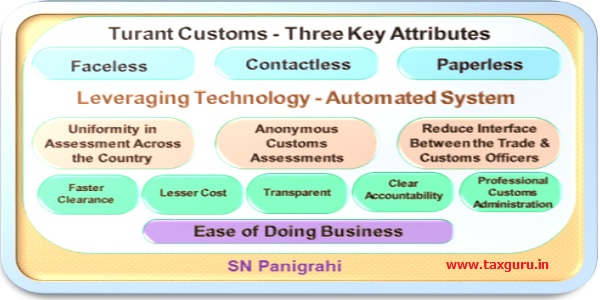

Trade Facilitation is a key enabler for simplification of procedures and reduction of barriers to the trade. The major Objective of Trade Facilitation is to Reduce Time and Cost for the EXIM community and help them become more competitive in the International Arena. In line with this momentum, CBIC has implemented next generation reforms through Turant Customs, strongly enabled by technology. The Components of the program are characterized by Three Key Attributes i.e. a Faceless, Contactless and Paperless Customs clearance processes. It is being rolled out in phases and is scheduled to cover the entire country. In this article we shall discuss on the Topic – Faceless Assessment.

Faceless Assessment is an IT-driven reform – a giant leap forward to Leverage Technology aimed to streamline trade processes for Faster Customs Clearance of Imported Goods at Lesser Cost to the Trade, Transparent Decision Making, Efficient and instill Accountability and Enable Professional Customs Administration Leading to Enhanced Ease of Doing Business.

Faceless Assessment enables an assessing officer, who is physically located in a particular jurisdiction, to assess a Bill of Entry pertaining to imports made at a different Customs station, whenever such a Bill of Entry has been assigned to him through an Automated System. This would enable uniform, anonymous Customs assessments and reduce interface between the Trade and Customs officers. Anonymity in assessment is a core feature of the Faceless Assessment initiative. This is aimed to reduce / eliminating the unnecessary need of a face to face interaction with a Customs official and providing uniformity in assessment across the country. Importers will now get their goods cleared from Customs after a faceless assessment is done remotely by the Customs officers located outside the port of import of Different Jurisdiction.

Objectives of Faceless Assessment

Faceless Assessment (also referred to as Virtual Assessment or Anonymised Assessment) uses a technology platform to separate the Customs assessment process from the physical location of a Customs officer at the port of arrival. This measure will bolster efforts to ensure an objective, free, fair and just assessment.

Key objectives of Faceless Assessment include:

> Anonymity in assessment for reduced physical interface between trade and Customs

> Speedier Customs clearances through efficient utilisation of manpower

> Greater uniformity of assessment across locations

> Promoting sector specific and functional specialisation in assessment

It is estimated that the Faceless Assessment initiative will help slash release time to only few minutes and few hours, substantially lower than the present clearance times averaging three to four days. Accordingly, Faceless Assessment is expected to have considerable impact on India’s performance on various independent global assessments and boost the country’s trade competitiveness, including ease of doing business

Faceless Assessment – Extended Across all Customs Ports in India

After running pilot programmes since August 2019, the first formal phase of Faceless Assessment commenced in Bengaluru and Chennai in June 2020 and is found successful. It primarily focused on cargo under Chapters 84 and 85 of the Customs Tariff Act, 1975. These Pilot Programmes helped test Faceless Assessment first in the same zone, then across zones. This was followed by other phases covering new Customs locations and new items of import. Post validation of the expected outcomes, it has been decided to roll out the programme nationally and now being extended across all Customs Ports in India to usher a more modern, efficient, and professional Customs administration, with resultant benefits for trade and industry.

