable rate of duty, value, benefit of exemption notifications claimed, if any, etc. in respect of the imported / export goods while presenting Bill of Entry or Shipping Bill.

3.2 The declaration filed by the importer or exporter may be verified by the proper officer when so interdicted by the Risk Management Systems (RMS). Such verification will be done selectively on the basis of the RMS, which not only provides assured facilitation to those importers having a good track record of compliance but ensures that on the basis of certain rules, intervention, etc., high risk consignments are interdicted for detailed verification before clearance. On the basis of interdictions under RMS, Bills of Entry may either be taken up for verification of assessment or for examination of the imported goods or both. If the self-assessment is found incorrect, the duty may be reassessed. In cases where there is no interdiction by RMS or non existence of any other factor, there will be no cause for the declaration filed by the importer to be taken up for verification, and such Bills of Entry will straightaway be facilitated for clearance without assessment and examination, on payment of applicable duty, if any.

3.3 The verification of a self-assessed Bill of Entry or Shipping Bill, which are interdicted by the RMS, shall be with regard to correctness of classification, value, rate of duty, exemption notification or any other relevant particular having bearing on correct assessment of imported or export goods. For the purpose of verification, the proper officer may order for examination or testing of the imported or export goods. The proper officer may also require production of any relevant document or ask the importer or exporter to furnish any other relevant information. Thereafter, if the self-assessment is not found to have been done correctly, the proper officer may re-assess the duty. This is without prejudice to any other action that may be warranted under the Customs Act, 1962. On reassessment, contrary to the self-assessment done by the importer or exporter, the proper officer shall pass a speaking order, if so desired by the importer or exporter, within 15 days from the date of re-assessment of bill of entry or shipping bill. When verification of self-assessment in terms of Section 17 requires testing / further documents / information, and the goods cannot be re-assessed quickly however, the importer or the exporter requires the goods to be cleared on urgent basis. In such cases, provisional assessment may be done in terms of Section 18 of the Customs Act, 1962, once the importer or exporter, as the case may be, furnishes such security as deemed fit by the proper officer of Customs for payment of deficiency, if any, between the duty as may be finally assessed or re-assessed as the case may be, and the duty provisionally assessed.

3.4 In cases, where the importer or exporter is not able to determine the duty liability or make self- assessment for any reason, except in cases where examination is requested by the importer under proviso to Section 46(1), a request shall be made to the proper officer for provisional assessment of duty under Section 18 (1)(a) of the Customs Act, 1962. In such a situation an option is available to the proper officer to resort to provisional assessment of duty by asking the importer / exporter to furnish security as deemed fit for payment of the deficiency, if any, between the duty as may be finally assessed or re-assessed, as the case may be, and the duty provisionally assessed.

3.5 For the purpose of proper assessment of duty and to ensure correctness of trade statistics, importers/exporters should mandatorily declare the Standard Unit Quantity Code (UQC), as indicated in the Customs Tariff Act, 1975.

[Refer Circular No. 26/2013-Cus. dated 19-7-2013] 32

4. Turant Customs

4.1 India has seen significant improvements in the World Bank’s Ease of Doing Business (EoDB) Index rankings in recent years. Customs is concerned with the `Trading Across Borders` (TAB) component of the EoDB index which is primarily based on time and cost of import and export processes. The improvements in the TAB parameter of EoDB Index have been made possible largely due to several reform measures initiated and implemented by the CBIC, which inter alia include SWIFT, e-Sanchit, DPD, revised AEO programme, RFID e-seal programme etc. which combined to reduce the time and cost of clearance of goods in the various Customs ports. The next target of Government is to be in the top 50 of the EoDB ranking in this category and the efforts in this direction are being spearheaded by the CBIC by the introduction of the next generation reforms aptly named Turant Customs which is a comprehensive package of various elements that have been implemented in recent years. The next generation reforms in the Customs clearance process under the umbrella of Turant Customs are with the objectives of speedy clearance, transparency in decision making, and ease of doing business. Board rolled out numerous changes to the Customs clearance process, which combine together support Turant Customs. These initiatives include the self-registration of goods by importers, automated clearances of bills of entry, digitisation of customs documents, paperless clearance, etc. The Turant Customs is primarily based on Faceless, Contactless and Paperless Customs processes.

4.2 Faceless Customs

4.2.1 Indian Customs has initiated Faceless Assessment on imports from June 2020 (Reference Circular No.28/2020-Customs and Instruction No.09/2020 both dated 5th June 2020). The first phase began by linking Chennai and Bengaluru which was gradually expanded to other geographical locations till eventual all India coverage by 31.10.2020. Briefly put, Faceless Assessment uses a technology platform to separate the Customs assessment process from the physical location of a Customs officer at the port of arrival. This measure is with the intent of bolstering efforts to ensure an objective, free, fair and just assessment. Key objectives of Faceless Assessment include:

(i) Anonymity in assessment for reduced physical interface between trade and Customs

(ii) Speedier Customs clearances through efficient utilisation of manpower

(iii) Greater uniformity of assessment across locations

(iv) Promoting sector specific and functional specialisation in assessment.

4.2.2 To further smoothen implementation of Faceless Assessment and to have a robust system in place for meeting desired objectives as above, the Central Board of Indirect Taxes and Customs (CBIC) constituted the National Assessment Centres (NACs) in September 2020. These NACs have been mandated, amongst other responsibilities, to monitor assessments, to set up structures for liasoning with different Customs formations and Directorates under CBIC, to function as knowledge hub for the commodities assigned to that particular NAC etc., (Reference Circular No.40/2020-Customs dated 4th September 2020).

4.2.3 Subsequent to all India coverage of imports by Faceless Assessment, CBIC took certain measures for timely assessment and faster clearance of goods such as-measures to ensure that there would be no delays on weekends and holidays, measures to minimize and rationalize raising of queries to importers, measures to streamline import cases which are to be sent for First Check examinations, measures for better facilitations by warranting interactions between NACs and Risk Management Division of CBIC, guidelines for reassessing imports as well as general grievance redressal mechanisms and issues relating to enforcement of Rules of Origin (Reference Circular No.45/2020-Customs dated 12th October 2020).

4.2.4 After comprehensive stakeholder consultations with members of the trade, CBIC issued fresh directions and clarifications on various aspects relating to Faceless Assessment such as re-assessments to be done in accordance with principles of natural justice, requirement of members of the trade to ensure full and complete submission of required documents and accurate declarations, increasing the monetary limits for assessment and for sensitizing Customs officers in assessment of liquid bulk cargo (Reference Circular No.55/2020-Customs dated 17th December 2020).

4.2.5 In July 2021, CBIC has taken a call to increase facilitation to 90 percentage (%). This implies that more number of import documents would be cleared without intervention of Customs officers. Linked to this decision, the existing Direct Port Delivery (DPD) scheme has also been revamped to shift to a regime of Customs document based DPD from existing client based DPD. CBIC has also prescribed time limits for assessments and has taken a call to further re-organise composition of Faceless Assessment Groups (FAGs) under the NACs with the intent to foster faster clearances and better facilitation. (Reference Circular No.14/2021-Customs dated 7th July 2021).

4.2.6 Standard Examination Order:

In order to enhance uniformity in assessments across various customs ports across the country, CBIC has implemented Standard Examination Orders in the Customs system. The said implementation started for goods covered under Assessment Group 4 in all the Customs Stations. This functionality is expected to enhance the uniformity in examination, and lower the time taken in the process as well as reduce associated costs. Considering the on track implementation and to harmonize the examination orders across FAGs, the Board has implemented the Standard Examination Orders to the goods across all other Assessment Groups also.

[Refer Circulars No.14/2021-Customs dated 07.07.2021, No.16/2022-Customs dated 29.08.2022, No.23/2022-Customs dated 03.11.2022 and No. 02/2023 dated 11.01.2023]

4.3 Contactless Customs: In recent years, CBIC has initiated reforms such as online registration of goods, automated queuing and automated clearances of Bills of Entry, simplified online registration in ICEGATE, auto debit of bonds, setting up of Turant Suvidha Kendras (TSKs) etc. All these have enabled an environment which has done away with the requirement of members of the trade to physically interact with Customs in the goods clearances process and has fostered a `Contactless Customs` environment.

4.3.1 Online registration of goods: A facility has been provided for the importers or their authorised persons to register the goods online on the ICEGATE web portal after the goods have arrived (and not after payment of duty, as per previous practice). This self registration has further reduced the time of clearance besides freeing the Customs officers for handling other important items of work.

[Refer Circular No.09/2019-Customs dated 28th February 2019]

4.3.2 Automated queuing of Bills of Entry: Significant changes have been made in the ICES 1.5 for clearance of imported goods after finalisation of assessment and payment of duty under Section 47(1) of the Customs Act, 1962. The proper officer now has access to a fully automated queue of Bills of Entry ready for the grant of clearance in the ICES 1.5 which obviates the present necessity of the importer/authorised person having to present the Bill of Entry number and date to this officer for seeking clearance. Based upon the Bills of Entry which are ready for clearance in this automated queue the proper officer would be able to directly and immediately grant clearance on the System. Besides greatly reducing the dwell time of the goods that are pending only for the grant of such clearance, this has reduced the interface of the trade with the department personnel to the advantage of both. The Bills of Entry which are fully facilitated by the Risk Management System will also be automatically routed to the proper officer for giving clearance after registration has been completed by the importer.

[Refer Circular No.09/2019-Customs dated 28th February 2019]

4.3.3 Automated clearances of Bills of Entry : A further trade facilitation initiative in the Customs clearance process is the Customs Compliance Verification (CCV) which operates after an importer registers the imported goods even while duty has not been paid or its payment is in process. Once the goods are registered, the proper officer carries out all necessary verifications as per Sections 17/18 and Section 47(1) of the Customs Act, 1962. On satisfaction that the goods are ready for clearance, but for the payment of duties, the proper officer confirms the completion of the CCV for the particular Bill of Entry in the System. Thereafter, on payment of duty by the importer, the Customs Automated System electronically gives clearance to the Bill of Entry, as provided for in the 1st proviso to Section 47(1) of the Customs Act, 1962. This facility of automated clearance of Bills of Entry has been introduced on a pilot basis in Chennai Customs House and Jawaharlal Nehru Customs House w.e.f. 06.02.2020. The said facility was introduced at an all India level w.e.f. 05.03.2020.

[Refer Circular No.09/2019-Customs dated 28th February 2019, Circular No.05/2020-Customs dated 27th January 2020, Circular No.15/2020-Customs dated 28th February 2020]

4.3.4 Registration of Authorised Dealer Code, Bank Accounts through ICEGATE : CBIC has now enabled functionality within ICEGATE login which allows the exporters to make an online request for registration/modification of their AD Code / Bank Account(s) and also electronically submit the Passbook copy or Bank Authorisation letter through eSanchit. The exporters would also have access to a Dashboard to view the status of approval and acceptance at PFMS, for quick rectification at their end.

[Refer Circular No.32/2020-Customs dated 6th July 2020]

4.3.5 Automated debit of bond after Assessment: CBIC has done away with the requirement for importers to physically visit Customs House for physical debit of Bonds after the Bill of Entry is returned (to the importer) for the payment of duty. ICES now automatically debits the Bond and reflect the same in the first copy of the Bill of Entry, provided the details of the Bond are provided during submission of the Bill of Entry.

[Refer Circular No.32/2020-Customs dated 6th July 2020]

4.3.6 Simplified Registration of Importers/Exporters in ICEGATE: Simplified Registration module for importers / exporters based on verification provided in associated GSTIN has been provided without the requirement of digital signature. These functionalities are useful to the importers / exporters and would help them in their management of imports and exports. Some of these functionalities are Management of Bank Accounts, Ledger View, IGST Refund status, Query Reply etc.

[Refer Circular No.32/2020-Customs dated 6th July 2020]

4.3.7 Setting up of Turant Suvidha Kendra in All Customs Formations: Circular No.28/2020-Customs, dated 05.06.2020 provided for setting up Turant Suvidha Kendras (TSK) for the purpose of implementation of 1st Phase of Faceless Assessment at Bengaluru and Chennai. Considering the benefits ushered in by providing single point interface, Board decided to extend TSKs to all the Customs formations for carrying out the functions as follows:

(i) The document verification by Customs officers at Assessment and Customs Compliance Verification (CCV) stages would normally be based on the documents uploaded in the e-Sanchit, not requiring physical submission of documents. However, if in any exceptional situation the physical submission of documents is required by Customs, for defacement or validation, such submission would be made only at the TSKs.

(ii) Documents requiring verification during examination for validation with goods would continue to be done during examination, as at present.

(iii) One or more TSKs may be set up for the convenience of the trade.

(iv) Suitable procedures are to be devised for handling & safe keeping of the documents produced at TSKs. Ideally these documents should also be kept in electronic form

[Refer Circular No.32/2020-Customs dated 6th July 2020]

4.4 Paperless Customs: CBIC has taken initiatives to enable digital submission and transmission of both Bills of Entry and Shipping Bills in 2020. Besides saving time, the cost of printing paper documents has also been substantially reduced.

4.4.1 PDF copies of Bills of Entry and gatepass- Board has decided to enable electronic communication of PDF based Final eOoC (electronic Out of Charge) copy of BoE and eGatepass to the importers/Customs Brokers. This electronic communication would reduce interface between the Customs authorities and the importers/Customs Brokers and also do away with the requirement of taking bulky printouts from the Service Centre or maintenance of voluminous physical dockets in the Customs Houses. The Final eOoC copy of BoE and eGatepass copy is now emailed to the concerned Customs Broker and/or importer, if registered, once the Out of Charge is granted. The eGatepass copy will be used by the Gate Officer or the Custodian to allow physical exit of the imported goods from the Customs area. These new features have been implemented w.e.f 15.04.2020.