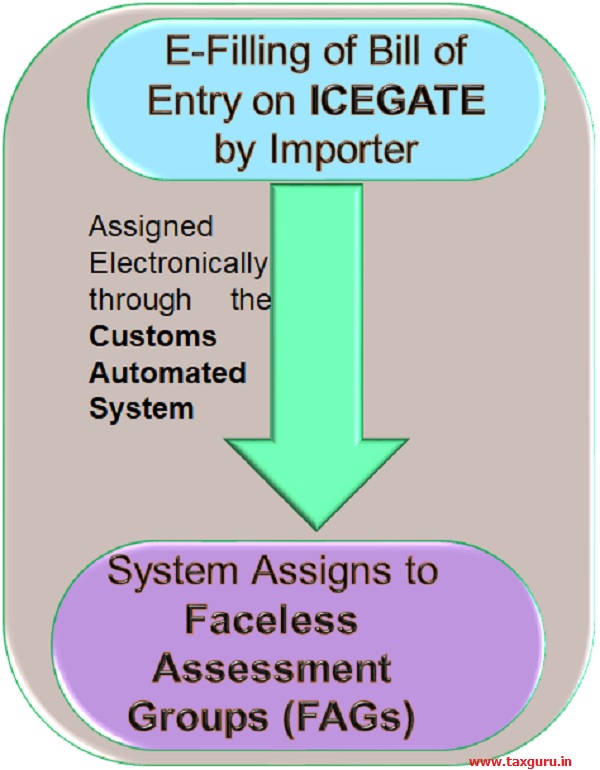

Faceless Assessment is based on the Customs Automated System assigning a Bill of Entry (BE) that is identified for scrutiny (non-facilitated BE) to an assessing officer, who is physically located at a Customs station, which is not the port of import.

Present Local Assessment Practices

It was seen that despite a centralized automated IT framework for carrying out Customs assessment, the varying assessment structures in the Zones were not compatible with the CBIC’s mission of having uniform and standardized Customs assessment practices. Moreover, as the assessment was being done in the port of import itself, local assessment practices would invariably creep in, despite all attempts at standardization. The different structures were also found to contribute to differences in dwell time of cargo, thereby bringing down the overall efficiency. Thus, it was clear that a fundamental change is warranted to meet the objective of the CBIC in providing a most efficient, transparent and standardized Customs assessment experience.

New Customs Assessment – a Fundamental Change in Structure

The new Customs assessment structure moves away from the physical constraint of assessment by local Customs officers at the Port of Import. It redefines the roles of Customs officers for assessment, examination and other related processes along with changes in ICES and creates a superstructure of Faceless Assessment Groups (FAGs), Port Assessment Group (PAG), National Assessment Centres (NACs) and Turant Suvidha Kendras (TSKs). The new dispensation virtually connects Customs assessment officers from different jurisdictions and provides for enhanced level monitoring of Customs assessments based on assignment of import clearance documents by the Customs Automated System (CAS) to officers of the FAGs irrespective of the port of import of the goods.

Functions of the FAGs

With the introduction of Faceless Assessment System, the assessment part of the Customs clearance procedure would be delinked with the geographical location where the goods are available for examination and instead be executed by the FAG. Each FAG would have an all India jurisdiction There is no territorial jurisdiction assigned to FAG. Each FAG would have jurisdiction over the Bills of Entry assigned in the system to FAG, irrespective of the same being filed anywhere in India.

In the previous system the assessment would queue in the system to an official in the same territorial jurisdiction of the cargo. Now, an algorithm decides where it would go for assessment thus bringing anonymity.

The functions of the FAGs will include:

> As is the present practice, may accept the self-assessment or re-assessment of the BE and pass a speaking order3 (unless acceptance is confirmed in writing).

> Providing importers an opportunity of hearing through Query or via video conferencing in case the importer before proceeding with the re-assessment.

> Assessing any BE assigned to them by the Customs Automated System, irrespective of the port where the goods have arrived.

> With the introduction of FAG, the assessment part of the Customs clearance procedure would be delinked with the geographical location where the goods are available for examination.

> The presence of FAG in a Zone is decided based on the import commodities profile of Customs location, quantum of BEs and availability of officers at DC/AC and Appraiser/ Superintendent level.

> The Principal Chief Commissioners/ Chief Commissioners of Customs may decide on the total number of officers to be placed in each FAG based on the volume of BEs for their respective zones.

Procedure for Verification of Assessment by FAG:

From an importer’s perspective, there will be no changes to the process of filing a BE. He/ she will continue to file his/ her documentation including BE and supporting documents4 on the ICEGATE portal.

Procedure

i. Customs Automated System will assign the BE to a FAG based on an inbuilt logic considering tariff entries in terms of either duty payable or highest assessable value, in that order.

ii. FAG will assess the BE for purposes of duty determination and compliance to restrictions. Accordingly, it may opt to:

a. assess and verify BE basis documents available in e-Sanchit

b. seek additional information or documents

c. identify BE for examination or testing

iii. In cases where the FAG seeks additional information, communication to and from the importer shall be managed electronically through the system (ICEGATE).

iv. On the basis of evaluation and clarification (if any), the FAG may either accept or re-assess the BE. While re-assessing the BE, it may be ensured that the representation from the importer by way of query may be taken into account. The importer can if he desires waive this requirement.

v. When the FAG re-assesses the BE and an importer disputes such re-assessment, the FAG shall issue a speaking order.

vii. While accepting the self-assessment or re-assessing the BE, the FAG may provide instructions for 2nd check examination of goods along with directions to shed officers at the Port of Import.

vii. Illustratively, instructions may include verification of originals, defacement of documents, taking custody of certain documents, seeking NoC from PGAs (Participating Government Agency) etc.

viii. Where authenticity of a document is in doubt and verification by an external agency is required, the same shall be communicated to shed officers at the Port of Import, for necessary action.

ix. Requests for storage of imported goods in warehouse pending clearance or removal6 shall be processed via the TSK.

x. Any assessment / speaking order passed by FAG, shall be appealable to the Commissioner of Customs (Appeals) at the Port of Import.