[Refer Circular No.19/2020-Customs dated 13.04.2020]

4.4.2 Electronic Communication of PDF Based Copies of Shipping Bill & e-Gatepass to Custom Brokers/Exporter: In its continuing endeavour to promote ‘Faceless, Contactless, Paperless Customs’ Board decided to rely upon digital copies of the Shipping Bill and do away with the requirement of taking bulky printouts from the Service Centre or maintenance of voluminous physical dockets in the Custom Houses. This reform will yield immense benefits in terms of saving the time and cost of compliance for the trade, thereby enhancing the ease of doing business, while providing enhanced security features for verification of authenticity and validity of the electronic document. Board has directed that w.e.f. 22.06.2020 only the digital copy of the Shipping Bill bearing the Final LEO would be electronically transmitted to the exporter and the present practice of printing copies of the said document for the exporters and also for maintaining a docket in the Customs House would stand discontinued.

[Refer Circular No.30/2020-Customs dated 22.06.2020]

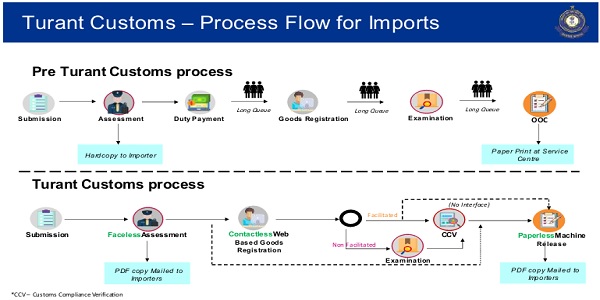

Diagrammatic Representation of Pre-Turant Customs and Post-Turant Customs process flow for Imports is illustrated in Figure 3.1, on the next page.

Figure 3.1: Process Flow for Imports- Pre and Post Turant Customs

5.Examination of goods:

5.1 The imported goods, which are interdicted for examination by the RMS, are required to be examined for verification of correctness of description/declaration given in the Bill of Entry and related documents. The imported goods may also be examined prior to assessment in cases where the importer does not have complete information with him at the time of import and requests for examination of the goods before assessing the duty liability or, where the proper officer, on reasonable belief feels that the goods should be examined before assessment, giving reasons for the same. Wherever required, samples are drawn in the examination area for chemical analysis, verification or any other purposes.

5.2 After assessment by the appraising group or for cases where examination is carried out before assessment, bill of entry needs to be presented for registration for examination of imported goods in the import shed. The proper officer of customs examines the goods along with requisite documents. The shipments, found in order are given clearance order by the proper officer of customs in the Import Shed.

5.3 Standard Examination Order: In order to enhance uniformity in assessments across various Customs ports across the Country Board introduced the RMS generated uniform examination orders for group 4 (Metal Products) from 5th September 2022 (part 1). In the first phase, the generation of uniform examination orders is for second check cases only and would be expanded to first check consignments in the 2nd Phase. Further, in part 2 under phase 1, the generation of uniform examination orders has also been implemented for group 5 (chapter 4) with effect from 15th September, 2022.

[Refer Circulars No.14/2021-Customs dated 07.07.2021, No.16/2022-Customs dated 29.08.2022 and No.23/2022-Customs dated 03.11.2022]

6. Execution of bonds:

6.1 For availing partial or complete exemption from duties under different schemes and notifications, execution of end use/ provisional duty bonds with Bank Guarantee or other surety may be required,in the prescribed forms. The amount of bond and bank guarantee is determined in terms of the instructions issued by the Board or conditions of the relevant notification or provisions of the Customs Act, 1962 or rules/regulations made there under.

7. Payment of duty:

7.1 The duty can be paid in the designated banks through TR-6 Challan. Facility of e- payment of duty through multiple banks is also available since 2007 at all major Customs locations.

7.2 With effect from 17-9-2012, e-payment of Customs duty is mandatory for importers registered under Accredited Clients Programme/Authorised Economic Operator scheme and importers paying duty of Rs. 1 lakh or more per Bill of Entry.

7.3 Customs Notification No. 134/2016-Customs (N.T) & 135/2016-Customs (N.T.) dated 2nd November, 2016 allowed Importers certified under Authorized Economic Operator Programme as AEO (Tier-Two) and AEO (Tier-Three) to make deferred payment of duty of Customs. The Deferred Payment of Import Duty Rules were notified vide Notification no. 28/2017- Customs (N.T.) dated 31st March, 2018

[Refer Circulars No.33/2011-Cus., dated 29-7-2011 and No. 24/2012-Cus., dated 5-9-2012, Circular No. 52/2016- Customs dated 15.11.2016]

7.4 Extension of Deferred Payment of Duty to ‘Authorised Public Undertakings’ (APU) : Vide Notification No. 78/2020-Customs (N.T.) dated 19.08.2020 ‘Authorised Public Undertakings’ (APU) have been permitted to avail the facility of deferred payment of Customs import duty under proviso to sub-section (1) of section 47 of the Customs Act, 1962.

[Refer Circular No.37/2020-Customs dated 19.08.2020]

8. Amendment of Bill of Entry:

8.1 Bonafide mistakes noticed after submission of documents, may be rectified by way of amendment to the Bill of Entry with the approval of Deputy/Assistant Commissioner. Levy of Fees (Customs Documents) Amendment Regulations, 2017, issued vide Notification No. 36/2017-Customs (N.T.) dated 11.04.2017, provides a number of amendments which can be allowed on payment of amount mentioned therein.

8.2 Request for amendments under Section 149 of the Customs Act, 1962 leading to reassessments: After introduction of Faceless Assessment, several representations have been received regarding dealing with amendments under section 149 of Customs Act,1962 and consequent reassessment of B/E, based on the request of the importers to change the elements of assessment. This is typically the case when the importer claims that he has forgotten to claim an exemption or is in possession of some document that requires an element such as freight etc. to be changed. The various scenarios and the prescribed routes for carrying out reassessment are laid down in para 2.5. of Circular No. 45/2020-Customs dated 12.10.2020.

[Refer Circular No.45/2020-Customs dated 12.10.2020]

9. Prior Entry for Bill of Entry:

9.1 For faster clearance of the goods, Section 46 of the Customs Act, 1962 allows filing of Bill of Entry prior to arrival of goods. This Bill of Entry is valid if vessel/aircraft carrying the goods arrives within 30 days from the date of presentation of Bill of Entry.

9.2 Often, goods coming by container ships are transferred at intermediate ports (like Colombo) from mother vessel to smaller vessels called feeder vessels. At the time of filing of advance Bill of Entry, the importer does not know which vessel will finally bring the goods to Indian port. In such cases, the name of mother vessel may be filled in on the basis of the Bill of Lading. On arrival of the feeder vessel, the Bill of Entry may be amended to mention names of both mother vessel and feeder vessel.

9.3 The Bill of Entry is required to be filed before the end of next day following the day (excluding holidays) on which the aircraft or vessel or vehicle carrying the goods arrives at a customs station at which such goods are to be cleared for home consumption or warehousing.

9.4 Wherein the Bill of Entry is not filed within the time specified in Para 8.3 above and the proper officer of customs is satisfied that there is no sufficient cause for such delay, the importer shall be liable to pay charges for the late presentation of Bill of Entry at the rate of rupees five thousand per day for initial three days of the default and at the rate of rupees ten thousand per day for each day of default thereafter.

[Refer Notification 26/2017-Cutoms (N.T.) dated 31.03.2017]

9.5 Section 46 of the Customs Act, 1962 has been amended vide the Finance Act, 2021. These changes facilitate pre-arrival processing and assessment of Bills of Entry (BE) by mandating their advance filing thus leading to significant decrease in the Customs clearance time. The amended Section 46 requires an importer to file a BE before the end of the day (including holidays) preceding the day of arrival of the vessel/aircraft/vehicle carrying the imported goods at a Customs port/station at which such goods are to be cleared for home consumption or warehousing. Board has amended the Bill of Entry (Electronic Integrated Declaration) Regulations, 2018 by issue of Notification No.34/2021-Customs(N.T.), dated 29.03.2021 thereby prescribing different time-limits for filing BE in respect of goods imported by various modes of transport. It may be noted that, the existing provision that a BE may be presented upto 30 days prior to the expected arrival of the aircraft or vessel or vehicle carrying the imported goods continues. Thus, with certain exceptions, as notified, the BE can now be filed anytime from 30 days prior to the expected arrival of the aircraft or vessel or vehicle upto the end of day preceding the day of such arrival.

[Refer Circular No. 08/2021-Cutoms dated 29.03.2021]

10. Bill of Entry for bond/warehousing:

10.1 A separate form of Bill of Entry is used for clearance of goods for warehousing. All documents, as are required to be filed with a Bill of Entry for home consumption are also required with the Bill of Entry for Warehousing which is assessed in the same manner and duty payable is determined. However, since duty is not required to be paid at the time of warehousing, the purpose of assessing the duty at this stage is only to secure the duty by way of execution of Bond. The duty is paid at the time of ex-bond clearance of goods for which an Ex-Bond Bill of Entry is filed. In terms of Section 15 of the Customs Act, 1962, the rate of duty applicable to imported goods cleared from a warehouse is the rate in- force on the date of filing of Ex-Bond Bill of Entry.

[Refer Circular no. 22/2016-Customs dated 31.05.2016]

11. Risk Management System in Indian Customs:

11.1 “Risk Management System” (RMS) is one of the most significant steps in the ongoing Business Process Re-engineering of the Customs Department. RMS is based on the realization that ever-increasing volumes and complexity of international supply chain and the deteriorating global security scenario present formidable challenges to Customs. Besides, the traditional gatekeeper approach of scrutinizing every document and examining every consignment will simply not work. Also, there is a need to reduce the dwell time of cargo at ports/airports, as well as the transaction costs in order to enhance the competitiveness of Indian businesses, by expediting the release of cargo where compliance level is high. Thus, an effective RMS strikes an optimal balance between facilitation and enforcement and promotes a culture of compliance. RMS is also expected to improve the management of the Department’s resources by enhancing efficiency and effectiveness in meeting stakeholder expectations and bringing the Customs processes at par with best international practices.

[Refer Circular No. 43/2005-Cus., dated 24-11-2005]

11.2 Facilitation of legitimate trade is one of the key motivating forces for simplification of procedures and reduction of barriers to the trade. Indian Customs has been at the forefront of taking initiatives aimed at catalysing economic development through transparency, harmonization, predictability and automation in trade. Risk management has been one of the key vehicles for Indian Customs to better meet the demands of the operating environment of the Trade facilitation. The risk management in its new avatar-an intelligence data driven risk management framework embedded with compliance culture-has enabled more effective decision-making at all levels. The past 15 years have produced many changes in implementation of risk management capabilities since its introduction in the year 2005 in imports. The technology stack, which is based on Oracle database remained the same, but the original port-wise distributed architecture was replaced by centralized architecture in the year 2010. Now, RMS for cargo clearance is functional for all the locations, which have the facility of electronic cargo clearance.

11.3 Indian Customs Risk Management System has already made forays into post-clearance audit, exports, container selection, IPR, integrated declaration and integrated risk management involving partner government agencies (single window), courier cargo, and e-sealing. With the insertion of proviso to Section 17 (2) of the Customs Act 1962 (vide Finance Act 2018), the selection for verification of self-assessed declarations (Bills of Entry or Shipping Bills) by the Assessing Officer shall primarily be on the basis of risk evaluation through appropriate selection criteria. Besides, provisos to Section 47 (1) and Section 51(1), the orders of clearance of imported goods for home consumption and goods for exportation respectively, in addition to the proper officer, may also be given electronically through the Customs Automation System on the basis of risk evaluation through appropriate selection criteria. This in turn paved way for machine release of goods through customs automation system in the case of imported and export goods.

11.4 Risk Management processes in Imports: Bills of Entry and IGMs filed electronically in ICES through the Service Centre or the ICEGATE are transmitted by ICES to the RMS. RMS processes the data through a series of steps and produces an electronic output for the ICES. This output determines whether a particular Bill of Entry will be taken-up for appraisement or examination or both or be cleared after payment of duty without assessment and examination. As a part of decision support, where necessary, RMS provides instructions for Appraising Officer, Examining Officer or the Out-of-Charge Officer. It needs to be noted that the appraising and examination instructions communicated by the RMS have to be necessarily followed by the proper officer. It is, however, possible that in a few cases the proper officer might decide to apply a particular treatment to the Bill of Entry which is at variance with the instruction received from the RMS. This may happen due to risks which are not factored in RMS. Such a course of action shall, however, be taken only with the prior approval of the jurisdictional Pr. Commissioner/Commissioner of Customs or an officer not below the rank of Additional / Joint Commissioner of Customs, authorized by him for this purpose, after recording the reasons for the same. A brief remark on the reasons and the particulars of Commissioner’s authorization should be made by the officer examining the goods in the departmental comments section of the electronic Bill of Entry in the EDI system.

11.5 Automated clearances of Bills of Entry : A further trade facilitation initiative in the Customs clearance process is the Customs Compliance Verification (CCV) which operates after an importer registers the imported goods even while duty has not been paid or its payment is in process. Once the goods are registered, the proper officer carries out all necessary verifications as per Sections 17/18 and Section 47(1) of the Customs Act, 1962. On satisfaction that the goods are ready for clearance, but for the payment of duties, the proper officer confirms the completion of the CCV for the particular Bill of Entry in the System. Thereafter, on payment of duty by the importer, the Customs Automated System electronically gives clearance to the Bill of Entry, as provided for in the 1st proviso to Section 47(1) of the Customs Act, 1962. This facility of automated clearance of Bills of Entry has been introduced on a pilot basis in Chennai Customs House and Jawaharlal Nehru Customs House w.e.f. 06.02.2020. The said facility was introduced at an all India level w.e.f. 05.03.2020.

[Refer Circular No.09/2019-Customs dated 28-02-2019, Circular No.05/2020-Customs dated 40

11.6 Post-Clearance Audit (PCA): Based on a set of criteria, bills of entry are selected for PCA under the Risk Management System for audit/verification of the correctness of the declaration/assessment of the bill of entry. The objective of PCA is to monitor, maintain and enhance compliance levels, while reducing the dwell time of cargo. The RMS selects the Bills of Entry for audit, after clearance of the goods, and these selected Bills of Entry are directed to audit officers for scrutiny.