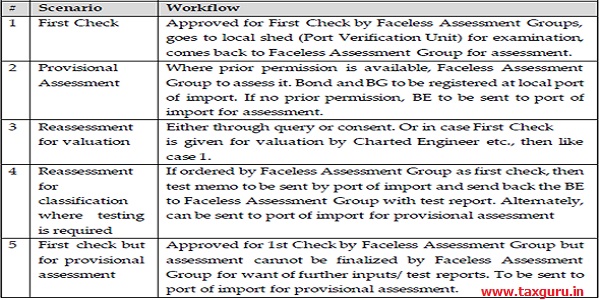

Workflow for BE under Faceless Assessment

Workflow for Self –Assessment & Re-Assessment

Workflow for 1st Check & Provisional Assessment

–

Key Considerations for Faceless Assessment

The Nodal Commissioners in the NAC shall co-ordinate to ensure that Faceless Assessment is implemented smoothly and creates no disruption in the assessment and clearance of goods. The following measures may be undertaken by the NAC:

Identification of Location of FAG

i. NACs have identified Customs locations within each Zone, where Faceless Assessment pertaining to a group would be undertaken. The volume of import and availability and experience of officers was considered for this purpose.

ii. It is critical to note that setting up adequate number of FAGs in a zone with sufficient number of officers is one key area which will enable faster disposal and more timely assessment

Uniform Assessment Practices

i. Consider audit objections, judicial and quasi-judicial decisions accepted by the Department relating to the assessment of the goods to be handled by the FAG under the concerned NAC and circulate among the officers

ii. Identify variations, if any, in assessment practices and harmonise them for application across FAGs for uniformity of assessment.

iii. Ensure that imported items are properly declared along with full details to ensure proper classification and eligibility for notification benefit.

iv. Keep track of all instances where the description is falling short of requirement and report the same in a monthly bulletin for the benefit of importers and customs brokers.

v. Study present assessment practice concerning major commodities in the Groups being imported at customs station and being assessed by them.

vi. Ensure uniformity in classification, valuation, exemption benefits, and compliance with import policy conditions

vii. Endeavour to reduce incidence of queries and issue public/ trade notices from time to time to sensitise trade on good practices required to reduce incidence of queries. For e.g. sensitizing trade to provide complete details and description of a commodity such as brand name, model and any other specifications essential for the assessment

viii. FAG officers shall make use of WCO explanatory notes, Classification decisions, Classification opinions available on WCO website.

ix. Maintain valuation circulars issued by DGOV regarding goods covered under the Groups and ensure valuation is in line with issued alerts.

x. Access to the National Import Data Base (NIDB) should be taken by FAG officers and they may resort to verification of valuation and classification of an imported product in the National import database.

xi. List demands raised u/s 28 against an importer by DRI or other agency (apart from audit objections on classification, exceptions etc.) relating to goods covered under the group during the last 5 years and ensure that the assessment is done after considering the precedents contained in the said cases/ audit objections.

xii. RMS instructions may be complied with.

xiii. Whenever RMS instructions are not related to imported goods in a BE, same shall be recorded and shared with Commissioner on a daily basis.

Grievances Redressal

For system related issues, first point continues to be ICEGATE Helpdesk (https://www.icegate.gov.in/contact_us.html). For other issues, every Port of Import has to set up Turant Suvidha Kendra to redress grievances related to delay in clearances including Faceless Assessment. The contact details are available in https://www.cbic.gov.in/htdocs-cbec/enquiry-points. Further, an officer at the rank of Additional Commissioner/ Joint Commissioner is also designated at each port to take care of timely redressal of grievances and escalation.

Functions of Turant Suvidha Kendra

Turant Suvidha Kendras at the Port of Import will be responsible for all documentary processes requiring physical submission / verification at the Port of Import.