11.7 As per the new scheme introduced in the Customs Act, 1962 (vide Finance Act, 2018), the endeavour is to audit the assessment and also to verify compliance of an auditee with the various provisions of the Customs Act and other allied laws in respect of imported or export or dutiable goods, as a means to measure and improve compliance. A new Section 99A (under Chapter XIIA) has been introduced in the Customs Act 1962, to provide a statutory framework for the procedure for conducting post clearance audit. The Customs Audit Regulations (CAR), 2018 framed under Section 99A of the Act are notified vide Notification No.45/2018-Customs (NT) dated 24.05.2018 in supersession of the On-site Post Clearance Audit regulations consequent to omission of Section 17(6) of the Act. Regulation (4) of the said CAR, 2018 stipulates that the selection of auditee or the selection of import declarations or export declarations, as the case may be, for the purposes of audit shall primarily be based on risk evaluation through appropriate selectivity criteria.

12. Risk Management processes in Exports:

12.1 Risk Management in export clearance was introduced in July 2013 (Circular No.23/2013-Customs dated 24.06.2013 refers). RMS in exports clearance has enabled low risk consignments to be cleared based on self-declaration by the exporters, while routing high-risky consignments to field officers for verification of self-declaration or examination of consignment or both. This has resulted in reduction in dwell time, transaction cost, clearance formalities without compromise with Custom controls and other regulatory compliances in respect of export of goods.

12.2 Shipping Bills filed electronically in ICES through the Service Centre or the ICEGATE are processed by RMS through a series of steps/corridors and an electronic output is produced for the ICES. This output from RMS determines the flow of the Shipping Bill in ICES i.e. whether the Shipping Bill will be taken up for verification of self-assessment/examination or both; or be given “Let Export Order” directly after payment of Export duty (if any) without any given verification of self-assessment/ examination.

12.3 To provide support in decision making and to ensure uniformity in verification practices adopted by customs officers, the RMS also provides suitable instructions for Assessing Officer and Examining Officer. Deviation or variance with RMS instructions as discussed under Para 10.4 in respect of import are also apply, mutatis mutandis, in export.

[Refer Para 5 of the Circular No.23/2013-Customs dated 24.06.2013]

12.4 The selection of Shipping Bills for verification of Self-assessment and/or examination is based on the output given by RMS to ICES. However, owing to some technical reasons if RMS fails to provide output to ICES or RMS output is not received by ICES , within a pre-defined time window, the existing norms of assessment and examination (Refer Para 10 of the Circular No.23/2013-Customs dated 24.06.2013) are applicable.

12.5 Pursuant to launch of RoDTEP (Remission of Duties or Taxes on Export Products) scheme on 01.01.2021, the phase-II of RMS in exports has been launched. Now subsequent to filing of EGM, the Shipping Bills having a claim of Duty Drawback or RoDTEP scheme are processed by RMS through a series of steps/corridors and an electronic output is generated for the ICES. This output determines the flow of the Shipping Bill in ICES i.e. whether the Shipping Bill will be taken up by the Customs Officers for verification of these claims or not, before grant of these export incentives to exporter. The RMS will select the Shipping Bills for audit, after issue of LEO, and these selected Shipping Bills will be directed to the audit officers for scrutiny.

13. Other RMS capabilities:

13.1 Data Analytics and Machine learning: Traditionally, Risk Rules are created by NCTC staff. Risk is assessed based on data analysis conducted through the use of various tools, as well as the analysis of legal changes, notifications, circulars. In order to leverage new technologies for automated analysis and targeting, machine learning based interdictions have been introduced in the RMS application. With the enhanced precision and accuracy in the interdiction of risky cargo, NCTC has successfully codified various descriptive fields and created data-based interdictions for automated identification of risky declarations through machine learning tools.

13.2 Express Cargo Clearance System (ECCS): ECCS is a web-based automated clearance System, which was launched in the year 2017, for risk based electronic clearance of express cargo, handled by courier companies. Currently, it is operational at three courier terminals viz Mumbai, Delhi, and Bengaluru. Customs declarations filed for clearance under ECCS are known as courier bills of entry (CBEs) and courier shipping bills (CSBs), and are different from the regular customs declarations, used for clearance of normal cargo. CBEs and CSBs filed for customs clearance under ECCS are subjected to RMS processes. RMS either facilitate or interdict a CBE or CSB as per risk parameters. Imported goods or export goods covered under CBEs or CSBs that are facilitated by RMS (no assessment and no examination) and cleared by customs Xray scanning shall be given out of charge or let export order, respectively. Under new initiatives of “auto out of charge” or “auto let export”, for fully facilitated CBE’s or CSEs are given automatic by ECCS System.

[Refer Circular No.40/2019-Customs dated 29.11.2019 and 41/2020-Customs dated 07.09.2020]

13.3 Container Selection Module (CSM): Non-Intrusive inspection (NII) is also an integral part of risk management ecosystem, wherein risk is assessed based on cargo declaration and risky containers are scanned to identify and mitigate risks related to concealment. Import General Manifests (IGMs), filed electronically, at a few selected locations, are processed by the RMS and an electronic output is produced, determining whether or not a container will be scanned by using NII equipment. By the end of 2020, CBIC has deployed 15 Container Scanners at 12 major port locations. After the linkage between Container Selection Module commonly known as “CSM” Application and Bill of Entry module of ICES has been established, a new feature is appearing as pop-up on the screen of OOC officers. The Docks Examiner and OOC Officer can see on their screen whether a container has been selected for scanning or not.

13.4 Logistics security- E-sealing of export containers: Board, in the year 2017, introduced e-sealing of self-sealed export containers replacing the existing procedure of supervised factory stuffing with one-time bottle seal. An e-seal is a sealing device, having an inbuilt unique Radio Frequency Identification (RFID) chip, which can be identified by chip readers. E-sealing has enhanced the supply chain security and cargo integrity of export containers, as it significantly reduces the possibility of any unlawful intrusion or replacement of cargo en-route to customs gateway port. NCTC-Cargo (former RMCC) has been entrusted with the overall management of the e-seal project, including the authorisation of vendors and e-sealing data management.

13.5 IPR Application: RMCC responsible for registration of intellectual property rights with Indian customs. These registered rights are protected by Indian Customs across all Customs stations. Based on set out parameters, RMS interdicts consignments that may be infringing the intellectual property rights of these registered right holders. In the year 2017, RMCC launched a new Web-based IPR Application (IPR::ICeR) for this registration. This Application provides for linkage with other sites, and also has provision for raising queries and replying to queries. UTRN (Unique Temporary Registration Number) function as user-id for access for amendments/query reply/sending infringement message, provision for registration under international agreements/protocols. The other facilities under new application include facility to the Right Holder to upload 20 images and features of genuine & fake products, amendment or renewal of UPRN (Unique Permanent Registration Number), sending infringement messages and to have access to bond Transactions.