Illustratively, their functions include:

> Accept bonds or Bank Guarantee;

> Carry out any other verifications that may be referred by FAGs;

> Defacing of documents/ permits licenses, wherever required;

> Debit of documents/ permits/ licenses, wherever required;

> Handle queries related to assessment; and

> Other functions determined by Commissioner to facilitate trade

Conclusion

CBIC has initiated many innovations in recent times (facilitating measures of course out of compulsions due to COVID -19) aimed at reducing physical interactions between trade and customs and paper less transactions & customs clearances (e-Sanchit & Faceless Assessment) increase objectivity, freedom and fairness of the assessment process in addition to enhancing quality of assessments and inducing greater efficiency and transparency.

The phased roll out of faceless e-assessment in particular is a welcome initiative in the Direction of Ease of Doing Business, as it obviates the physical interface between the importer and customs authorities. Assessing officers physically located in a particular jurisdiction will assess bills of entry of imports of a different customs station or port, which will be assigned to them through an automatic system. The processing will be done without any direct interaction between the importer and Customs authorities, thereby, significantly reducing the cargo clearance time and transaction cost and also expected to reduce disputes and ensure uniformity in assessment.

Comments

Though introduced with Good Intension, Contrary to the General Expectations, the Real Experience proving other way with extensive delays in most of the Cases and leading to Additional Costs to the Importers in terms of demurrage, detentions etc. Trade also Expressing Confusion Galore with Customs Officials Hapless.

The Habitual Hungry Hunting Attitude of Officials who have dexterity in practicing Easy Money Making & undue Enrichment with their Policing Mind Set is a Biggest Stumbling Block for Implementing the Well-Intended System, as it seems the Officials are willingly Creating Troubles rather Resolving the issues.

The Customs Brokers (CBs) / Customs House Agents (CHAs) are Not Happy as the Faceless Assessment hitting their Business which they have developed over a period of time & established good Rapport & Understanding with the Local Officials and Smoothened their Operations in Connivence & Collusion with the Local Authorities. Now Vested Interests of both the Customs Brokers as well as Official are hit very hard, therefore naturally there will be Resistance, that is making the System to Fail off course at the Cost & Disadvantage to Trade & Importers.

It will also make a Break of Fraudulent & Fake Operations which are Continuing in the Trade with the Protected Shelter of some unscrupulous Officials at every Local Level of Customs, therefore there are some forces operating to make the New System Fail.

There are also apprehensions that with the RMS (Risk Management System) in place, the practice of routine assessment, concurrent audit and examination of almost all Bills of Entry were discontinued long back and now mostly (80%) Bills Entry are being cleared Automatically without Assessment & Examination and therefore the New Faceless Assessment System doesn’t provide much relief & benefit to the Trade but reflection of Trade is that the New System Creating more Confusion & unnecessary hiccup in the Name of Enabling High Technology.

To make this initiative a success, more & more interactions between Trade & Customs Officials is very much essential with official’s positive & friendly approach for understanding the real issues, analysing feedback on experience of using the system by trade and try to come out with Resolve Attitude rather Defending Mode.

Over a Time in case these new initiatives work well & smoothened, then the Importers may themselves can fill the Bill of Entry & make Customs Clearances without hiring External Third-Party Assistance.

References

1 Circular No. 45/2020-Customs regarding Faceless Assessment – Measures for timely assessment of Bills of Entry and clarification on defacement of physical documents dated 12.10.2020

2. Circular No. 40/2020-Customs regarding All India roll out of Faceless Assessment dated 04.09.2020

3 Public Notice 59/2020 regarding 2nd phase of All India roll-out of Faceless Assessment dated 05.08.2020 (at New Customs House, ACC Delhi)

4 Office Order 19/2020 regarding 2nd phase of All India roll-out of Faceless Assessment dated 03.08.2020 (at ICD TKD)

5 ICES Advisory 25/2020 (Turant Customs) regarding Implementation of Phase II of the Faceless Assessment dated 31.07.2020

6 Standing Order 02/2020 regarding Advisory to the officers of Faceless Assessment Group dated 12.06.2020 (at Bengaluru Customs Zone)

7 Circular No. 28/2020-Customs regarding 1st phase of All India roll-out of Faceless Assessment dated 05.06.2020

8 Instruction No. 09/2020-Customs regarding 1st phase of All India roll-out of Faceless Assessment dated 05.06.2020

9 ICES Advisory 19/2020 (Turant Customs) regarding Rollout of Phase I of Faceless Assessment.

*****

Disclaimer : The views and opinions; thoughts and assumptions; analysis and conclusions expressed in this article are those of the authors and do not necessarily reflect any legal standing.

Author : SN Panigrahi, GST & Foreign Trade Consultant, Practitioner, International Corporate Trainer & Author.

Available for Corporate Trainings & Consultancy Can be reached @ snpanigrahi1963@gmail.com

Author Bio

Sir thanks for a very well explained article.