13.6 Under Single Window initiative (SWIFT), import-related risks of PGAs, such as Central Drug Standard and Control Organisation (CDSCO), Food Safety and Standards Authority of India (FSSAI), Plant Quarantine (PQ), Animal Quarantine (AQ), and Wildlife Crime and Control Bureau (WCCB), are being gradually managed in the RMS application by adopting an integrated risk management approach. A risk-based selection of Bills of Entry for four PGAs namely FSSAI, WCCB, PQ, and CDSCO has already been implemented.

14 National Risk Management Committee (NRMC):

14.1 Risk Management is a dynamic process. Risk Management policies and processes need to be continually monitored and reviewed at a senior level. Board had constituted the NRMC vide Circular No.23/2007-Customs dated 28.06.2007, with a mandate to review the functioning of, and supervise the implementation of, Risk Management System (RMS). Risk Management Division (RMD), renamed as NCTC-Cargo has been assigned the task of convening the meetings of NRMC. The NRMC was expected to meet at least once every quarter; however, at its 4th meeting held in February 2014 at Mumbai, the Committee formally decided to meet annually.

14.2 Initially, DG (Systems) was designated as the head of the NRMC, and representatives of various Directorates viz. Directorate of Revenue Intelligence, Valuation, Audit, and Trade Facilitation and Tax Research Unit, were nominated as its members. Joint Secretary (Customs) was included as a member of the Committee vide circular 39/2011-Customs dated 2-9-2011. Consequent upon the transfer of operational control of RMD from DG Systems to DG DRI in April 2013, the NRMC was headed by DG DRI. RMCC (now NCTC) is placed under Directorate General of Analytics and Risk Management (DGARM) vide OM No. A-11013/19/2017-Ad.IV dated 11.07.17.

14.3 There shall be established a National Risk Management Committee for Customs and GST. The DGARM, Delhi will be the nodal agency responsible for convening the NRMC meeting to review the functioning of the NCTC-Cargo, NCTC(Pax) and the GST Business Analytics Wing. These wings under the DGARM will supervise the implementation and enhancement of RMS, APIS and the DGARM applications and provide feedback for improving the effectiveness of risk management and all related aspects. The NRMC will be a Standing Committee with the Member (Investigation), CBIC, as Chairman and Additional Director General, DGARM Hars, Delhi will the Member Secretary of the NRMC.

14.4 The NRMC shall be convened once every year and will have the following main (but not limited to) functions:

(i) Review the effectiveness of existing Risk Parameters employed in various modules namely Import, Export, container Scanning, Express Cargo Clearance System (ECCS), Post Clearance Audit (PCA), Protection and enforcement of Intellectual Property Rights (IPR) etc., and Risks posed by changes in Modus Operandi, new exemption notifications and new CCR’s.

(ii) Review existing parameters and suggest new parameters to address concerns on border and port security.

(iii) Once NCTC(Pax) is operationalized, the NRMC shall look at incremental improvements to be made in the Automated Targeting System.

(iv) he Business Analytics wing of GST implements various modules e.g., Risky Exporters, Risky Taxpayers, Scrutiny of Returns, Audit, Analytical reports etc. The NRMC will advise on changes, if any, to be made in the various risk criteria that define the Risk in these modules.

(v) Deliberate and advise on new and emerging risks and suggest ways to address systemic risks, having cross-cutting implications.

(vi) Discuss new initiatives and projects for stepping up risk management strategy and associated processes, including the development of new modules and deployment of new technologies.

(vii) Be the Forum for giving feedback and suggestions on improving the efficacy of risk management.

(viii) Discuss and recommend measures for timely and effective risk mitigation by field formations.

(ix) Deliberate on economic trends, changes in policies, duty rates and exemptions, etc., that could be exploited by the trade to evade Duties and Prohibitions and suggest remedial action for the same.

(x) Discuss the efficacy of the Examination orders that would be made available shortly through the ICETAB, obviating the need for printing in the paper.

(xi) Have an oversight on the generation of the centralised examination orders based on various parameters and its rollout in phases to enhance uniformity.

(xii) To discuss and advise on enhanced use of technology, data sources and analytics capabilities to discern Security related Risks. Deliberate on use of Al/ML, Image analytics, geospatial analysis etc

(xiii) To address security vulnerabilities in the International Supply Chain through entity profiling of stakeholders, leveraging information in databases about movement of vessels and containers etc.

(xiv) Any other matter that DGARM may consider for seeking the views of the NRMC. [Refer Instruction No. 3/2022-Customs dated 23-03-2022]

15. Local Risk Management (LRM) Committee:

15.1 A Local Risk Management (LRM) Committee headed by Commissioner of Customs has been constituted in each Custom House / Air Cargo Complex / ICD, where RMS is operationalised. The LRM Committee comprises the Additional / Joint Commissioner in charge of Special Investigation and Intelligence Branch (SIIB), who is designated as the Local Risk Manager and includes the Additional / Joint Commissioner in charge of Audit and a nominee, not below the rank of a Deputy Director from the regional / zonal unit of the DRI, and a nominee, not below the rank of Deputy Director from the Directorate of Valuation, if any. The LRM Committee meets once every month and some of its functions are as follows:

(i) Review trends in imports of major commodities and valuation with a view to identifying risk indicators,

(ii) Decide the interventions at the local level, both for assessment and examination of goods prior to clearance and for PCA.

(iii) Review results of interventions already in place and decide on their continuation/ modification or discontinuance etc.

(iv)Review performance of the RMS and evaluate the results of the action taken on the basis of the RMS output.

(v) Send periodic reports to the NCTC with the approval of the Pr. Commissioner/Commissioner of Customs. [Refer Circular No.43/2005-Cus., dated 24-11-2005]

16. Authorized Economic Operator scheme:

16.1 The earlier Accredited Clients Programme (ACP)/Authorized Economic Operator (AEO) scheme granted assured facilitation to importers who have demonstrated capacity and willingness to comply with the laws administered by the Customs. The earlier existing ACP and AEO programmes were merged into the new AEO programme vide Circular No. 33/2016-Customs dated 22-7-2016. For the economic operators other than importers and the exporters, the new programme offers only one tier of certification (i.e. AEO-LO) whereas for the importers and the exporters, there are three tiers of certification (i.e. AEOT1, AEO-T2 and AEO-T3).

16.2 Considering the likely volume of cargo imported by the Authorized Economic Operator, Custom Houses are advised to create separately earmarked facility/counters for providing Customs clearance service to them. Commissioners of Customs are also required to work with the Custodians for earmarking separate storage space, handling facility and expeditious clearance procedures for these clients.

16.3 The RMD maintains the list of AEOs centrally in the RMS and also monitors their levels of compliance, in co-ordination with the DRI/Commissioners of Customs. Where compliance levels fall, the importer is at first informed for self-improvement and in case of persistent non-compliance, the importer may be deregistered under the AEO.

16.4 The new combined three tier AEO programme enhance the scope of these programmes so as to provide further benefits to the entities who have demonstrated strong internal control system and willingness to comply with the laws administered by the Central Board of Indirect Taxes and Customs. Benefits besides lowered risk ratings on RMS includes simplified Customs procedure, declarations, etc. besides faster Customs clearance of consignments of/for AEO status holders The features and details of the revised programme are available in CBIC Circular No. 33/2016-Customs dated 22-7-2016

[Refer Circular No. 33/2016-Customs dated 22-7-2016, No.03/2018-Customs dated 17.01.2018 and No.26/2018-Customs dated 10.08.2018. For more details, please refer Chapter 34.]

17. Export procedure – Shipping Bill:

17.1 For clearance of export goods, the exporter has to obtain an Importer- Export Code (IEC) number from the DGFT prior to filing of Shipping Bill. Under the EDI System, IEC number is received online by the Customs System from the DGFT. The exporter is also required to register authorized foreign exchange dealer code (through which export proceeds are expected to be realized) and open a current account in the designated bank for credit of Drawback incentive, if any.

17.2 All the exporters intending to export under the export promotion scheme need to get their licenses etc. registered at the Customs Station. For such registration, original documents are required.

17.3 eSANCHIT has been extended to all ICES locations on PAN India basis for all types of exports under ICES.

[Refer Circular No. 29/2018- Customs dated 30.08.2018, Circular 43/2018- Customs dated 08.11. 2018]

18. Waiver of Guaranteed Remittance (GR) form:

18.1 Generally the processing of Shipping Bills requires the production of a GR form that is used to monitor the foreign exchange remittance in respect of the export goods. However, there are few exceptions when the GR form is not required. These exceptions include export of goods valued not more than US $25,000/- and export of gifts valued upto Rs.5 lakhs.

[Refer RBI Notifications No.FEMA.23/2000-RB, dated 3-5-2000, and No.FEMA.116/2004-RB, dated 25-3-2004]

19. Arrival of export goods at docks:

19.1 The goods brought for the purpose of export are allowed entry to the customs area on the strength of the check list and other declarations filed by the exporter in the Service Center. The custodian has to endorse the quantity of goods actually received on the reverse of the check list.

20. Customs examination of export goods:

20.1 After the receipt of the goods in the customs area, the exporter/ customs broker may contact the Customs Officer designated for the purpose, and present the check list with the endorsement of custodian and other declarations along with all original documents such as, Invoice and Packing list, ARE-1, etc. The Customs Officer may verify the packages of the goods actually received and enter the same into the system and thereafter mark the Electronic Shipping Bill, handing over all original documents to the Dock Appraiser who assigns a Customs Officer to carry out examination of goods, if required under the Risk management System and indicate the officers’ name and the packages to be examined, if any, on the check list and return it to the exporter/ Customs Broker.

21. Examination norms:

21.1 The Board has been fixing norms for examination of export consignments and such norms depend upon the quantum of incentive, value of export goods, country of destination etc. The instructions under the Risk Management System and examination order by the Appraising Groups follow the norms framed in this regard.

21.2 After presentation of goods for registration to Customs and determination of action as to whether or not to examine the goods, no amendments request in the normal course should be entertained. However, in case an exporter still wishes to change any of the critical parameters resulting in change of value, Drawback, port etc. such consignment should be subjected to examination to rule out malafide in the request of the exporter.

21.3 Notwithstanding the examination norms, any export consignment can be examined by the Customs (even up to 100%), if there is any specific intelligence in respect of such consignment. Further, to test the compliance by trade, once in three months a higher percentage of consignments (say for example, all the first 50 consignments or a batch of consecutive 100 consignments presented for examination in a particular day) would be taken up for examination. Out of the consignments selected for examination a minimum of two packages with a maximum of 5% of packages (subject to a maximum of 20 packages) would be taken up for checking/examination.

21.4 In case export goods are stuffed and sealed in the presence of Customs/Central Excise officers at the factory of manufacture/ICD/CFS/warehouse and any other place where the Commissioner has, by a special order, permitted, it may be ensured that the containers should be bottle sealed or lead sealed. Also, such consignments shall be accompanied by an examination report in the prescribed form. In case of export through bonded trucks, the truck should be similarly bottle sealed or lead sealed. In case of export by ordinary truck/other means, all the packages are required to be lead sealed.

[Refer Circulars No.6/2002-Cus., dated 23-1-2002, and No.1/2009-Cus., dated 13-1-2009]

21.5 Routine examination of perishable export cargo is not to be conducted. Customs resort to examination of such cargo only on the basis of credible intelligence or information and with prior permission of the concerned Assistant Commissioner/ Deputy Commissioner. Further, the perishable cargo which is taken up for examination should be given Customs clearance on the day itself, unless there is contravention of Customs laws.

[Refer Circular No.8/2007-Cus., dated 22-1-2007]

22. Drawl and testing of samples:

22.1 The representative sample from the consignment is drawn in accordance with the orders of the proper officer.

22.2 If considered necessary, the Assistant / Deputy Commissioner, may order sample to be drawn for purposes other than testing such as for visual inspection and verification of description, market value inquiry, etc.

22.3 Request for re-testing of sample made within a specified time by the importer or agent may be granted by the Additional Commissioner or Joint Commissioner of Customs as a trade facilitation measure. For uniformity in procedure at the various field formations, Board has issued detailed guidelines for retesting of samples.

[Refer Circular No. 30/2017-Customs dated 18.07.2017]

22.4 CRCL Module – Forwarding of samples using electronic Test Memo to CRCL and other Revenue Laboratories : As detailed in Circular No.46/2020-Customs dated 15.10.2020, CRCL and other Revenue Laboratories have been upgraded with several new, state of the art equipment, thereby enabling the testing of a wider variety of commodities in lesser time, with greater accuracy. For details, the CRCL brochure available at .in may be perused. In order to further ease the testing process, DG Systems has enabled a ‘CRCL module’ in ICES with the objective of automating all paperwork related to sampling, forwarding of test memos to CRCL and other Revenue Laboratories, and electronic receipt of test reports, instantly by the Customs Officers. The officials of CRCL and other Revenue Laboratories have been provided access for both import and export functionalities in the CRCL module. The CRCL module is also seamlessly integrated with current modules of ICES.

[Refer Circular No.46/2020-Customs dated 15.10.2020 and Instruction No.14/2021-Customs dated 21.06.2021]

22.5 For list of identified laboratories where field formations may directly forward samples of certain goods where CRCL labs are not equipped, refer Circulars No.43/2017- Customs dated 16.11.2017, No.11/2018-Customs dated 17.05.2018, No.28/2018-Customs dated 30.08.2018 and No.15/2019-Customs dated 07.06.2019.

23. Stuffing / loading of goods in containers:

23.1 In case of container cargo, the stuffing of container at Dock is done under Preventive supervision. Further, loading of both containerized and bulk cargo is to be done under Preventive supervision. The Customs Preventive Officer supervising the loading of container and general cargo into the vessel may give “Shipped on Board” endorsement on the Exporters copy of the Shipping Bill.

23.2 Palletization of cargo is done after grant of Let Export Order (LEO). Thus, there is no need for a separate permission for palletization from Customs. However, the permission for loading in the aircraft/vessel is to be obtained.

. [Refer Circular No.18/2005-Cus., dated 11-3-2005]

24. Amendments:

24.1 Any correction/amendment in the check list generated after filing of declaration can be made at the Service Centre provided the documents have not yet been submitted in the EDI system and the Shipping Bill number has not been generated. Where corrections are required to be made after the generation of the Shipping Bill number or after the goods have been brought into the Export Dock, the amendments will be carried out in the following manner:

(i) If the goods have not yet been allowed “Let Export” the amendments may be permitted by the Assistant / Deputy Commissioner (Exports).

(ii) Where the “Let Export” order has already been given, amendments may be permitted only by the Additional/Joint Commissioner in charge of Export.

24.2 In both the cases, after the permission for amendments has been granted, the Assistant Commissioner/Deputy Commissioner (Export) may approve the amendments on the EDI system on behalf of the Additional/Joint Commissioner. Where the print out of the Shipping Bill has already been generated, the exporter may first surrender all copies of the Shipping Bill to the Dock/Shed Appraiser/Superintendent for cancellation before amendment is approved on the system. [Refer para 6 in Chapter 2 on types of Amendments]

Drawback claim:

25.1 After actual export of the goods, the Drawback claim is automatically processed through EDI system by the officers of Drawback Branch on first-come-first-served basis. The status of the Shipping Bills and sanction of Drawback claim can be ascertained from the query counter set up at the Service Center. If any query is raised or deficiency noticed, the same is also shown on the terminal and a print out thereof may be obtained by the authorized person of the exporter from the Service Centre. The exporters are required to reply to such queries through the Service Centre. The claim will come in queue of the EDI system only after reply to queries/deficiencies is entered in the Service Centre.

25.2 All the claims sanctioned on a particular day are enumerated in a scroll and transferred to the Bank through the system. The bank credits the drawback amount in the respective accounts of the exporters. The bank may send a fortnightly statement to the exporters of such credits made in their accounts.

25.3 The Steamer Agent/Shipping Line may transfer electronically the EGM to the Customs EDI system so that the physical export of the goods is confirmed, to enable the Customs to sanction the Drawback claims.

[ For more details on duty drawback Scheme, please refer Chapter 22]

26. Export General Manifest:

26.1 All the shipping lines/agents need to furnish the Export General Manifests, Shipping Bill-wise, to the Customs electronically before departure of the conveyance.

26.2 Apart from lodging the EGM electronically the shipping lines need to continue to file manual EGMs along with the exporter copy of the Shipping Bills in the Export Department where they would be entered in a register. The shipping lines may obtain acknowledgement indicating the date and time at which the EGMs were received by the Export Department.

27. Electronic Declarations for Bills of Entry and Shipping Bills:

27.1 Bill of Entry (Electronic Integrated Declaration and paperless processing) Regulations, 2018 and Shipping Bill (Electronic Integrated Declaration and paperless processing) Regulations, 2019 as amended, have been framed in exercise of powers conferred under section 157 read with section 46 and section 50 of the Customs Act, 1962 to mandate self-assessment by the importer or exporter, as the case may be.

[Refer Notifications No.36/2018-Cus (N.T.) dated 11-05-2018 and No.33/2019-Cus (N.T.) dated 25-04-2019]

28. 24×7 Customs clearance facility:

28.1 With effect from 31.12.2014 the facility of 24×7 Customs clearance had been made available for specified import viz. goods covered by “facilitated” Bills of Entry and specified exports viz. factory stuffed containers and goods exported under free Shipping Bills, at the 18 sea ports and the facility of 24×7 Customs clearance for specified imports viz. goods covered by facilitated Bills of Entry and all exports viz. goods covered by all Shipping Bills had also been made available at the 17 air cargo complexes (ACCs). Lately, it has been decided to extend the facility of 24×7 Customs clearance for specified imports viz. goods covered by facilitated Bills of Entry and specified exports viz. reefer containers with perishable/temperature sensitive export goods sealed in the presence of Customs officials as per Circular no. 13/2018-Cus. Dated 30.05.2018 and goods exported under free Shipping Bills. Presently 24×7 Customs clearance facility is available at 20 sea ports and 17 Air Cargo Complexes.

[Refer Circulars No.19/2014- Cus. dated 31-12-2014, 01/2016 dated 06.01.2016,31/2018 dated 05.09.2018 and ]

28.2 Board had advised all the Pr. Chief / Chief Commissioners, having jurisdictions over Inland Container Depots (ICDs) to consider having the ICDs within their jurisdictions designated with extended facility of Customs clearance beyond normal working hours in any of the following ways, namely :-

a) The facility of Customs clearance may be made available on a 24×7 basis, similar to the current Board guidelines for Sea Ports and Air Cargos/Airports;

b) The facility of Customs clearance may be extended on all seven (7) days of the week (including holidays), with stipulated timings (say from 9 :30 AM to 6 :00 PM);

c)The facility of Customs clearance may be extended beyond normal working hours for specified days in a week and with specified timings.

The decision to designate an ICD in any manner under para 3(a), 3 (b) or 3(c) above, based on location requirement and resources availability, could be for specified imports viz. goods covered by ‘facilitated’ Bills of Entry only, or specified exports viz. reefer containers with perishable/ temperature sensitive export goods sealed in the presence of Customs officials only or goods exported under free Shipping Bills only, or for all the three categories mentioned

[Refer Circular No. 11/2022-Customs dated 29.07.2022]

29.Sealing of Export Goods: electronic sealing facility

29.1 Board has laid down a simplified procedure for stuffing and sealing of export goods by introducing self-sealing subject to certain conditions.

29.2 Exporter shall inform the details of the premises whether a factory or a warehouse or any other place where container stuffing is to be carried out to the jurisdictional officer at least 15 days before first planned movement of a consignment from his factory premises for consideration of grant of permission by the jurisdictional Commissioner.

29.3 Customs formation granting the self sealing permission shall circulate the permission along with GSTIN of the exporter to all Customs Houses/Station concerned. Principal Commissioners/ Commissioners would also communicate to RMD the IEC of the exporters newly granted permission for self-sealing; exporters already operating under self-sealing procedure, exporters permitted factory stuffing facility, AEOs.

29.4 Exporter shall seal container with tamper-proof electronic seal of standard specification before leaving the premises. The physical serial number of the electronic seal shall be declared by the exporter at the time of filing integrated online Shipping Bill. Prior to sealing the container, exporter shall feed data such as name of exporter, IEC, GSTIN, description of goods, tax invoice number, name of authorized signatory (for affixing the e-seal) and Shipping number in the electronic seal.

29.5 Exporter shall procure the RFID seals from vendors conforming to the standards specified by the Board.

29.6 All consignments in self-seal containers shall be subject to risk-based criteria and intelligence, if any, for inspection/ examination at the port of export. At the port/ ICD, Customs officers would verify the integrity of the seals to check for any sign of tampering enroute.

[Refer Circular no. 26/2017- Customs dated 01.07.2017, Circular no. 36/2017- Customs dated 28.08.2017, Circular no. 37/2017- Customs dated 20.09.2017, Circular no. 41/2017- Customs dated 30.10.2017, Circular no. 44/2017- Customs dated 18.11.2017, Circular no. 51/2017-Customs dated 21.12.2017]

Source – Custom Duty Manual 2023

VERY USEFUL AND HIGHLY INFORMATIVE